CUZ - Buy Office If You Missed Mall And Hotel Renaissance

2023-06-20 03:56:15 ET

Summary

- The office real estate market has suffered due to the work-from-home trend and aggressive monetary policy, leading to investor pessimism.

- Similarities can be drawn to the mall and hotel segments' sell-offs during the pandemic, with some companies recovering and providing strong returns for investors.

- To profit from the office crisis, investors should focus on large-cap companies with strong balance sheets, high-quality assets, distant refinancing profiles, and lease expirations.

Since the Fed began raising interest rates back in early 2022, the office market has gone from bad to worse. Already during the pandemic period, many office property owners suffered drastic losses of capital due to a sudden paradigm shift in how people work. Namely, the work-from-home movement did inflict a serious damage on the occupancy rates and rendered the office supply/demand dynamics unfavourable.

So, the combination of increasing number of employees working from home and the aggressive monetary policy has caused severe direct and indirect consequences on the office real estate.

Here are the main factors explaining the overall pessimism among investors towards the office real estate space:

- A significantly accelerated work-from-home trend , which reduces the demand for office space (both new and existing), especially that of low quality.

- Surging interest rates , which put a downward pressure on the valuations and make it harder for office players to maintain growing or even stable FFO generation levels.

- Tight lending conditions coupled with a significant slowdown in capital markets activity , which diminishes the accessibility to sound financing.

- Huge cost inflationary factors impose material headwinds for accretive redevelopment activities, which in most cases are per definition very expensive (e.g., repurposing standard office building to a residential property).

{kind=link}

The 3-year historical total return performance chart clearly confirms that office REITs are currently out of favour. The S&P 1500 Office REITs Sub-Industry Index has diverged from the overall REIT market and the S&P 500 by ~52% and ~87%, respectively.

In this article I will outline the similarities of the relatively recent sell-offs in the mall and hotel segments, and provide a couple of pillars, which should be considered to materialize the current opportunity in the office REIT market.

Elimination of low quality stocks in the mall segment (2020-2021)

The outbreak of COVID-19 sent a major shockwave across the entire retail sector. Many retailers were forced to close down their operations due to a sharp loss in the foot walks (physical sales) and a massive shift towards e-commerce channels. Retailers that were hit the most had relatively weak balance sheets, already tight margins and no direct economic moat. And there were many of this kind.

Consequently, mall operators also got hit hard by the amounting bankruptcies, which in turn impacted their operations via:

- Higher vacancy rates at times when the supply stock (from bankruptcies) was rapidly outpacing the demand.

- Partially captured rents.

- Stricter financing conditions due to massive uncertainty in the overall retail market at that time.

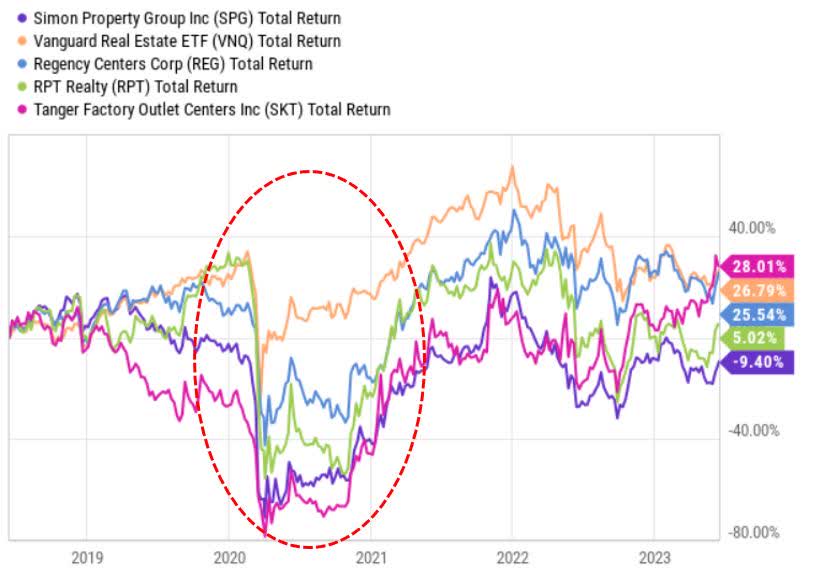

The stock market was heavily discounting the mall REITs (and other REITs with similar factor exposures, i.e., shopping centers).

{kind=link}

The negative dynamics surrounding mall REITs back in 2020-2021 were very similar to those of what we currently can observe in the office segment. In fact, many mall REITs went belly up during this turbulent time period.

For instance, Washington Prime Group Inc, Pennsylvania Real Estate Investment Trust (PRET) and CBL & Associates Properties, Inc. (NYSE: CBL ) filed for Chapter 11. Macerich (NYSE: MAC ) was forced to significantly dilute its shareholder base to survive.

