SAVE - Buy Spirit Airlines For The Same Reason JetBlue Is: The A321neo

2023-11-19 02:26:33 ET

Summary

- Spirit Airlines and JetBlue's proposed merger is still awaiting a final verdict from the DOJ after almost a year and a half.

- Spirit's value lies in its Airbus orders, which include more than 100 airplanes that will significantly increase capacity and fuel efficiency.

- Despite a forecasted net loss for FY'23 and FY'24, there is potential for Spirit to become profitable again in H2'24 and achieve significant net income in the future.

Since July 2022, Spirit Airlines ( SAVE ) shareholders are waiting to see if the proposed acquisition by JetBlue ( JBLU ) will be closed or not. At that time, Spirit had a Market Cap of $2.5 billion and JetBlue, with a Market Cap of $3 billion, was offering $3.8 billion to buy it. JetBlue likely took aim in Spirit because of the more than 100 Airbus A320/1neo that the company has in orders and because it probably felt the need to consolidate further to continue to compete with the big carriers.

However, almost a year and a half after the proposal, we are still waiting a definition on this merger because the DOJ decided to sue to block the deal as it reasons that it would likely kill the major ultra-low-cost carrier in the US. Since then, both companies have taken a hit to their prices and are currently trading at less than $1.5 billion, while waiting for the final verdict. For this article, I'll avoid discussing the DOJ case as I believe Spirit has value in itself, without the need for a merger with JetBlue. Spirit value comes from those Airbus orders that JetBlue is so interested and I'll walk you through how I see Spirit's Net Income evolving the next years due to these new airplanes.

