MTG - Buy MGIC: Ramping Up The Cash To Investors

2023-11-02 10:33:30 ET

Summary

- MGIC, a private mortgage insurance company, offers high per share growth potential with steady insurance premiums and increasing investment income.

- The key parts of MGIC's income statement appear stable to improving - insurance premiums, investment income, operating expenses and, most important of all, mortgage default claims payments.

- MGIC has excess capital and plans to increase capital return to shareholders, making it an attractive investment opportunity.

- My target price is $25.

Sure, you can find some REITs and selected other stocks yielding double-digits. But one with a growth rate? We're now in rarefied territory. This is what MGIC (MTG), in the sleepy and largely unknown private mortgage insurance industry, offers you. I offer evidence in this piece that this bold statement has facts behind it.

Let's start with MGIC's just-announced Q3. It reported EPS of $0.64, or $184 million. I subtract off $11 million of cash claims payments and get an estimated $173 million of cash flow, or about $700 million annualized. Is this $700 million a reasonable run rate going forward? I say yes. Let's review the key income statement items for evidence.

Insurance premiums: Steady as she goes

MGIC earned $241 million of insurance premiums during Q3, a function of a 33 bp average premium and $294 billion of mortgage loans insured. Importantly, note that the 33 bp premium is net of 6 bp of premium paid to reinsurers who guarantee they will absorb a significant portion of MGIC's mortgage default claims payments in the event of a material recession.

Looking ahead, the 33 bp looks pretty steady. After years of declines because higher yielding - and far riskier - insurance rolled off, it has been stable all year. And MGIC raised prices a year ago.

The insurance portfolio also appears stable for the foreseeable future. National mortgage debt ground to a halt when housing affordability collapsed over the past three years in the wake of a nearly 40% increase in home prices and a rise in the mortgage rate from 3% to 8%. For example, Fannie Mae's mortgage-backed securities outstanding is up this year only 1% annualized. I don't expect much national mortgage debt growth until mortgage rates decline enough to bring back home sales. Fannie Mae expects flat home sales next year, at depressed levels.

Investment income: Up nicely

MGIC has nearly $6 billion in 3-4 year average maturity fixed income investments. That portfolio has taken a mark-to-market hit as interest rates rose over the past two years, but its earnings on the portfolio are rising as maturing debt is replaced at higher yields. Investment income rose by $52 million annualized over the past year. MGIC should add at least that much over the next two years.

Operating expenses: Pretty stable

It looks like MGIC operating expenses will come in at about $235 million this year, or less than 25% of expenses. MGIC said on its Q3 investor conference cal l " We do expect that there's capacity for us to decrease the expense ratio going forward".

Claims payments: The best news

In the event of default on a MGIC-insured mortgage, the company has to make a claims payment to the loan's primary insurer, namely Fannie Mae or Freddie Mac. MGIC's claims payments were $11 million during Q3, or $44 million annualized. To put that number in perspective, MGIC's claims payments for 2005 - the peak of a massive housing bubble - were $612 million! And that $11 million? $7 million were losses on loans made during that pre-2009 housing bubble! As a matter of fact, cumulative losses for all loans insured since 2009 are a mere $195 million.

Looking forward, I remain optimistic that claims payments won't rise much from here, for two reasons:

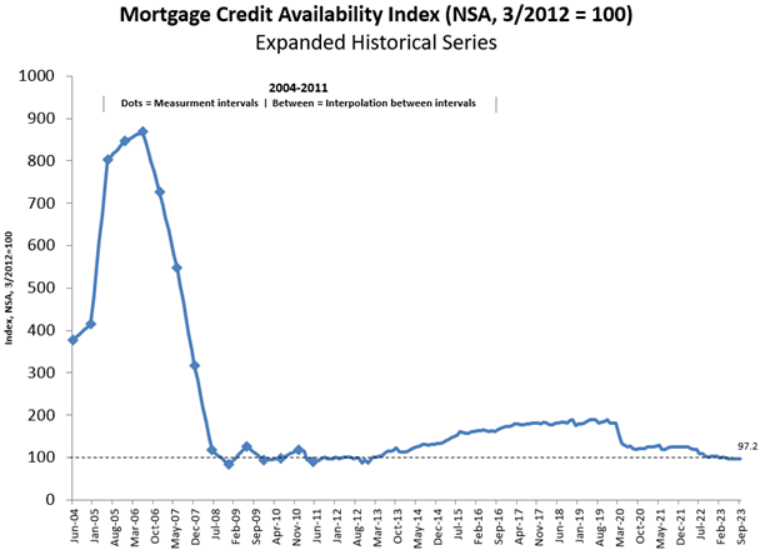

1. Underwriting standards remain conservative. That is the primary difference between pre- and post-2008 claims payments. Check out this mortgage quality index maintained by the Mortgage Bankers Association:

{kind=link}

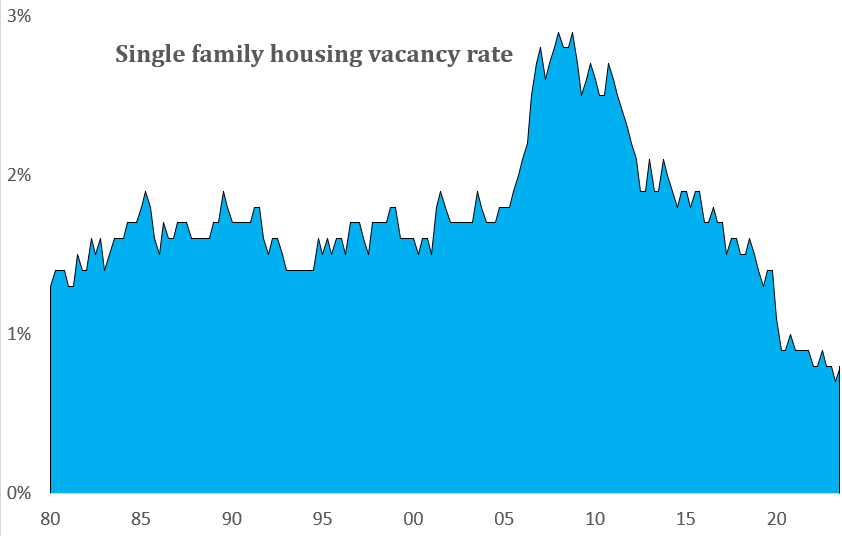

2. Housing remains in short supply. An excellent measure of the housing supply/demand balance is the vacancy rate. It sits right near its all-time low:

{kind=link}

How short are we on housing? Short enough that despite the record-setting rise in mortgage rates, S&P/Case-Shiller says that home prices just hit an all-time high in August.

Sure, home prices and home defaults are at risk to a major recession. But isn't the stock market as a whole at risk to that scenario also? And MGIC has loads of reinsurance protection in that event.

Capital: Sitting on a huge excess

MGIC's regulator establishes a capital requirement for MGIC based on ((A)) its mortgage volume insured, ((B)) the underwriting quality of those mortgages, and ((C)) the value of its mortgage reinsurance in reducing MGIC's share of losses. At the end of Q3, MGIC held $6.0 billion of regulatory capital, but was required to hold only $3.6 billion based on the factors above. That leaves $2.4 billion of excess, or $1.0 billion if MGIC wants to maintain at least a 40% excess capital cushion. That $1.0 billion excess could fund 25% insurance portfolio growth, meaning MGIC could comfortably fund the next five years of growth without needing to retain earnings.

The excess cash flow and its uses

I said above that MGIC's cash flow for Q3 was $173 million. Shareholders got $121 million of that cash flow, as follows:

- $33 million in dividends, or 11.5 cents per share.

- $67 million in share repurchases. The 3.9 million shares bought back reduced MGIC's share count by 1.3%.

- $21 million from the repurchase of a convertible debenture.

That $121 million is $1.70 annualized, or a 10% yield on the current stock price of $16.92.

I've made the case above that MGIC's cash flow going forward should be at least stable at $700 million a year, with some upside. I've also shown that MGIC need to retain any of that cash flow in order to fund growth. The logical conclusion, then, is that MGIC can pay out even more capital to shareholders going forward. And it seems management agrees! On the Q3 investor conference cal l, the company said:

"We expect our capital return payout will increase from the level in recent quarters, and you can begin to see that in our October repurchase activity."

In October, MGIC bought back 2.2 million shares. Annualized, that is a return of $450 million to shareholders. Add in the dividend, and the return to shareholders is over $2.00 a share, or a 12% return on the current stock. And because the buybacks will reduce MGIC's share count by nearly 10%, that means growth in cash return per shares of nearly 10%.

That is pretty interesting math, at least to me. My target price is $25. Consider joining me for the ride.

For further details see:

Buy MGIC: Ramping Up The Cash To Investors