UMH - Buy The Dip: 2 REITs Getting Way Too Cheap

2023-03-21 08:05:00 ET

Summary

- REITs sold off heavily in recent months.

- This has led to some historic buying opportunities.

- We highlight 2 REITs that are getting way too cheap.

Is now a good time to " buy the dip ?"

We just had the 2nd and the 3rd largest bank failures in the country's history, and it all happened within a few days.

Now, it is also speculated that Credit Suisse Group AG ( CS ), one of the world's largest financial institutions, could also collapse, and UBS Group AG ( UBS ) has offered to buy it out.

Uncertainty is very high, and the " fear & greed index " signals that the market is currently affected by 'extreme fear' - a rare occurrence.

But I am sure you've heard this before:

The time to buy is when fear is high and valuations are low. You should "be fearful when others are greedy, and greedy when others are fearful" because fear leads to great long-term buying opportunities.

And today, we think that this applies particularly well to real estate investment trust ("REITs") ( VNQ ), which are listed real estate investment vehicles.

They are today priced at large discounts relative to the value of the real estate they own, net of debt. They were already discounted prior to the recent selloff, but they then dipped even lower following the recent banking crisis, which sparked memories of the great financial crisis.

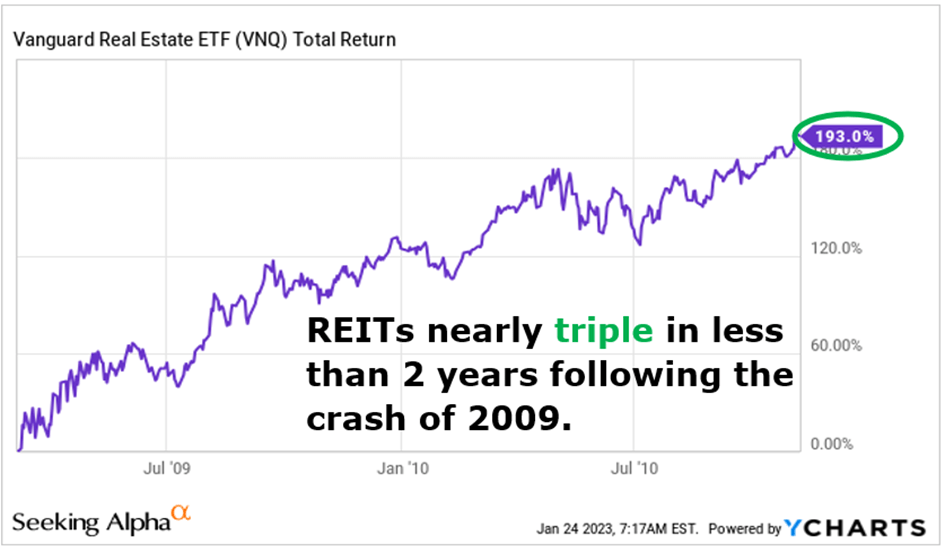

But... what investors appear to forget is that REIT share prices nearly tripled in just two years following the great financial crisis... and returns were so great because valuations had dropped too low:

{kind=link}

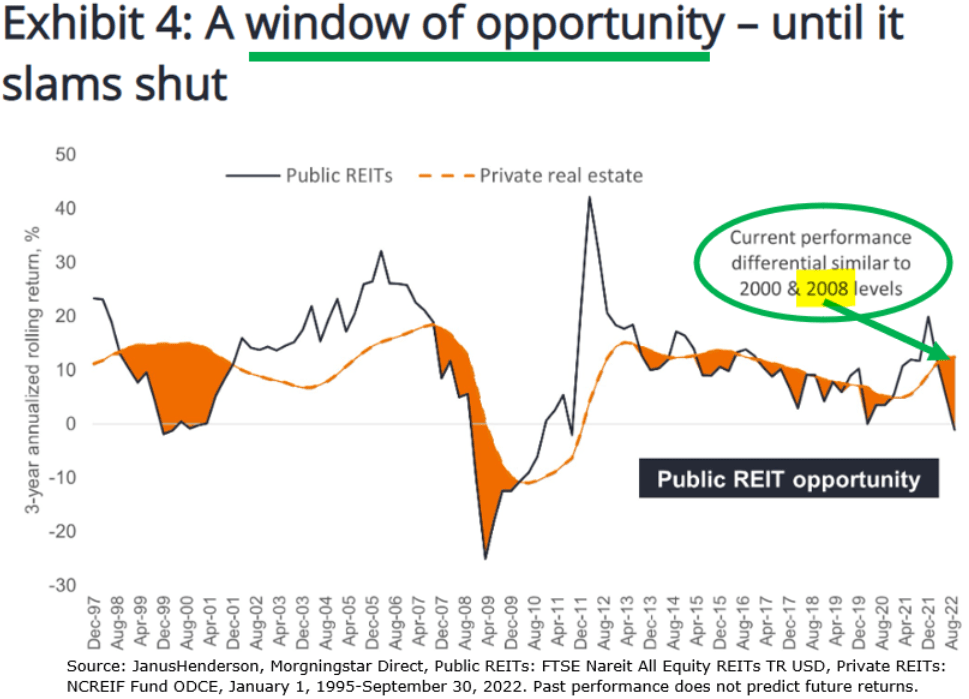

Today, valuations are reminiscent of the great financial crisis according to a study by Janus Henderson, and I predict that REITs will again richly reward "dip buyers" in the coming years as they recover from today's depressed valuations:

{kind=link}

But not everything is worth buying.

You want to buy REITs that enjoy:

- Strong growth

- Defensive fundamentals

- Solid balance sheets

- Shareholder-friendly management teams

- & Discounted valuations, of course.

Below we highlight two REITs that we have been buying lately at High Yield Landlord. We think that they are both heavily discounted and offer attractive risk-to-reward following their recent dips:

UMH Properties, Inc. ( UMH )

UMH Properties is one of just three REITs that focus on manufactured housing communities. The two others are Sun Communities, Inc. and Equity LifeStyle Properties, Inc. ( ELS ).

I have previously explained that I like manufactured housing communities because they:

"generate recession-resilient cash flow and enjoy limited capex because the landlord typically (but not always) only rents the sites and the tenants bring their own homes. Out of UMH's ~20k occupied sites, 12k of them are rented without the home. Since moving a home from one community to another is expensive and impractical, the tenants of these sites are also very dependent on UMH, reducing turnover and lease delinquencies."

UMH Properties

I added that:

"Also, if the tenant does not pay the rent for its site, the landlord may also be able to foreclose on the tenant's home, which is likely worth a large multiple of the missed rents, providing margin of safety. Finally, affordable housing is always in great demand, especially during times of crisis, and UMH proved that during the pandemic as it experienced rapid growth."

Despite that, the new supply is strictly limited because it is hard to get permits to build new ones. This is partly because most people don't want one in their backyards.

This makes them very attractive investments, because you have limited supply, growing demand, recession-resistant cash flow, limited capex, and growing NOI.

UMH Properties

It explains why these assets are typically priced at high valuations with low cap rates in the private market and high funds from operations ("FFO") multiples in the public REIT market.

But today is an exception.

All three of these REITs are undervalued, trading at low FFO multiples and large discounts to their net asset values.

UMH is probably the cheapest following its recent dip. It was already discounted in early 2023, but it then dipped a lot lower when it announced its 4th quarter results.

The market didn't like them because its FFO per share came lower than expectations.

But as we have explained previously, the quarterly FFO figures of UMH are not useful because:

(1) they own securities, which impact their quarterly FFO, and

(2) their acquisitions are often dilutive at first, but highly accretive once the value-add kicks in.

They will commonly acquire communities at low cap rates because they are poorly managed, suffer some deferred capex, etc. but as they then improve them, they are able to significantly bump their occupancy rates and rents.

The business model leads to some bumpiness in quarterly results and the market often overreacts to it.

We estimate that the shares trade at a ~40% discount to their NAV, 14x FFO, and you earn a 6% dividend yield while you wait for the upside.

The management has previously told us in an interview that they expect to grow their FFO per share by 50% over the coming 5 years and we expect to soon schedule another interview with them.

Crown Castle Inc. ( CCI )

CCI is potentially the highest-yielding blue-chip high-growth REIT in the entire marketplace right now.

Historically, its yield has been in the 2.5-3.5% range during most times, which makes sense for an investment-grade rated blue-chip REIT that invests in cell towers.

