BUR - Burford's Price In The Heat Of The YPF Trial Suggests Liquidation Value

2023-07-28 09:59:10 ET

Summary

- Burford Capital is the largest litigation finance provider and is currently involved in a damages trial against Argentina over the appropriation of Petersen's stake in YPF.

- The exact damages are being determined this week, with the remaining uncertainty centered around the notice date and pre-judgment interest.

- A reverse valuation suggests investors should be willing to pay at least $16 per share even if Burford were to liquidate its existing franchise.

We believe Burford Capital (BUR) is a strong buy, based on solid downside protection. In this post, we zoom in on the probabilistic minimum price investors should be willing to pay for Burford, while in a future post we may zoom in on fair value.

We take a look at the implied valuation of Burford Capital at the current share price today, as the YPF case damages trial is ongoing this week. Burford is the world's largest litigation finance provider by a wide margin. Litigation finance is a nascent sector, and Burford's founders were instrumental in getting it off the ground in the wake of the financial crisis. The original product that litigation financiers offer to clients is to finance the costs of litigating as a plaintiff in a commercial case. The expenses are drip-fashion, and the pay-off is binary (win/lose) with timing risk. A finance textbook would dictate investors should be willing to get very low returns on these cases as there is almost zero cyclical risk (the counterparty risk when litigating against blue chip companies, Burford's bread & butter), and virtually all risk is idiosyncratic to the case, hence uncorrelated to the economic cycle. Interestingly, Burford has achieved ~30% average IRR's quite consistently over the decades.

Burford's founders have patiently built a one-stop shop for litigation, so today Burford's business can be broken down into a few main pieces:

- Core litigation finance: financing individual cases or portfolio of cases of law firms or companies, using

- Burford's own balance sheet

- External institutional capital (with extraordinary performance fees ranging ~20-50%)

- the "Strategic Value Fund" strategy: a much smaller activity to buy equities with inherent litigation upside. Becoming a shareholder in public companies allows to take control (as opposed to core litigation finance where taking control from the client is usually prohibited by law)

- activities I will call "strategic but ancillary" to provide "one-stop shop" capabilities to clients:

- providing finance (advances) to clients where litigation risk is already off the table (settlement or adjudication occurred) but for some reason the payment has yet to occur

- collecting claims where the adversary is not paying its legal debt

In terms of value per share, one very successful investment in a case against Argentina has to be mentioned, which has the potential to cover Burford's full market cap today.

This post will focus on the downside protection by looking at the value of all these components as if Burford would willingly liquidate the business.

Argentina has been found guilty of appropriating Petersen's stake in YPF without offering a pre-determined price to the previous international investors, as required by the YPF bylaws. The exact damages are being determined this week. Burford bought a piece to this claim out of bankruptcy many years ago.

The remaining uncertainty in the YPF litigation centers around two issues:

- the exact notice date Argentina should've used to offer Petersen a pre-determined price for its YPF shares (the last verdict tells us the uncertainty is bounded to 2 months)

- the pre-judgment interest Argentina should pay on the damages incurred 11 years ago

