VLKPF - Buy Porsche Holding Instead Of Porsche AG Directly

Summary

- Porsche Automobil Holding SE (Porsche Holding) is a holding company different from Dr. Ing. h.c. F. Porsche AG (Porsche AG).

- Porsche AG produces the iconic Porsche cars and is a brand within the Volkswagen group.

- Porsche Holding controls Volkswagen, as it owns the majority of Volkswagen AG ordinary shares. It also owns a significant part of Porsche AG directly.

- The Porsche AG IPO in September 2022 has been especially beneficial to Porsche Holding.

- The net asset value of its Volkswagen shares alone is less than the Porsche Holding market cap - making Porsche Holding a very cheap play on Porsche AG.

Thesis

(Note: all amounts in the article are in EUR. At the current exchange rate this is almost equivalent to USD.)

The Porsche and Volkswagen group of companies have a complicated ownership structure. This has resulted in a discount to the share price of Porsche Automobil Holding SE ( OTCPK:POAHF ) ( OTCPK:POAHY ) and also Volkswagen AG ( OTCPK:VWAGY , OTCPK:VWAPY , OTCPK:VLKAF , OTCPK:VLKPF ). The IPO of Dr. Ing. h.c. F. Porsche AG (DRPRY) ( OTCPK:DRPRF ) in September 2022 has added complexity and has increased the discounts.

Porsche Holding SE controls Volkswagen as it owns the majority (53.33%) of Volkswagen AG ordinary shares and 31.4% of the total capital. In parallel to the Porsche AG IPO, Porsche Holding acquired 25% + 1 share of Porsche AG ordinary shares and now owns 12.5% of Porsche AG directly in addition to the 24.9% it owns indirectly through Volkswagen.

The current NAV of its Volkswagen shares is EUR 12.6bn, compared to a market cap for the Porsche Holding shares (ordinary shares not publicly listed) of EUR 8.4bn. And those Volkswagen shares look cheap by themselves, see my recent article on Volkswagen for more on that. Other recent articles on Seeking Alpha express the same view regarding a Volkswagen undervaluation.

Porsche Holding paid 10.1bn to acquire the stake in Porsche AG. 2.2bn was conveniently paid through a special dividend from Volkswagen (actually 3.1bn, but Porsche Holding has to pay capital gains tax) and the remaining 7.9bn are debt. Considering the increase in the Porsche stock price since the IPO, the NAV has increased from 2.2bn to 3.82bn. I assume that the 7.9bn debt can be repaid at least to a large extent through Porsche AG dividends alone, if not in full. Not surprisingly Porsche AG has committed to a 50% pay-out ratio. Profit after tax for Q1-Q3 2022 was a handsome 3.86bn.

Additional IPOs of Volkswagen brands could financially benefit Porsche Holding and enable it to increase its share in Porsche AG if they follow the same structure as the Porsche IPO (more on that later). Audi is the most likely candidate here.

All this makes Porsche Holding an interesting and cheaper alternative way to invest in Porsche AG, the Porsche car manufacturer.

Porsche Holding SE overview

I want to start with an overview of Porsche Holding and the group share structure. If you would ask somebody to come up with a complicated corporate and share structure, the various Porsche and Volkswagen companies and share categories would be a decent outcome.

Porsche Holding SE is a holding company that owns Volkswagen AG shares and after the IPO also Dr. Ing. h.c. F. Porsche AG shares, the company that actually produces the iconic Porsche cars.

According to its Q3 report, the company has only 36 employees. It categorizes holdings into longer term core holdings and shorter term portfolio holdings. The core holdings are Volkswagen AG and Dr. Ing. h.c. F. Porsche AG. Both together make up more than 99 percent of Porsche Holding assets.

Portfolio holdings are smaller investments that are held over a certain period of time. Due to the small size, portfolio holdings are quite irrelevant in any discussion about the valuation of Porsche Holding, so I will not discuss them here. (This does not mean they are not interesting. In November Porsche Holding e.g. invested in Xanadu, a start-up that develops quantum-computing technology. For those who are interested please find the list of portfolio holdings here .)

Share and ownership structure

Shares of Porsche Automobil Holding SE are equally divided into 153,125,000 ordinary shares with voting rights, and the same number of preferred shares which do not have voting rights. The preferred shares are publicly listed. There are also corresponding ADRs which are traded in the U.S. For U.S. investors ADRs generally should be the better choice, as the preferred shares have no voting rights anyway.

