SNYNF - Buy These 3 Deep Value A-Rated Dividend Stocks Hand Over Fist

2023-12-04 07:05:00 ET

Summary

- Here are three undervalued stocks with promising growth potential and high-quality A-rated balance sheets.

- It's just one of three incredible opportunities that combine to create a 16% annual return potential for the next decade, 350%, almost 3X more than the S&P.

- These are wide moat industry legends, blue-chip bargains hiding in plain sight.

- Wall Street has been blinded by its obsession with explosive growth in AI and obesity drugs. But that creates incredible opportunities to lock in gains in other megatrends.

- In the short term, luck is 20X as powerful as fundamentals. In the long term, fundamentals are 33X as powerful as luck. That's where regular investors like you have an edge.

This article was co-produced with Kody Kester of Kody's Dividends .

----------------------------------------------------------------------------------

No matter what the market is doing, there are always potentially smart investment options.

This especially includes ultra SWANS, the closest thing to a sure bet over the long run in this uncertain world.

Caterpillar Inc. ( CAT ), Sanofi ( SNY ), and Prologis, Inc. ( PLD ) are three businesses with promising growth potential, investment-grade balance sheets, and trading 23% under historical fair value.

Buying these companies could limit downside risk versus the 12% premium that the S&P 500 (SP500) is currently sporting.

The trio could deliver nearly 350% cumulative total returns in the next ten years, 2.5X the S&P.

