EPRT - Buy The Dips: High Inflation Should End Soon

2023-06-27 07:30:00 ET

Summary

- We are slowly creeping into a recession.

- And also lower inflation and interest rates.

- Here is what it means for investors.

Co-produced by Austin Rogers.

"Inflation remains hot, the labor market remains strong, and a recession is nowhere in sight. We may not even have a recession!

On top of that, relatively high inflation and interest rates are likely here to stay for a long time because globalization is dead, the labor shortage is permanent, deficit spending is out of control, and the green revolution is causing certain commodity prices to soar."

That's a common narrative in the media.

But we believe this narrative is misguided.

- Inflation (properly measured) has fallen back to low levels.

- Tight credit conditions are causing a sharp pullback in the flow of credit.

- Leading economic indicators are at recessionary lows.

- The consumer has weakened and is reining in spending.

- Commodity prices are falling, and producer price growth has cooled considerably.

- Supply chain pressures have eased significantly.

- Artificial intelligence ("AI") should gradually reduce the labor shortage, especially in services industries that continue to put upward pressure on inflation.

We believe that the U.S. economy will be in a recession by the end of this year, although it is difficult to say just how deep of a recession it will be or what effect it will have on stocks ( SPY ), bonds ( BDN ), and REITs (VNQ).

Below, we'll cover a swathe of the evidence. We see that a recession is almost upon us and that inflation has already cooled considerably and is likely to either remain muted or fall further for the foreseeable future. Finally, we'll finish with some thoughts on how this outlook affects REITs.

Economic Tailwinds Turning Into Economic Headwinds

Our macroeconomic thesis for about a year and a half now has been that the combination of massive fiscal stimulus and the sudden and prolonged drop in production during COVID-19 caused a huge, one-time, lagged surge in inflation. Moreover, social distancing measures caused a huge surge in demand for goods exactly as production slowed and supply chains broke down.

But we don't think this surge in inflation indicates that a new secular uptrend in inflation is upon us.

Rather, just as the unprecedented, one-time factors caused a surge in inflation, so too will the removal of those factors cause a sharp slump in inflation.

We can see the unprecedented spike in fiscal stimulus in the year-over-year growth in the money supply in 2020 and 2021.

YCHARTS

But that emergency stimulus spending has not continued into 2022 and 2023. As such, YoY growth in the money supply has fallen just as sharply and has in fact turned negative for the first time in modern history. Interestingly, money supply growth has not been this deeply negative since the Great Depression in the 1930s.

With the Fed remaining adamant on tight monetary conditions, asset prices (especially in office real estate!) falling, and bank reserves rising, there doesn't appear to be an end in sight (yet) for this decline in the money supply. That puts downward pressure on consumer spending and inflation.

What about the supply side?

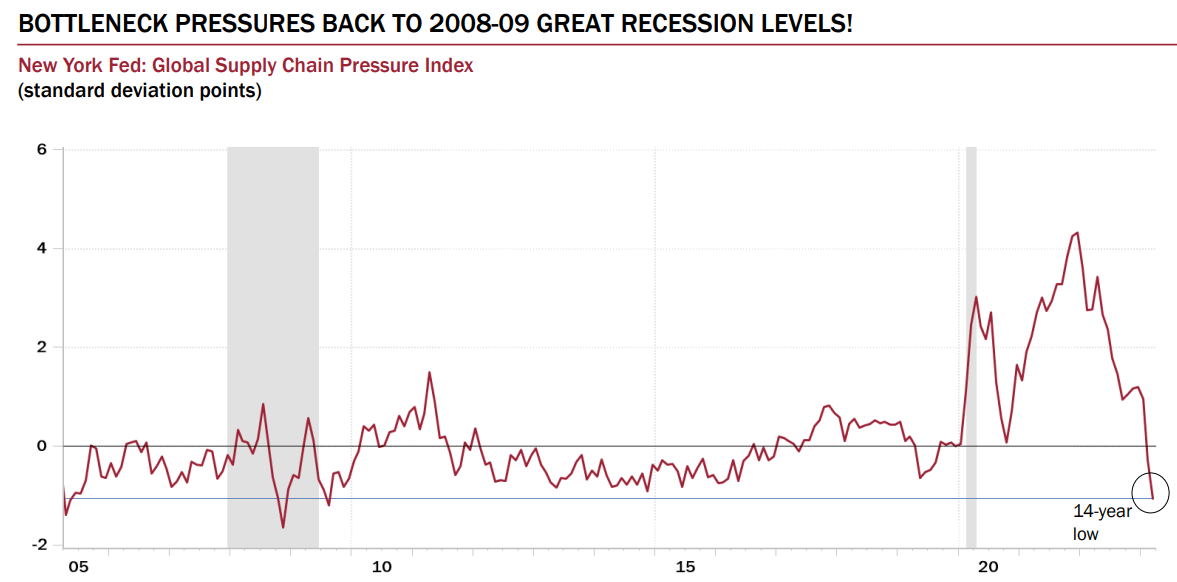

Well, we can see the sudden, huge spike in supply chain pressure/bottlenecks at the onset of COVID-19, reasserting itself in 2021 and early 2022.

