WPC - Buy Alert: 3 Blue Chip High Yield REITs To Buy On The Dip

2023-05-23 07:00:00 ET

Summary

- REITs have sold off lately.

- We believe there are a number of increasingly attractive opportunities in the sector.

- We share three blue chip high yield REITs to buy on the dip.

REITs ( VNQ ) have sold off quite a bit lately:

As a result, we believe there are a number of increasingly attractive opportunities in the sector to put capital to work. In fact, the sell-off has gotten so bad that there are quite a few blue chip REITs with impressive track records that offer attractive dividend yields backed by payouts that should only continue to grow moving forward. In this article, we discuss three blue chip high yield REITs to buy on the dip.

#1. W. P. Carey ( WPC ) Stock

WPC is a very attractively priced REIT that should enable investors to rake in high current income while sleeping well at night. Thanks to the stock declining by nearly 20% since late January, it is now on sale:

Despite recently completing its transition to being a recession-resistant pureplay triple net lease REIT, proving its mettle as arguably the best performing triple net lease REIT during COVID-19, earning a credit rating upgrade from BBB to BBB+ from S&P, and continuously increasing its allocation to industrial real estate while decreasing its percentage allocation to office and retail, WPC's stock currently sits at a steep discount to several historical valuation metric averages.

On an EV/EBITDA basis it sits at 15.35x compared to its five year average of 17.9x, on a P/AFFO basis it sits at a mere 12.69x compared to its five year average of 14.84x, and on a dividend yield basis it offers an attractive 6.26% yield compared to its five year average of 5.64%.

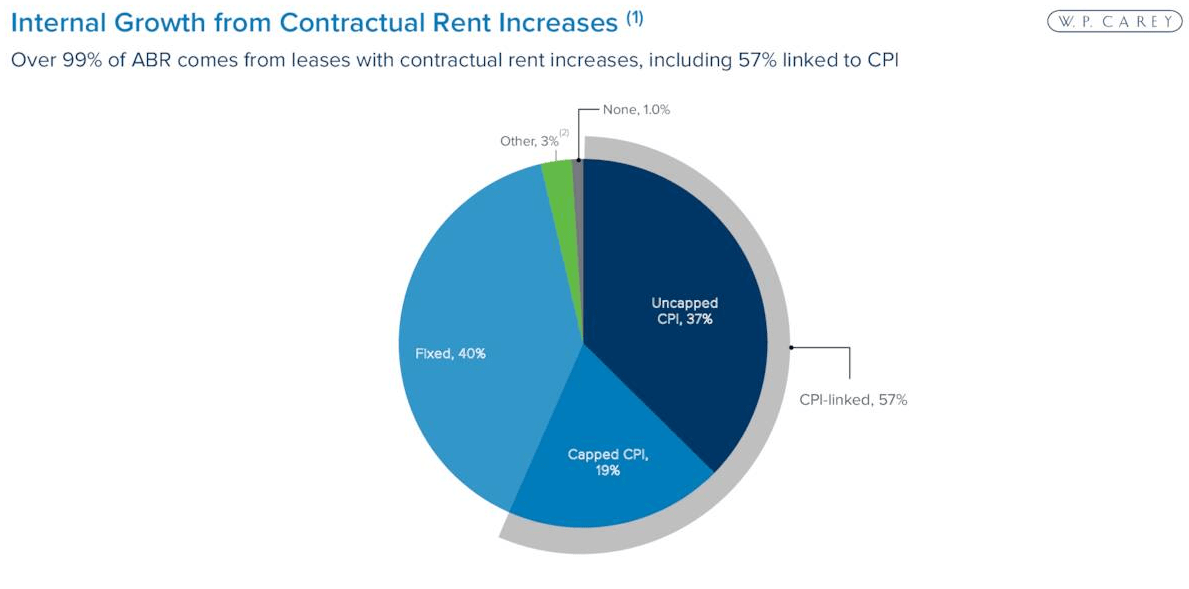

Moreover, it offers some of the best inflation protection in the triple net lease space, with 57% of its ABR linked to CPI and over 99% of its ABR coming from contractual rent increases. As a result, it generates robust and very consistent organic growth.

{kind=link}

On top of that, it is enjoying substantial acquisition momentum, as the recent pullback in commercial real estate lending from regional banks ( KRE ) has increased demand for the sale-leaseback product that WPC specializes in. In summary, WPC offers investors a:

- strong balance sheet

- very safe and attractive dividend

- roughly quarter century dividend growth streak

- well-diversified and conservatively positioned high quality real estate portfolio

- recession resistance and organic inflation protections

- positive growth environment

- clearly discounted valuation

As a result, we rate it a Strong Buy and think it is an excellent pick for risk-averse, income-oriented investors who also want to achieve double-digit annualized total returns over the long-term.

