FCPT - Buy Small Inefficient Net Lease REITs As Current Environment Favors M&A

2023-12-08 22:50:27 ET

Summary

- Elevated capital costs will lead to investors favoring efficiency, resulting in a widening valuation gap between large efficient REITs and small inefficient REITs, opening the door for further M&A activity.

- Public-to-public M&A is favorable to public-to-private M&A due to a disconnect between public and private markets, and access to cheaper debt capital assuming the acquiree's debt can be assumed.

- Top candidates for acquisition include: NetSTREIT Corp., W. P. Carey Inc., and NNN REIT Inc.

Given elevated capital costs as the market expects interest rates to remain higher for longer, I think that operational efficiency will remain front of mind for investors, resulting in a widening valuation gap between large efficient REITs with access to the lowest cost capital and small inefficient REITs. Furthermore, given the disconnect between public and private markets, which I previously wrote about in Net Lease REITs: Holding Off Until Cap Rates Stabilize , public-to-public M&A makes far more sense than public-to-private M&A.

While some investors look to a REIT’s nominal implied cap rate (i.e. a REIT’s net operating income divided by its enterprise value adjusted for non-real estate assets) as a measure of its economic return, skilled investors know that most real estate strategies involve at least some level of additional costs such as maintenance CapEx that further reduces cash proceeds to investors. Because maintenance CapEx is typically nonexistent for Net Lease REITs, I will ignore maintenance CapEx for the purpose of this article.

Furthermore, unlike a real estate portfolio that typically does not have overhead beyond property level operating costs, REITs have a G&A burden that further reduces economic returns to investors. Finally, while investors are quick to mark the left side of the balance sheet to market as interest rates rise and cap rates adjust, what is often forgotten, is the equally important exercise of marking the debt on the right side of the balance sheet to market, especially in a rapidly rising interest rate environment like we have seen over the past two years.

Google Finance, Public Company Filings.

{kind=link}

After making these three adjustments, you can arrive at what I consider to be the economic implied cap rate that represents the actual economic return to an investor. However, since the majority of acquiree’s G&A can be eliminated when acquired by a larger REIT, it is prudent to add the G&A back to arrive at what is the acquiree implied cap rate.

Analyst estimates.

A public REIT acquiring another public REIT not only makes sense from an asset valuation perspective given that public market real estate values react to changes in capital costs far quicker that private markets, but also from the perspective of acquiring debt.

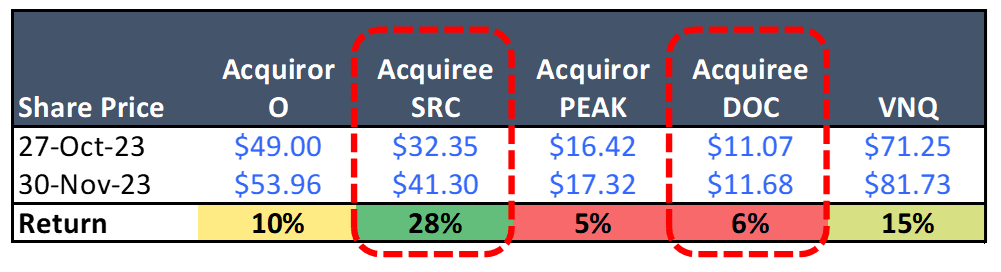

When Realty Income Corp ( O ) acquired Spirit Realty Capital Inc ( SRC ), not only was O able to acquire real estate equity at a price significantly below its private market value, since the transaction was a non-cash stock-for-stock transaction, O was able to assume SRC’s $4.1bn of debt with a weighted average interest rate of 3.48%, far below what the market rate of that debt would yield in today’s current high interest rate environment, where the 10 year US Treasury currently yields 4.17%.