{kind=link}

But what about today? In the second half of 2022 and into 2023, consumers shifted the bulk of their spending from goods to services, and supply chain pressures quickly eased.

Notice that there are no news headlines about how many container ships are moored off the coast of Southern California anymore. That's because there are none!

Ports and other supply chain infrastructure are back to operating at full efficiency, and unusually high demand for goods has reversed.

Hence we find in the chart above that supply chain pressures have actually dropped back to recessionary lows!

Now, it is true that we have not seen real GDP growth turn consistently negative yet, but this is a coincident or even lagging indicator of recession, not a leading one.

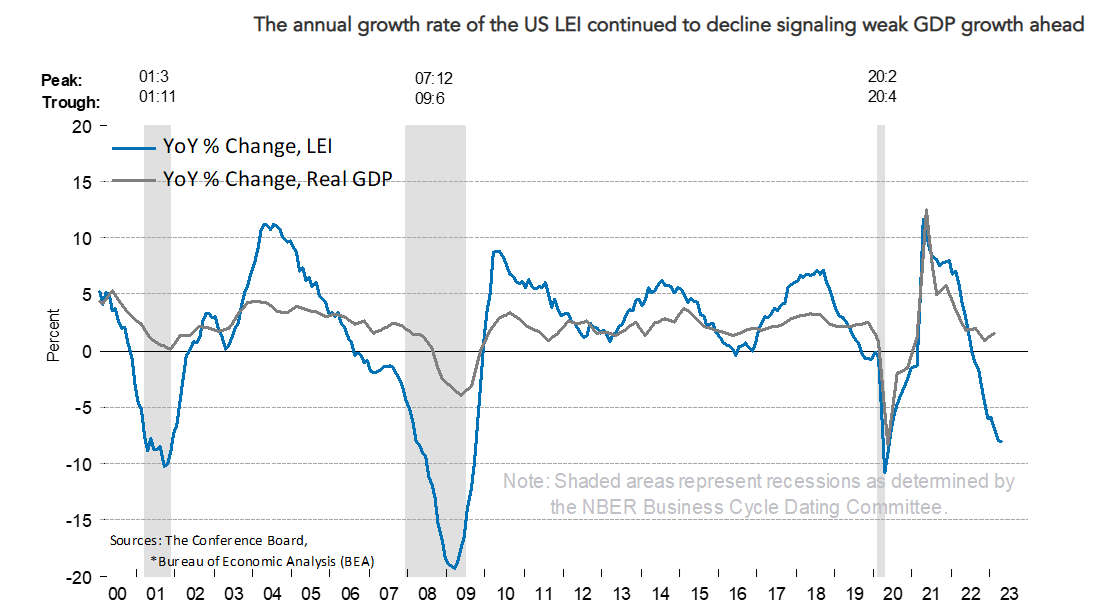

To look for an oncoming recession, you need to "skate to where the puck is going," to quote hockey player Wayne Gretzky, by watching leading economic indicators like manufacturing orders and building permits.

The Conference Board has an index of these Leading Economic Indicators that collectively have a very strong track record of predicting recessions. For over a year now, the LEI has been in freefall, plunging right into negative territory.

{kind=link}

According to the Conference Board, this depth of negative LEIs is strongly predictive of an upcoming recession.

The Conference Board forecasts a contraction of economic activity starting in Q2 leading to a mild recession by mid-2023.

But there's a lot more to the recession forecast than the money supply and supply chain easing.