All ordinary shares of Porsche Holding are owned by the Porsche/Piëch family, going back to the founding of Porsche and Volkswagen.

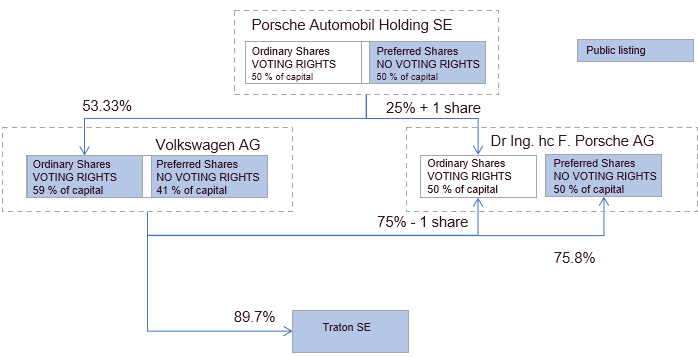

With the similarity of names and different share structures, it can be difficult to understand who owns what and how. I hope the following picture helps:

{kind=link}

Source: Author based on company information

Porsche IPO

It also can be difficult to understand what happened in the Porsche IPO, as important things were done outside of the IPO, are but very much related to it. Although not a direct party to the IPO, Porsche Holding was the most significant beneficiary from it, in my opinion. Here is a quick recap of the IPO and what was done:

- At the start of the IPO, Porsche AG was a fully owned subsidiary of Volkswagen. This was not always the case and the history behind it is quite fascinating, but beyond the scope of this article. There are several articles on Wikipedia that are actually quite helpful if you are interested. A good place to start is the Porsche SE page . I recommend reading the articles if you are an investor in Porsche or Volkswagen or are interested in becoming one. It gives you a useful context on the decision making in the group, but it is also quite interesting stuff for those who like a corporate soap opera.

- In the first step Porsche AG's share structure was changed, so that there are 455.5 million ordinary shares and the same number of preferred shares (with no voting rights), totaling 911 million shares overall, a nice play on the company's most famous and iconic Porsche 911 car model. Holders of the preferred shares receive an additional dividend of 0.01 euros per share on top of what is paid out on ordinary shares. At the IPO price of EUR 82.5 this is a meagre 0.012%.

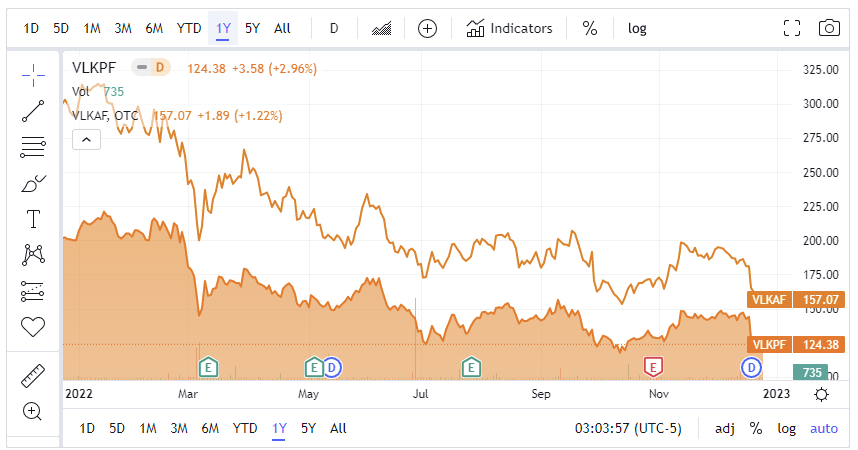

- Next, Volkswagen AG sold 25% + 1 share of Dr. Ing. h.c. F. Porsche AG ordinary shares to Porsche Holding SE at a premium of 7.5% to the IPO price of EUR 82.5, so for 88.69. Porsche Holding SE owns the majority of the voting rights of Volkswagen AG, so you could say they gave it to themselves. I suppose there was some governance around how the 7.5 percent were determined, but it seems low to me. As a reference, Volkswagen AG has a similar dual share structure. But the premium of Volkswagen AG ordinary shares on the preferred shares is 24 percent, and it has been around this number for all of 2022 (see chart below). The gap was closer in previous years, but still the 7.5% premium seems too low in comparison. Anyway, for Porsche Holding shareholders it was certainly not a bad deal.

