BFI - BurgerFi: Good Burgers Unproven Financials

Summary

- BurgerFi makes a good burger, and has seen a year of significant revenue growth in line with its recent acquisition of Anthony's Coal Fired Pizza & Wings.

- Yet, the company has saddled itself with significant debt and is not generating robust cash flows from its operations.

- This has created a record low level of negative retained earnings.

- Additionally, a slowdown in revenue growth makes the overall financial picture inspire caution.

- As such, the company is worth paying attention to long term but not investing in until financial performance improves.

Overview

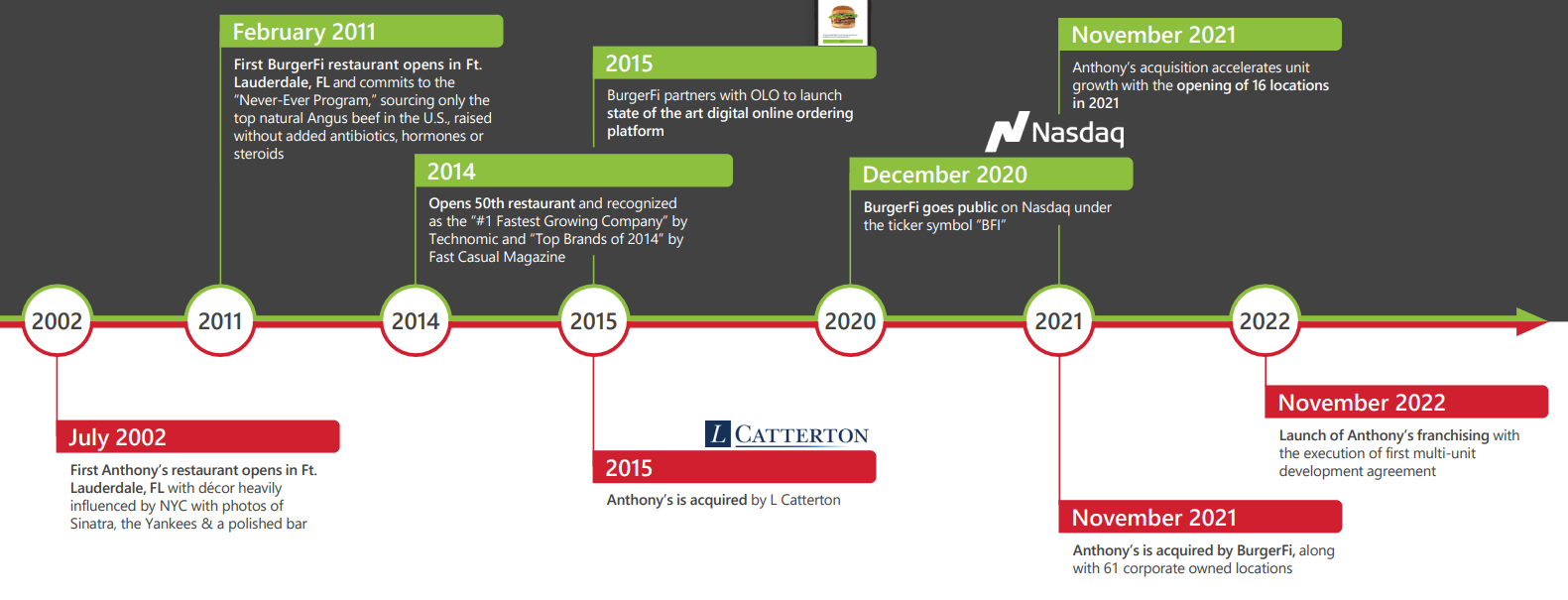

BurgerFi International ( BFI ) is an upstart fast-casual burger restaurant chain. It is not yet international in its footprint and operates exclusively in the United States. The company operates two brands – BurgerFi and Anthony’s Coal Fired Pizza & Wings – through both direct ownership as well as franchising.

First opening a location in 2011, BurgerFi has seen continued growth as well as a public listing in December 2020. The company subsequently acquired Anthony’s Pizza and has continued to trade as a joint entity since.