The Airbus Orders

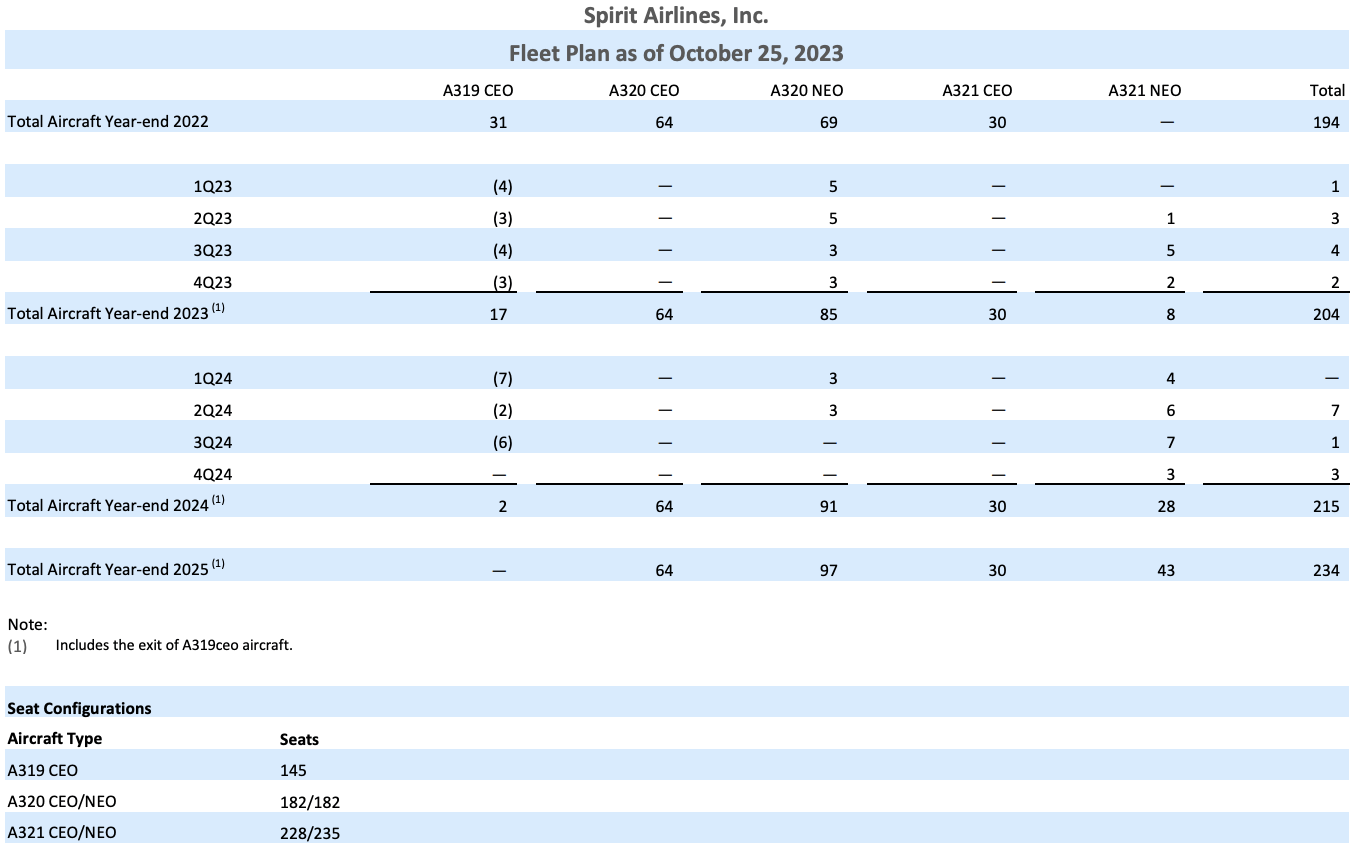

The main reason why JetBlue is so interested in Spirit is due to the Airbus orders that Spirit has: 101 airplanes, comprised of 41 A320neo and 60 A321neo. It's important to note that this order has recently been amended to switch the A319neo for A320neo and/or A321neo and to push the delivery of these airplanes more into the future. Spirit provides an expectation of when they will receive these new planes and when they will retire the old A319ceo.

Spirit Airlines Fleet Plan as of October 2023 (Spirit Airlines IR)

{kind=link}

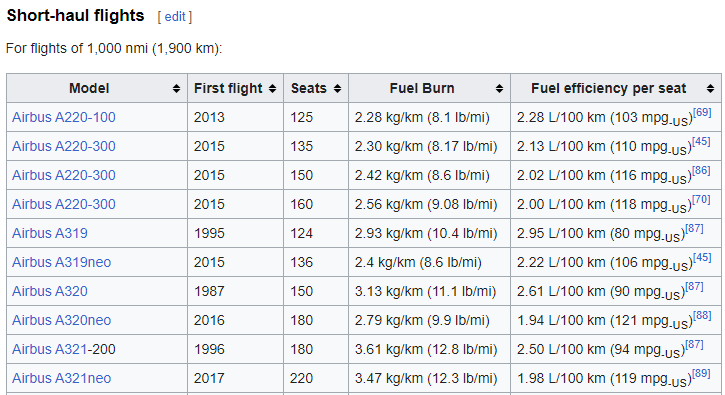

As the table shows, for the next four quarters (Q4'23 to Q3'24) Spirit will receive 9 A320neo, 19 A321neo and retire 18 A319ceo. This will boost Spirit's fleet by 10 airplanes while significantly increasing the seats available per flight as the A319ceo has 145 seats and the A320neo/A321neo have 182 and 235, respectively. This is a very important development for Spirit as any route flown today with an A319ceo will now have an A320neo/A321neo doing it, boosting by 40 or 90 seats per route the plane capacity. But higher capacity isn't the only important thing: fuel efficiency is as or even more important than plane capacity. Wikipedia has a great article comparing the estimated fuel efficiency of Airbus models:

Fuel Efficiency Comparison between Airbus models (Wikipedia)

{kind=link}

Since Spirit configures their Airbus with a different number of seats, some recalculation is needed to adjust Fuel Efficiency per Seat and compare these models. Spirit's A319ceo has around 2.5L/100km when considering the 145 seat-configuration, while the A320neo has 1.9L/100km and the A321neo has 1.85L/100km. If we calculate this Fuel Efficiency per Seat given the proportion of A320neo and A321neo that Spirit will receive, the result is 1.87L/100km. This is 25% lower than the current Fuel Efficiency per Seat of the A319ceo that will be retired. In sum, each route that Spirit will fly with an A320neo or A321neo instead of A319ceo not only has more revenue potential due to more seats available but it is also 25% more efficient in terms of fuel. This is why JetBlue wants to buy Spirit and this article will consider these numbers in order to assess financial performance shortly.