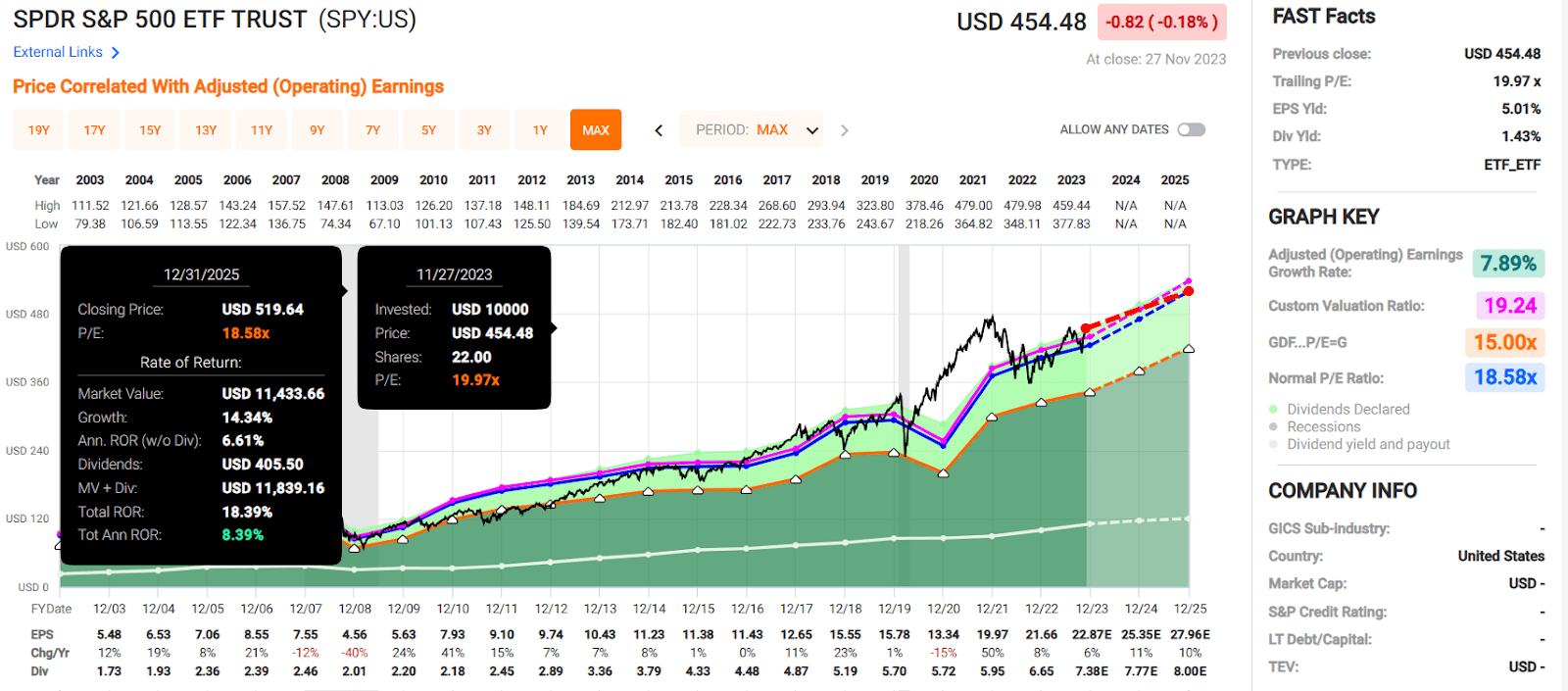

The market is 12% overvalued at 18.8X forward earnings, without even factoring in a recession on the horizon.

The good news is that at any given time, excellent dividend-paying stocks are attractively valued. Here are three strong-to-very-strong buys we’ll dive into as the article unfolds.

They are 23% undervalued and could trounce the market’s long-term total return potential.

In the next decade, analysts expect 341% cumulative total returns from the trio, compared to 137% from the S&P 500.

Savvy investors know that regardless of what is happening in the world or financial markets, there will always be intelligent investments that can be made. That is because, as many bright minds in the investing community have said, the stock market is a market of stocks.

FactSet, Goldman

The S&P 500’s forward P/E ratio of 18.8 (not even factoring in a probable 2024 recession) is 12% above its historical forward P/E ratio of 16.8. As the saying goes, the stock market is a market of stocks; this could be discouraging.

But when looking deeper, investors will find that most of the S&P’s 19% gains in 2023 were powered by the 70%+ average gains of the Magnificent 7. For context, Goldman Sachs’ ( GS ) equity research team found that the S&P 493 (less those 7 large stocks) has gained just 6% year to date.

Simply put, plenty of other world-class businesses have largely traded range bound in 2023. Here are three that could significantly outpace the S&P 500’s projected cumulative returns for the coming ten years.

