BOOT - Burlington Stores Q1 2023 Earnings Preview: Approaching The Business Cautiously Heading Into Earnings

2023-05-19 08:34:43 ET

Summary

- Burlington Stores' shares have generated an upside of 16.4% in the past year, outperforming the S&P 500's 6.5% increase.

- The company's 2022 revenue declined 6.6% compared to 2021, with net income dropping almost half to $230.1 million.

- Burlington Stores is expected to see revenue growth of 12% to 14% in 2023, but market uncertainty and a lofty valuation has pushed me to downgrade it.

For the most part, I don't care to buy shares in retailers. High levels of competition, low margins, volatility during uncertain economic times, and being subjected to the whims of consumers, is not a combination that I care to deal with. But every so often, I find myself a retail prospect that I can be bullish about. Last year I did exactly that when I analyzed Burlington Stores (BURL). Given how the company had performed leading up to that point, and because of how shares were priced, I ended up taking a bullish stance on the firm. However, that picture has changed some since then. And on top of that, the company has experienced a nice bit of upside. The good news for investors is that management is slated to report financial results for the first quarter of the company's 2023 fiscal year in the next few days. If the picture changes, I could become bullish on the company again. But for now, I've decided to downgrade the company from a 'buy' to a 'hold'.

Less enthusiastic now

As I mentioned already, I found myself taking a bullish stance on Burlington Stores when I wrote about the company last year. In fact, that article came out almost exactly a year ago, on May 24th. In that article, I talked about how well the company had done from a growth perspective over the prior few years. It achieved this with virtually no online sales, which is definitely peculiar in this modern era. At the time, shares of the company were pricey compared to similar firms. But the attractive growth of the business, and the fact that shares looked reasonably priced on an absolute basis, led me to rate the business a 'buy'. Since then, things have gone as well as I could have expected. While the S&P 500 is up 6.5%, shares of Burlington Stores have generated upside of 16.4%.

{kind=link}

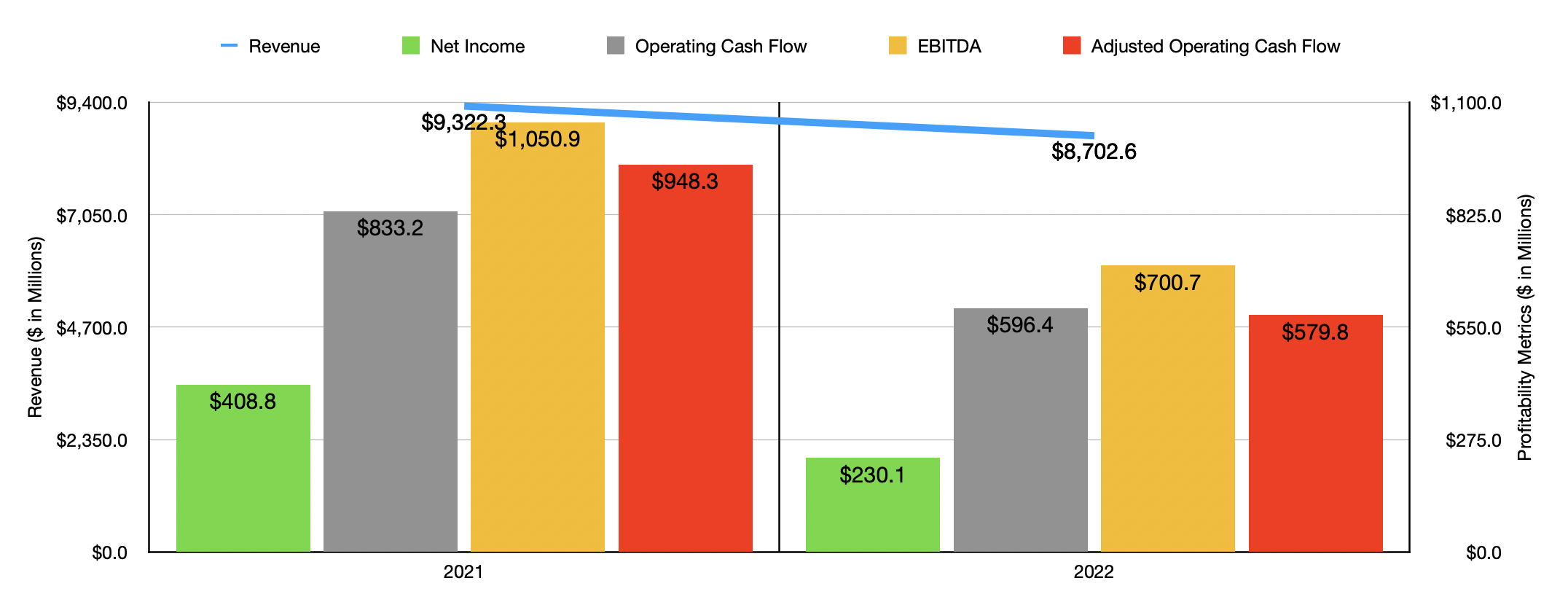

This move higher has come about at a time when the company has generated some rather depressing results. Consider how the company performed in 2022 compared to 2021. In 2022, overall revenue for the business came in at $8.70 billion. That represents a decline of 6.6% compared to the $9.32 billion the business generated in 2021. Interestingly, this sales decrease came even at a time when the company added to the number of locations that it has in operation. By the end of last year, the company had 927 stores. This was 87 more than the 840 that it had at the end of 2021. The key driver behind the weakness on the top line, then, was soft demand that resulted in comparable store sales plunging 13%.