The New Pilot Contract & Jet Fuel

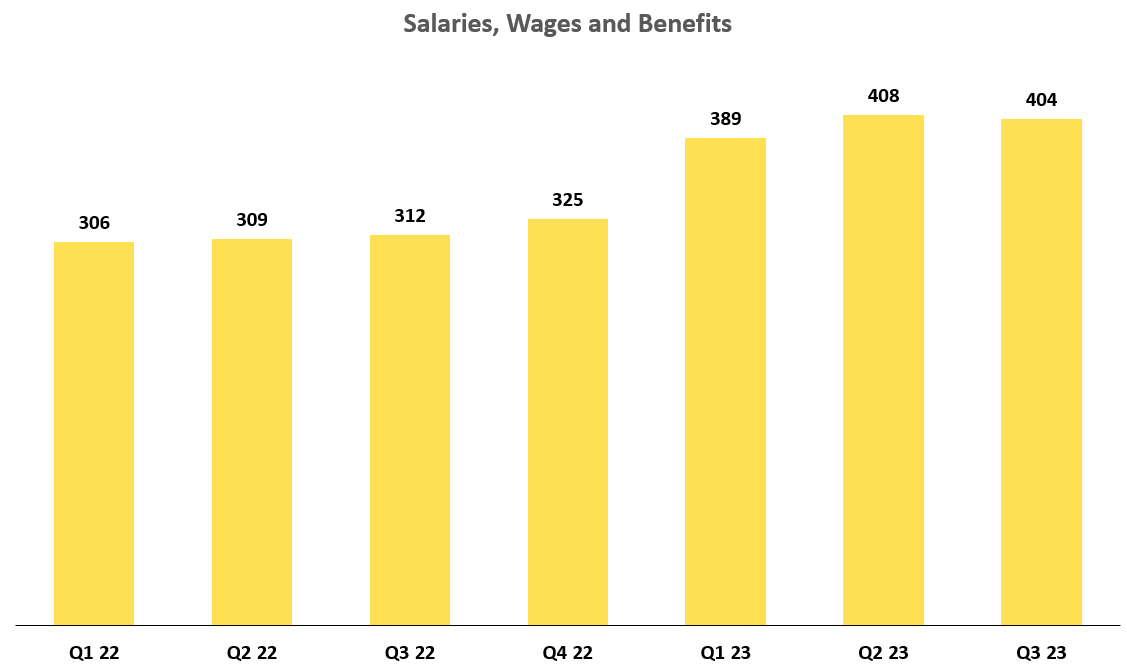

Earlier this year Spirit signed the new labor contract agreement with its Pilots. The impact is already visible in Spirit's financial statements as the line item "Salaries, Wages and Benefits" has increased from an average of $313 million per quarter in 2022 to $400 million in the first three quarters of 2023. Given that the average increase for two-year contract is expected to be 34%, this means that we should have another increase of $20 to $30 million per quarter in 2024.

{kind=link}

A good starting point would be to model salaries at $430 million per quarter for the year of 2024, but we should also consider that the Spirit's fleet is expanding and new pilots will likely need to be hired. Given that fleet will be increasing by 5% we can add another 5% increase in salaries and arrive at close to $450 million per quarter.

