CDTX - Buy Cidara Therapeutics For The Cloudbreak Platform

2023-08-16 08:18:35 ET

Summary

- Cidara Therapeutics has recently gained FDA approval for rezafungin and is now focused on advancing its Cloudbreak platform in oncology and infectious disease indications, which has great potential.

- Potential revenue from rezafungin, CDTX's partnership-based business model and track record, and the major advantages of Cloudbreak platform all point to major upside potential for CDTX.

- My recommendation is "Buy" rather than "Strong Buy" because the Cloudbreak platform is still at a very early stage; setbacks are more likely than not and dilution risk is high.

Overview of the thesis

Cidara Therapeutics ( CDTX ) has recently gained FDA approval of rezafungin (an once weekly echinocandin antifungal) for therapeutic use, which however currently has a small target population. Nevertheless, potential further milestone payments and royalties, approval and commercialization in other parts of the world (EU approval pending), as well as future label expansion for prophylaxis indication, could provide CDTX with meaningful income and support development of the rest of CDTX's pipeline, thus limiting to some extent the potential downside risk.

CDTX has sold rezafungin rights to Melinta therapeutics (US) and Mundipharma (ex-US, ex-Japan) and is now focused on its Cloudbreak platform, which I believe has significant potential. It is a novel form of immunotherapy based on drug-Fc conjugates, which is targeting well-validated targets in both infectious diseases (CD388 for flu) and oncology (CD421 for solid tumors) and has significant theoretical advantages over alternatives (small molecules and monoclonal antibodies) for the same targets.

Investment in CDTX will need patience and the stock may be volatile in the short-to-medium term. Positive news on Janssen deal regarding CD388 would be a nice surprise that could spark a good rally, but the chances of that happening have become lower based on recent de-prioritization by Janssen of its infectious diseases and vaccines pipeline.

De-risking by rezafungin

The focus of this thesis is the potential of CDTX's Cloudbreak platform. However, I believe that recent FDA approval of rezafungin, combined with potential future milestone payments, limit downside risk in case of setbacks with the Cloudbreak platform.

Briefly, rezafungin is a long-term (once-weekly) antifungal belonging to the class of echinocandins (the following being currently in clinical use: caspofungin, anidulafungin and micafungin). The spectrum of activity and efficacy of rezafungin is similar to that of other echinocandins. The major advantage of rezafungin is the potential for once weekly dosing (versus daily for other echinocandins). This could allow faster discharge from the hospital of patients needing prolonged treatment with echinocandin (the minimum treatment duration for invasive candida infections is typically 2 weeks, but often longer is necessary), especially for infections caused by fluconazole-resistant Candida species, i.e. when oral switch to fluconazole is not an option. Notable is that non-albicans species (some of which, including C. auris, have inherently high fluconazole resistance) are increasing .

The major limitation of rezafungin is the limited available data for its use, as well as failing to achieve non-inferiority at a 10% cut-off in the phase 3 RCT (vs caspofungin). As a result, rezafungin is not going to replace echinocandins, and will likely be used predominantly for the above-described population (i.e. to allow faster discharge from the hospital of patients with invasive candidiasis needing prolonged treatment and for whom oral switch to fluconazole is not an option).

CDTX has established the following partnerships for rezafungin ( Partnerships - Cidara Therapeutics )(see 10-Q for more details).

Melinta therapeutics agreement: Melinta will be solely responsible for the commercialization of rezafungin in US, at its sole expense. CDTX is still responsible for completion of the ongoing ReSPECT Phase 3 trial for prophylaxis and preparation and submission to the FDA of a supplemental NDA for the Prophylaxis Indication. The total potential transaction value is $460m, of which CDTX has received upfront $30m + $20m following FDA approval of rezafungin. Therefore, remaining potential value is $410 (although the chances of reaching commercial milestones - details of the deal are not known- are likely small). CDTX is also "eligible to receive tiered royalties on U.S. sales in the low double digits to mid-teens". According to CDC estimates there are approximately 25,000 cases of candidemia in the US yearly. Candidemia reflects about half of invasive candida infections, meaning a total US target market for rezafungin of about 50,000 cases per year. Based on recent estimates, about 7% of candidemias are caused by fluconazole-resistant species, thus decreasing rezafungin target population to about 3,500 US cases per year. Given rezafungin's label most of these cases are likely to be treated by daily echinocandins. Assuming a 10% market penetration this would mean 350 US cases per year. Assuming an average of 1.5 doses per patient (some will need just 1 dose, other 2 doses, and few with hard-to-treat infection sites more doses) this means 525 doses in the US per year. Considering about $2,000 price per vial this means sales of just $1M per year. Assuming 12% royalties this means about $120K per year for CDTX, which is not much.

