ESNT - Buy Mortgage Insurer NMI Holdings. About To Turn On The Cash Hose

Summary

- My target price for this $23 stock is $40.

- Its biggest risk, claims payments on foreclosed homes, continues to be benign despite fears of another housing bubble.

- Its capital-light operating strategy is working very well.

- Industry pricing is stabilizing.

- Stock buybacks should sharply increase this year, and the beginning of a dividend payment is likely.

I write for Seeking Alpha about mortgage insurance stocks a lot. I usually write about MGIC (MTG), but today it's NMI Holdings (National Mortgage) (NMIH).

The reasons I keep telling you readers about mortgage insurers are (a) they are cheap, (b) their business models are shareholder friendly, and (c) their operating environment is positive. National Mortgage is no exception. Today's stock price of $23.35 is an embarrassingly low 6.5 times '23 expected EPS, and only 107% of book value. I believe a 10 P/E is achievable. My target price is therefore $40, or up 70%.

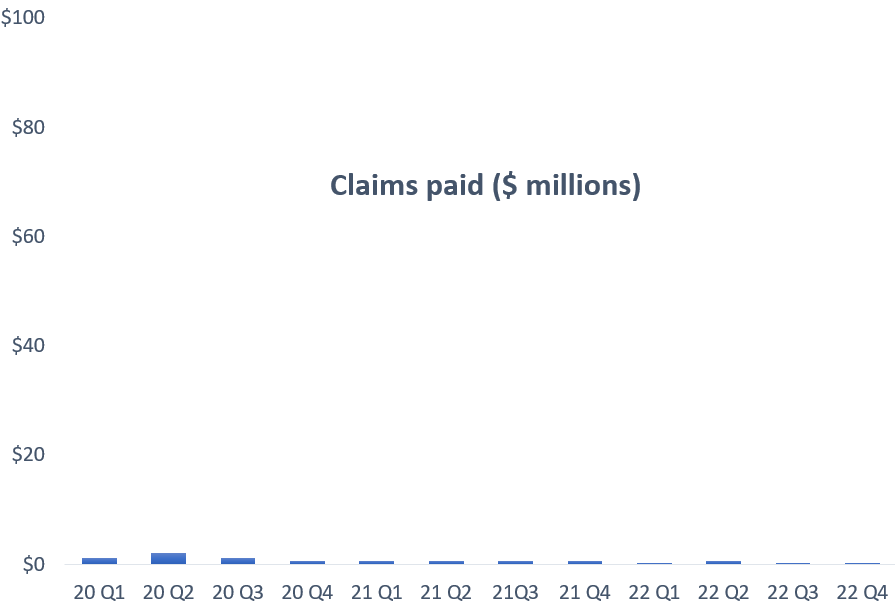

Claims payments are, and will stay, exceptionally low

National Mortgage's main earnings risk is a spike in claims payments on its mortgage insurance caused by a rise in mortgage foreclosures. The company has $184 billion of mortgage insurance outstanding, and in the worst case - all of the mortgages default - stands to lose $48 billion. That's a lot, right? For example, in 2005 peer company MGIC paid out $612 million in claims on its $170 billion in insurance in force. So let's take a look at National Mortgage's recent quarterly claims payments, setting the range of the chart at $100 million a quarter to reflect MGIC's losses:

{kind=link}

National Mortgage's claims payments are less than one-tenth of 1% of MGIC's losses two years before the housing crisis hit. How come they are so much lower? I'll summarize three of the major reasons (I've addressed them in detail in many prior Seeking Alpha articles) and then drill down on the 4th because of new information. The four are:

- Far better underwriting. 2005 was during the bad old days of aggressive subprime mortgage lending. Home mortgage underwriting has been exceptionally clean for over a decade.

- A far more favorable housing supply/demand balance. In 2005 the country had 1 million excess housing units, on its way to 2 million by 2007. Today, we have a nearly 2 million shortfall.

- Less unemployment risk. In 2005, there were 8 million unemployed people and 4 million job openings. Today there are only 6 million unemployed people and a near-record 11 million job openings.

- Mortgage payments are highly affordable. How can I say that when home prices spiked by 35% since the Pandemic and mortgage rates are over 6%, from a recent low of 3%? Because the mortgage insurers' policies weren't all written yesterday. Mortgage insurer Essent reported the average mortgage rate for its borrowers by year in its recent Q4 earnings press release. I added cumulative changes in the Shiller home price index. Here is a table of the results:

Essent Q4 '22 earnings report, Shiller home price index

Essent's average customer has only a 3.9% mortgage rate and has 20% appreciation on their home! National Mortgage is certainly similar. The fact is that the bulk of its customers has very affordable mortgage payments.