{kind=link}

Volkswagen AG ordinary and preferred shares over 2022 (Source: Seeking Alpha)

- Volkswagen also sold 25% of preferred shares in the actual IPO. Significant parts of this were pre-assigned to large institutional investors, especially the Qatar Holding.

- In total Volkswagen received EUR 19.5bn from the whole exercise, the IPO plus the sale of ordinary shares to Porsche Holding.

- In December 2022 it gave out half of that as a special dividend to its shareholders. There was criticism about the huge pay-out from retail shareholder groups , but for Porsche Holding it was again a very good deal, as it helped to reduce the debt financing:

Porsche Holding debt financing for Porsche AG ordinary shares acquisition (Source: Porsche Holding SE)

- One additional row was that the State of Lower Saxony did not want to receive the money in 2022, so the shares went ex-dividend in December 2022, but the payment comes weeks later in 2023, so for many shareholders inconveniently in a different tax year. The State of Lower Saxony has a 20% minority stake in Volkswagen ordinary shares, but through the so called ‘Volkswagen law’ this minority stake gives them a veto right on significant decisions. Important decisions such as changes to the Articles of Association and capital increases can only be made with a majority of more than 80 percent of the votes.

Porsche AG valuation

Porsche AG is by far the most profitable brand within the Volkswagen Group. For Q1-Q3 2022 Porsche accounted for only 6% of vehicles sold, but 16% of the total revenue and 32% of the operating result.

While all segments increased revenue and operating profit on the back of higher unit prices, Porsche was the only segment of the group that also managed to increase vehicle sales YoY, from 209,000 to 221,000. Porsche’s operating margin was an outstanding 19.4% in Q1-Q3 2022 with an average vehicle price of EUR 110,000.

Especially nice to see is that the EV share was 11% of deliveries, despite the limitation that Porsche has so far only one EV model on the market. Going forward, I expect Porsche to benefit from the scale of the Volkswagen group regarding its transition to EVs through investments in platform, EV charging infrastructure, software etc., while the separate listing allows the higher P/E ratio due to the superior economics of the brand.

On the flip side, with a 2022 P/E ratio of 17 Porsche AG is not cheap for an auto manufacturer. I would assess it as fairly valued at the moment, but with future potential.

All three large German auto manufacturers - BMW, Mercedes and Volkswagen - have managed to increase profits and cash flows in 2022 significantly, but investors have not rewarded this. The market is forward looking and, among other things, sees the risk of a recession in 2023. I think that Porsche with its lower units sales, but higher profit margins is in a better position than its parent Volkswagen, but also BMW and Mercedes, who need much higher unit sales and are more sensitive to price pressures. Mercedes did actually lower its EV prices significantly in China just recently, as did Tesla. I do not expect Porsche to do this and I like that they managed to increase both unit sales and prices in 2022.

Additional IPOs of other Volkswagen brands

The Porsche IPO was quite successful, raising 19.5bn for Volkswagen. Afterwards, Porsche AG CEO Oliver Blume (see the German newspaper Handelsblatt ) said that he wants to focus the group more on the capital markets. He asked all brands to prepare what he called “virtual equity stories” to sharpen their focus on brand identity, market positioning and economic performance.

I do not think that actual IPOs will follow these exercises in the immediate future, but if all goes well, Audi is a potential candidate in maybe one or two years. The other Volkswagen luxury brands - Bentley and Lamborghini - are probably too small to have a meaningful impact.

Porsche Holding investors should benefit from any future IPO as they did from the Porsche IPO. So this is a potential additional bonus down the road.

Conclusion

If you hold Porsche shares and have a good opinion on the business, you can do worse than owning the stock, but you should think about switching to Porsche Holding; especially if you have been holding the stock since the IPO as you can realise your gains.

For new investors who are interested in owning a Porsche, I recommend buying Porsche Holding instead. Directly, and indirectly through Volkswagen, Porsche Holding owns 37.3% of Porsche AG. I think Porsche Holding is undervalued and a better way to invest in Porsche than going directly through the Porsche AG preferred shares. This should get more obvious over time as Porsche Holding uses the dividend from Porsche AG to pay back the debt it took on for the acquisition, continuously increasing the NAV.

Most U.S. investors are probably better off not buying the Porsche Holding shares directly, but the U.S. ADRs ( OTCPK:POAHY ). As the preferred shares do not have voting rights anyway, there is not a meaningful difference for U.S. investors.

For further details see:

Buy Porsche Holding Instead Of Porsche AG Directly