Higher Capital Costs Environment Favors Efficiency

Assuming elevated capital costs for the foreseeable future as the market accepts that rates will remain higher for longer, I think operational efficiency will remain front of mind for investors. Similar to how higher rates has the effect of exposing inefficient “zombie companies” that can only remain profitable in a low capital cost environment, I think that higher rates will result in investors favoring REITs that have the most scale, efficiency, and access to capital with the lowest costs. While I don’t think that higher capital costs will be detrimental to most REITs in terms of continuing as a going concern given the current relative strength of REIT balance sheets, I do think it is likely to result in a widening gap in valuation, opening the door for larger more efficient REITs with lower costs of capital to acquire smaller less efficient REITs in an accretive manner.

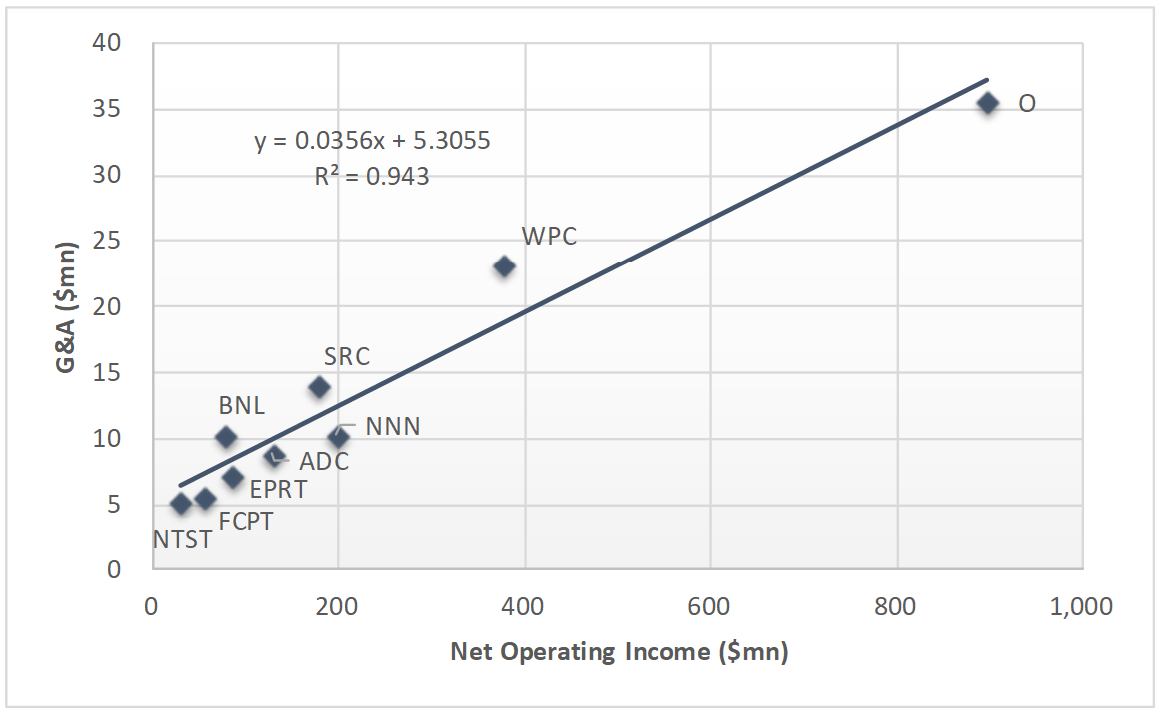

Comparing G&A to NOI shows a clear correlation (R-squared of 0.943) where the more NOI a REIT generates, the more G&A the REIT typically incurs. For their relative size, REITs that are above the trend line are relatively inefficient in terms of G&A, while REITs below the trend line are using G&A efficiently relative to their size. Not surprisingly, it was announced on October 30 th that SRC, which stands above the trend line, would be acquired by peer O, the largest REIT in the net lease space which lies below the trendline (i.e. efficient for its size).

