NVEC - Buy NVE Corporation: Bargain Growth Valuation Won't Last

2023-08-19 04:23:28 ET

Summary

- NVE Corporation is a small semiconductor company with patented technologies for miniature-sized, low-energy, durable sensors and MRAM memory products.

- The company's stock quote has risen nicely over the last 14 months, but remains undervalued with strong profit margins and returns on capital.

- If the company continues to grow at its current rate, the stock price could potentially double to $150 a share in the next 12-18 months.

I have written several bullish stories on a small Minnesota semiconductor company, that makes its product in-house, with patented technologies for miniature-sized, low-energy, durable sensors and MRAM memory chips (used in rugged applications like hearing aids and smart vehicles). The good news is NVE Corporation ( NVEC ) has experienced a nicely rising stock quote in kind over the past couple of years, although underlying operations have been compounding even faster for growth and returns.

So, at $77 a share in the middle of August, investors can buy a superbly run business, with some of the strongest profit margins on sales and returns on capital of any company in America, at a "growth valuation" that may be as cheap as last summer. The upside bonus is you still get a 5%+ annual dividend yield, now easily covered from regular earnings and its large cash stash (vs. an almost liability-free balance sheet).

My last article on NVEC was posted in June 2022 here . Since then, the stock has outlined a total return of +71% vs. the equivalent S&P 500 index price gain of +12% and total return of +13.7%.

{kind=link}

Seeking Alpha Article - Paul Franke, NVEC, June 27th, 2022

Valuation Buy Argument

Believe it or not, the current business valuation on EPS and sales is about the same as last summer, despite the major uptick in share pricing. A somewhat disappointing June quarterly report has dinged the share price about -20% over recent months. My thinking is this has opened another great opportunity to acquire shares. Why?

The answer is, growth has returned with a thump over the last 18 months, delivering its highest rate of expansion in about 15 years. Below, I have graphed the big jump in both EPS and revenues measured from the 2020-21 pandemic lows in customer demand. You will notice both numbers have roughly DOUBLED over three years. This works out to a compounded annual rate near 25%.

{kind=link}

Seeking Alpha - NVE Corp, Annual EPS, Since 2016

{kind=link}

Seeking Alpha - NVE Corp, Annual Sales, Since 2016

If growth continues as management expects, and I am forecasting at rates of 15% to 25%, today's trailing P/E of 16x is simply too low. This is a discounted number vs. the S&P 500 forecast of 19x for 2023 . Plus, on forward 1-year results, NVEC's P/E could easily be trading under 14x (good for a 7% earnings yield on investment).

YCharts - NVE Corp, Price to Trailing EPS & Sales, 10 Years

Anyway you slice it, shares are likely valued at a PEG Ratio (P/E divided by earnings growth rate) well under 1.0, traditionally considered buy territory by Wall Street. PEG could be as low as 0.6x forward income levels if 25% annualized growth is maintained.

Other fundamental data points are sitting at a low-growth level, not the solid to rising growth reality. Subtracting out $53 million owned in cash and municipal bonds from the present equity market cap of $370 million at $77 per share (NVEC has zero debt and under $2 million in total liabilities), enterprise valuations remain depressed. Trading multiples of 13.6x EV to EBITDA and 9x sales are actually not far above 10-year lows.

YCharts - NVE Corp, Enterprise Valuations, 10 Years

I dare you to find another business with no debt and profit margins anywhere near the NVE Corp. setup. In addition to this good news for shareholders, operating and final after-tax margins above 50% on sales are honestly improving from rising interest income on its cash and long-term bond investments (with climbing interest rates in America).

YCharts - NVE Corp, Profit Margins, 10 Years

Technical Trading Picture

Measured from my last article, NVE Corp. has strongly outperformed the semiconductor industry ( SOXX ), Big Tech ideas ( QQQ ), the S&P 500 index ( SPY ), and smaller cap equities ( IWM ). Over less than 14 months, company total returns have beaten the U.S. market by about +50%!

YCharts - NVE Corp vs. Peer/Alternative Indexes, Total Returns, 14 Months

Following a huge earnings blowout report for the March quarter, June's quarterly results were a little disappointing, with YoY normalized EPS growth of 15% (excluding items) and sales expanding by 20% over the June 2022 period. The end result is price has zigzagged right back to where it traded before the March beat was announced.