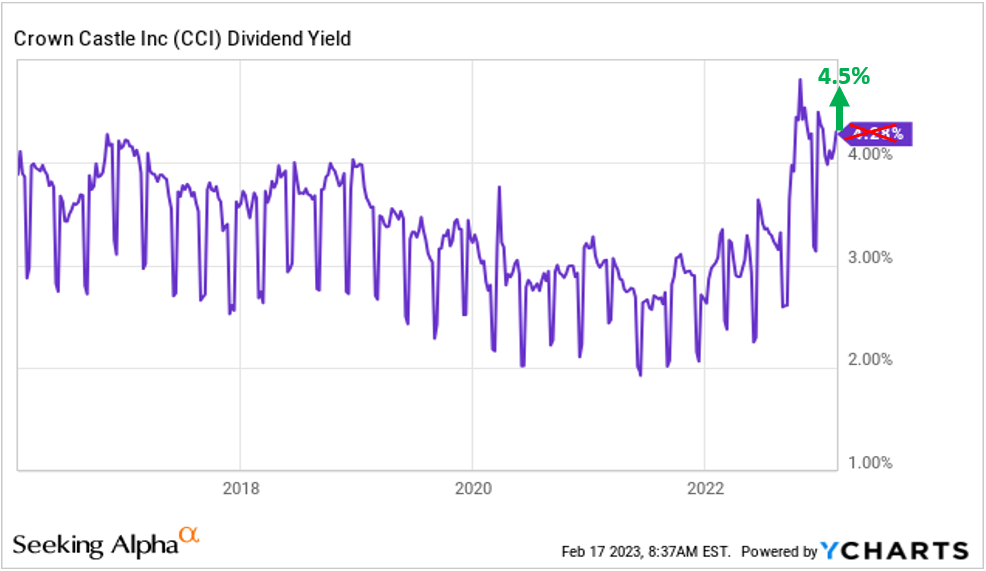

But following its recent dip and its 6.5% dividend hike, it now yields more than ever at 4.5%:

{kind=link}

The market has repriced CCI at a higher dividend yield because it is expected to grow slower than usual in the coming years. The management has been open about their slow-down and hasn't tried to hide from the market.

The reason why its growth is slowing down is that CCI had some lease cancellations after T-Mobile US, Inc. ( TMUS ) bought Sprint. Tower REITs profit when they can add additional tenants to a tower, but this also means that they suffer from carrier consolidation. Previously, CCI may have leased space to both, T-Mobile US, Inc., and Sprint, but it will lose the revenue coming from Sprint going forward as leases expire.

{kind=link}

This will be a headwind in the next few years, but even despite that, CCI is still expected to keep growing, albeit just at a lower rate.

More importantly, what the market appears to forget is that this is just a temporary headwind. Here is what the CEO commented on their most recent conference call (emphasis added):

"So to wrap up, we are excited about the strength of our business and our ability to execute on our strategy to deliver the highest risk-adjusted returns for our shareholders by growing our dividend over the long-term and investing in assets that will help drive future growth. We have delivered 9% compound annual and dividend per share growth since we established our 7% to 8% dividend per share growth target in 2017. And I believe that we are positioned well to return to 7% to 8% dividend per share growth as we move beyond the Sprint decommissioning impacts in 2025."

So they expect slower growth for just 2 years. After that, they expect to return to their 7-8% annual dividend growth target, which they have historically outpaced:

{kind=link}

High-quality REITs like CCI that are able to grow their dividend at 7-8% per year are typically priced at closer to a 3% dividend yield. To return to that yield level, its share price would need to appreciate by 50%, and while you wait you earn a 4.5% dividend yield that's relatively safe and growing.

It is hard to beat that in terms of risk-to-reward, and this is why we are today making CCI the largest holding of our Retirement Portfolio.

Bottom Line

The REIT market is today heavily discounted because the market fears that the surge in interest rates will lead to lower cash flows.

But the opposite is happening. REIT cash flows just hit new all time highs and most REITs continue to grow at a good pace even in 2023. This is because leverage is at all-time low, debt maturities are long and well-staggered, and rents keep on growing.

Yet, valuations are now heavily discounted and we are buying the dips.

For further details see:

Buy The Dip: 2 REITs Getting Way Too Cheap