{kind=link}

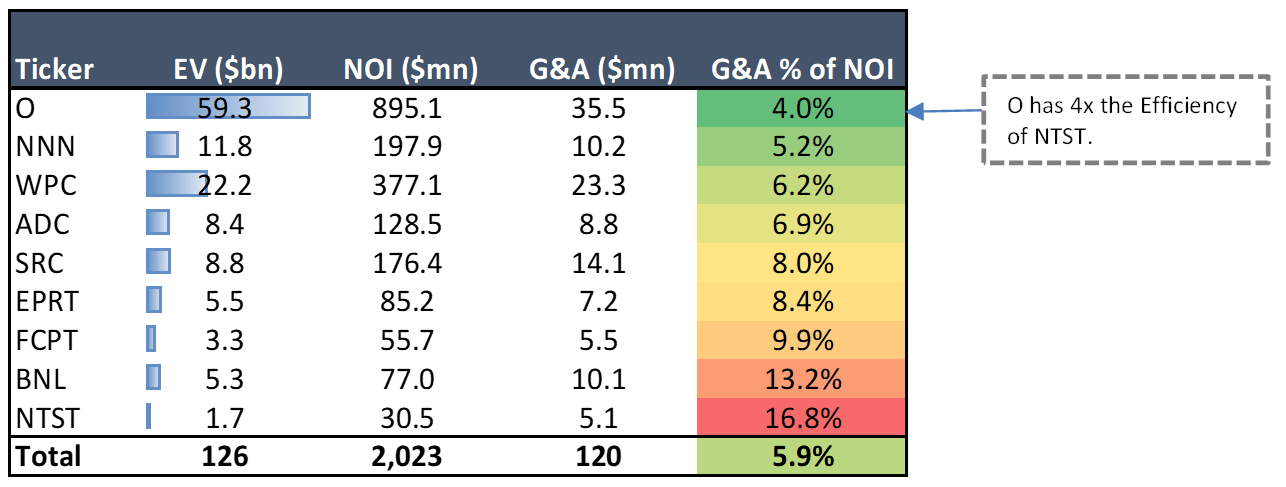

While it makes sense for a larger REIT to have more G&A, this correlation is not 1 for 1. Looking to G&A as a % of NOI reveals that the largest REIT in terms of Enterprise Value (EV) O has a G&A load equal to 4.0% of its NOI, while NETSTREIT Corp ( NTST ), the smallest REIT in terms of EV, has a G&A load equal to 16.8% of its NOI, indicating that O is 4x more efficient than NTST in terms of G&A load.

Google Finance, Public company filings.