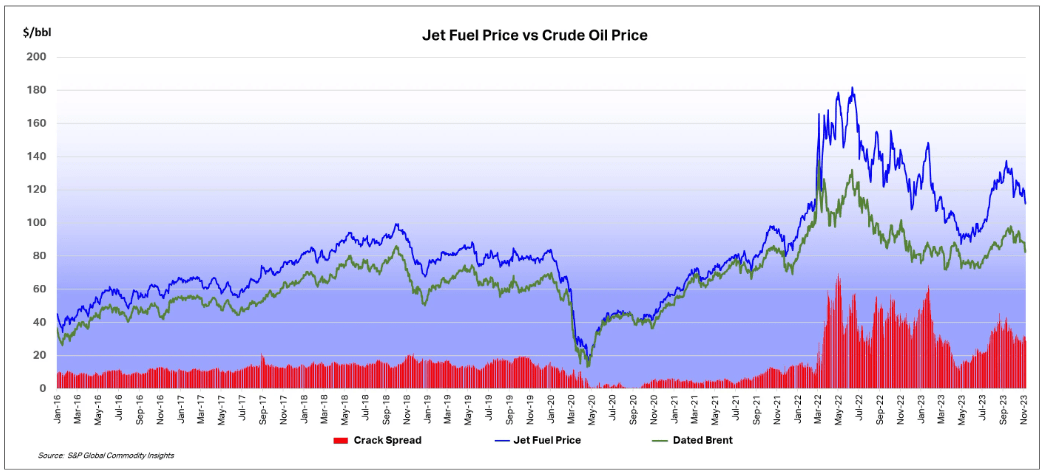

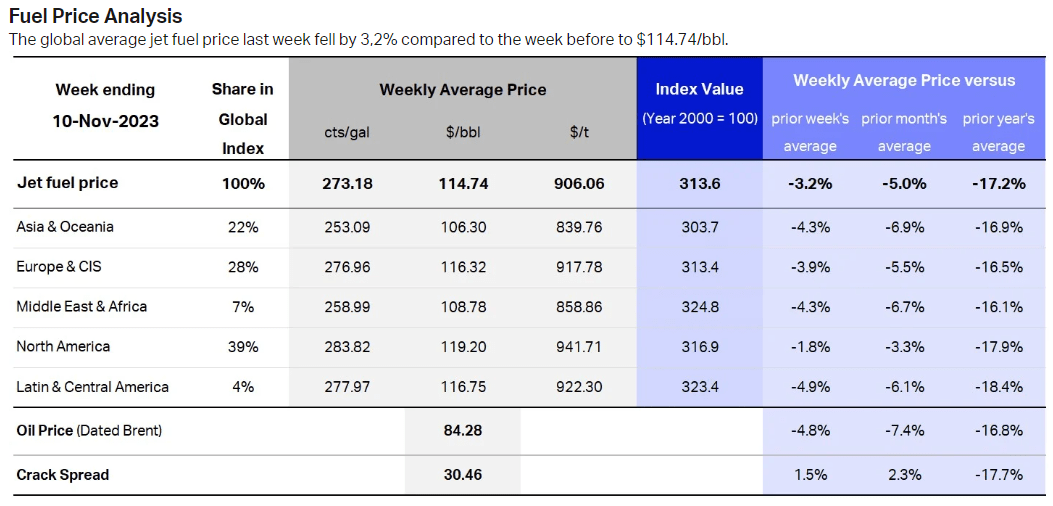

Jet Fuel has also been a negative contributor to Spirit's expenses increasing by more than 10% in Q3'23 vs Q2'23, but still much lower than its peak during 2022. The good news seems to be that the trend, even with a recent spike in September/October, is downwards as is shown below:

{kind=link}

Direction of Jet Fuel prices are to anyone's guess, but if I had to make a personal bet, I'd be more inclined to say that they will continue to go down. This can also be seen in the Weekly Average Price for North America that shows a negative variance on all metrics (vs Week, vs Quarter and vs Year).