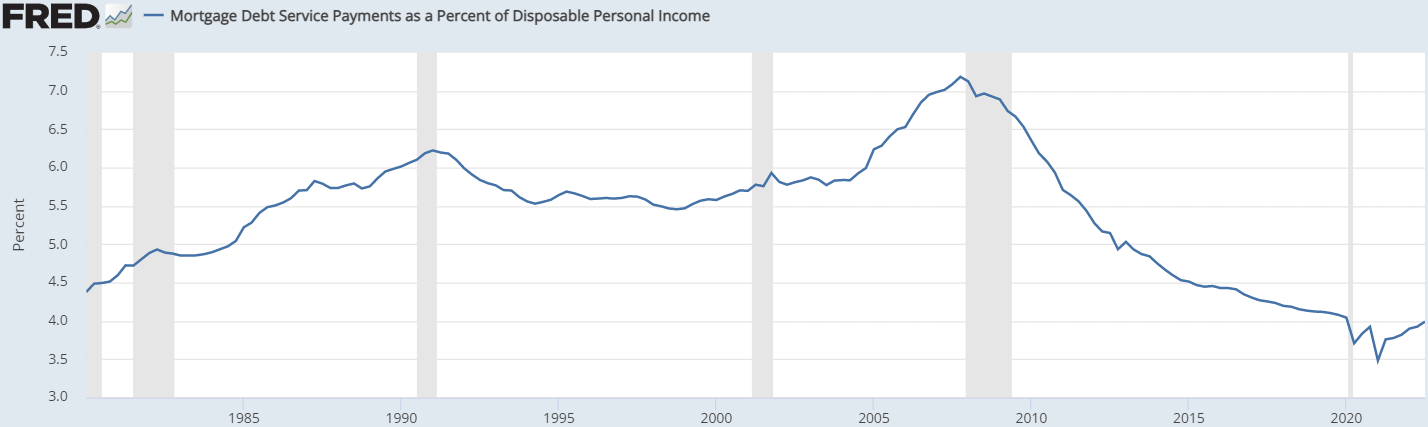

Further evidence is supplied by our good friends at the Federal Reserve . They calculate a ratio of mortgage debt service payments as a percent of personal income. Here it is:

{kind=link}

We are just off at least a four-decade-long bottom, compared to a near-record level in 2005. Conclusion: The great bulk of homeowners will fight tooth and nail to keep their low housing payments, come what may in the economy.

National Mortgage's capital-light strategy is literally paying dividends, with lots more to come

National Mortgage, like every other insurance company, is required by regulation to hold capital to make sure that it has the funds available to pay claims, even in a stressful environment. As I said above, National Mortgage has can lose a maximum of $48 billion, called its risk in force. Mortgage insurance regulators require the companies to hold about 6.5% in capital against their risk in force, or about $3.1 billion. But National Mortgage's actual regulatory requirement is only $1.2 billion. How?

Because National Mortgage reinsures a substantial part of its risk, by two means:

- Quota sharing. National Mortgage currently has shifted 26% of its risk to reinsurance companies. That reduces National Mortgage's capital requirement by about $0.8 billion.

- Excess of loss reinsurance. National Mortgage has covered the great bulk of its risk in force with agreements that absorb losses above a minimum amount (generally 2.0-2.5% of cumulative losses) up to a maximum (generally 6.5-7.0%). The best way to think about excess of loss insurance is that National Mortgage has to pay for a normal recession, but gets a lot of help in a bad recession, then pays again in a housing depression. These excess of loss agreements reduce National Mortgage's regulatory capital requirement by about $1.0 billion.

Why does National Mortgage pursue this capital-light strategy?

For one, it clearly pays off in a bad recession. But in good housing times like now, it has to pay the reinsurers without having many losses to share. That seems bad. But the following math shows why this strategy benefits shareholders now:

Super-cheap capital. For 2022 National Mortgage paid its reinsurers $84 million and got $2 million of losses paid. But that $82 million of net expense reduced its capital needs by $1.9 billion. That's an after-tax cost of capital of a mere 3.5%! At a 7 P/E, National Mortgage's actual cost of equity capital is more like 15%. A bargain.

The ability to grow. National Mortgage grew its insurance in force by 21% last year. Without reinsurance, that growth would have required an additional $575 million in capital. But National Mortgage earned only about half of that. So without reinsurance, it would have had to restrain growth or sell more stock. Instead, in 2022 National Mortgage not only added lots of new business but also added over $300 million of excess capital and gave shareholders $56 million through share repurchases.