BFI Investor Presentation Q1 2023

{kind=link}

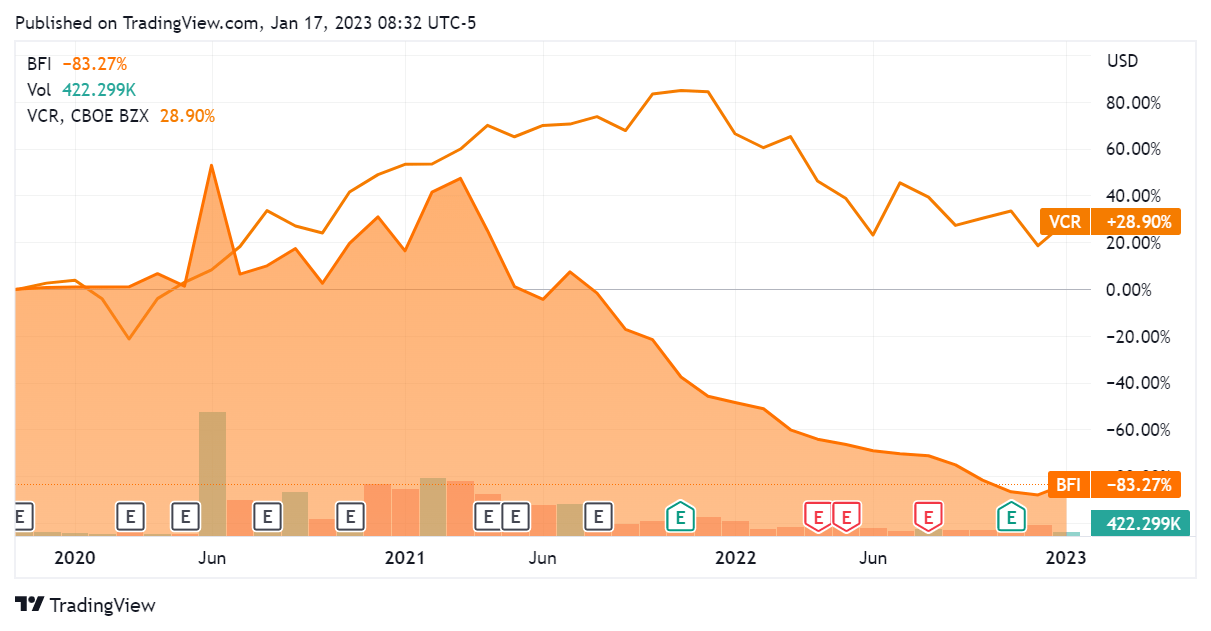

The stock has depreciated significantly since the company’s IPO, presently trading at $1.75 as of this article. Notably the security has also underperformed the consumer discretionary sector as a whole (sector returns indexed by the Vanguard Consumer Discretionary Index, VCR), returning -83.3% versus 28.9% for the sector since Q4 2020.

