ESS - Buy The Dip: 2 REITs Getting Way Too Cheap

2023-05-18 08:05:00 ET

Summary

- There are some unbelievable bargains in the REIT sector.

- Their cash flows have kept on rising even as their share prices collapsed.

- We highlight two of our favorite "buy the dip" investment opportunities.

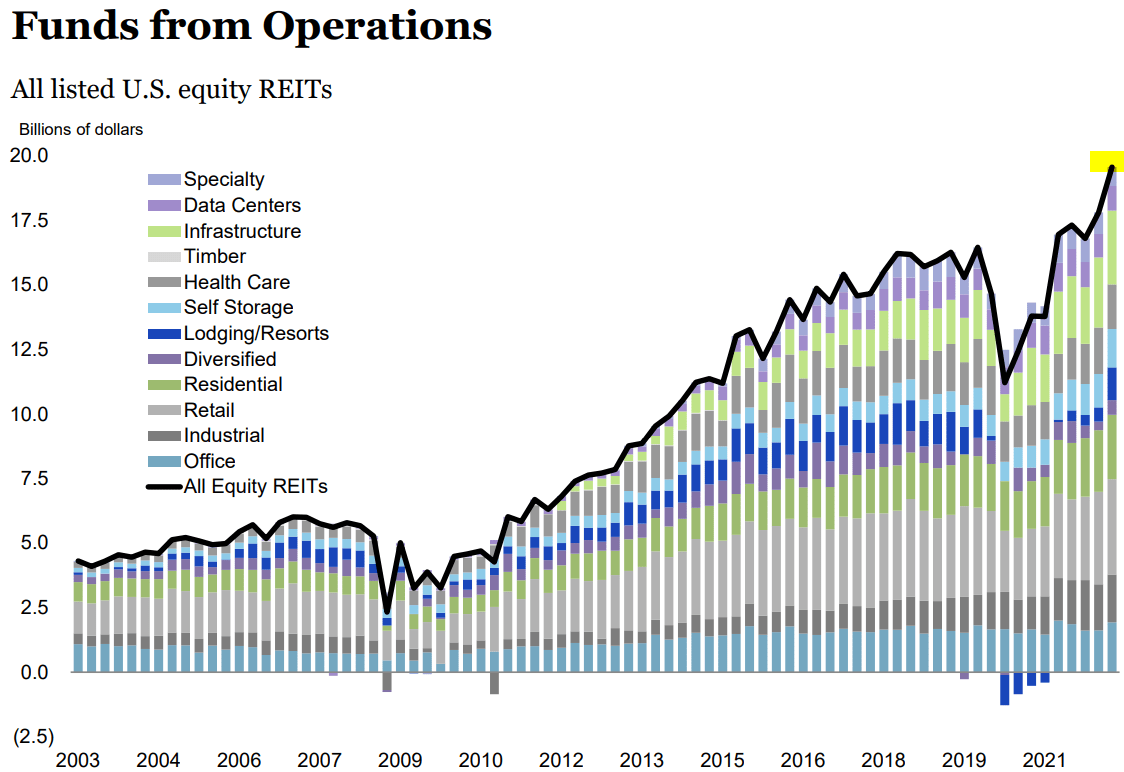

Currently, there is a clear disconnect between the fundamentals of real estate investment trusts ("REITs") and their share prices.

REIT cash flows and dividend payments keep on rising for the most part even as their share prices keep on declining.

Just look at the contrast between these two charts:

{kind=link}

Now, earnings season is underway and REITs are once more announcing strong results, but the market does not seem to care.

Cash flows are rising, more dividend hikes are announced, and despite that, REITs remain discounted as if they were going through severe challenges.

We think that the market is misjudging REITs and that this has led to a historic opportunity for long-term-oriented investors. REITs are now heavily discounted even as they keep on delivering strong results.

In what follows, we highlight two REITs that recently released strong results, but remain discounted nonetheless:

Armada Hoffler Properties, Inc. ( AHH )

We have in the past described AHH as a "quasi-apartment REIT" because nearly 50% of its portfolio (as measured by NAV) is invested in apartment communities and their strong performance has dominated its fundamentals in recent years.

Moreover, as their rents keep on rising at a rapid pace, and AHH continues to develop/acquire new apartment communities, we expect its allocation to this asset class to grow even larger in the coming years:

{kind=link}

That's very important because apartment communities are today doing very well. The surge in interest rates has made home ownership unaffordable for most people and it has led to a surge in demand for apartments.

