MTG - Buy MGIC: 15% Cash Returns To Investors And Growing

Summary

- MGIC reported a strong Q4 of $0.56, up 12% from a year ago.

- Why I don’t worry that MGIC’s claims payments will surge.

- MGIC the cash machine.

- The magical stock buyback math.

- My target price is $25.

Introduction. What?

On Thursday, MGIC Investment Corporation ( MTG ) reported a Q4 earnings beat and reported $2 billion of excess capital. Meanwhile, Bed Bath & Beyond ( BBBY ) defaulted on a bond payment and has net debt of nearly $2 billion. The result? MTG rose by a paltry 0.4% and BBBY rose by 18%. What?

All this perplexed value investor can do is soldier on.

MGIC's 4th quarter - steady as she goes

MGIC reported EPS of $0.64. I adjust its operating EPS to $0.56, as follows:

- MGIC recorded negative $31 million for mortgage default losses, meaning that it decided that the reserves it had set aside (mostly after COVID) were too high. I replace this non-cash accounting adjustment with its actual claims paid of $14 million.

- It looks like MGIC threw in $10-15 million extra into its pension fund. I reduced operating expenses by this amount.

The $0.56 operating EPS compares to $0.50 a year ago, a nice 12% gain. But MGIC's revenues (insurance premiums received after sharing some with reinsurers) of $292 million were actually down $2 million from a year ago. And dollar operating income of $166 million was down by the same amount. Huh?

I'll leave you in brief suspense about MGIC's magic (allow me one corny joke). Let's first address the major worry that investors appear to have about MGIC and its mortgage insurance peers, namely whether their claims payments can remain so low. After all, the $14 million MGIC paid last quarter compares to $91 million five years ago and $628 million ten years ago in the wake of the housing bust. And we are all aware of the sharp decline in home sales over the past year, and a shift towards a decline in home prices. So why aren't home foreclosures set to rise sharply?

Why I don't worry that MGIC's claims payments will surge

For those of you who have read any of my numerous Seeking Alpha articles on MGIC and its peers, you've already seen versions of the data I'm about to show. But considering the significant fear factor built into MGIC's valuation, the data bears repeating.

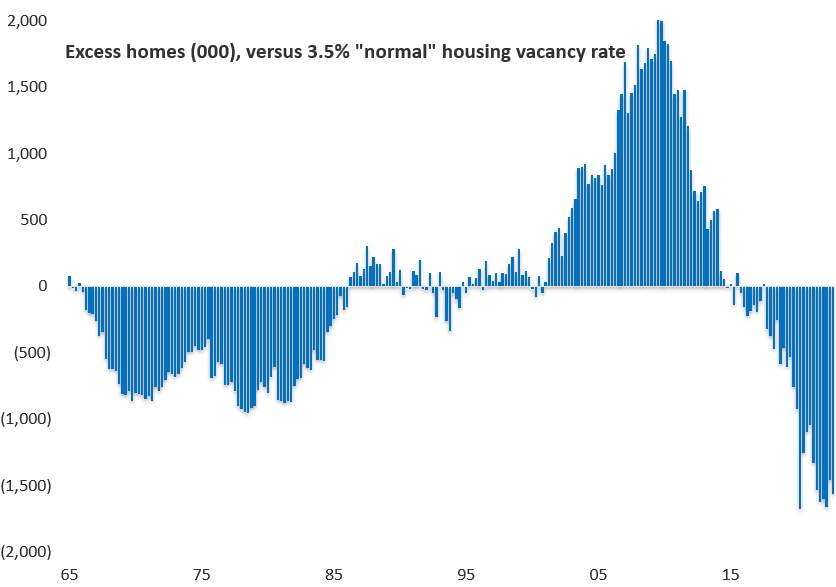

The first data set concerns the balance of supply and demand for housing , which can neatly be summarized by the housing vacancy rate. A high level of vacant housing means the risk of a sharp home price decline to clear the excess, and lots of mortgage defaults. A shortage of housing supports home prices and limits defaults. So let's look at the history of the housing vacancy rate, which was just updated this week by the Census Bureau. I compare the number of vacant units to the 3.5% long-term vacancy rate average:

{kind=link}

The chart clearly shows that the country remains mired in a record housing shortage. And you can see that the '07-'11 housing bust was partly caused by a record housing excess.

The second data set is mortgage credit quality . Mortgage underwriting standards are far more conservative today than back in '08, as these charts from peer mortgage insurer Radian ( RDN ) show:

Radian financial reports

Today's far safer underwriting dramatically reduces the risk of mortgage defaults going forward.

There is actually a lot more data to support my view on mortgage defaults, but let's move on. Net/net, I am very comfortable that outside of a major recession, MGIC's mortgage default claims payments will remain low. And therefore, its annual dollar earnings should be stable in the $650 million range.

MGIC, the cash machine

Here's a list of the cash that MGIC paid to its shareholders last year:

- $111 million in dividends

- $386 million to repurchase 28 million shares

- $89 million to repurchase most of a high-yielding and dilutive convertible preferred

That's $586 million in total, or $1.90 per share. Or a 13% return on the current stock price. Despite the high payout, and despite the fact that MGIC grew its loans insured by 8%, it actually had more excess capital at the end of the year than at the start.

How is all this possible? Two reasons:

- MGIC is generating high returns for an insurance company. Its $650 million earnings run rate is a 15% return on 130% of its required capital.

- MGIC's low-risk strategy - those conservative lending standards plus the aggressive use of reinsurance - means that essentially all of its earnings are free cash flow available to investors.

The magical stock buyback math

We can now circle back to MGIC's Q4 operating earnings growth of 12% with flat dollar earnings. MGIC had 339 million diluted shares during Q4 '21, but only 300 million during Q4 '22. That's a 12% decline. I expect another 8% decline in the share count this year, and for the foreseeable future, unless the share price rises materially. Plus, steady increases from the current $0.40 dividend.

In other words, MGIC should return all of its $650 million of operating earnings to shareholders each year. This year, that means $2.25 per share. Next year, $2.45 because of fewer shares, and so on. All without any assumption of growing operating earnings, which will occur when ((A)) the housing market stabilizes, and ((B)) MGIC completes its transition to its low-risk strategy, which shouldn't be more than a year or two away.

Valuation. This stock is cheap

How much would you pay for a company earning $2.25 per share and growing by 8% a year? That growth rate is at least what the S&P 500 can generate long-term, and probably higher. The S&P 500 currently trades at an 18½ P/E ratio. That valuation puts MGIC's stock at $42, or a triple from here.

OK, financials never trade at the market multiple. But why not a 10 P/E? That's still a 45% multiple discount to the market. And over a 50% upside to the current price. So $25 is my target price.

For further details see:

Buy MGIC: 15% Cash Returns To Investors And Growing