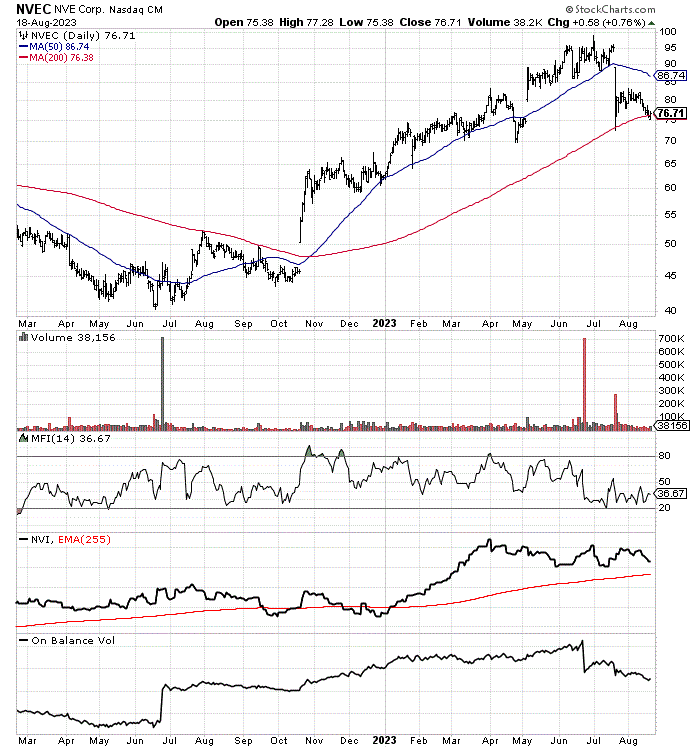

Today, price is bumping up against its 200-day moving average, which may or may not hold in coming weeks. I prefer that any downward move under $75 a share is short-lived. My feeling is price should hold above $70, assuming a stock market crash generally on Wall Street is not approaching into the seasonally-volatile autumn months.

The 14-day Money Flow Index has been stuck under 50 for better than two months, similar to recent past bottoms in price during August-September and March-May 2022.

The Negative Volume Index and On Balance Volume indicators look relatively healthy over the intermediate term, although both diverged at the late June price peak at $100.

{kind=link}

StockCharts.com - NVE Corp, 18 Months of Daily Price & Volume Changes

Final Thoughts

All told, if the business can grow in 2024 like it has in 2023, I am projecting price could rise into the $125 to $150 share range over the next 12–18 months. Looking at the raw math, the current valuation is roughly a 40% discount to its trading history over the last decade (on price and EV to sales and earnings).

If the trailing EPS rate of $4.75 increases into the $6 per share area (25% growth rate) by the end of calendar 2024 (which is my forecast), I find it difficult to justify price falling much below today's quote, even given a global recession backdrop (assuming such happens, which it may not). In fact, $6 in earnings generated by a top-notch A+ balance sheet, with incredibly high and sustainable profit margins, deserves a major premium valuation in my book. A 25x multiple on $6 EPS supports $150 for price, not the current $77 quote.

What are the risks? Unlike the majority of U.S. semiconductor companies that actually produce chips in Asia or elsewhere, NVEC's supply chain is limited to raw materials imported from outside of Minnesota. The company is not directly affected by rising interest costs with zero debt. Its main building is leased over a number of years, and could easily be replaced with another location. Lastly, a cash/investment position greater than annual sales should cushion the impact of a major recession, at least in terms of going-concern liquidity.

With rapidly improving customer acceptance of its products and the value proposition of supporting American-made devices (think new customers each quarter), the long-term outlook for NVEC's business is excellent.

My biggest concern for share pricing is the macro future for U.S. stock market direction. Our equity market remains quite overvalued using the Shiller P/E indicator, or total market cap to GDP ratio. So, another -20% bear market decline could hold NVEC in check, although it's possible price may be able to fight any macro drawdown if growth rates remain positive.

My only debate is whether to put a Buy or Strong Buy rating on shares. If you can purchase the stock under $75, I am leaning toward a strong buy with my money. Today, NVEC is one of my largest holdings outside of the gold/silver sector (hedges on rising long-term inflation and a recession). My trading plan is to add shares on any price weakness going forward.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Buy NVE Corporation: Bargain Growth Valuation Won't Last