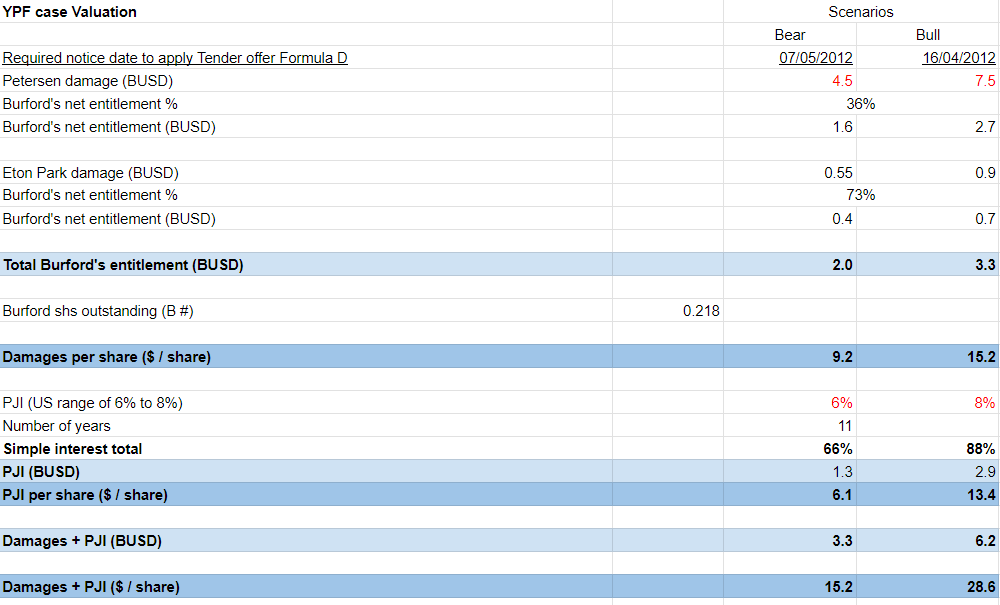

I capture these two uncertainties in a bear and bull scenario. The bear scenario takes the worst possible notice date for Burford investors (May) and a pre-judgment interest on the low side (not what Argentina is asking, at 0%). The bull case takes the best notice date, and a more customary 8% pre-judgment interest.

Author's work based on court documents, Burford's own PR

{kind=link}

Burford has produced evidence showing Argentina officials themselves said as much to have taken control of the YPF shares from Petersen at the bull case date. This is why I believe the bull case date is the most likely outcome.

Regarding pre-interest, it's quite likely it will be in the range of 6% to 8%. Judge discretion for this rate is customary, and perhaps the judge will provide a bit of relief with a 6% rate, as the country Argentina is experiencing hardship right now.

I used Burford's own net entitlement numbers from its own PR following the last verdict determining Argentina guilty. These numbers are approximations, and might vary slightly depending on the outcome.

Regardless, we see the bear and bull scenario yield claims of 15.2$ and 28.6$ per Burford share respectively.

Burford reverse valuation: Valued as if going out of business

Let us proceed to the valuation, or more specifically, a reverse valuation. What does the market imply in Burford's share price today?