Tightening Credit Conditions

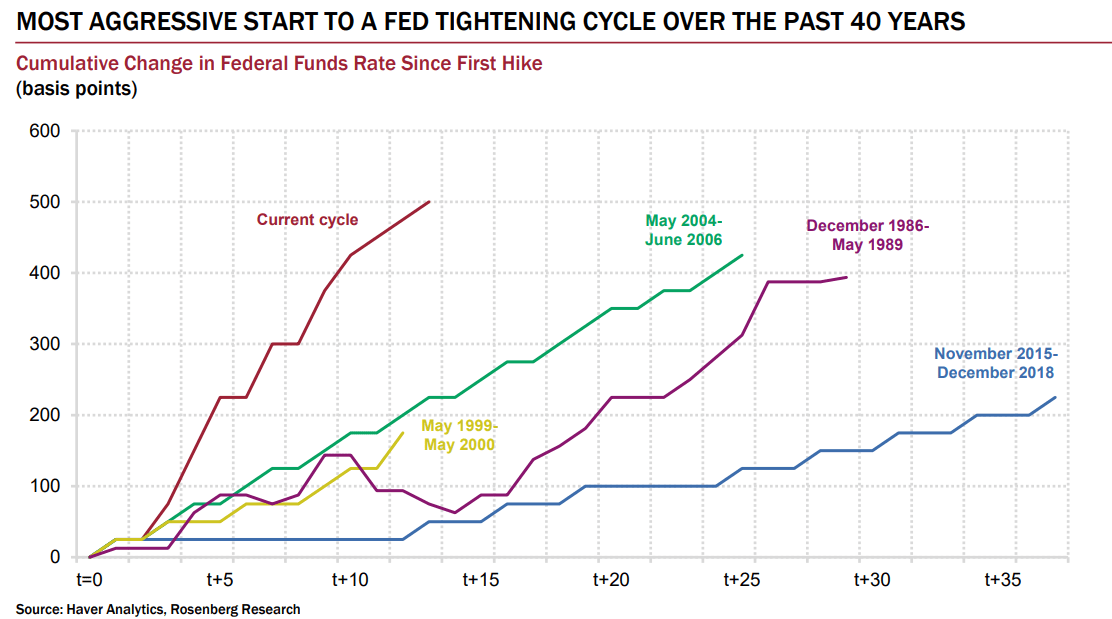

Over the past year or so, the Fed has raised interest rates at its most aggressive pace since the late 1970s -- faster than any rate hiking cycle since 1981.

{kind=link}

In such a heavily indebted economy, it would seem naive to believe that such aggressive rate hiking would not weigh heavily on the economy.

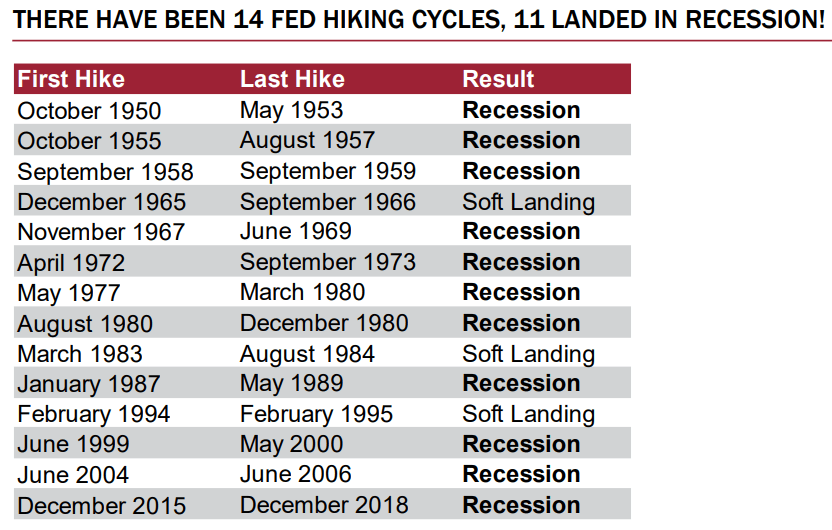

The overwhelming majority of rate hiking cycles (most of which were milder than the current one!) have led to recessions.

{kind=link}

How exactly do they do this? In two ways:

- Higher interest rates raise borrowing costs and reduce demand for debt from consumers, who reduce their spending, and businesses, who reduce investment.

- Banks are forced to tighten lending standards as inverted yield curves raise their cost of deposits and shrink their net interest margins.