{kind=link}

However, now the company - Simon Property Group (NYSE: SPG ) -, which survived that period has come back with a vengeance providing investors, who entered right when there was 'blood on the streets', with fat and juicy returns. SPG investors have almost doubled their money capturing strong alpha returns relative to the broader REIT market.

Depressed hotel REITs in the pandemic world (2020-2021)

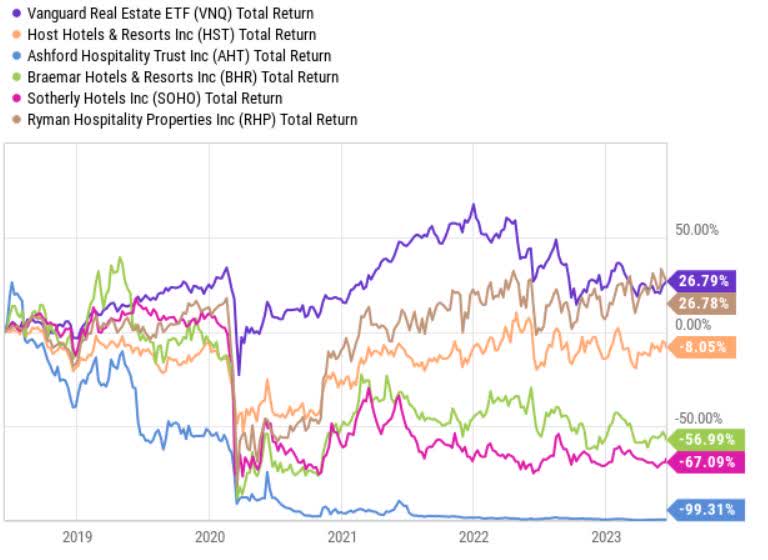

Even more pronounced consequences of the COVID-19 were felt by the hotel REITs. Many of hotel REITs saw their revenues completely destroyed with huge uncertainty on future cash generation.

{kind=link}

In other words, from 2020 to 2021, hotel REITs were subject to the same treatment as currently the office REITs are experiencing. There was a significant uncertainty on whether the overall hotel market will be able to survive without massive equity dilutions and / or bankruptcies. Lenders were extremely hesitant to refinance maturing debt obligations. Many analysts feared that a structural shift has taken place in terms of the long-term demand for hotels, which in turn was set to put a secular downward pressure on pricing power and occupancy rates. As a result, the market panicked and discounted hotel REITs accordingly.

{kind=link}

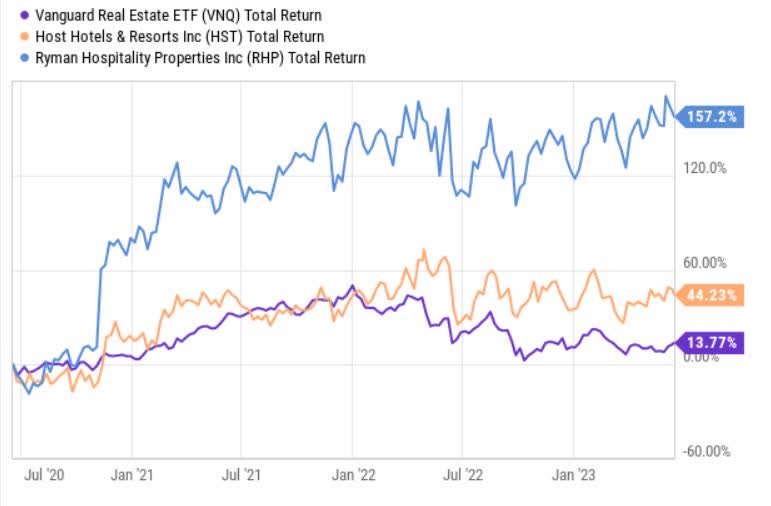

Nevertheless, as it was for the mall case, once the market normalized and achieved equilibrium, several hotel REITs enjoyed well-deserved returns stemming from recovering cash generation and valuation multiple expansion.