{kind=link}

Financials

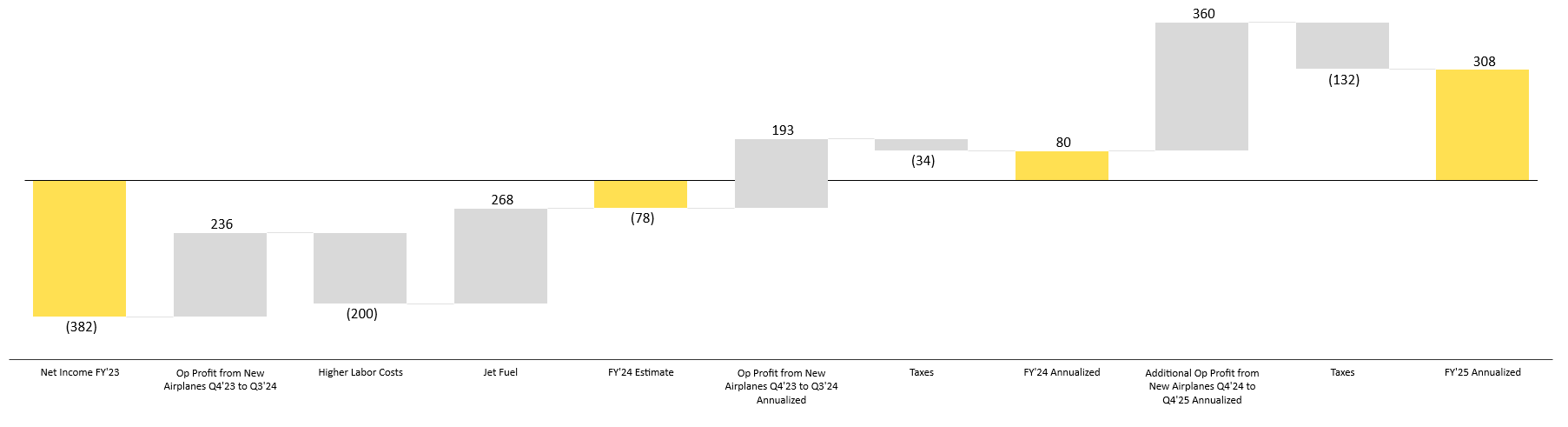

Finally, let's put the number to the test. Although I don't enjoy doing forecast for the short-term, it's important to estimate Spirit's Q4'23 in order to have a full view of Net Income for FY'23. My approach was quite simple: I kept everything the same as Q3 with the exception of Revenue and Jet Fuel that I applied a % growth similar to what happened between Q4'22 and Q3'22. With that, I arrived at a Net Loss of almost $400 million for FY'23 (current YTD Net Loss is $260 million). This is our starting point and below I show you my Net Income walk for Spirit considering the new airplanes, the new Pilot contract and some minor forecast for Jet Fuel.

Spirit Estimated Net Income Walk (in millions) (Author)

{kind=link}

Op Profit from New Airplanes Q4'23 to Q3'24: The $236 million addition to Net Income is based on the new airplanes that will arrive between Q4'23 and Q3'24 (for my forecast, I considered that an airplane received in Q4'23 is only operational in Q1'24). Based on RASM (Revenue per Available Seat-Mile) reported by Spirit of $.0914 and an average of 2.4 million miles flown by year per plane (11h Daily Utilization times 600mph average jet speed times 365 days) it's possible to calculate how much revenue an A319ceo is generating and how much the A320neo and A321neo could generate when replacing or being added to the fleet. I calculated that $430 million is how much we can expect of incremental revenue when the 18 A319ceo are replaced by the new airplanes and how much we can expect of new revenue from the 10 completely new airplanes to be added to the fleet in this period. This revenue is offset by $195 million in costs related to the new airplanes. It's difficult to forecast how much each airplane costs, mainly because we are talking about three different models. However, like RASM, the CASM (Cost per Available Seat-Mile) is known and we also know that the A320neo and A321 neo are 25% more fuel efficient than the A319ceo. Still, I decided to keep the cost flat in an attempt to be more conservative, so I'm not forecasting any efficiency here.

Higher Labor Costs: As already discussed, it's likely that Spirit will increase its "Salaries, Wages and Benefits" by $50 million per quarter during FY'24.