{kind=link}

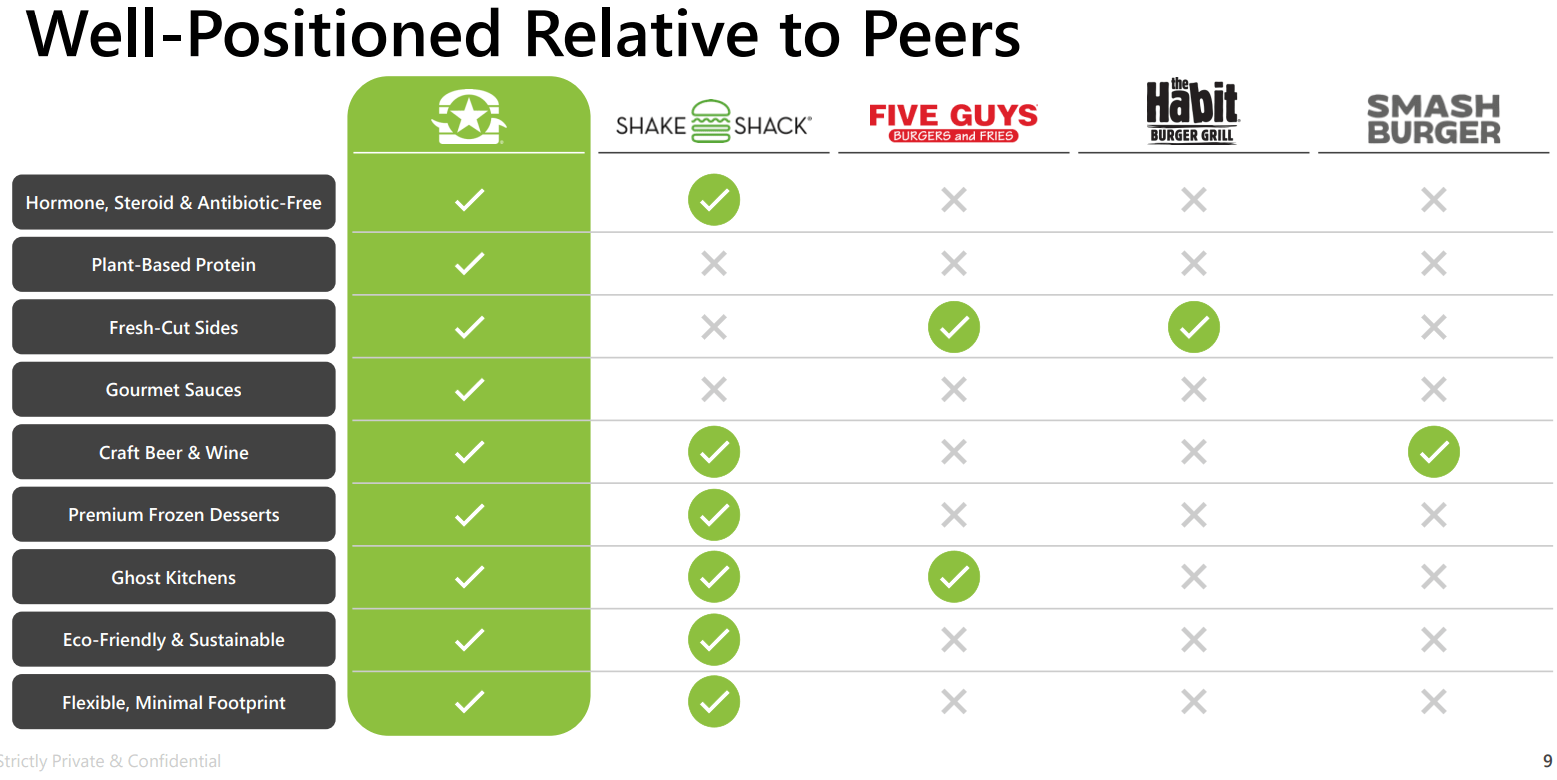

Having eaten at a BurgerFi restaurant last week, I was pleasantly surprised by both the food as well as the fact that it is a tradeable security. I believe that it’s fair to consider this a ‘fast casual’ offering as opposed to just fast food. The décor as well as the quality of the meat make this chain more readily comparable to a Chipotle as opposed to a McDonald’s in terms of both pricing and quality.

The menu has antibiotic and hormone-free meat across the board, driving the 'fast casual' nature of this business home; other menu elements, such as beer on tap, also serve to place this chain squarely in that bracket from my perspective. The standard double burger, fries, and drink set me back about $15 and change in Brooklyn, New York; not the cheapest burger, but certainly priced competitively in line with its peers and competitors. This article will review the firm's financial picture and determine if this company presents an investment opportunity.