This is the main reason why AHH has done so well in recent years, and once again, it posted strong first quarter results with 5.3% same property NOI growth, and it even hiked its dividend by another 3%.

Seeking Alpha

But despite that, AHH's share price has kept on dropping, and it is today 40% below pre-covid levels. That's despite paying a higher dividend than ever:

We suspect that this is because the market focuses on the other half of AHH's portfolio, which is mainly office and retail.

The market does not see AHH as a " quasi-apartment REIT. " It sees it as a " diversified REIT " with a significant office and retail component, which is precisely what it hates.

As a result, it has priced AHH at a low valuation of just 8.7x funds from operations ("FFO") and an estimated 35% discount to its NAV - despite its strong results.

We think that this is an opportunity because most apartment REITs like Mid-America Apartment Communities, Inc. ( MAA ), Equity Residential ( EQR ), and Essex Property Trust, Inc. ( ESS ) are priced at closer to 17x FFO - nearly a 2x higher multiple.

It appears that the market's concerns over one-half of its portfolio are causing it to heavily discount the entire company. Moreover, AHH's offices and retail properties are actually doing quite well. The retail is mostly service-oriented, Amazon-proof ( AMZN ), and recession-resistant; and the offices are Class A buildings, located in prime mixed-use locations. Their same property NOI growth is also positive and occupancy rates are near 100% - despite all the fears.

{kind=link}

So to make it short, here you get to buy an interest in this multifamily-heavy portfolio of Class A properties that generates growing cash flow at a low multiple of 8.7x FFO. We believe that the company has at least 30% upside potential today, but as interest rates return to lower levels, it probably has closer to 50% upside potential, and while you wait, you earn a 7.1% dividend yield, and its dividend keeps on rising.

I like the risk-to-reward.

Whitestone REIT ( WSR )

Whitestone REIT is our favorite retail REIT today. We like it so much because it owns the type of retail that's doing very well.

These are mainly service and grocery-oriented strip centers and they are located in some of the best neighbors of rapidly growing sunbelt markets like Phoenix and Austin.

As a result, they generate resilient cash flow that's growing rapidly. Today, the company's leases are deeply below market and it provides it an opportunity to bump up rents by 10-20% as leases gradually expire, leading to sector-leading same-property NOI growth:

Whitestone REIT

But despite that, the market isn't liking it!

The company just posted strong first-quarter results with 13% rent bumps on new leases and it reaffirmed its same property NOI guidance, which again puts it among the fastest-growing REITs in its peer group. WSR is growing even faster than blue-chip peers like Federal Realty Investment Trust ( FRT ) and Regency Centers Corporation ( REG ):

Whitestone REIT

But the market didn't like it and its share price has kept on dipping.

I am having a hard time finding a reason for this, but if I had to make a guess, I would speculate that the dip may be because the company's FFO per share was 20% lower in the first quarter. This is only because of one-time compensation benefits, but since the market focuses on such headline figures, it may have sparked the sell-off.

As a result, the company is today priced at an exceptionally low multiple of just 8x FFO and an estimated 40% discount to its NAV. The company recently sold some assets at low cap rates and this provided further evidence that this steep discount to NAV is real.

We recently also talked with the company's management and in our exclusive interview, they explained to us that they plan to close this discount by selectively selling assets and deleveraging the balance sheet, which should prove the value of their assets and remove concerns over rising interest rates.

The upside potential could be very significant. Even at a 50% higher share price, the company would still be priced at a discount to peers. While we wait for this upside, we earn a near 6% dividend yield.

Again, I think that the risk-to-reward is very compelling as a result of its discounted valuation.

Bottom Line

Here is what billionaire investor Barry Sternlicht said in a recent interview (emphasis added):

"By the way, when credit comes back, you are gonna see REITs take off. REITs are on sale. There are some unbelievable bargains in REITs. We did the same thing during the pandemic. We bought a dozen stocks all over the world and we had a 70% IRR on that stuff. We are already buying some stuff in the public market because I do think that rates are going down."

He is the CEO of Starwood, which is one of the biggest private equity investment firms in the world. He is famous for being opportunistic and has one of the best track records of all investors.

He is now buying REITs and so am I, because valuations are exceptionally low.

For further details see:

Buy The Dip: 2 REITs Getting Way Too Cheap