{kind=link}

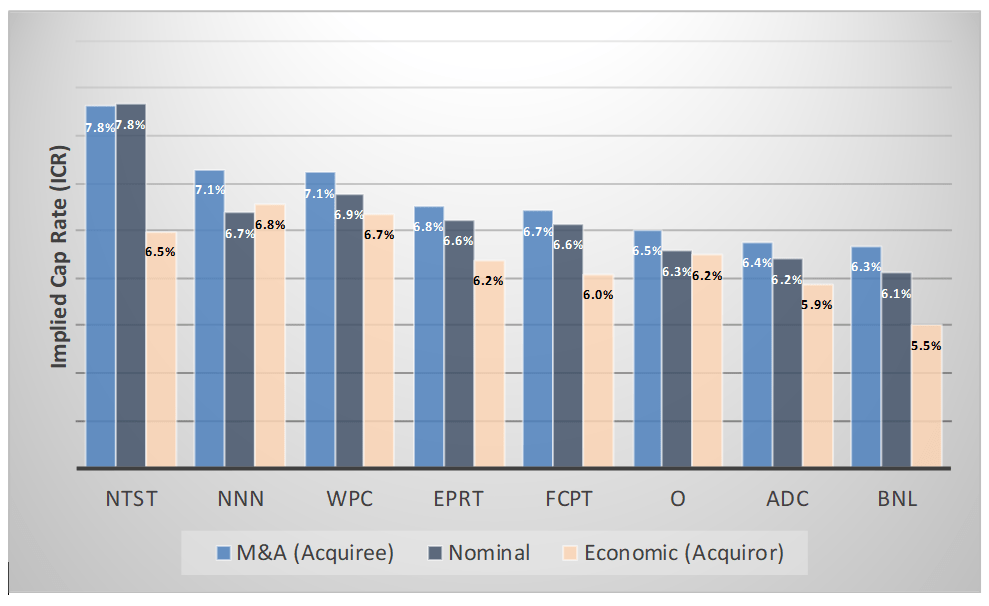

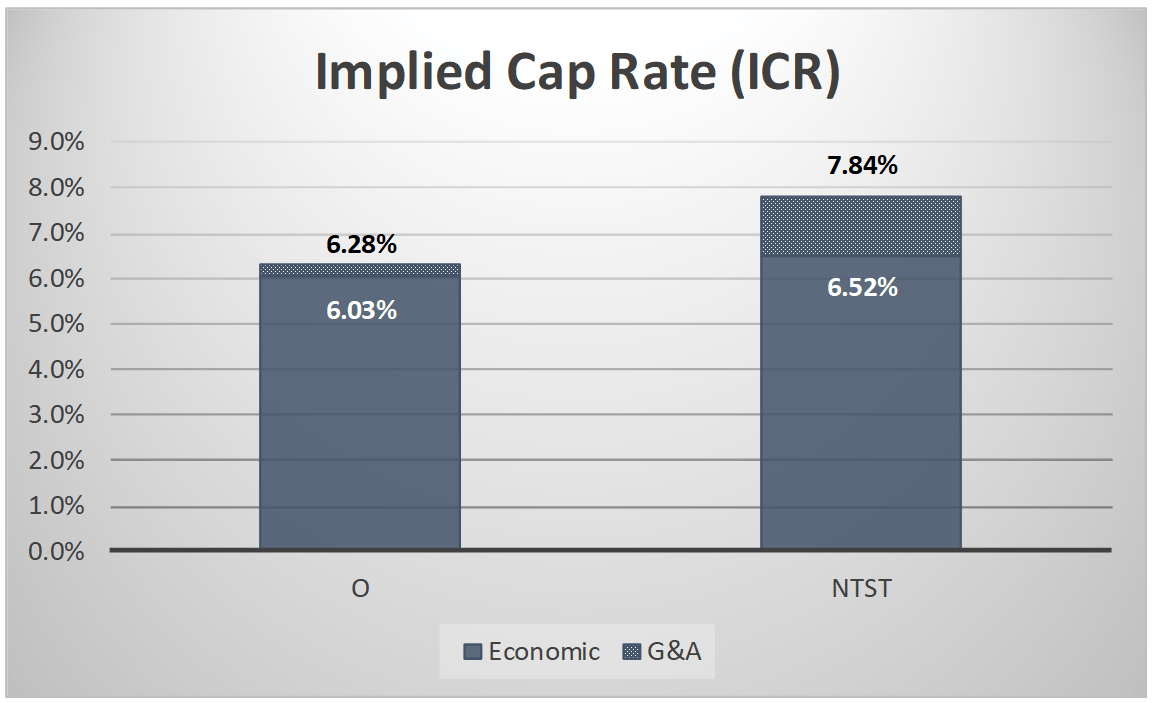

Converting the above analysis to an implied cap rate perspective, NTST may appear inexpensive to O on a nominal cap rate basis as O trades 156bps inside of NTST. However, when taking out their respective G&A loads, this valuation gap closes to 49bps.

Google Finance, Public company filings.

