SAFE - Buy The Dip: 2 REITs For 2023

2023-03-13 08:05:00 ET

Summary

- We find most opportunities in the small-cap segment of the REIT market.

- They often trade at large discounts to their larger peers.

- We highlight 2 undervalued REITs that we are buying for 2023.

The biggest and most popular REITs like Realty Income ( O ) rarely trade at a large discount because they get plenty of attention.

However, at High Yield Landlord, we find a lot of opportunities in:

- The small-cap segment of the REIT sector.

- Foreign REIT markets.

- As well as special situations.

Investing in such undervalued individual REITs has historically allowed us to earn a nearly 2x higher total return than the Vanguard Real Estate ETF ( VNQ ):

{kind=link}

And in what follows, we will highlight two such opportunities that we are buying at the moment:

BSR REIT ( OTCPK:BSRTF / HOM.U)

BSR REIT is an apartment REIT just like Camden Property ( CPT ) and AvalonBay ( AVB ) but BSR is unique in that it is highly concentrated on Dallas, Houston and Austin.

These Texan markets have enjoyed rapidly growing rents over the past year and BSR was ideally positioned to capitalize on this. Here are some highlights from its recent earnings report:

- Its net asset value per share rose by 9.8% in 2022 and reached $21.75.

- Its FFO per share rose by 21.1% in 2022.

- Its rents rose by 11.7% on average.

{kind=link}

With such strong results, you would have expected the company's share price to surge, but against all odds, it dropped very significantly. It would be an understatement to say that it has been frustrating to own BSR stock:

As a result of this crash, the shares now trade at a 40% discount to their net asset value. In other words, you get to buy an interest in a portfolio of Texan apartment communities that enjoy rapidly growing rents at about 60 cents on the dollar.

The management just had their earnings call and they seemed very optimistic about the future and so they are aggressively buying back shares to take advantage of this market dislocation:

As you're likely aware, we announced in early October that the TSX approved our normal course issuer bid that enables us to purchase up to approximately 3.3 million units. We're about 10% of our public flow over a 12-month period. We were very active on this front during Q4, repurchasing approximately 1.08 million units under the NCIB and our automatic securities purchase plan at an average price of $13.55 per unit. We will continue to take advantage of opportunities to repurchase units when appropriate, enabling us to strengthen unit holder returns... [emphasis added]

The market is pricing BSR at such a low valuation because it fears that the rising interest rates will hurt the company.

But contrary to that, the company just had its best year ever in 2022, and it guided for another strong year in 2023. Here is what the management said on the call:

Yesterday, we provided guidance for 2023. Our guidance calls for further solid growth in our key operating metrics. We currently expect FFO per unit of $0.90 to $0.96 compared to $0.86 last year. [emphasis added]

So at the mid-point, they expect to grow their FFO per share by 8% in 2023. Their rents continue to grow and the positive impact of this is much greater than the negative impact of rising interest rates because they use relatively little debt. Their LTV is just 35% and their maturities are well-staggered.

So in short, you get to buy rapidly growing assets at a steep discount to their fair value, and you get paid a 4% dividend yield while you wait.

We also think that the company is likely to announce another dividend hike sometime in the coming months. Their payout ratio is now just 65% because their cash flow grew a lot faster than their dividend in 2022.

I like the risk-to-reward a lot.

Farmland Partners

Farmland Partners ( FPI ) is one of just two farmland REITs. The other one is Gladstone Land ( LAND ).

