CAT - Buy Caterpillar's Recent Breakout

2023-06-27 07:14:49 ET

Summary

- Caterpillar recently broke out of a triangle pattern.

- CAT stock has pulled back, and is likely close to the point where it turns higher again.

- The valuation is cheap enough, and pricing increases are likely sticky enough for sustained margin gains.

With prolonged talk of recession so far in 2023, and the otherworldly start to the year that tech has shown, you'll excuse investors for eschewing industrial stocks of various kinds. However, there are some that appear to be in good shape both from technical and fundamental perspective.

The last time I visited yellow-clad digging machine legend Caterpillar ( CAT ), the stock was on the verge of a breakdown. It did move lower, but has soared in the months since it bottomed last September. Is there more where that came from? I think there's a pretty good chance of that, but it's not a slam dunk.

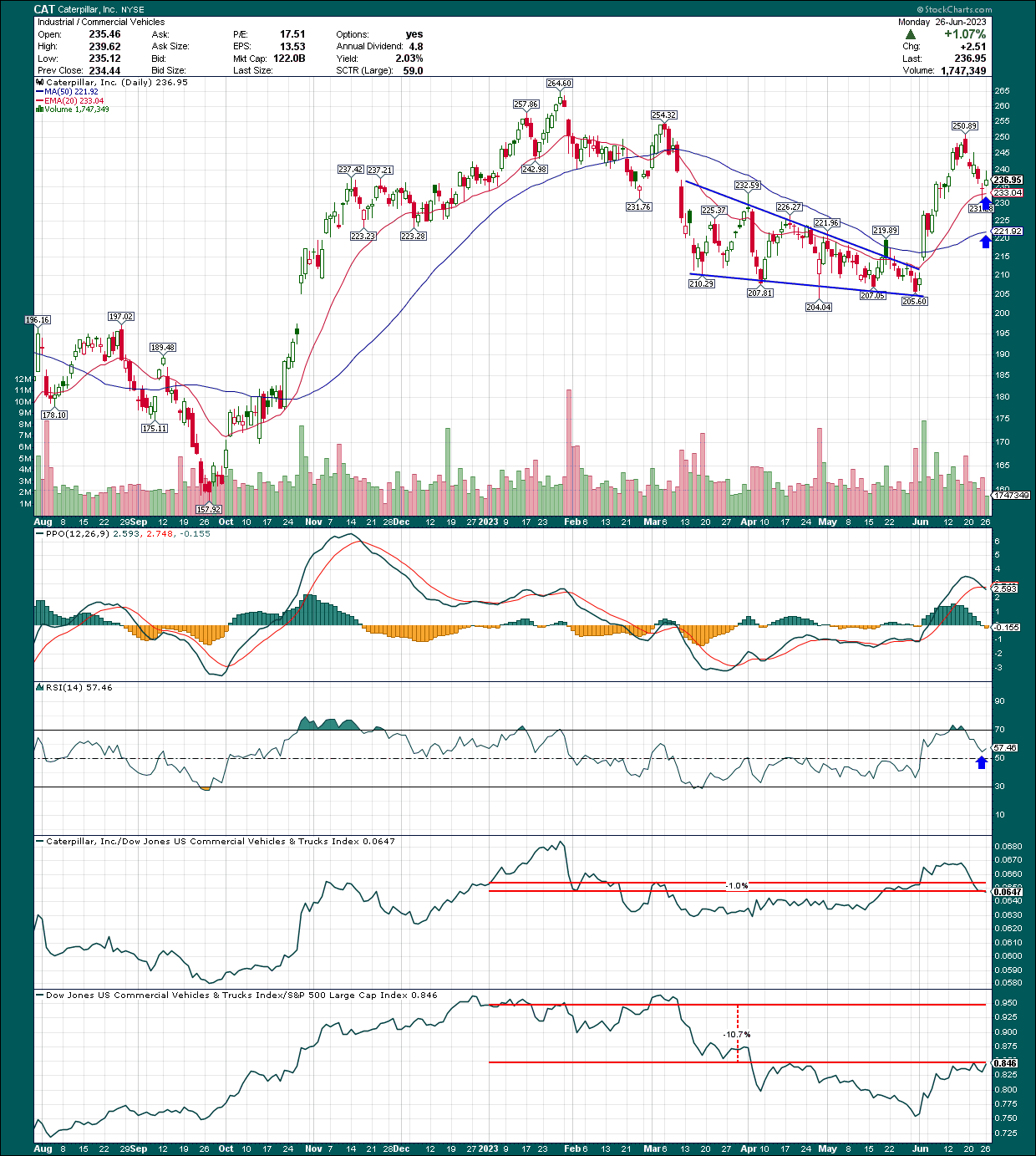

A big breakout, but the retest is critical

Let's start with the price chart, which shows a big breakout (and bigger rally) out of a wedge formation, as seen below.