{kind=link}

On October 30, 2023, Net lease REIT O announced its merger with smaller peer SRC in a $9.3bn all stock deal. The same day, Healthpeak Properties Inc ( PEAK ) announced its merger with smaller peer Physicians Realty Trust ( DOC ). See REIT Merger Standoff: Spirit Realty The Clear Winner With A Low Risk Potential 18.5% Return for further analysis. A total of $100mn of synergies between both acquisitions are expected, effectively eliminating the G&A load of the smaller REITs that were acquired.

{kind=link}

REIT M&A Capital Costs

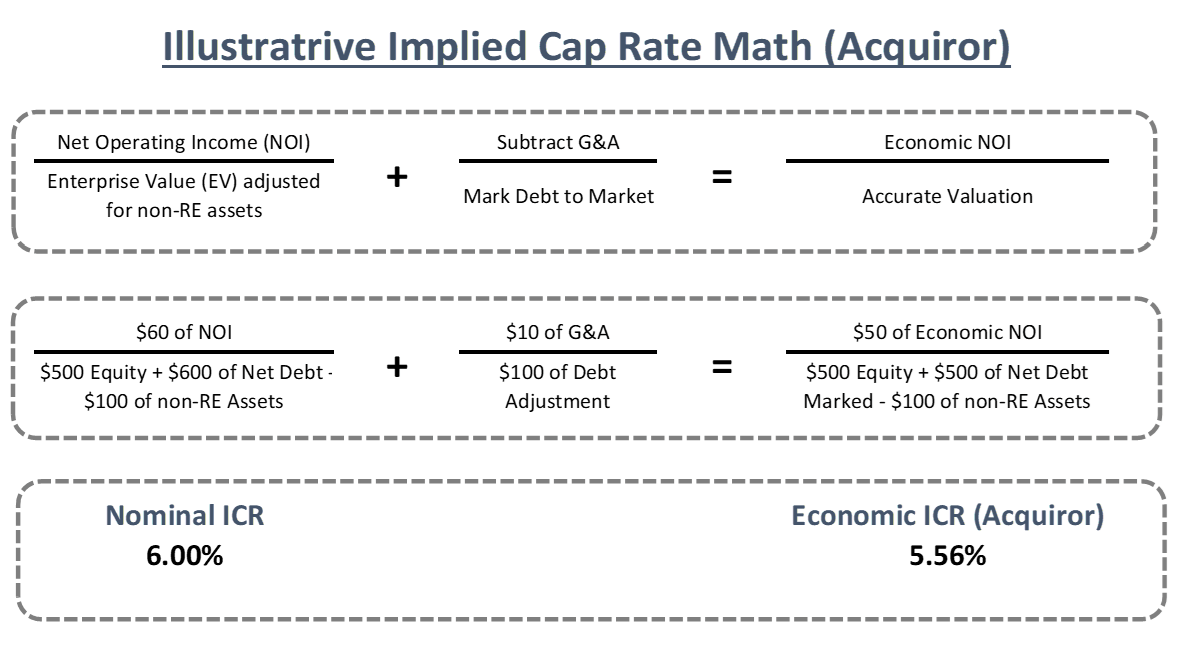

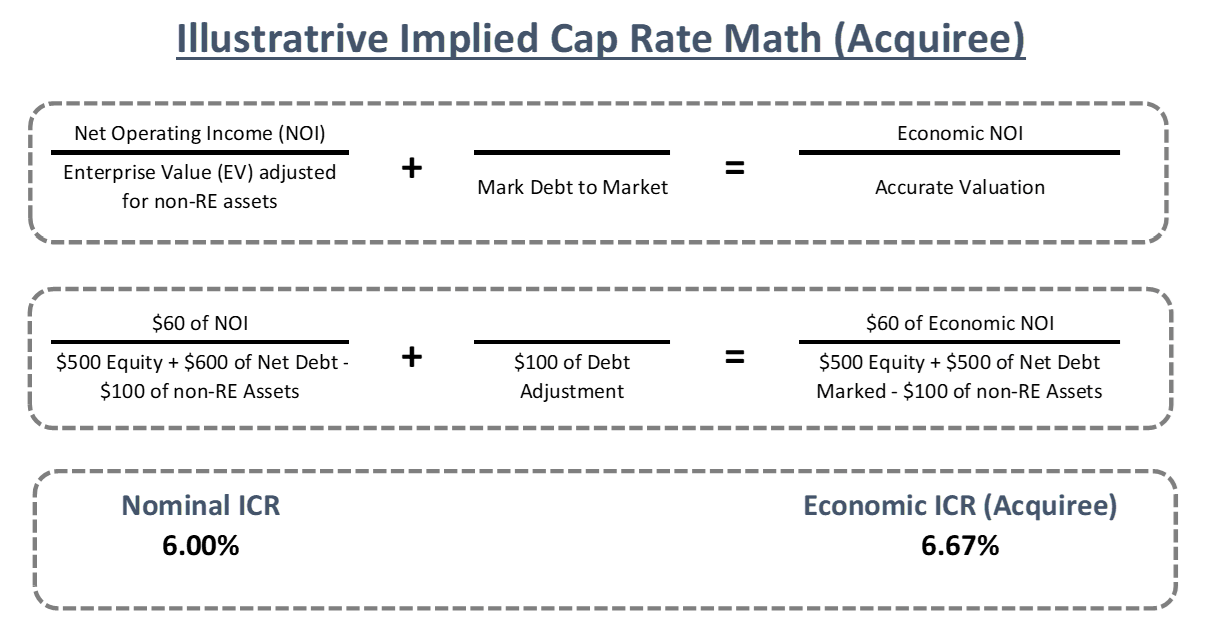

While some investors look to a REIT’s nominal implied cap rate (i.e. a REIT’s net operating income divided by its enterprise value adjusted for non-real estate assets) as a measure of the cost of capital for the acquiring entity, assuming the acquisition will require no additional G&A, the acquiring entity can spread its G&A burden out among additional NOI. In this case, the appropriate cost of capital for the acquiring entity should be an implied cap rate (ICR), where the G&A load is subtracted from the NOI in the numerator.