Mundipharma agreement: Commercialization rights outside U.S. and Japan. CDTX and Mundipharma share the developmental costs 50/50 (up to a cap of $31.2m). Mundipharma is responsible for activities necessary to obtain and maintain regulatory approvals outside of the U.S. and Japan, at Mundipharma's sole cost. The total potential transaction value is $568.4 million. CDTX has already received up-front fee of $30.0 million, plus the research and development funding of $31.2 million, plus milestones achieved of $13.9 million. Therefore, the remaining potential value is $493.3m (although the chances of reaching commercial milestones - details of the deal are not known- are likely small). CDTX is also "eligible to receive double-digit royalties in the teens on tiers of annual net sales".

Global echinocandin market is estimated to reach $796M by 2029. Assuming just 10% penetration by rezafungin and 12% royalties this would mean global rezafungin income potential of about $9.5M per year for CDTX. Nevertheless, I believe my above estimations for market potential in US and globally are quite conservative and there are several factors that could significantly increase that; (1) As more data become available clinicians may be more comfortable in using rezafungin (once weekly vs daily dosing is a major advantage) as a first line alternative to echinocandins (rather than as a last resort option), (2) As more clinical data become available, off-label empirical use of rezafungin or additional single-dose before patient discharge (to extend antifungal coverage duration beyond discharge from the hospital) are possible scenarios. Notably, treatment of invasive fungal infections is often empirical due to difficulties in establishing microbiological confirmation. (3) Fluconazole-resistant Candida infections are increasing, especially considering emergence and spread of fluconazole-resistant species including C. auris and fluconazole-resistant C. parapsilosis . In some centers fluconazole-resistance has been reported as high as 17 - 48 %. (4) Potential label expansion to prophylaxis indication. A combination of above factors could result in multi-fold higher rezafungin income for CDTX.

Also, I have to emphasize that above estimation only account for royalty income and do not include the above-discussed potential milestone payments, which would represent a major source of income for CDTX.