Lots of money is heading towards shareholders. National Mortgage is now sitting on $1.2 billion of excess capital, or $750 million even after assuming a 35% cushion to regulatory capital. And its insurance in force growth will slow this year because of slower home sales. So it could end this year with $1.0 billion of above-cushion excess capital. I think this is the year that National Mortgage starts to aggressively return capital to shareholders. I am confident that share repurchases will rise, and I believe it will start paying a dividend. Peers MGIC and Radian are already paying out substantial cash to investors.

Revenue growth is about to turn up

In this growth-obsessed investment world, National Mortgage and its peers have committed the cardinal sin of minimal revenue growth. For example, despite its 21% growth in insurance in force, '22 revenue growth was only 8%. And in '21, the numbers were even worse - 37% insurance growth generated only 13% revenue growth. In other words, the average insurance premium National Mortgage earned has been declining.

Three factors have been pushing National Mortgage's premiums earned lower:

- Increased use of reinsurance meant more ceding of premiums to those reinsurers.

- The capital-light strategy meant that the mortgage insurers could earn very attractive returns even with lower earnings. For example, National Mortgage's return on regulatory capital last year was about 25%, huge for an insurance company.

- As mortgage defaults kept declining over the past decade, the mortgage insurers felt comfortable charging lower prices.

But it appears that the pricing bottom has been reached. For example, from National Mortgage's Q4 earnings conference call :

"We expect our core yield, which strips away a lot of the noise of our reinsurance program and cancellation earnings will be generally stable through the year."

And from peer Radian's Q4 conference call :

"We've been increasing our pricing to reflect the environment and continue to see evidence of price increases among our mortgage insurance peers as well."

Finally, from Essent's Q4 call :

"We expect that the net earned premium rate for the full year 2023 will be largely unchanged from the fourth quarter rate of 34 basis points."

You get the idea.

What this means for earnings per share - steady growth

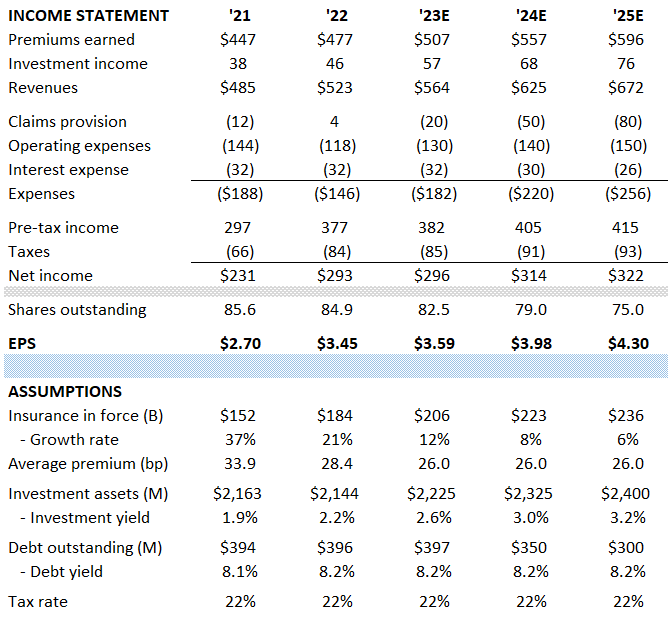

Here is my simple earnings forecast model:

{kind=link}

My key assumptions are derived from my views on credit and pricing that I detailed above:

- Insurance in force growth slows down because of slowing U.S. mortgage debt growth and National Mortgage maturing.

- The average premium bottoms this year and stabilizes.

- Claims paid rise moderately because of flat home prices and a moderate rise in the unemployment rate.

- Shares outstanding decline as National Mortgage expands its share buyback program.

My resulting EPS estimates are very close to the Wall Street average, as compiled by Seeking Alpha .

The catalysts for my $40 target price

One catalyst is simply time. Many investors still fear that the housing market is in a bubble and will revisit its '07-'11 blow-up. As that continues not to happen, they will gain confidence in the mortgage insurers' earnings.

The other catalyst is the fact that the great majority of its earnings going forward will be free cash available to pay shareholders. I expect National Mortgage's stock buybacks this year to far exceed last year's $56 million. And I expect it to initiate a dividend this year, or next year at the latest.

For further details see:

Buy Mortgage Insurer NMI Holdings. About To Turn On The Cash Hose