Additionally, while investors are quick to mark the left side of the balance sheet to market as interest rates rise and cap rates adjust, what is often forgotten, is the equally important exercise of marking the debt on the right side of the balance sheet to market, especially in a rapidly rising interest rate environment like we have seen over the past two years.

{kind=link}

From the perspective of the acquiree, assuming that the G&A of the REIT to be acquired can be eliminated after the acquisition closes, the acquiree’s G&A should be ignored (i.e. not subtracted) since the G&A will be eliminated anyways. In terms of debt, the fixed rate debt of the acquiree should be marked to market.

{kind=link}

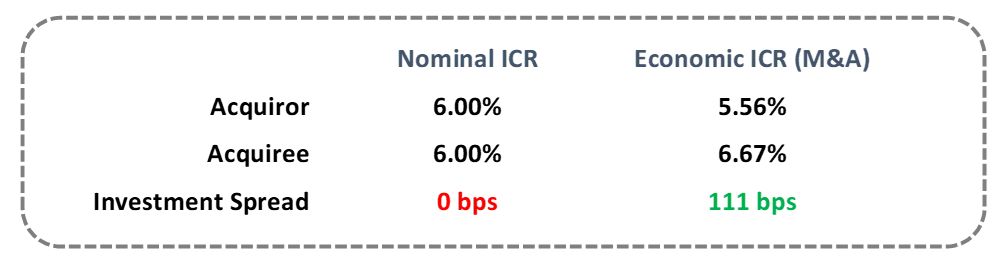

After making the above adjustments to the ICR’s of a potential acquiror and acquiree, the M&A accretion arithmetic can change substantially. Especially in the current era, where the vast majority of publicly traded REITs have debt on their balance sheets with interest rates that are far below market interest rates, these adjustments can change an acquisition from being dilutive to accretive.