Overview of the Cloudbreak platform

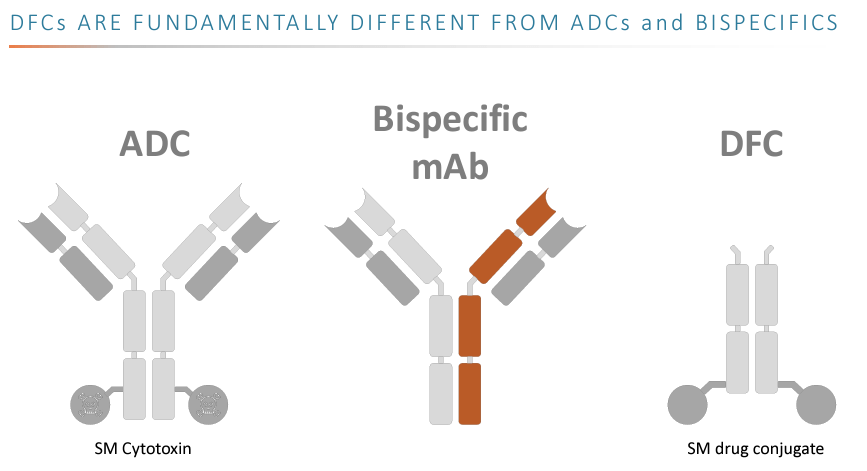

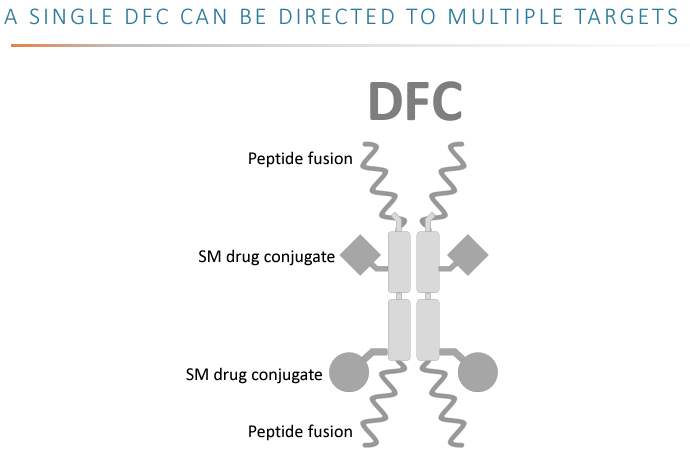

As described by CDTX "Cloudbreak platform is a fundamentally new approach to treating and preventing serious diseases such as viral infections and solid tumors". Candidates of this platform are drug-Fc conjugates (DFCs), i.e. a new generation of immunotherapeutic agents that couple potent drugs to a human antibody fragment (the Fc moiety)(see 1st figure below). The Fc moiety can be tailored to specific requirements (potency, improved half-life, immune-activating vs immune silent). Furthermore, the same Fc molecule can be conjugated with multiple molecules, thus allowing multi-targeting from a single molecule (see 2nd figure below).

{kind=link}

ADC= antibody-drug conjugate, mAB= monoclonal antibody, SM= small molecule

{kind=link}

SM= small molecules, DFC= drug-fc conjugates

Theoretical advantages of the Cloudbreak platform over monoclonal antibodies and small-molecule therapeutics

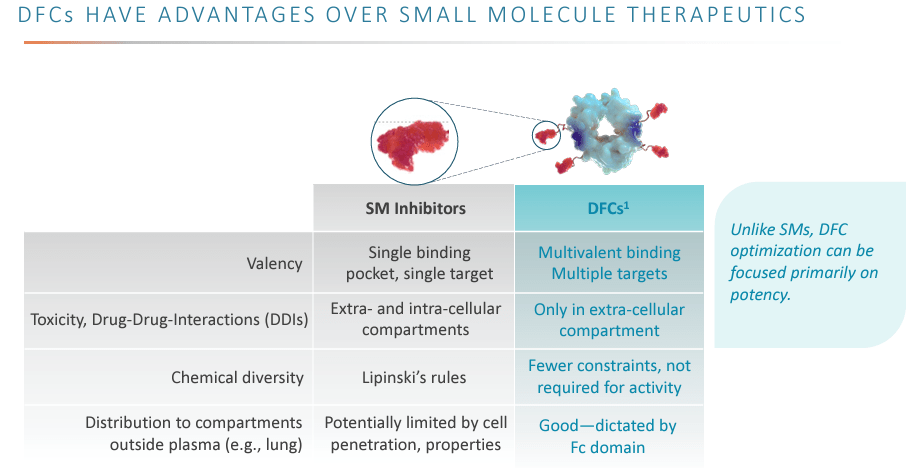

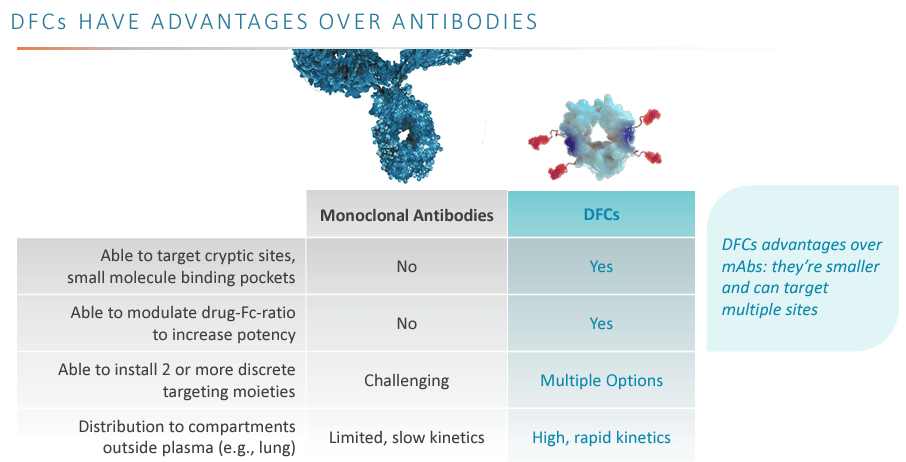

I believe advantages of the platform are well-summarized in the company's presentation (see figures below). Briefly these advantages include:

- Improved pharmacokinetics; long duration of action from single dose (e.g. CD388 is expected to provide protection for the whole flu season).