Jet Fuel: Here things are very open to interpretation. If you expect Jet Fuel to go up (and airfare tickets not increasing enough offset it) then Spirit will likely face more challenges in the near future. Based on the long-term data provided by IATA, between 2016 and 2020 Jet Fuel never hit the $100 mark and even after the chaos of the Russia-Ukraine war it was already on its way back to $100 before this spike in September/October. I'm expecting the downward trend to continue, so I included a reduction of 15% in Jet Fuel costs over the FY'23 numbers.

FY'24 Estimate: In the end, I'm still expecting Spirit to lose money in FY'24. Close to breakeven, but not there yet. So where is the upside then? It rests in the full potential of the A320neo and A321neo delivered during FY'24 and those that will be delivered in FY'25.

Op Profit from New Airplanes Q4'23 to Q3'24 Annualized: Remember that my forecast considers that an airplane delivered in Q4'23 is only fully operational in Q1'24? This means that all Airplanes that were delivered in Q1'24 or after were not considered in annualized terms for my FY'24 Estimate. When we include them for a full year, it means they can add another $193 million in Op Profit.

Taxes: I add a 30% tax rate to the Net Income calculated.

FY'24 Annualized: With these new airplanes for a full year, we could expect Spirit to have a Net Income close to $100 million. This also means that I'd expect Spirit to become profitable again sometime during H2'24. Taking this approach, it's now possible to see an interesting future path for Spirit and why JetBlue is interested. Important to highlight again that this is not the FY'24 estimate of Net Income, but just to show that the potential for a positive Net Income would already be within reach.

Additional Op Profit from New Airplanes Q4'24 to Q4'25 Annualized: In the Fleet Plan shared at the beginning of this article it's also available the aircraft forecast for Q4'24 and FY'25. Spirit expects to retire the remaining 2 A319ceo and add 6 A320neo and 18 A321neo, for a total of 22 additional airplanes in the fleet. If we apply the same rationale to these new aircraft, we could expect an annualized addition to Op Profit of $360 million. The full impact would only be in FY'26, but it would be expected that Spirit would continue to increase its Net Income going forward after becoming profitable again in H2'24.

FY'25 Annualized: Although I'm calling it FY'25, it is not an estimate of FY'25 Net Income. It is to show that at the end of FY'25 the company would have everything it needs to achieve more than $300 million in Net Income on an annualized basis.

Takeaway

Considering my expectation of close to $300 million in Net Income for Spirit somewhere between the short and mid-term, it means that the company trades at less than 4x forward P/E. This is much lower than the 8x to 12x that the company used to trade before the pandemic. Investors could double or triple their money at this point if Spirit manages to become profitable and its P/E is close to historical data. Even if you believe my forecast is somewhat aggressive, you can still make this kind of return by betting on the JetBlue merger. Since JetBlue offer is close to $30, this also means a 2.5x return to Spirit shareholders.

Despite all this, it's always important to remember that airlines are cyclical. My numbers are just that: numbers. If tomorrow a new data comes up that makes Jet Fuel go to the sky or anything different impacts this sector (pandemic anyone?), Spirit and all airlines are bound to suffer. If you're considering investing in Spirit, I'd caution you about the following risks.

Jet Fuel could easily go up the same way it has been going down. My forecast is based on a decrease of 15%, so if you disagree with this premise my conclusion likely doesn't hold.

Recently Pratt & Whitney disclosed an issue with their turbines. If anything disturbs the delivery schedule of the new airplanes or Spirit is unable to fly them, this will also have a material impact on my analysis.

Although Spirit next significant debt maturity is only in FY'25, airlines are particularly sensitive to interest rates. If the FED restarts hiking rates, this could really hurt Spirit.

Finally, although I consider myself a Buy and Hold investor and Spirit doesn't fit this criteria, I still believe there is value to the investor in Spirit. However, this is a not a Buy and Forget stock. If you buy it, make sure you're aware of how the previous topics I highlighted are evolving so you don't miss the bus.

For further details see:

Buy Spirit Airlines For The Same Reason JetBlue Is: The A321neo