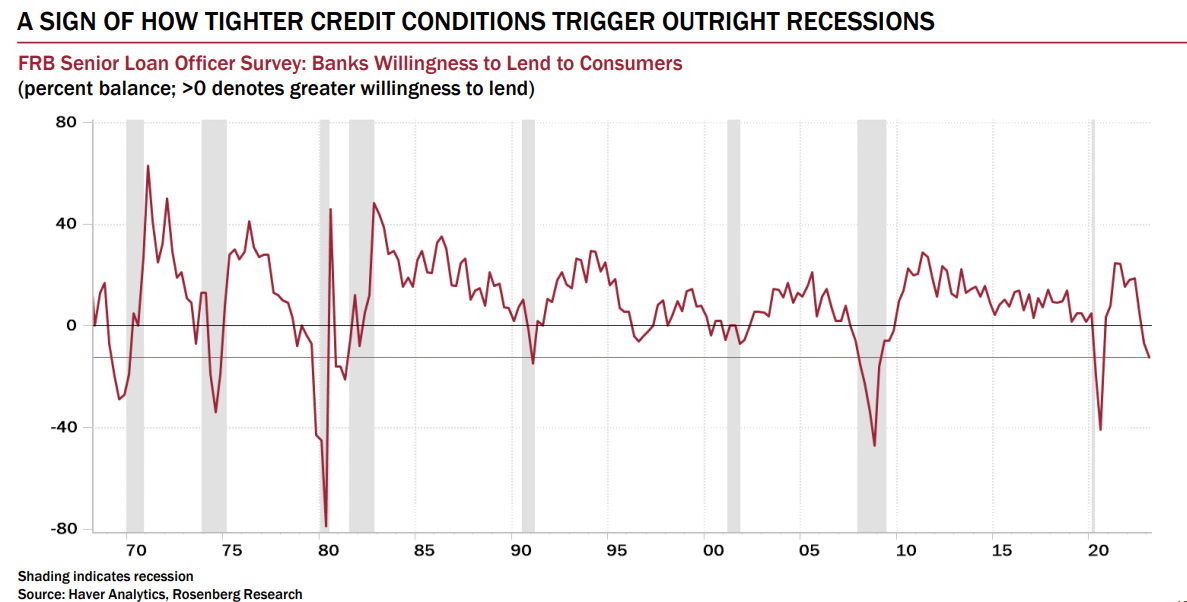

The pullback in banks' willingness to extend credit has been incredibly sharp in the last year, exacerbated by the failure of multiple regional banks in recent months.

{kind=link}

Less lending = less spending and investment = less economic activity.