- Potential for multiple targets in a single molecule (may improve efficacy and minimize risk of resistance to the treatment, important for both infectious diseases and oncology).

- Less toxicity (vs small-molecules) due to being limited to the extra-cellular compartment.

- Smaller than monoclonal antibodies, which allows better tissue penetration and potential to access cryptic binding targets.

- Less expensive than monoclonal antibodies.

{kind=link}

SM= small molecules, DFC= drug-fc conjugates

{kind=link}

Why I believe the Cloudbreak platform could be a success

(1) Validated targets (=de-risking): Cloudbreak platform candidates have well-validated targets;

- neuraminidase (influenza); The current standard of care for treatment of influenza involves neuraminidase inhibitors (oseltamivir, zanamivir, peramivir, laninamivir) and baloxavir. VIR biotechnology is also developing an investigational neuraminidase-targeting monoclonal antibody, which further validates the target, but is still in preclinical stage.

- spike protein (SARS-COV-2); COVID-19 vaccines, as well as monoclonal antibodies target the spike protein.

- Inhibition of adenosine pathway (cancer immunotherapy); the pathway is a well-established target with several molecules in clinical or pre-clinical development. Inhibition of this pathway can help overcome the immune-suppressive tumor microenvironment (a major hurdle for immunotherapies in solid tumors) and can be combined with other immunotherapies (such as CAR-T cells). Competition in the field is fierce, with many companies targeting the pathway (including among others AstraZeneca, ORIC pharma and Arcus Biosciences), but this further validates the potential of the target.

(2) Significant theoretical advantages of drug-fc conjugates vs alternatives for same targets (e.g. small molecules and monoclonal antibodies).

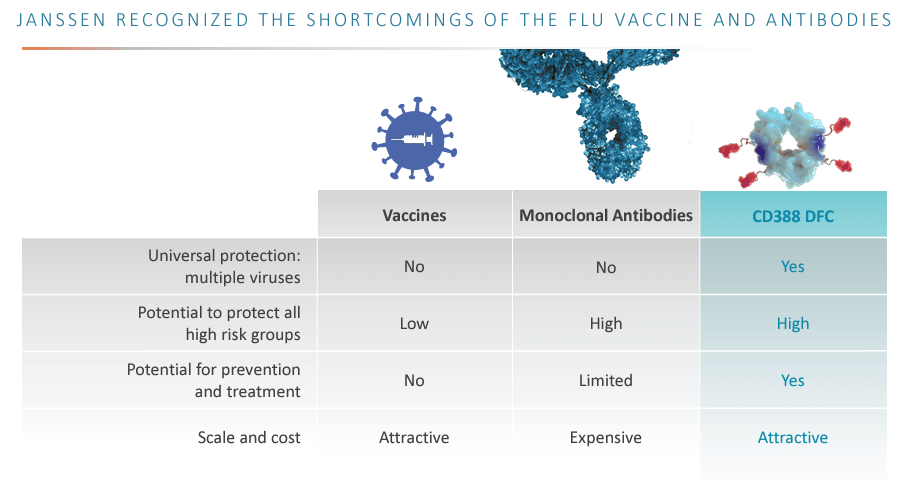

- CD388: Current options for prophylaxis of influenza include: vaccines and prophylactic antivirals (neuraminidase inhibitors or baloxavir). However, influenza vaccines' efficacy is suboptimal typically ranging between 40-60%, and can be even lower for certain high-risk populations that do not respond as well, especially severely immunocompromised patients taking therapies that prevent them from mounting sufficient antibody responses to flu vaccines (such populations would be ideal targets for CD388). Influenza vaccine efficacy may also be much lower in some seasons when vaccine strains are not well-matched to circulating flu strains. In contrast to influenza vaccines (whose compositions needs yearly updates based on predictions for which flu strains are going to circulate), CD388 is aimed for universal influenza protection, i.e. no need for updates in the formulation each year. Regarding the other prophylactic option, prophylactic neuraminidase inhibitors require daily treatment and protective effect stops as soon as treatment stops. CD388 can overcome all above limitations: universal flu strain coverage + a single dose is expected to protect for the whole flu season + likely better efficacy than vaccines in high-risk populations.