{kind=link}

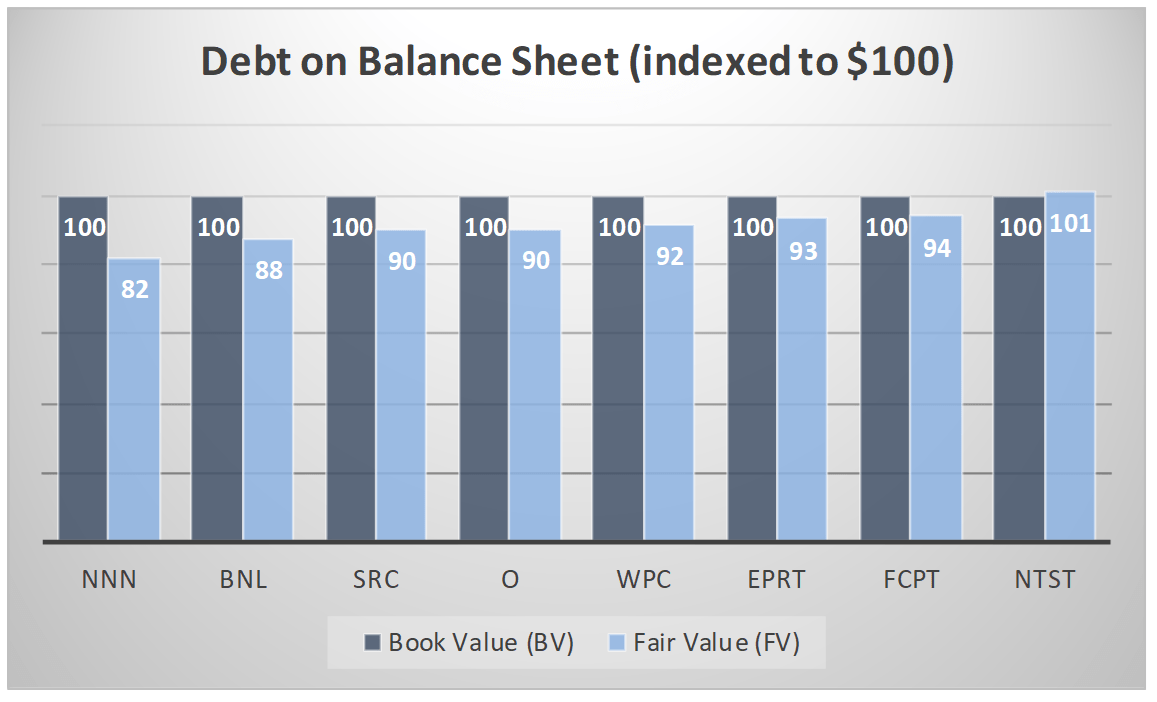

Taking the book value of fixed rate debt that REITs reported in their most recent 10-Q SEC filings and comparing that to the reported fair value that REITs reported in the same filing, you can back into the adjustment that is required to convert the book value of the debt to the fair value of the debt. Given the unprecedented rise in interest rates that we have experienced since March 2022 (when the Fed started its current tightening cycle), it is not surprising that every REIT with the exception of NTST, which is a relatively nascent REIT (IPO’d in mid-2020), has debt on its balance sheet that has a fair value below its book value. Put another way, every REIT with the exception of NTST has debt on its balance sheet with interest rates that are below current market interest rates with NNN REIT, Inc. ( NNN ) having the largest adjustment where the fair value of its debt is worth 82% of its book value and NTST being the only REIT that has an upward adjustment to its debt, where the fair value of its debt is worth 101% of its book value. This means that an acquiring REIT can not only get access to real estate equity that is below private market values, but they can also gain access to cheaply priced debt capital by assuming the acquiree REITs debt outstanding.