BFI Investor Presentation Q1 2023

{kind=link}

Financials

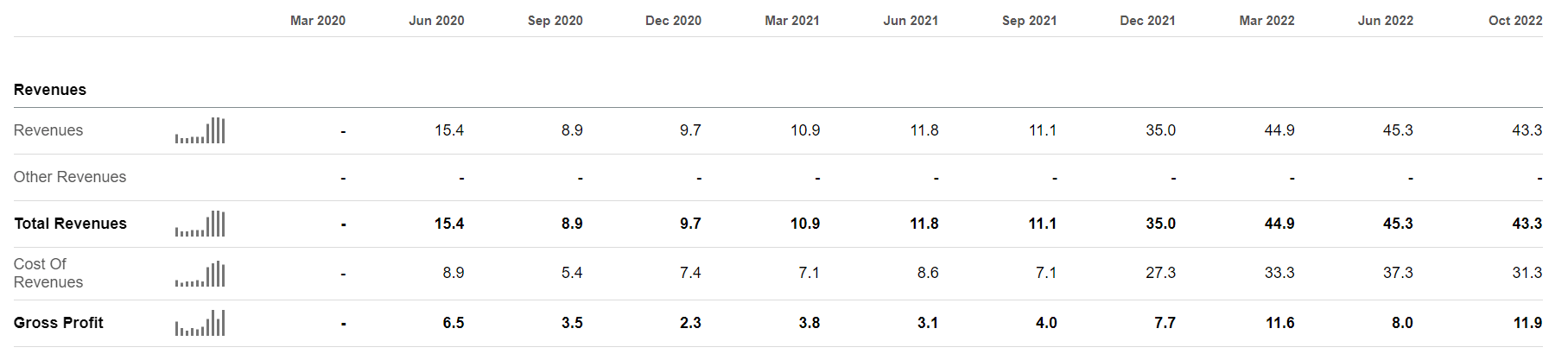

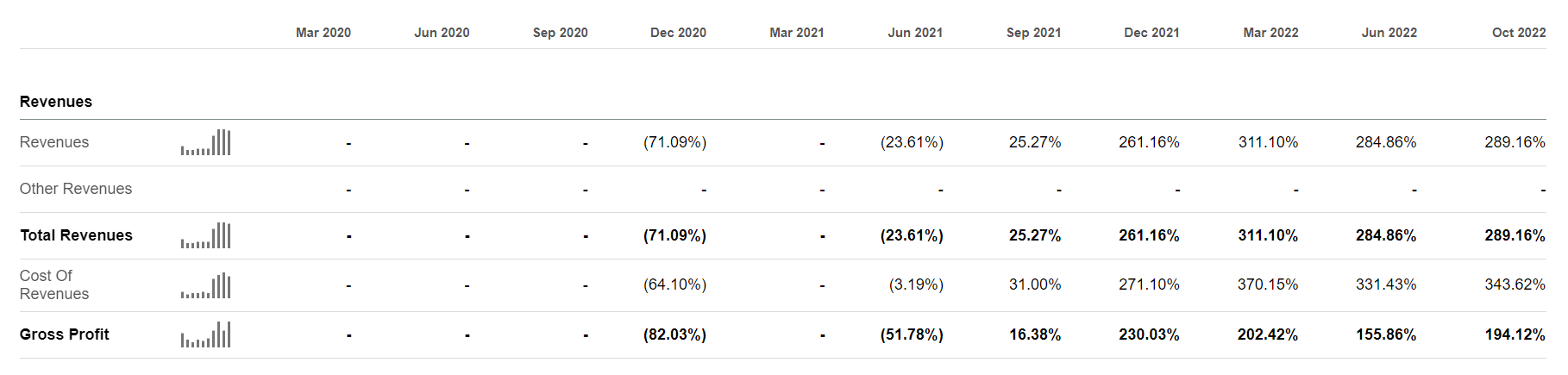

Beginning with the top-line numbers, we see that BurgerFi initially had its momentum clipped by the pandemic but has since reclaimed significant growth in terms of revenues. In line with its acquisition of Anthony’s Pizza, the company has posted a banner year between Q3 2021 and Q3 2022, with triple digit YoY revenue growth for 4 quarters running. While it will be interesting to see the results for Q4 2022 as well as the year-end totals, the overall trendline here is clear.

However, revenue growth did appear to stall in Q3 2022, with the numbers for that quarter coming in slightly lower than they were for Q2 2022. This was a miss as to consensus expectations. While this trend will certainly come into clearer focus with the full-year numbers for 2022, the latest report at least demonstrated a record quarterly gross profit along with the slightly lower revenue number. Company management chalked this up to the effects of hurricane Ian and its effects on the west coast of Florida, where the company has a significant presence; I think this is credible. Overall, I am cautious to be overly optimistic or pessimistic about the direction that revenues are headed with the data that we have on hand.

BFI SeekingAlpha.com 1.17.22 BFI SeekingAlpha.com 1.17.22

{kind=link}

{kind=link}

Going further on the income statement, we see that BurgerFi is still very much an early-stage company and is not yet consistently profitable. While the company was able to post a small positive net income prior to its acquisition, it sustained a significant ‘non-cash impairment charge’ of $115M to its net income, owing to its acquisition of Anthony’s. This is essentially a one-off depreciation of assets acquired and should not impact earnings going further. Since then, the company has not yet reclaimed profitability but may very well do so next quarter.