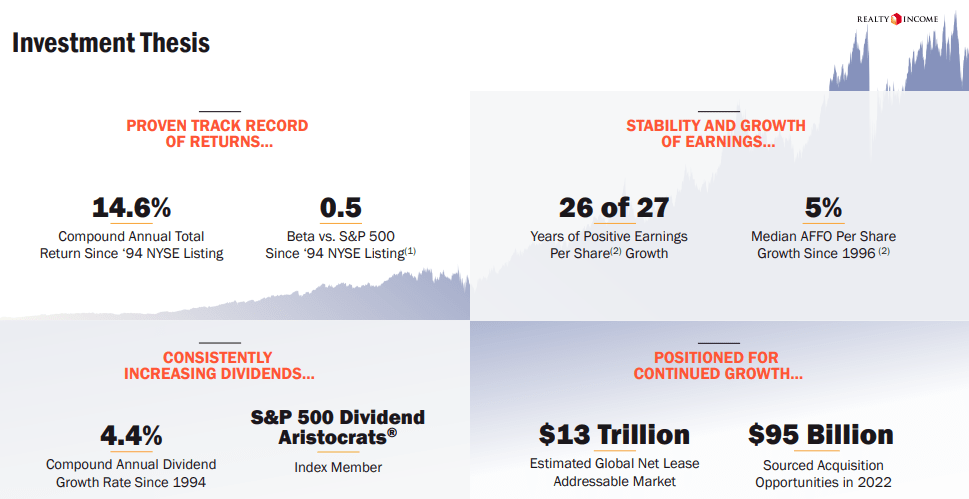

#2. Realty Income ( O ) Stock

O is similar to WPC in many ways in that it offers investors a:

- stellar balance sheet (A- credit rating)

- very safe and attractive dividend

- in impressive dividend growth streak (every year since going public in 1994)

- the largest real estate portfolio in the triple net lease sector with high exposure to investment grade tenants

- proven recession resistance and steady organic growth through contractual rent escalators

- positive growth tailwinds from the recent banking crisis

While it lacks the same amount of inflation protection as WPC, its track record is second to none in the triple net lease sector and is arguably as good as anyone's in the entire REIT space:

{kind=link}

Nicknamed "The Monthly Dividend Company," O is the quintessential passive income stock given its extremely reliable and steadily growing monthly dividends that it sends to shareholders.

Moreover, investors can now buy it at a discount to its historical valuation multiple averages. Its EV/EBITDA ratio is 16.26x compared to its five year average of 19.38x, its price to AFFO ratio is 14.88x compared to its five year average of 18.50x, and its dividend yield is 5.14% compared to its five year average of 4.37%.

As a result, we rate it a Buy and believe that now could be a good time to lock in a very reliable and attractive income stream by buying the dip:

#3. Simon Property Group ( SPG ) Stock

Last, but not least, SPG is the world's leading publicly traded mall landlord. In a period of time where virtually all other publicly traded mall landlords either went bankrupt or were taken private, SPG has continued to stand tall, relatively unflinchingly. By way of comparison, it has soundly beaten the total return performance of the only other remaining publicly traded mall/outlet landlords (Tanger Factory Outlet ( SKT ) and Macerich ( MAC )) over the past decade:

Moreover, its balance sheet remains in excellent shape, with an A- (stable outlook) credit rating from S&P and an equivalent rating from Moody's. It also has substantial wiggle room relative to its debt covenants, meaning that it is well prepared to take on a recession:

SPG Balance Sheet (Investor Presentation)

Last, but not least, the stock price looks very attractive right now after declining by nearly 20% since the beginning of February:

The EV/EBITDA is attractive at 15.09x compared to its five year average of 16.41x, the price to AFFO ratio is only 9.7x compared to its five year average of 12.32x, and its dividend yield is 7.09% compared to its five year average of 6.05%.

Moreover, thanks to its strong balance sheet and the fact that most of its weakest tenants and many of its competitor malls have already been weeded out through the retail apocalypse of the past half decade, it is well positioned to weather a recession as well.

As a result, we rate it a Strong Buy and think it provides investors a compelling opportunity to lock in a well-covered 7.1% dividend yield (a 68% expected 2023 AFFO payout ratio), that will likely continue growing at a low to mid single digit CAGR moving forward.

Investor Takeaway

Thanks to the sell-off in the REIT sector over the past several months, investors can latch on to several compelling high yield blue chip bargains. While a recession may hurt some REITs and the troubles afflicting office REITs like Boston Properties ( BXP ) are scaring many away from all commercial real estate, opportunistic value investors can now take advantage of overblown market pessimism on REITs by buying low risk, high yield stocks like WPC, O, SPG.

For further details see:

Buy Alert: 3 Blue Chip High Yield REITs To Buy On The Dip