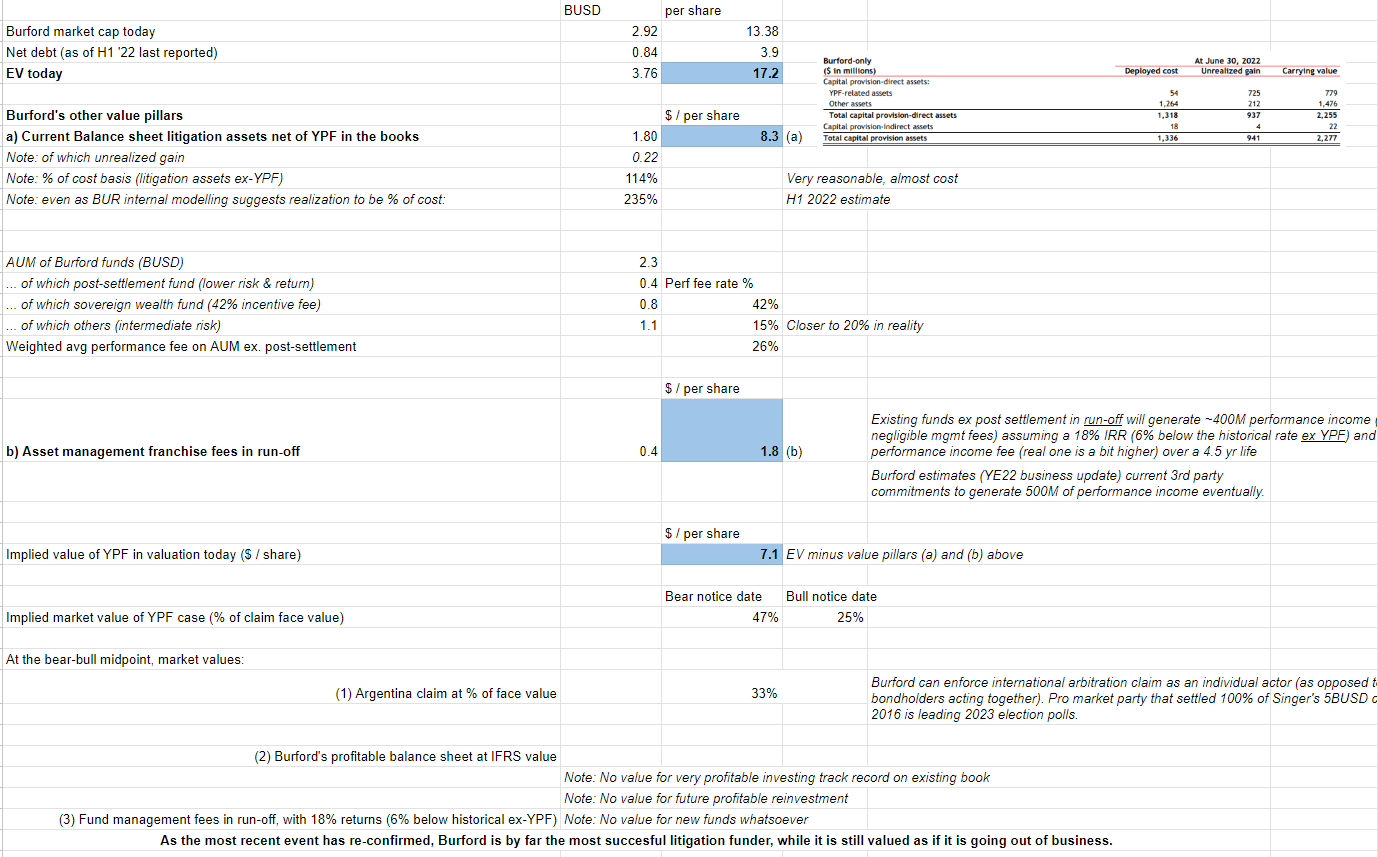

The following table starts of counting Burford's net debt. It is senseless to make statements such as "the value of the YPF covers the market cap" without counting the debt. We can see right away that Burford's enterprise value is fully covered by the headline YPF bull case claim!

Author's own work, using company source documents Author's own work, using company source documents

{kind=link}

Let us weigh the probabilities: what exactly is implied in Burford's enterprise value today?

Follow along in the table above:

We sum up the values as if Burford were to liquidate its (for now very profitable franchise) as the existing litigation assets are wound up.

In (a) we count Burford's litigation assets, excluding the YPF claim, as valued in the books, this yields 8$ per share. Note that only a small part is unrealized gain. You can see these claims are barely valued above cost basis. Note I used Burford's valuation before the recent valuation changes from the collaboration with the SEC.

We will value these claims at 117% of historical cost, even though internal Burford probabilistic modelling (from investor presentations) would tell us the most likely outcome is 235% of cost. This latter number is very much in line with Burford's historical performance. Doubters have raised doubts about the sustainability of these returns in the last 5 years, but the returns of closed cases has remained in line with historical performance.

Next we value the asset management fees to come in (b) in run-off. Assuming a 18% IRR (6 percentage points below historical performance ex YPF) and a weighted 26% performance income fee (part of Burford's AUM has 50% performance fees), we get 400 MUSD of fees, or $1.8 per share.

Remember we are being very punitive, valuing the existing litigation assets at cost, much below historical performance.

Deducting (a) and (b) from the EV, we get $7.1 per share of implied valuation for the YPF claims. This means the market is valuing the Argentina claims at 47% of face value for the bear case, and 25% of face value for the bull case.

At the mid-point between bear and bull case, the market values the claim at 33% of face value.

Multiple people more knowledgeable than me about pursuing damages attribute a present value at 50% of the YPF claim, see here for example. The balance of power is that Burford can make Argentina's politicians life difficult (and lose face) with asset freezing levers, while Argentina knows it is in Burford's best interest to get money sooner than later, given Burford's high cost of capital. The Argentina election polls seem to be turning very "pro-business", and the settlement will probably feature as a big part of a larger Argentina settlement with its creditors. For reference, see what happened with the election of Macri in 2015.