Weakening Consumer Finances

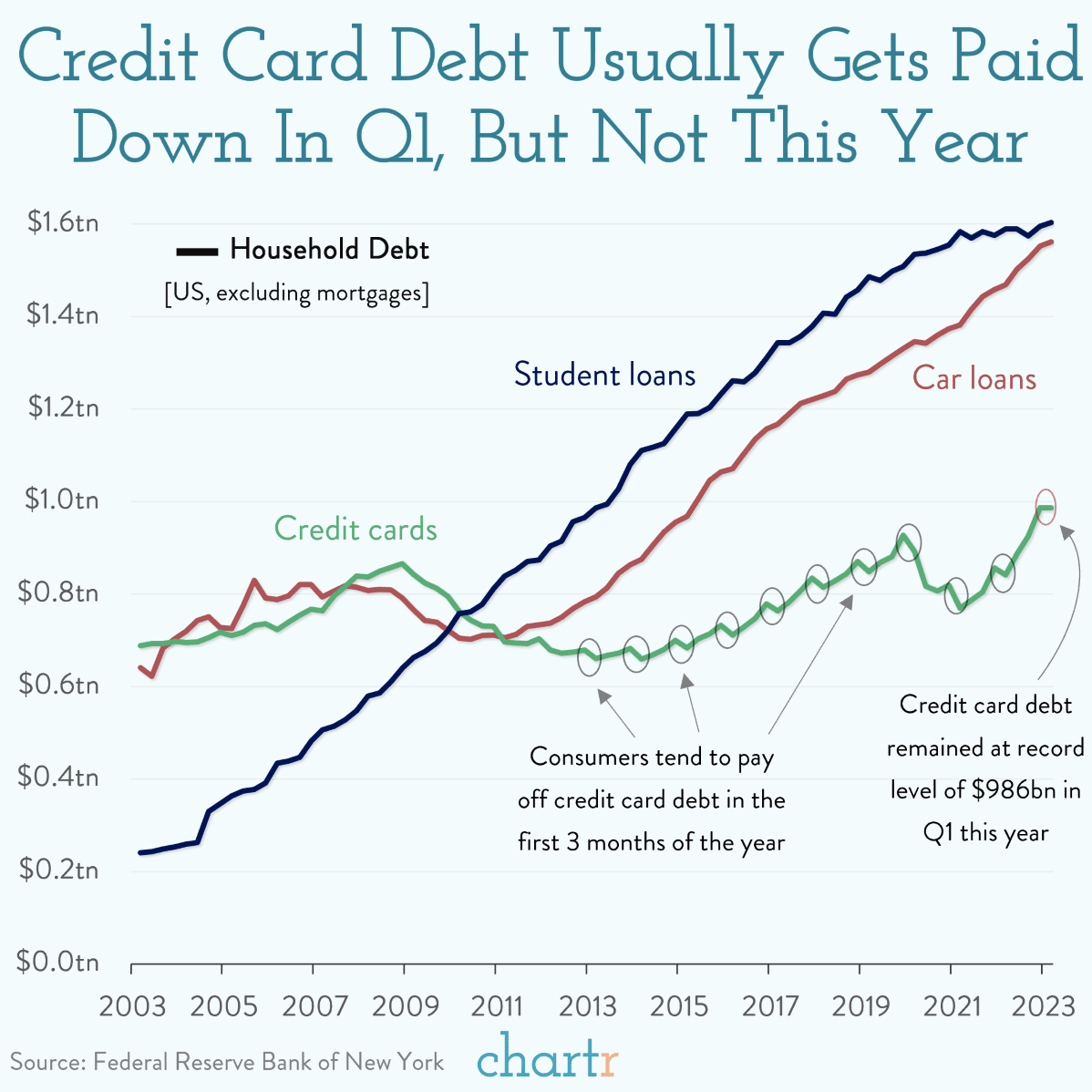

One of the primary reasons a recession has not begun already is that consumers had a large amount of savings from the fiscal stimulus that had not been immediately spent. But there are multiple signs that these pent-up savings have mostly been depleted, leaving consumers with less and less capacity to buoy economic growth by spending.

One sign of this is U.S. credit card debt, which remained at an all-time high just shy of $1 trillion in Q1.

{kind=link}

Interestingly, breaking with the well-established pattern of consumers paying off holiday credit card balances in the first three months of the new year, Q1 2023 credit card debt stayed flat quarter-over-quarter.

If consumers were still financially healthy with ample savings, why would they not pay down the credit card balances from their holiday spending? Given 20%+ credit card interest rates, we doubt consumers would choose to keep this level of debt if they had the ability to pay it down.

Now consider that, after two years of elevated growth in retail sales, retail spending is now pretty much flat YoY.

YCHARTS

And this is nominal retail sales. If you listen to the conference calls of almost any retailer, you'll find that revenue is rising mostly or entirely due to price increases, not growth in the volume of units sold.

For the most part, retailers are selling fewer widgets at higher prices.

Disinflation Reasserting Itself

But how long can businesses continue to raise prices?

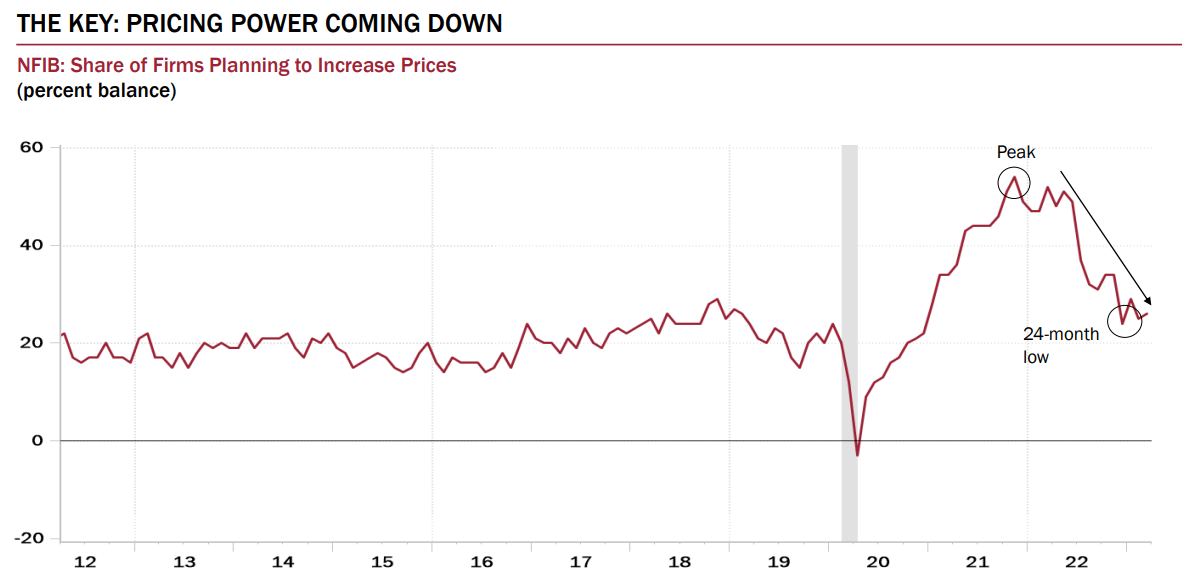

According to most of them: Not much longer. The bulk of price hikes are behind us.