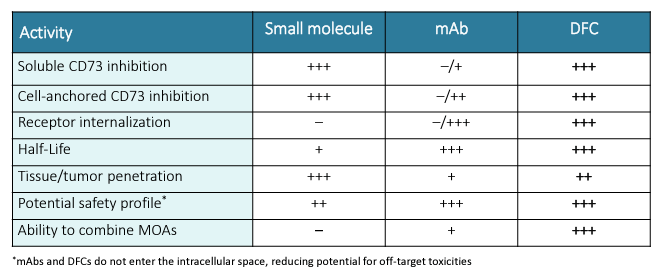

- CD421 : CD421 is a CD73 inhibitor aiming to block the adenosine pathway. As a drug-fc conjugate, CD421 has significant advantages over alternative CD73-targeting moieties, i.e. small molecules or monoclonal antibodies, combining the good properties of both; long duration of action, good tissue penetration and safety (see figure below).

(3) Validation of the platform's promise by CD388 and Janssen partnership: But see next paragraph.

(4) Fast track designation by FDA of CD388 validates unmet need

(5) Huge potential for expansion of the Cloudbreak platform to various indications: Given above-described advantages of DFCs over mAbs/ADC/small molecules, the platform has theoretical potential to penetrate mAbs/ADC/small molecules market for numerous established indications. Although CDTX has not revealed such plans, I believe this to be a very probable scenario.

CDTX company presentation CDTX presentation

{kind=link}

{kind=link}

mAb= monoclonal antibodies, DFC= drug-fc conjugates, MOAs= mechanisms of action

CD388 and the Janssen deal

Unfortunately, as recently announced by CDTX; "Janssen has announced its intention to discontinue internal development of the majority of its infectious disease pipeline, including JNJ-0953 (CD388). However, at this time, Janssen has not informed Cidara of any intention to terminate the agreement between the two parties". Janssen has 90 days after receiving the complete ph2a data (later this year) to officially inform CDTX whether it will proceed with CD388 clinical development. Janssen also has the option to sublicence or assign the rights to a third party, in which case all terms of the Janssen deal would survive without modification.

On the plus side, Janssen's decision to cut-down on its infectious diseases and vaccines program doesn't have to do anything with CD388. Considering that the deal with Janssen was struck at a much earlier stage it is possible that CDTX could even get a better new deal (if CDTX receives the rights for CD388 back from Janssen) considering positive ph2 results and recent fast track designation . However, time is of the essence considering competition in the field and forming a new partnership would take time. Nevertheless, CDTX could in the meantime (while having discussions for partnerships) advance the CD388 program by preparing (with FDA's guidance given fast track designation) the next clinical trials. Ideally, CDTX would want to have the next clinical trial ready to start before next year's flu season (i.e. before October 2024).

CDTX could also elect to proceed with CD388 alone but that would mean the need to raise significant cash which would most likely be very dilutive. On the other hand, a partnership at a later stage could mean a better deal for CDTX. However, considering CDTX's current business model (see below) chances are that CDTX will not elect proceeding alone.

Recent news by VIR biotechnology and implications for CDTX

VIR recently announced that its flu prophylactic monoclonal antibody failed to meet the primary endpoint in a ph2 trial. Setbacks in competition is probably good news for CDTX. Note that VIR-2482 is targeting hemagglutinin, in contrast to CD388 which is targeting the neuraminidase. Notable is that VIR is also developing "an investigational neuraminidase-targeting monoclonal antibody" (VIR-2981) further validating the target. However, in contrast to CD388 (which could be phase 3 -ready within the next 2 years) VIR-2981 is still in the preclinical stage.

Also note that VIR's phase 2 trial enrolled only healthy patients. Although this is a much larger target market it also means need for much larger study populations given the lower risk of influenza in healthy patients (VIR-2482 did have some promising, but non-significant, signals of efficacy in secondary endpoints). Monoclonal antibodies would be expected to work much better in older patients and patients with comorbidities (especially immunocompromised patients), i.e. patients that are less likely to mount a good (protective) antibody response from vaccination. This is the population that CDTX would most likely target first (based on April 17th Needham presentation).