{kind=link}

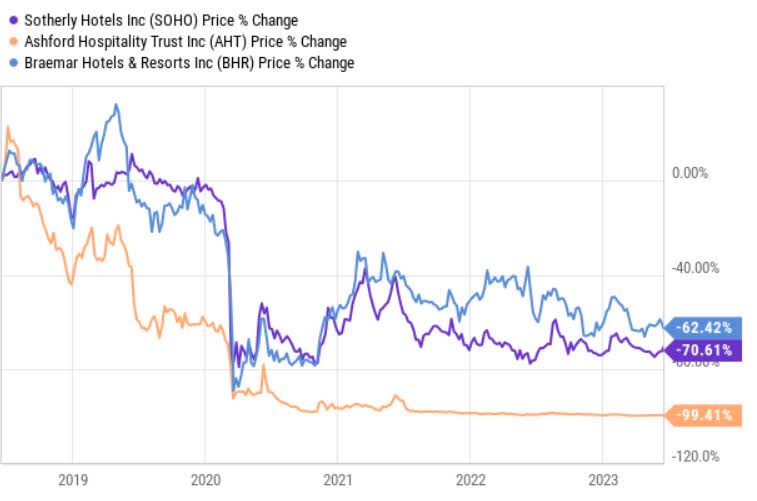

Granted, several lower quality hotel REITs have not yet recovered despite the positive sector-specific tailwinds. Similar to a mall situation, the 2020-2021 period resulted in some bankruptcies. For instance, currently Ashford Hospitality (NYSE: AHT ) is one step away from going belly up.

5 aspects to consider to profit from the office crisis

The prevailing situation in the office market embodies many similar characteristics, which resemble the previous turmoil in mall and hotel REIT sectors.

Reflecting back and seeing now which REITs have survived and which have suffered permanent impairment of capital, we can make justified conclusions about what pre-conditions office REIT champions have to possess to survive and deliver alpha once the market reverts back to normalcy.

- Be greedy when others are fearful. The only way to profit from the office opportunity is by actually opening up an exposure towards the sector via stocks that are underpinned by the following characteristics:

- Large cap and fortress balance sheets. Looking at the survivors and those mall and hotel REITs, which have successfully bounced back without any equity dilutions, it is very obvious how the investment graded balance sheets and large capitalizations factors came in handy. Having fortress balance sheets and sufficient scale is critical to access capital from diversified sources. Ultimately, this allows the companies to achieve two things: (1) secure financing at favourable terms (both cost of financing and maturity profile) and (2) act opportunistically on the M&A and development front to capture high-yielding cap rates.

- High quality assets. A common pattern among the hotels and malls, which are now thriving and exceeding market is the notion of having an exposure towards top class assets. This is also what we see happening in the office markets, where A and trophy buildings are showing solid signs of resiliency and favourable like-for-like development, while B and lower class buildings are facing surging vacancy rates and depressed rent levels. In real estate business there is a famous saying, which holds true especially in this market situation - i.e., location, location, location. Namely, location is everything.

- Distant refinancing profile. No matter the state of balance sheet and overall accessibility to sound financing, it helps to have refinancing events during times when the financiers are not extremely pessimistic about the sector the company operates in. This way the odds are increased for securing more favourable financing. In the context of the current office market dynamics, REITs, which have no or very minimal refinancing needs in the next 2-3 years, are likely to avoid the short-term volatility in the financing and capital markets.

- Distant lease expiry profile. In addition to a distant refinancing profile, having a well-laddered and relatively back-end loaded lease maturity dates helps. Currently, it is a 'tenant' market, where the bargaining power has clearly shifted in the hands of tenants. Usually, lease renewals imply a lock-in of negotiated lease/rent level for at least couple of year ahead. The further the lease maturity dates are, the less risk there is that an office REIT will be forced to sign rent agreement at a notable discount to the existing level.

In closing

In my humble opinion, the market currently offers another opportunity for investors to achieve alpha over a medium-term time horizon. This time it lies in the office REIT space, which has many parallels with the recent sell-offs in the mall and hotel REIT segments.

To capitalize on this opportunity, investors have to find high quality gems, which carry strong investment grade balance sheets and have structured their cash flows (financing and rents) in a manner, which allows to act opportunistically and avoid significant renegotiations of lenders and tenants over next 12 - 24 months.

Looking at the prevailing landscape of publicly traded office REITs, there are at least two solid candidates, which comply with the aforementioned aspects.

Cousins Properties (NYSE: CUZ )

- Durable portfolio diversified across favourable geographies.

- Fortress balance sheet that supports growth in a prudent manner.

- Distant lease expiries and debt maturities.

- Depressed valuation levels and a reasonable probability of mean reversion.

- Attractive development pipeline.

See more details in my recent article on CUZ here: Cousins Properties: Major Signs Of Resiliency In The Q1 Figures

Alexandria Real Estate Equities, Inc. (NYSE: ARE )

- A and A+ properties based in favourable geographies.

- Upper investment grade balance sheet and large cap status.

- Distant debt maturities (no refinancing until 2025) and positive trends in the recent financing transactions.

- Strong like-for-like performance despite negative sector-specific backdrop.

See more details in my recent article on ARE here: Alexandria Real Estate: Upgrading Rating To Buy, I Disagree With Jonathan Litt

For further details see:

Buy Office If You Missed Mall And Hotel Renaissance