As you can imagine, profits and cash flows followed revenue lower. Net income, for instance, totaled $230.1 million in 2022. This was down almost half compared to the $408.8 million generated in 2021. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, plunged from $833.2 million to $596.4 million. If we adjust for changes in working capital, the picture was even worse, with the metric declining from $948.3 million to $579.8 million. Meanwhile, EBITDA for the business fell from $1.05 billion to $700.7 million. This makes sense when you consider that, not only did the company have lower revenue, but also that the large amount of assets required in order for the company to operate means that a reduction in sales translates to a disproportional contraction on the bottom line because of the same fixed costs having to be distributed across a lower sales base.

Although the results for the company for 2022 were disappointing, management remains optimistic about 2023. For the year as a whole, the company is expecting revenue growth of between 12% and 14%. That's actually excluding an extra 2% that should be attributable to the fact that it has an extra week of operations this year compared to last year. Much of this growth should be driven by the addition of between 70 and 80 new stores. However, the company does also expect comparable store sales to grow by between 3% and 5% as demand recovers. This would be great since the company does have a bit of an inventory glut at the moment. Overall inventories at the end of 2022 totaled $1.18 billion. That was 15.8% above the $1.02 billion the company had in 2021.

On the bottom line, management expects earnings per share to be between $5.50 and $6. $0.05 per share of this should be attributable to the extra week that the company should enjoy. Striping that out and looking at the midpoint, we would expect overall profits for the business to come in at $370.5 million for the year. The company is also expecting EBIT margin expansion of about 1%. Assuming that depreciation and amortization remains flat compared to what it was last year and if we adjust to remove the extra week of operating results, this would imply EBITDA for 2023 of around $852.5 million. Based on my own estimates, this should result in adjusted operating cash flow of around $705.4 million.

{kind=link}

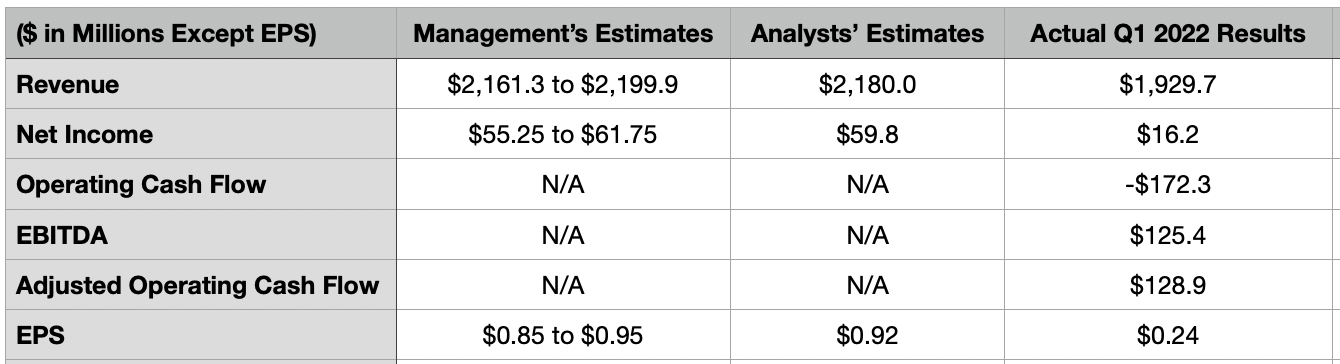

Focusing on the year as a whole may be problematic because of uncertain economic conditions. Having said that, the company will be reporting financial results covering the first quarter of the 2023 fiscal year before the market opens on May 25th. The great thing about this is that the new data should give investors and opportunity to reevaluate how things are going. At present, analysts think that revenue will come in at around $2.18 billion. If this does come to fruition, it would translate to a 13% increase over the $1.93 billion the company reported one year earlier. Management also provided guidance, with comparable store sales growth of 5% to 7% pushing overall revenue up by between 12% and 14% for the quarter.

On the bottom line, analysts believe that the company will generate a profit per share of $0.92, with adjusted profits of $0.93. This would represent a significant improvement over the $0.24 per share that the company generated last year, earnings that translated to a net profit for the quarter of $16.2 million. For context, management believes that earnings per share will be between $0.85 and $0.95. No guidance was given when it came to other profitability metrics. However, for context, operating cash flow in the first quarter was negative to the tune of $172.3 million. If we adjust for changes in working capital, we would get a reading of $128.9 million. And finally, EBITDA came in at $125.4 million.