{kind=link}

The breakout point was about $210, and we'll generally see the price test the breakout point when a formation is busted like this one. However, I'm not sure we're going to see a price that low here. The stock closed right on the 20-day exponential moving average on Monday, and the 50-day simple moving average is looming below at $222. Both are rising sharply, which is indicative of bull market behavior, and I would be surprised to see the 50-day SMA fail. The 20-day EMA just might given the stock's momentum hasn't fully reset yet - as evidenced by the PPO and 14-day RSI - but either way, I don't think there's a huge amount of downside potential from here.

Relative strength has been, well, weak this year, with the stock about flat to the peer group, but off about 11% to the S&P 500. That's a mark against Caterpillar from a technical perspective, but I otherwise think this one looks reasonably bullish.

Tailwinds abound

Let's start the fundamental conversation with a look at the analyst community's bullishness, which literally could not be higher.

{kind=link}

All 37 revisions in the past three months have been higher. Not much to say here other than there's a huge amount of optimism from analysts at the moment, and it doesn't get better than this.

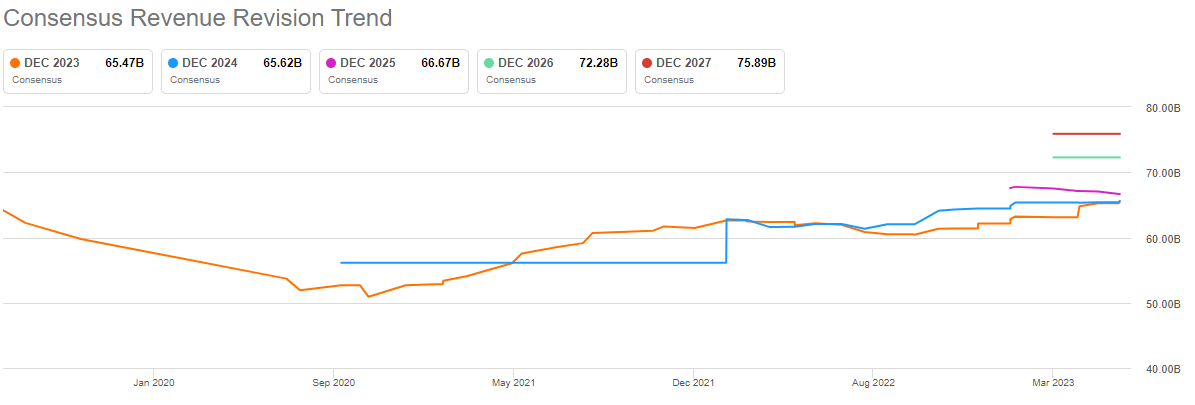

Now, let's take a deeper look at revenue and EPS estimates, starting with the top line. We can see the revisions here have been gradual, and relatively small. Caterpillar's volumes aren't exactly flying, but that's okay because the company's been able to boost prices extremely effectively in recent quarters.