{kind=link}

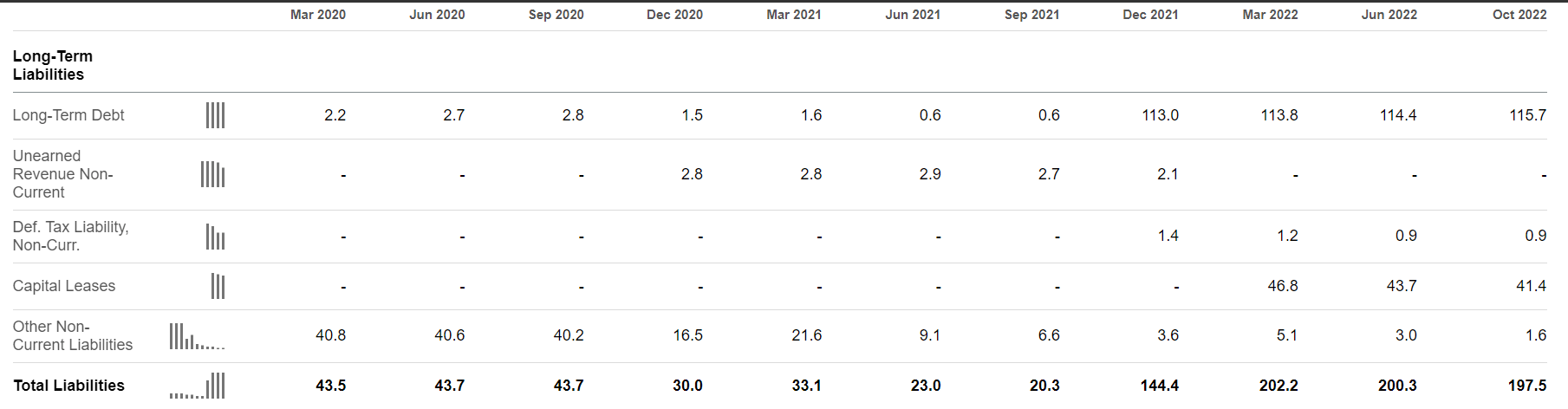

The acquisition also had a material impact on the balance sheet, with long-term debt ballooning to $113M in Q4 2021 and growing somewhat to $115.7M as of the end of Q3 2022. Present liabilities grew as well, and BurgerFi is now operating with a significantly larger overall liability footprint.

{kind=link}

This has created an ongoing interest expense of $2.2M for the firm, which is a manageable proportion of its revenues. Nonetheless it will take some time for this company to pay down this debt, with increasingly negative retained earnings showing just how far the firm has to go - $201M just to get back to 0. This is a significant burden the company has placed on its valuation due to growth.

BFI SeekingAlpha.com 1.17.22 BFI SeekingAlpha.com 1.17.22

{kind=link}

{kind=link}

Looking at cash flows, the picture is frankly not the best. We see that BurgerFi’s cash from operations fluctuates around 0 and was negative for most quarters, including the most recent one. This doesn’t represent an operating picture that gives me comfort giving the company’s debt and significant negative retained earnings; it will have to ‘beef up’ these numbers significantly to get to a non-negative fundamental valuation.

{kind=link}

The overall cash situation doesn’t seem to have a clear trendline, but this is a company that generally loses cash overall.

{kind=link}

Overall these financials indicate that BurgerFi has taken on significant liabilities in order to grow and has not generated sustainable cash flows.

Conclusion

BurgerFi makes a good burger. Yet, the financial picture here is simply not investment-grade as of yet. Record levels of debt, weakening revenue growth, poor cash flows, and the numbers from the recent acquisition make me hesitant to enter this stock. While undoubtedly cheap on a sales basis, this company is too early-stage to readily compare it to its more built-out industry peers.

If there was a strong record of operating cash flows then the story would be different – but there isn’t as of yet. While I believe the offering in question here is a quality one and may very well see continued traction, I think investors should exercise caution at this stage and will rate this a hold for the time being.

{kind=link}

For further details see:

BurgerFi: Good Burgers, Unproven Financials