CDTX's business model and financials

CDTX's business model is currently based on partnerships. CDTX has successfully achieved this with rezafungin and may also be similarly successful with the Cloudbreak platform with already one partnership (Janssen) for CD388. On the one hand, this model could limit future profits potential. On the other hand, CDTX is a small biotech that does not have either the cash or the infrastructure necessary to support commercialization. Therefore, partnerships is likely the best way forward for CDTX which significantly derisks the company and still leaves potential for major upside considering target markets of Cloudbreak platform (solid tumor cancer treatment market is expected to reach $337.47B in 2027, influenza vaccines market is expected to reach $12B in 2030). According to Seeking Alpha, CDTX's current enterprise value (EV) is just $37M. Considering, pending milestones, rezafungin conservative peak sale estimations and a 7.1 EV/Revenue multiple ( typical for biotechs ) CDTX appears undervalued (or at the least fairly valued) just on income potential of rezafungin.

Cash and cash equivalents totaled $50.4M as of June 30, compared with $32.7M as of December 31, 2022. Total operating expenses in Q1 2023 were $20.4M (R&D $17,1m + G&A $3.3) but are likely to increase as CDTX advances its pipeline, if Janssen deal gets terminated and CDTX fails to achieve new partnerships. This means that CDTX has enough cash for just 2 more quarters (Q3-Q4 2023) and might soon need to raise cash, especially if the Janssen deal is terminated. Nevertheless, CDTX is "eligible to receive additional non-dilutive capital of up to approximately $47.1 million in development and regulatory milestones from our existing partnerships contingent on successful completion of activities planned for the next twelve months". This has the potential to extend the cash runaway " without the need to rely on equity markets to raise additional capital in the near-term ". Furthermore, considering CDTX's business model it is very likely that CDTX will be able to advance the Cloudbreak platform pipeline relying on income from partnership/licensing deals with other pharma companies, thus limiting risk of dilutive capital raise.

Catalysts

The major catalyst would be Janssen opting-in (or sub-licensing the deal) to proceed with clinical development of CD388, although the chances of this may be low based on recent news. Other potential catalysts over the next 1-3 years:

- Final results of the ongoing phase 2 studies for CD388 (later this year)

- Rezafungin approval in Europe

- News on further clinical development of CD388 (e.g. agreement with FDA about next clinical trial)

- IND approval for CD421

- Partnership announcement for CD421 and future Cloudbreak targets

- News on other oncology targets

- Completion of ongoing Phase 3 ReSPECT prophylaxis study

- Topline results of ongoing Phase 3 ReSPECT prophylaxis study

Risk

- The major short-term risk for CDTX is Janssen opting out of CD388. This would have the following implications: It would deprive CDTX of much-needed cash. As a result, CDTX would soon need to raise cash. CDTX would also probably have to look for another partner, but this would take time which could significantly impact CD388 future commercial potential considering competition in the field. CDTX could also chose to continue developing CD388 on its own but would need to raise significant amount of cash to do so.

- Rezafungin currently has a limited target population. Therefore, commercialization (and milestones-royalties for CDTX) may not go as planned, and my above estimations, even though conservative, may prove to be over-optimistic.

- Cloudbreak platform is at a very early stage and setbacks are more likely than not.

- CDTX's business model is based on achieving partnerships. Failing to do so would probably mean significant dilution for early investors.

Summary and recommendation

Termination of Janssen deal for CD388 would be a significant setback for CDTX and could negatively affect the stock price in the short/medium term. However, the downside risk is somewhat limited by recent approval of rezafungin and potential future milestones and royalties. Furthermore, the potential of the Cloudbreak platform is promising considering validated targets (which significantly increases probability of success in clinical trials) and major advantages over alternative therapies for same targets. Finally, CDTX has a proven business track record, with 3 partnerships, and is likely to continue to be able to form partnerships that will help support development of the Cloudbreak platform.

Buying CDTX is a high-risk speculative investment and will need patience, especially if Janssen deal will be terminated. Considering current market cap and cash needs the potential for significant dilution is a major risk. Invest only what you can afford to lose.

For further details see:

Buy Cidara Therapeutics For The Cloudbreak Platform