According to the National Federation of Independent Business, over half of businesses planned to increase prices around the end of 2021. Today, only about 25% plan to raise prices.

{kind=link}

For reference, this number of firms planning to raise their prices is only slightly above 2019 levels and around the same as the level from the second half of 2018.

(Anecdotal evidence: For the first time in a few years, I [Austin] noticed lots of discounts on price placards at the grocery store the last time I went. Be on the lookout for slashed prices like this. They are a sign of diminished consumer spending and increased pressure on retailers to reduce inventory.)

But businesses are less eager to raise prices not just because of a weakening consumer. They also feel less need to raise prices because input prices for commodities and materials have been falling.

After big surges in 2022, commodity prices have been falling across the board this year.

Alliance Bernstein

That's great news for goods producers.

But what about services?

It's true that services inflation has been among the most stubborn as it remains elevated because of rising labor costs due to the worker shortage.

There are a few reasons for optimism about services inflation coming down soon.

First, though the services segment of the CPI remains elevated, the services segment of the producer price index , which amounts to input costs for consumer service providers, has been much more muted.

YCHARTS

Prices have continued to creep up for services largely because of consumers' "revenge spending" on travel, hotels, vacations, massages, dog boarding, etc. that had been foregone during the pandemic.

But travel plans are made months in advance, which means that consumer demand for services will be the last domino to fall on the consumer side of the economy.

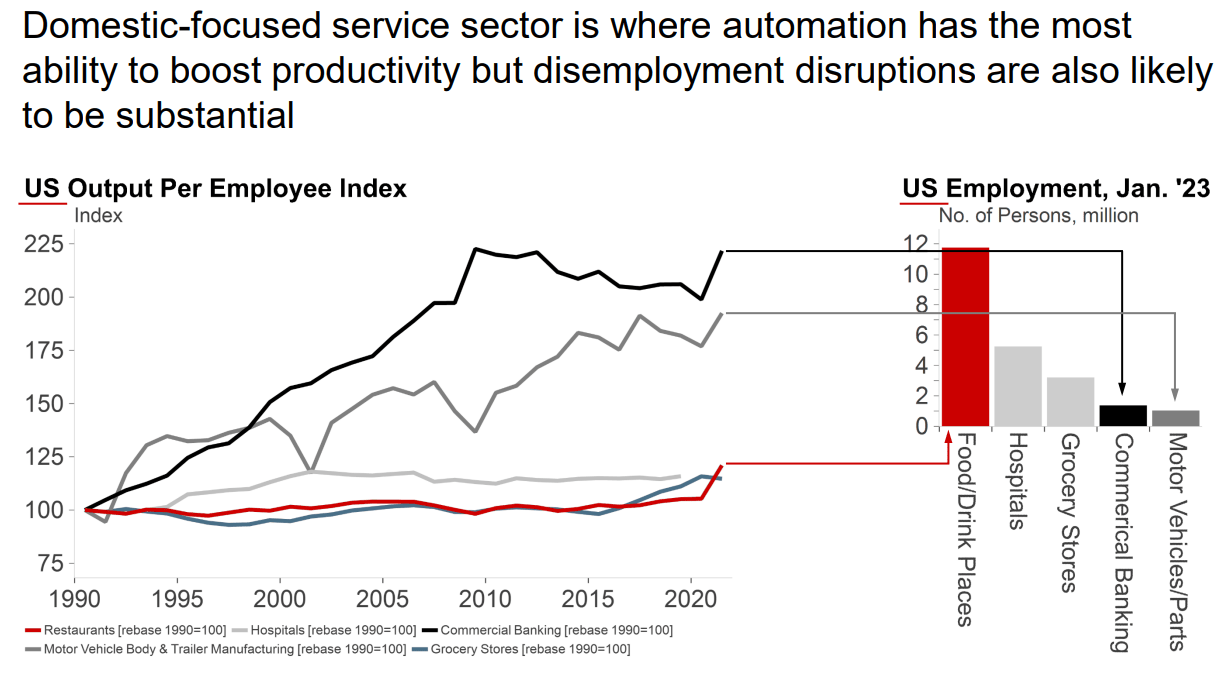

What about the increasing labor costs for services providers? In services, labor is often the largest cost of doing business, and as such, rising wages often brings with it higher prices for consumers.