{kind=link}

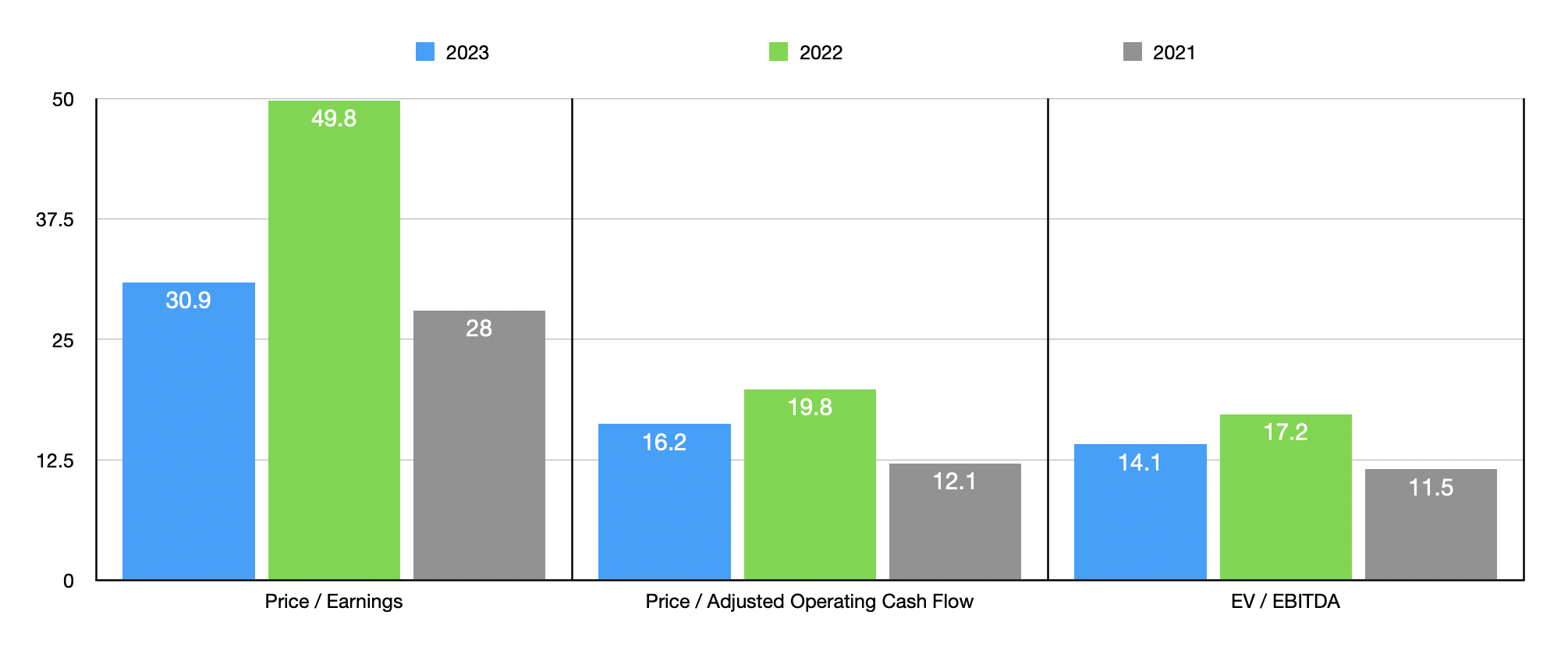

Unless management can come through with results and guidance that exceed what is expected, I do think that it's appropriate at this time to downgrade the company from a 'buy' to a 'hold'. I say this based on how shares are priced on a forward basis. As you can see in the chart above, I priced the company using results from 2021 and 2022, as well as using estimates for 2023. On a price to earnings basis, the forward multiple for the company is a rather lofty 30.9. The price to adjusted operating cash flow multiple is 16.2, while the EV to EBITDA multiple is 14.1. In the table below, you can see how shares are priced compared to five similar firms. On a price to earnings basis, four of the five prospects are cheaper than Burlington Stores. Using the price to operating cash flow approach, only two of the companies are cheaper. But when it comes to the EV to EBITDA approach, all five firms were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Burlington Stores |

| 30.9 |

| 16.2 |

| 14.1 |

| The Gap ( GPS ) |

| 81.7 |

| 4.9 |

| 7.1 |

| Aritzia (ATZAF) |

| 22.9 |

| 57.1 |

| 9.3 |

| Foot Locker ( FL ) |

| 11.6 |

| 22.9 |

| 5.1 |

| American Eagle Outfitters ( AEO ) |

| 21.6 |

| 6.5 |

| 5.1 |

| Boot Barn Holdings ( BOOT ) |

| 12.0 |

| 108.2 |

| 8.5 |

Takeaway

Financially speaking, Burlington Stores is doing better after what was definitely a difficult year for it. So far, investors seem happy with the results. This year should definitely be better, barring something unexpected occurring. But this doesn't necessarily mean that now is a good time to buy in. I suspect that, in the long run, Burlington Stores will do just fine. But given the uncertainty in the market, combined with what other opportunities exist out there, I do believe that a modest downgrade is appropriate at this time.

For further details see:

Burlington Stores Q1 2023 Earnings Preview: Approaching The Business Cautiously Heading Into Earnings