{kind=link}

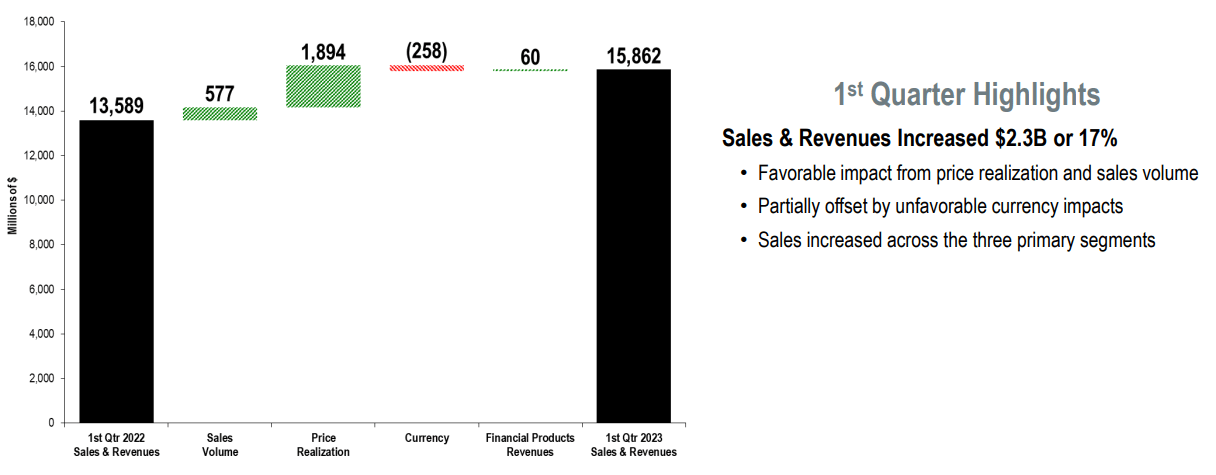

That's led to the gradual slope we see above for top line estimates, and below, we can see just how impactful those price increases have been. The below is the most recent quarter infographic, which is a terrific example of just how meaningful raising prices effectively can be.

{kind=link}

Caterpillar added $1.9 billion to the top line in the first quarter from price realization, with volumes adding less than a third of that in addition. Now, pricing increases cannot go on forever, and there will be a time, likely in the near future, that pricing increases will stop being a source of comparable revenue gains. However, these gains have had what could be a lasting impact on the company's margin profile as well.

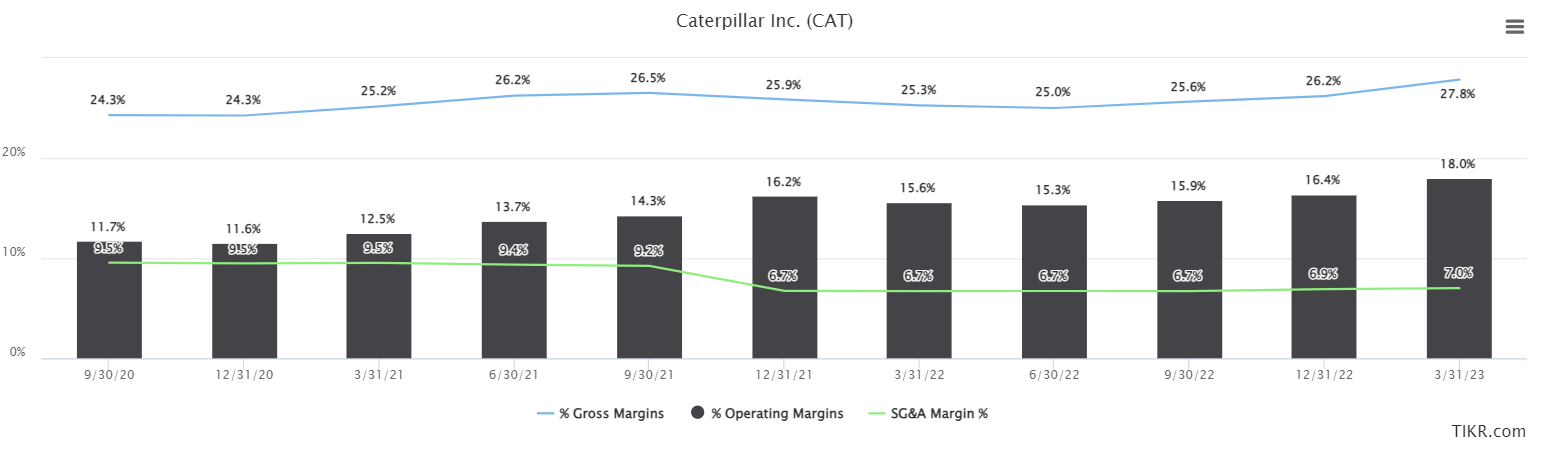

Below we have trailing-twelve-months gross profit, SG&A costs, and operating margins, to illustrate this point.

{kind=link}

Since the middle of 2021, Caterpillar has leveraged down its SG&A costs, in addition to driving higher gross margins through price increases. That has led to much higher operating profits over time, and in the most recent quarter, operating margin was 21% of revenue. That means there's likely another two or three quarters of meaningful upside to these numbers before the comparables become more difficult. That's certainly a potential upside catalyst for the stock in the coming months.

