ISNPY - Buy Intesa For Its 11% Dividend Yield

2023-09-18 18:10:06 ET

Summary

- Intesa Sanpaolo has reported strong operating performance and a sustainable dividend, but shares trade at a discount due to a new banking tax in Italy.

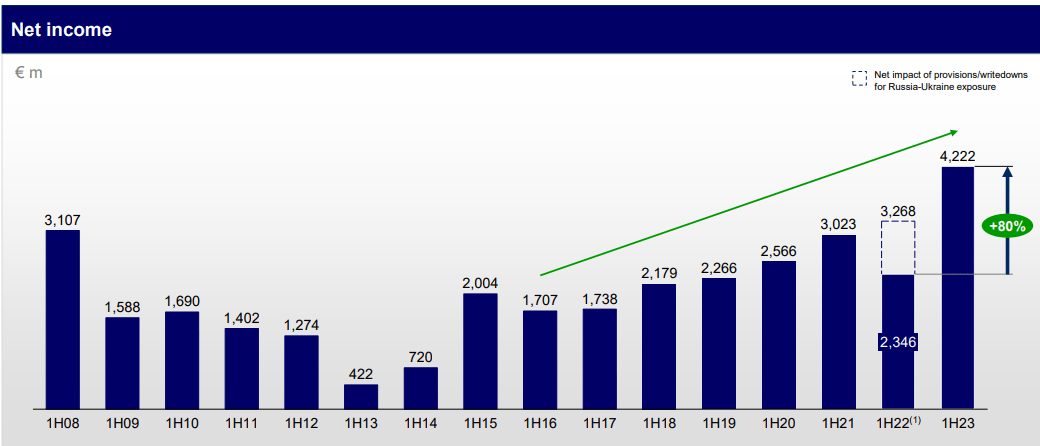

- The bank's net income in H1 2023 increased by 80% YoY, reaching a record level for the first half of the year.

- Intesa's dividend yield is attractive at 11%, supported by its earnings and strong capital position, making it a good income play in the European banking sector.

Intesa Sanpaolo ( ISNPY ) has reported a strong operating performance and its dividend is clearly sustainable, but the new banking tax in Italy is a major reason why its shares trade at a discount to its European peers.

As I’ve covered in a previous article , Intesa is one of the European banks with a higher-dividend yield, while its shares also trade at a relatively low valuation. However, since my last article, the Italian government announced a new extraordinary tax on Italian banks, which can be quite negative for the stocks of Italian banks.

Despite that, Intesa’s stock is up over the past three months and has been able to outperform the S&P 500 index by a small margin, which can be considered a resilient performance during this period. In this article, I analyze Intesa’s most recent earnings and update its investment case, to see if it remains an interesting income play within the European banking sector.

Article performance (Seeking Alpha)

Earnings Analysis

Intesa has reported its half-year results at the end of July, maintaining a positive operating momentum supported by higher interest rates in Europe.

While Intesa is not among the banks most geared to rates, as the bank’s strategy over the past few years has been to diversify its revenue stream, it’s still quite exposed to rates and this has been a strong support for revenue and earnings growth, reaching record net income during the past few quarters.

Indeed, Intesa’s net income during H1 2023 was above €4.2 billion, a new record level for the first-half of the year, increasing by 80% YoY. However, its H1 2022 net income was impacted by extraordinary provisions related to Russia/Ukraine exposure, thus adjusted for this effect its net income increased by 29% YoY, still a very good growth rate.

{kind=link}

Due to this strong performance in the past couple of quarters, Intesa has increased its guidance for net income in the full year, to more than €7 billion in 2023, while its previous guidance was to achieve a net income of about €5.5 billion (expected back in February) .

This shows that Intesa’s operating performance has been quite strong and even above its management expectations, as rates have increased more than expected at the beginning of the year, and credit quality has remained quite strong.

Nevertheless, the main factor justifying this good performance is strong growth in net interest income ((NII)), which amounted to more than €6.8 billion in H1 2023, an increase of 69% YoY. This is justified by the fact that loans in Italy are mainly related to floating rates, thus most of its loan book has re-set interest loans at higher rates in recent months, due to the European Central Bank’s hiking pace since the summer of 2022. This trend is also valid for its closest competitors, given that this is an industry-wide profile in Italy and not specific to Intesa.

While Intesa has pushed for fee-based products in recent years, in asset management and insurance operations, its fee income was about €4.3 billion in H1 2023, representing a decrease of 4.2% YoY.

Due to strong growth in NII, Intesa’s revenue mix has changed somewhat in recent quarters, given that NII’s weight on total revenues increased to around 55% in H1 2023, while in the recent past its weight was less than 45%. Despite this increase in total income, Intesa’s reliance on NII is still below the level of European banks with higher exposure to rates, which have a weight of NII on total revenues of about 75%.