But some experts think that automation and AI are poised to have a major beneficial effect on labor productivity in some of the most labor-heavy industries like restaurants, hospitals, and grocery stores.

{kind=link}

While this would likely reduce demand for workers in these industries, it should also increase productivity per worker, which could in turn result in higher wages per worker.

CPI "Shelter" Disinflation Has Just Begun

One of the only things keeping the headline year-over-year CPI number as high as it remains today is the "shelter" component, which lags real-time changes in housing costs by about a year.

The lag is easy to illustrate with a few charts.

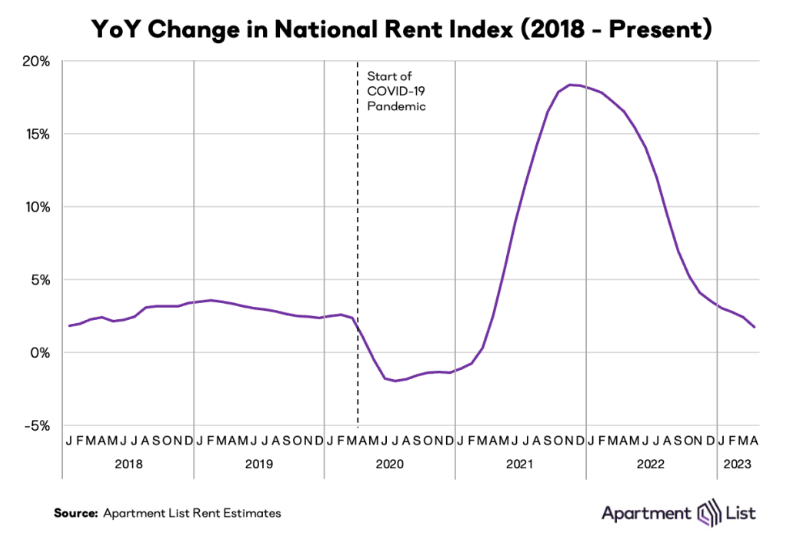

For real-time information about housing prices, take a look first at Apartment List's YoY change in the national rend index:

{kind=link}

As you can see, it has fallen from the high teens back down to the pre-COVID YoY growth rate of the low single-digits.

Meanwhile, here's how the national home price index looks year-over-year:

YCHARTS

While YoY growth in home prices crested 20% a little over a year ago, they've since dropped back down to the low single-digits.

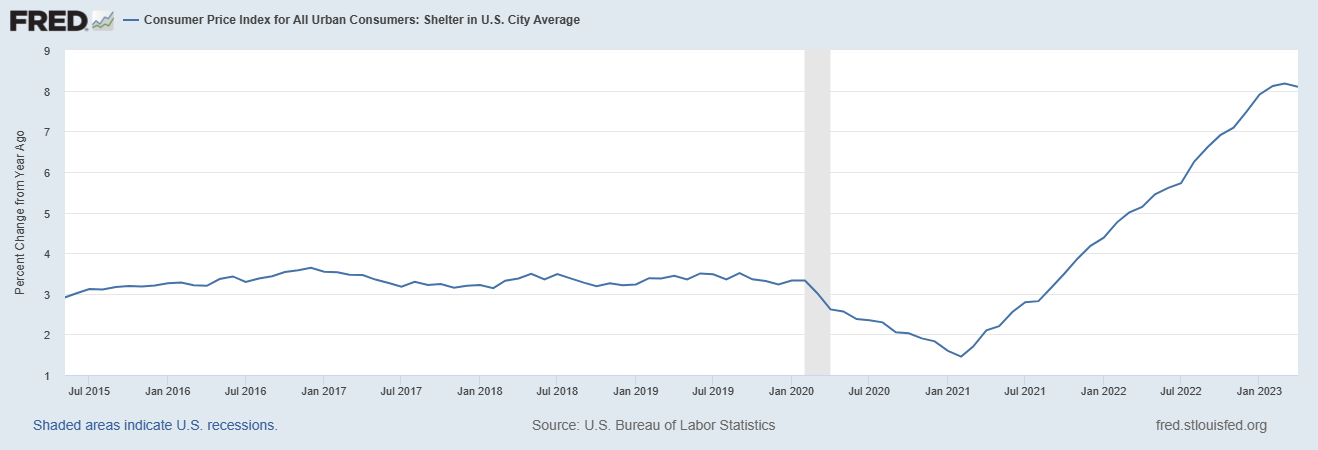

And yet , despite these real-time indicators showing that housing cost growth has dropped, the lagging shelter component of the CPI continued to show YoY growth in housing costs of over 8% as recently as April!