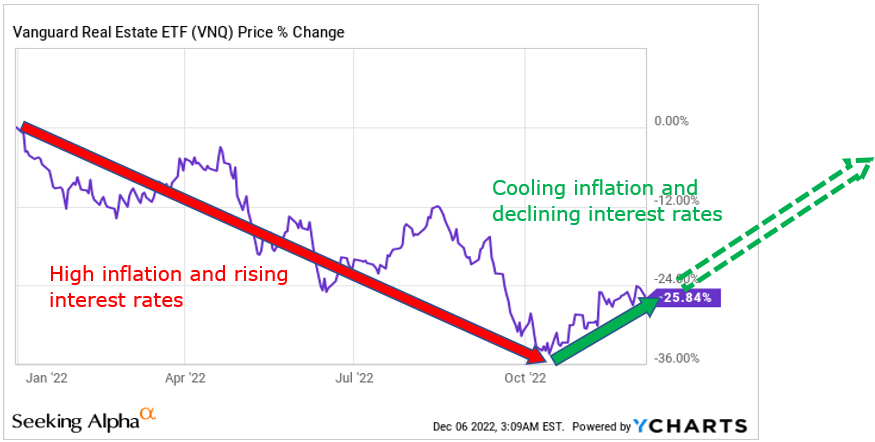

FPI was one of our best-performing investments in 2022. It delivered a 6% total return even as the rest of the market crashed ( VNQ ).

It outperformed by so much because farmland is one of the best inflation hedges in the world:

YCHARTS Farmland Partners

But a few weeks ago, the share price crashed as the company released its quarterly results and it has trended down ever since:

We think that this dip is an opportunity and so we just bought the dip.

As is often the case, we think that the market is overreacting to short-term news. The company reported very good results for 2022 with 16% average rent hikes on its expiring leases. The value of its farmland also grew significantly as a result of the high inflation and it paid off about 14% of its debt.

However, 2023 is going to suffer from a number of temporary headwinds. Here is what the CEO noted in their press release:

Supply chain disruptions, weather events, and other factors resulted in volatility in certain crop yields and crop prices. Our bottom line will be negatively impacted by these headwinds.

Moreover, its interest expense will rise quite significantly as a result of the rising interest rates. Therefore, its AFFO per share is expected to be materially lower in 2023 and since most REIT investors focus almost exclusively on these headline figures, it caused FPI's share price to crash.

But here's why we bought the dip.

Firstly, the underlying value of its farmland is not materially affected by these near-term headwinds. The value of its farmland rose very significantly in 2022 and we estimate that its net asset value is around $16 per share. Farmland values are very resilient and didn't drop even in 2008-2009 when most other real estate sectors lost significant value. The CEO of the company has previously noted that they expect their portfolio will keep appreciating by ~5% per year on average over the coming decade. This would result in a nearly 10% annual gain since the company is leveraged. Today, you get to buy an interest in this portfolio at ~65 cents on the dollar and the value is expected to remain resilient and keep growing in the long run, despite the volatility in its cash flow:

{kind=link}

Secondly, the main reason why we invested in FPI is that we expect it to build a sizable farmland asset management/brokerage business in the long run. They recently acquired a company called Murray Wise and the management confirmed to us in an interview in 2022 that the goal of this acquisition is to grow an asset management business (You can read our interview by clicking here ).

Currently, they only have $50 million of external assets under management that earn them fees, but in the coming couple of years, they would like to grow this external AUM to a size that's equivalent to their wholly-owned portfolio. This is huge considering that FPI owns $1.1 billion of assets. This means that they expect a very rapid ramp-up of external AUM, which will generate substantial fees for the company.

This is today completely ignored by the market.

Farmland Partners

Finally, if and when interest rates begin to decrease, FPI should be among the biggest beneficiaries, just like Safehold ( SAFE ), because it focuses on lower cap rate assets. Our thesis is not solely dependent on this, but we like to hold some more interest rate-sensitive investments in our Portfolio for the purpose of diversification.

We have previously explained that we expect interest rates to come back down as inflation gets back under control and this should be a powerful catalyst for REITs like FPI in the coming years.

{kind=link}

So in short, the market today focused on near-term headwinds, while we continue to focus on long-term tailwinds. This provides us an opportunity to buy high-quality farmland at 65 cents on the dollar. The yield is low at 2.2%, but the long-term growth prospects between the value appreciation and the growth of the asset management business could be very substantial.

We expect to soon again interview the company's CEO for members of High Yield Landlord. Let me know if you have any questions for him.

Bottom Line

The REIT sector includes some good, some bad, and some average investment opportunities.

REITs can be very rewarding investments, but you need to be selective and invest in the right REITs at the right time to optimize your risk-to-reward.

For further details see:

Buy The Dip: 2 REITs For 2023