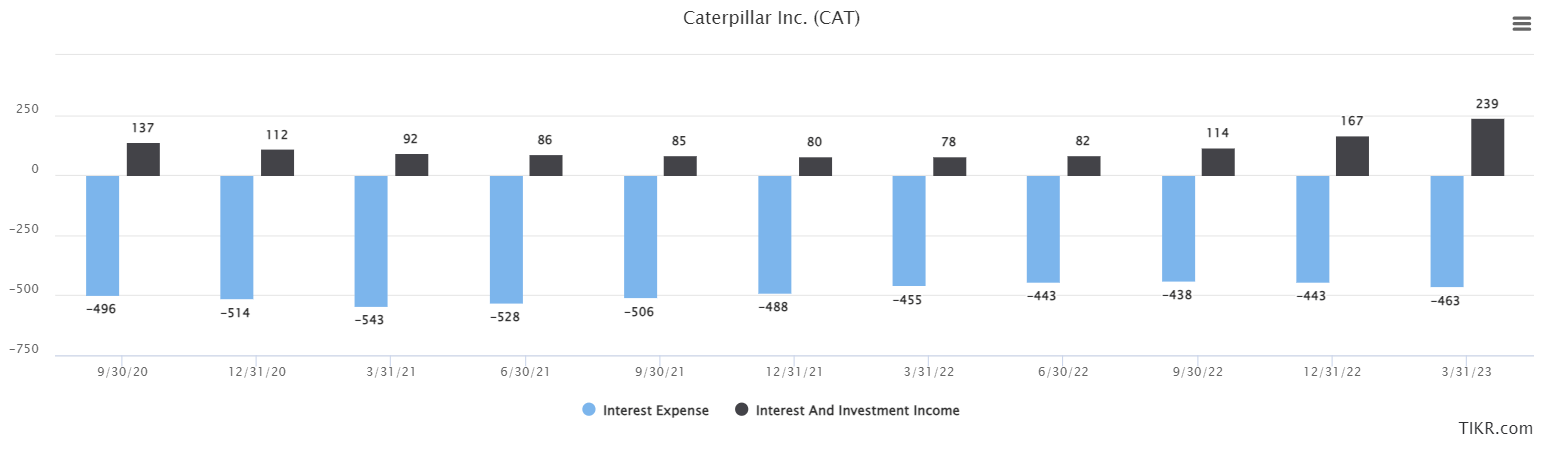

Next up, Caterpillar's use of debt has been a pretty sizable headwind to earnings in the past, but now, it's much less so. A reduced headwind is the same as a tailwind, and below, we see the relationship between interest expense and investment income narrowing sharply.

{kind=link}

In the March quarter of 2021, the gap (net expense) was $451 million on a trailing-twelve-months basis. Two years later, it was $224 million, half as much. That's $227 million Caterpillar can let trickle to the bottom line, and while this isn't game-changing money for Caterpillar, every little bit helps. So long as rates stay near current levels, we should continue to see this improve as well.

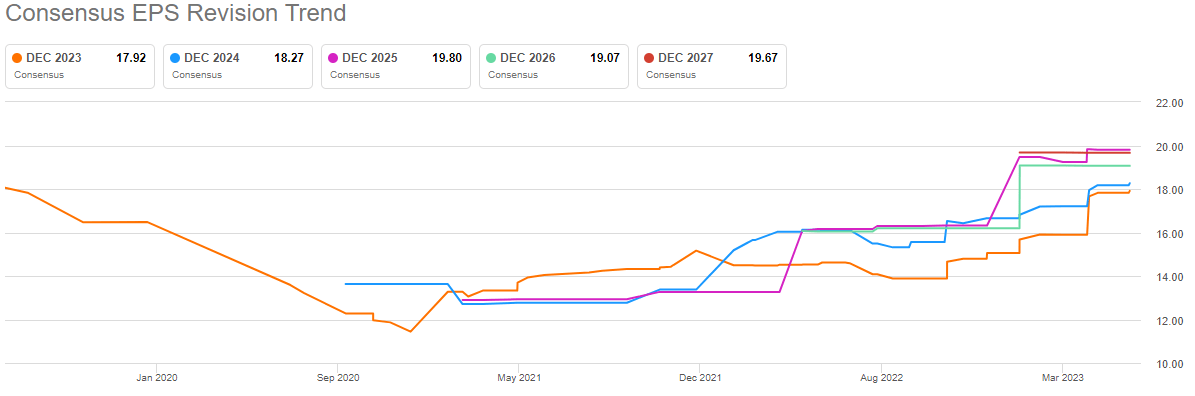

If we put all of this together, we get - perhaps unsurprisingly - pretty aggressive EPS revisions upward by analysts.

{kind=link}

EPS estimates plummeted in the wake of COVID, but have since regained lost ground and then some. These lines are moving up and to the right, which is exactly what we want to see.