US CPI: Shelter (YoY Percent Growth):

{kind=link}

But, as you may be able to see in the chart above, the shelter component of the CPI has reached its (lagged) peak and is now on its way back down, following the real-time housing cost data presented in the charts above.

As the CPI shelter component follows the real-time data, we should expect to see it cause an increasing drag on the headline YoY CPI number for at least the next year, but probably longer than that.

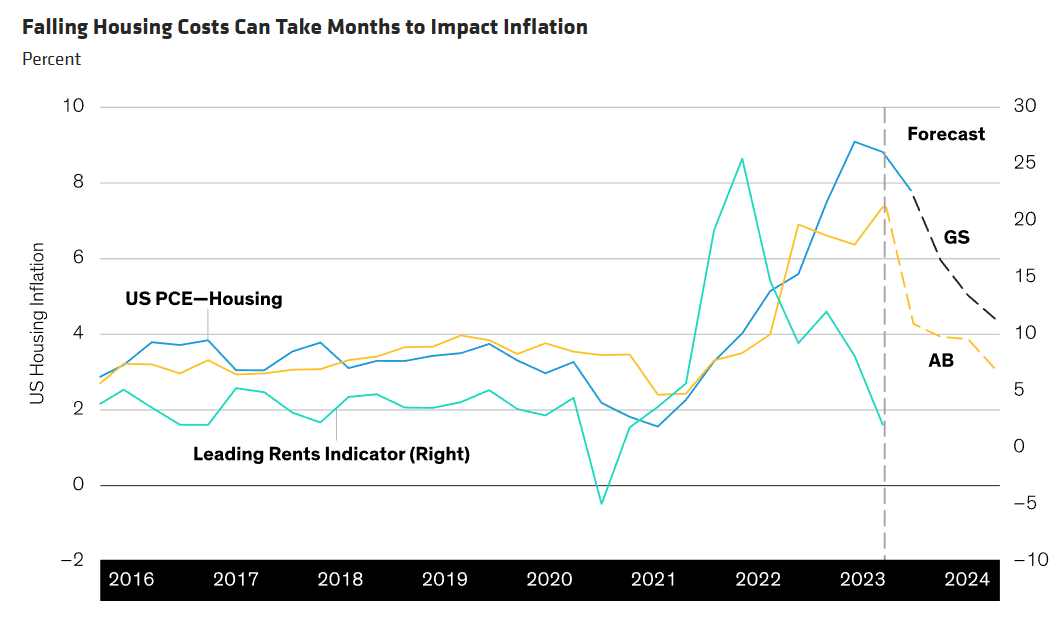

To show it all together, here's a chart from Alliance Bernstein illustrating the housing component of the PCE (personal consumption expenditures) index as well as Alliance Bernstein's and Goldman Sachs' forecasts for where this metric is headed going forward:

{kind=link}

As you can see, the U.S. shelter/housing components of the CPI and PCE both follow the leading rents indicator with about a one-year lag, so both AB and GS forecast that this inflation component will fall well into 2024.

In fact, according to macro maven Eric Basmajian , annualized growth in CPI ex shelter has been a mere 1.4% over the last 8 months and 1.2% over the last three months. So, if we omit the lagged shelter component of the CPI, the Fed has already overshot their target of 2% annual inflation!

Takeaway For Investors

The economy is weakening. The American consumer is reining in spending. Credit conditions are very tight. Some of the largest bank failures in U.S. history have taken place in just the last few months.

Meanwhile, just as the Fed reacted far too late to swelling inflation, they now appear to be reacting far too late to economic weakness.

At High Yield Landlord, we don't make investment decisions based on macro factors alone. We are fundamentally bottom-up value investors.

But awareness of current conditions, especially the likelihood of an impending recession, can inform our investment decisions.

Today, most of our REIT investments have defensive businesses that should do relatively well in a recession and they also enjoy relatively low payout ratios, low debt, few upcoming debt maturities, and time-tested strategies and management teams.

Examples would include Alexandria Real Estate ( ARE ), Essential Properties Realty Trust ( EPRT ), Crown Castle ( CCI ), and Safehold ( SAFE ).

But even more importantly, they are heavily discounted and should enjoy significant upside potential given our view that inflation is already lower than is being reported in the headline numbers and it is only a matter of time before interest rates also fall.

While falling interest rates will benefit all REITs, we think our selection of REITs should do particularly well and outperform the market.

For further details see:

Buy The Dips: High Inflation Should End Soon