{kind=link}

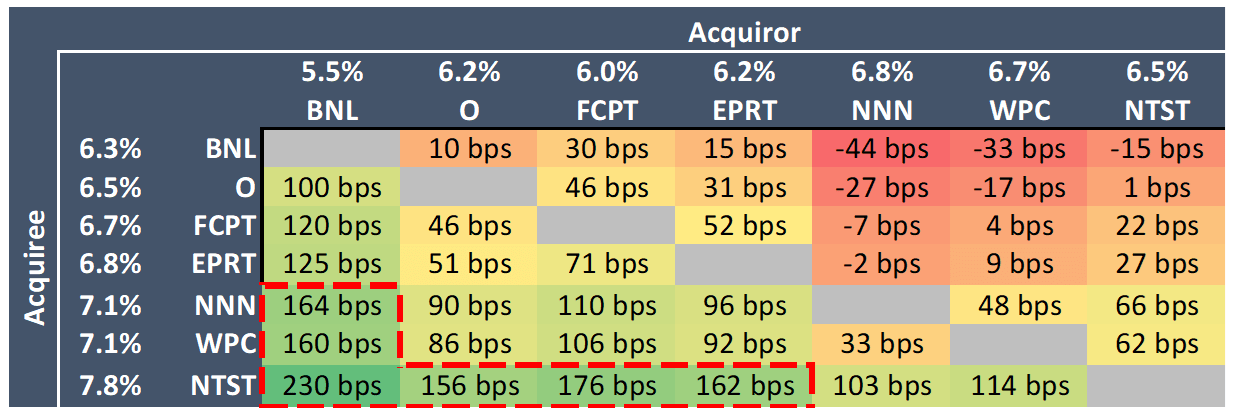

Calculating the appropriate acquiror and acquiree implied cap rate (ICR) for every net lease REIT under analysis, and looking to relative spreads shows what the most accretive potential M&A opportunities would be. In terms of acquisition targets, the REITs with the highest acquiree cap rates (i.e. NETSTREIT Corp., W. P. Carey Inc. ( WPC ), and NNN REIT, Inc.) are the most likely candidates for being acquired while the REITs with the lowest acquiror cap rates (i.e. Broadstone Net Lease, Inc ( BNL ), Realty Income Corp. ( O ), and Four Corners Property Trust, Inc. ( FCPT )) are the most likely candidates for acquiring another REIT. In terms of individual transactions, BNL or O acquiring NTST would be the most accretive and therefore the most likely transactions to occur in my opinion.

Google Finance, Public company filings.

{kind=link}

Looking to share price performance of O, SRC, PEAK, and DOC since the trading session before their respective transactions were announced reveals that not surprisingly, the smaller and less efficient acquiree REIT outperformed the larger more efficient acquiror REIT in both situations. While both transactions were considered mergers of equals that were all non-cash stock-for-stock transactions, I am referring to the smaller less efficient REIT as the acquiree for the sake of this article.

{kind=link}

Given the disconnect between public and private markets, which I previously wrote about in Net Lease REITs: Holding Off Until Cap Rates Stabilize , public-to-public M&A makes far more sense than public-to-private M&A.

A public REIT acquiring another public REIT not only makes sense from an asset value perspective, as public markets react to changes in interest rates far quicker than private real estate valuations, it also makes sense from a debt perspective. Given that the vast majority of debt capital on the balance sheets of public REITs was raised prior to the unprecedented swift increase in interest rates that started in March of 2022 when the Federal Reserve started its current interest rate raising cycle, most of the publicly traded REITs have debt capital that is far below market. I therefore think it is prudent to own net lease REITs that are small and inefficient in the current interest rate environment. I think the best REITs to own currently are NTST, WPC and NNN.

Potential risks to my thesis include: (1) interest rates revert to pre-COVID levels resulting in growth being favored over efficiency and (2) real estate transaction markets become more liquid allowing smaller REITs to become more aggressive on the external growth front.

For further details see:

Buy Small Inefficient Net Lease REITs As Current Environment Favors M&A