This means that Intesa’s upside related to rates is lower compared to some peers, but its revenue mix is more recurring over the long term, which is a positive factor of its business model in my opinion.

Regarding costs, Intesa reported a very good cost control during an inflationary environment, given that operating costs increased only by 0.9% YoY to €5.2 billion, leading to an operating income of about €7.1 billion. Its cost-to-income ratio, a key measure of efficiency in the banking sector, was 42% in H1 2023, being one of the best banks in Europe by this measure.

On credit quality, Intesa booked provisions of €556 million in the first-half of 2023, representing a cost of risk ratio of only 25 basis points (bps). In 2022 , the bank reported a cost of risk ratio of 70 bps, but some 40 bps were related to Russia/Ukraine provisions and write-downs, thus its H1 2023 risk ratio was a small improvement from last year. This is a positive trend because higher interest rates make households and corporates more financially strained, which could lead to higher loan defaults, but so far that has not been the case.

While Intesa’s operating performance has been quite strong in recent quarters, this is not expected to maintain in future quarters, as the European Central Bank may be near the top of its hiking cycle and therefore further NII gains may be harder to achieve.

According to analysts’ estimates , Intesa’s NII is expected to be around €13.8 billion in 2023 (vs. €9.5 billion in 2022), but should decline to €13.5 billion in 2024 and €13.4 billion in 2025. This means that current consensus suggest we shouldn't expect further rate hikes in the next year, but it’s not also forecasting interest rate cuts, which would be a positive scenario for the bank as revenue and earnings would be somewhat stable over the next three years.

However, if inflation returns to more normal levels and the economic situation deteriorates further in the coming quarters, potentially the European Central Bank may decide to cut rates in 2024 or 2025, which would lead to lower NII for Intesa. While there is significant uncertainty about interest rate levels in the next couple of years, this is a scenario that investors shouldn’t overlook as it would have a negative impact on the bank’s earnings and dividends to shareholders in the near future.

Despite that, it’s likely that Intesa will remain a high-dividend yielder in the coming years, given that its dividend is well covered by earnings and the bank’s capital position is solid and therefore it does not need to retain much earnings in the near term.

At the end of last June, Intesa’s CET1 ratio was 14%, well above its capital requirement of 8.95% and its own internal target of at least 12%. Thus, Intesa has an ‘excess capital’ position and can distribute the vast majority of its earnings to shareholders, with the bank’s goal being to distribute some 70% of its annual profits through dividends and share buybacks.

Capital ratio (Intesa)

Its last annual dividend amounted to a cash outflow of €3 billion, while in H1 2023 it already said it intends to distribute €2.45 billion in November as an interim payment. For the full year, the market expects a dividend per share of €0.27, an increase of 70% from the previous year, which at its current share price leads to a forward dividend yield of about 11%. This is very attractive for income investors and Intesa’s dividend is sustainable because it's supported by the bank’s earnings and strong capital position, making it a good income play within the European banking sector.

This high-dividend yield is also justified by a relatively weak share price, which in my opinion is largely justified by Italy’s political risk rather than fundamental issues at the bank. A good example was the Italian government's recent announcement of a ‘special’ tax on banks , to penalize them for ‘excessive’ profits related to higher interest rates. This seems to be a populist measure, but the government wants to collect about €3 billion annually from this new tax, which is obviously negative for Italian banks.

Given that Intesa is the largest bank in Italy by total assets, it will share a large part of the burn, being a new headwind for profit growth ahead. While this new tax should impact mainly its 2024 and 2025 earnings, this represents a new risk for investors and justifies to some extent why Intesa’s valuation seems to be out of synch with its fundamentals.

Indeed, Intesa is currently trading at 0.8x book value, at a slight discount to the European banking sector, even though it has a quality profile and much higher than usual dividend yield. However, all Italian banks are currently trading at a discount to European peers due to political risk, thus I don’t expect a re-rating in the near term, as investors aren’t likely to give Intesa or other Italian banks higher valuations in the coming quarters.

Conclusion

Intesa has reported good operating performances in recent quarters, reaching very solid levels of profitability, which is a great support for its high-dividend yield. However, political risk in Italy should not be overlooked and the new tax presented one month ago is a good example of that, being a key reason why Italian banks trade at a discount to its European peers.

While this new tax does not put Intesa’s dividend ambitions in jeopardy, it’s a headwind for a higher valuation and therefore Intesa’s investment case is now mainly geared to income rather than value.

For further details see:

Buy Intesa For Its 11% Dividend Yield