Risks and other considerations

Now, just because recession has been staved off thus far does not mean it will continue to be. People buy machines from Caterpillar when they're bullish on their respective business; that does not generally happen much in a recessionary environment. I'm not seeing signs of recession in the stock market, but it is certainly a possibility.

In addition, Caterpillar's projected EPS growth from here is set to be somewhat muted. I mentioned the impact of pricing increases isn't going to repeat over time in the magnitude that it is driving results today. At some point, the company will need to be able to see higher volumes again, and if volumes do fall in the coming quarters, the margin growth story will become challenging.

I don't see these risks as unduly high at the moment, but don't want to discount them entirely. It's something to consider.

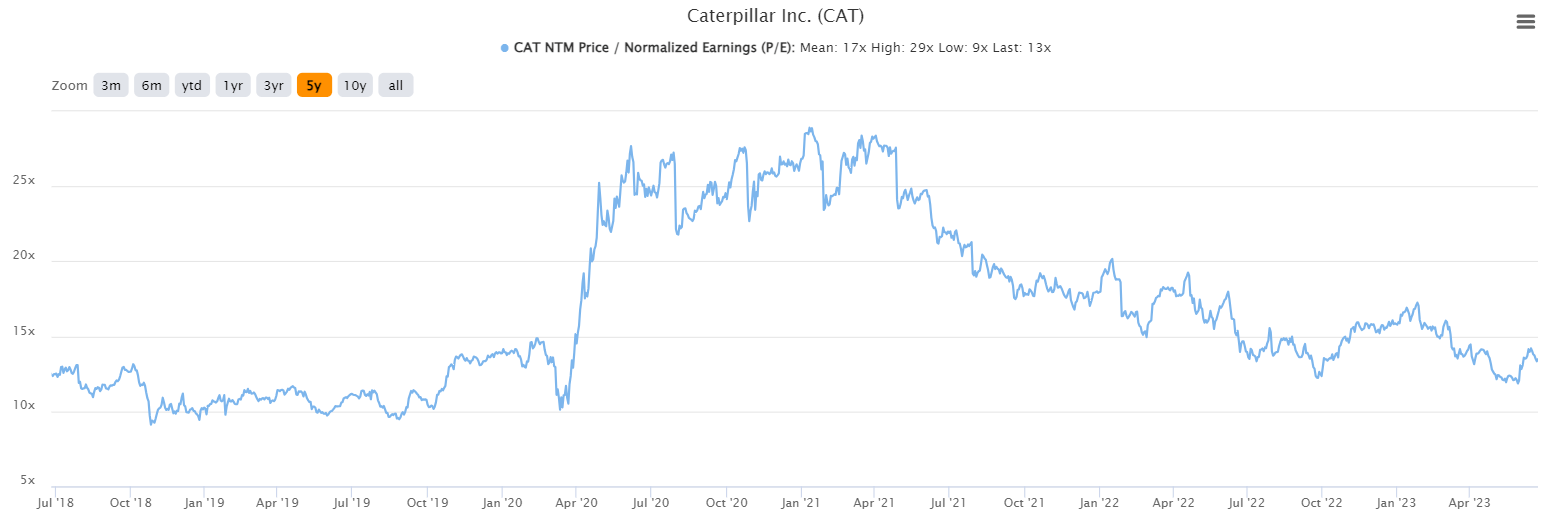

Cheap, but is it cheap enough?

That's the key question as we look at the forward P/E ratio, which stands at 13X today.

{kind=link}

Caterpillar had distinct valuation periods pre-COVID, during COVID, and now post-COVID. The lead up to COVID saw the stock valued at 10X to 14X forward earnings. COVID saw EPS estimates plunge, and valuations rise as a result. Since then, however, valuations have normalized, and we're back at 13X forward earnings.

We can see that's near the bottom for the past year, so in that sense, the stock looks cheap enough. I can't say we won't see 10X earnings for Caterpillar again, but I think the fact that its margin profile has improved to the extent that it has makes that unlikely. If margins hold, I would see its fair value range at 13X to 17X, or something akin to that, rather than the prior 10X to 14X.

The bottom line here is that we have a reasonably bullish chart, and a company that has proven it can raise prices at will without sacrificing anything, really. The valuation is good enough, and as I said, is quite near the bottom for the past couple of years. All in all, I'm upgrading Caterpillar to buy.

For further details see:

Buy Caterpillar's Recent Breakout