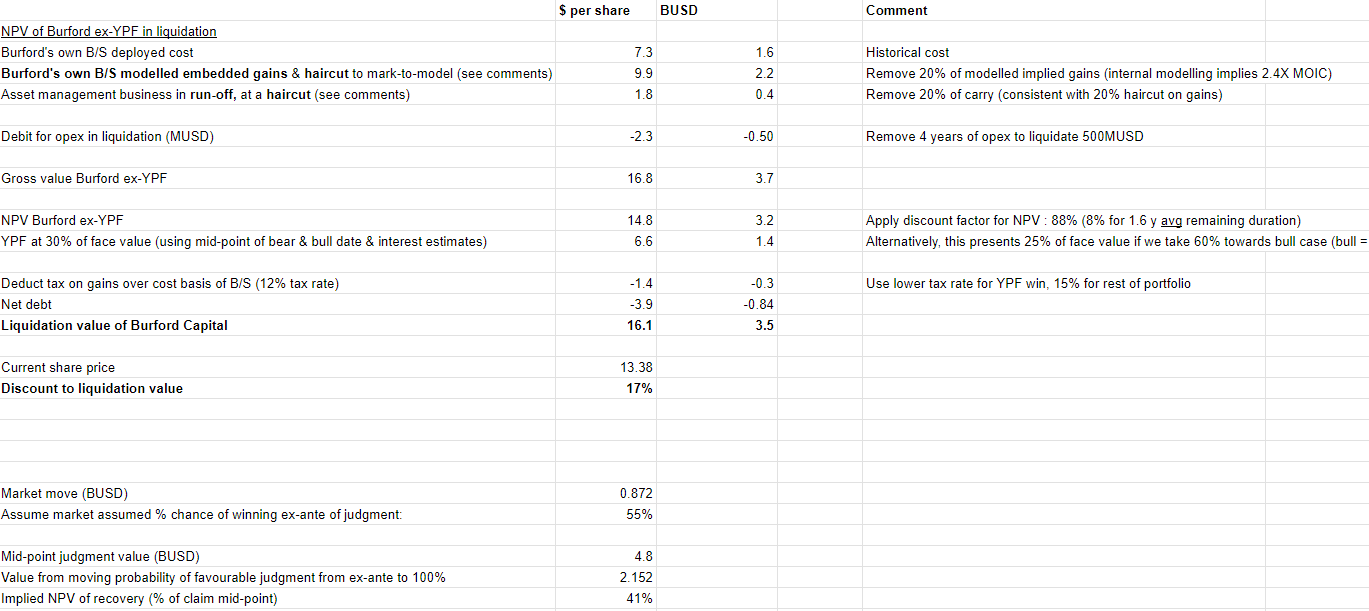

An alternative reverse valuation I made goes as follows. Instead of using the hyper-conservative historical cost for the other litigation assets, one underwrites a 20% haircut to the current litigation assets as valued by Burford internally (and shared in investor presentations). We deduct management opex to allow for liquidation (we use 2.5 years of opex). We value YPF at 30% of face value (conservative). In this exercise, we still get a liquidation value for Burford of $16.1 per share.

Author's own work, based on company documents.

{kind=link}

What I tried to do in the latter part of the last table is estimate the market's own implied value as a % of YPF claim face value by looking at the price move when Argentina was found guilty, and assuming the market was assigning a probability of this outcome of 55% before the outcome. The incremental face value of (100% - 55%) x 4.8BUSD mid-point of damages, or 2.1B. However, the market move in BUR was only $4 a share before stabilizing around $13, or 0.87B. This implies the market is valuing the Argentina claim at around 41%.

If I were to plug 41% into this latest table (instead of 30%), the liquidation value becomes $18.4 per share (for a 27% discount to liquidation value).

All of this I think is an exercise in caution. As Burford's track record - including the recent events - shows, the company returns are great and not deteriorating. As confirmed on the last earnings call by CIO Molot: after opex, Burford's ROE should be around 20% on average, as it has been historically, and Burford is growing quickly. Burford could become the one-stop-shop franchise similar to Blackstone 10 to 20 years ago, but for a nascent asset class instead. Remember a lot of institutional AUM needs name recognition, as the allocators want to play safe and avoid losing their job. Private equity, including Burford, enjoys a sort of premium similar to the luxury industry.

What I tried to show in this post is my personal "lower boundary" estimate of Burford's value before the trial outcome. A true lower boundary for Burford is $16 per share in my opinion. If Burford were to liquidate (an absurd scenario given its historical returns and the recent stability thereof), investors should still be willing to pay $16.

This explains why Burford is now my second biggest position and I have not sold a share since the recent move up.

Risks

Even though I believe I would take the Burford bet any day on a probabilistic basis, there is obviously event risk from the damages and payment outcome in the case against Argentina. Despite looking at quite a few expert sources available publicly, I could also be wrong on the case valuation as a percentage of face value.

Another risk of note is the lumpy quarterly results due to timing risk: Burford does not provide guidance as it is impossible to predict when cases will resolve (despite the fact the average maturity of cases have remained around 2-3 years). Covid-19 brought a drought of resolutions because of delays. However, these delays accrue to the total returns when the cases do resolve: litigation finance contracts often have a payout formula to the financier which is the maximum between a fixed percentage of the award and an IRR. This is part of the near-term bull case I could explain in a next post.

Burford is also a complex company to analyze, and this brings volatility at times. I have followed the company and read every single shareholder letter since IPO, which I highly recommend. However, the previous share price crash following the - in my opinion, at best incompetent and at worst misleading Muddy Waters report - suggests that many public investors do not seem to share the same understanding. This post is not a recommendation and for entertainment purposes only. Please do your own work first, as the history of Burford shows that many less informed investors have changed sentiment at the worst possible times in the past.

For further details see:

Burford's Price In The Heat Of The YPF Trial Suggests Liquidation Value