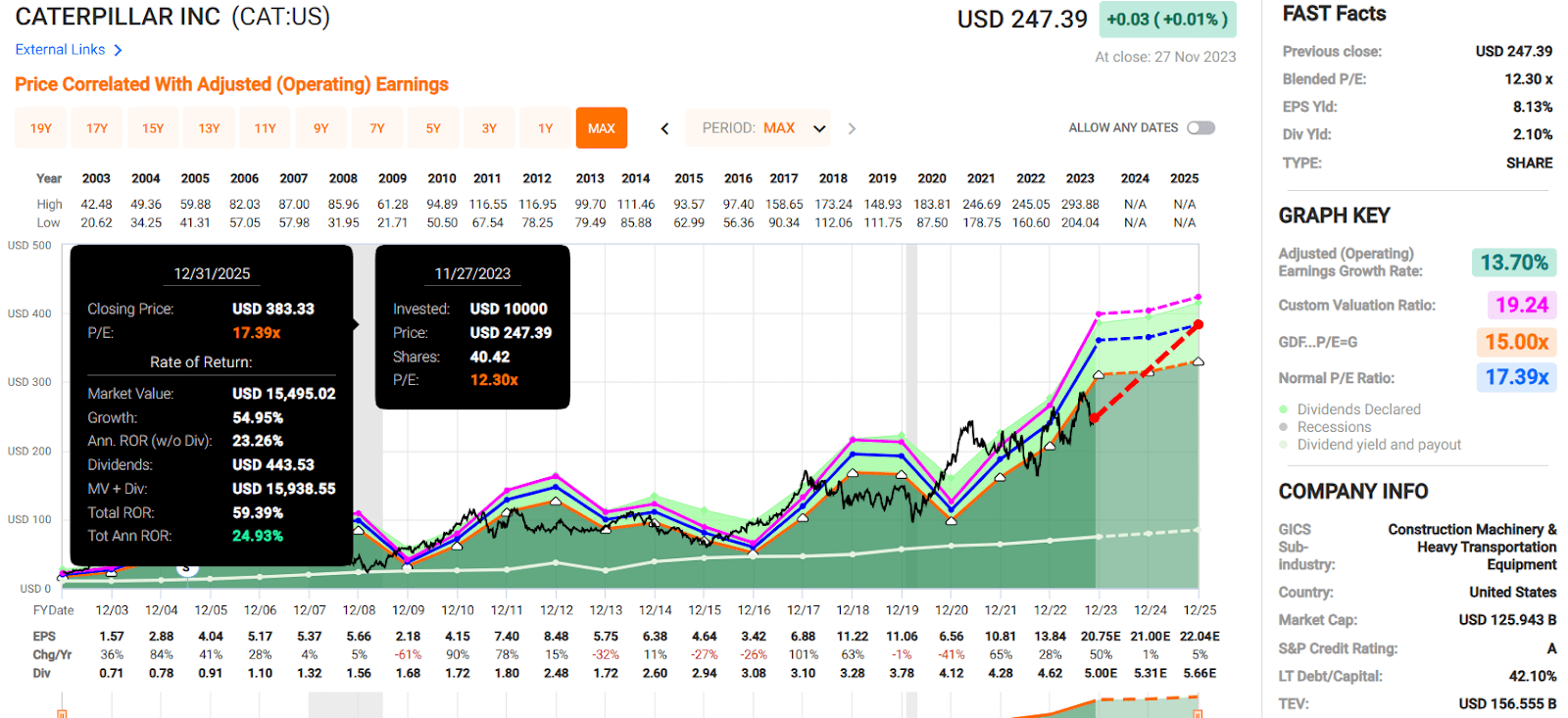

Caterpillar: A Leading Industrial Dividend Aristocrat

Many industries we rely on most daily heavily lean on the equipment sold by the industrial powerhouse Caterpillar. These most prominently include the construction, mining, energy, and transportation industries. Caterpillar’s $59.4 billion in 2022 revenue positions it as the most dominant industrial company in the world.

Investor Presentation

The company’s global footprint should position it well for the future. This is because Caterpillar consistently derives over half of its revenue outside of the United States, with many of these markets growing in population at higher rates. Greater population numbers and expanding global wealth should translate into more demand for housing and the raw materials that make our lives possible. Thus, construction and mining equipment demand should also grow throughout a full economic cycle. This explains why FactSet Research believes Caterpillar’s earnings can grow by 17.3% annually.

The company also stands out for its 29-year dividend growth streak, which makes it a Dividend Aristocrat. Caterpillar’s 2.1% yield appears to be reasonably safe moving forward. The company’s 31% EPS payout ratio is well below the 40% EPS payout ratio that credit rating agencies consider safe for industrials per Dividend Kings.

Caterpillar’s balance sheet is also healthy. The company’s 39% debt-to-capital ratio is comfortably lower than the 50% rating agencies prefer from industrials. That’s why Caterpillar enjoys an A credit rating from S&P on a stable outlook. This implies a mere 0.66% risk of the company going bankrupt by 2053.

As a cyclical business, it’s hard to predict where Caterpillar stock goes in the next few weeks, months, or even years. But based on its historical fair value using dividend yield and P/E ratio, Dividend Kings estimates the fair value of the stock to be $360 a share. From the current $247 share price (as of November 28, 2023), Caterpillar is 31% undervalued.

If the company grows as anticipated and returns to fair value, here are the returns it could generate for shareholders in the 10 years that lie ahead:

-

2.1% yield + 17.3% FactSet Research annual earnings growth consensus + 3.8% annual valuation multiple expansion = 23.2% annual total return potential or a 706% cumulative 10-year total return vs S&P 134%.

{kind=link}

S&P 500

{kind=link}

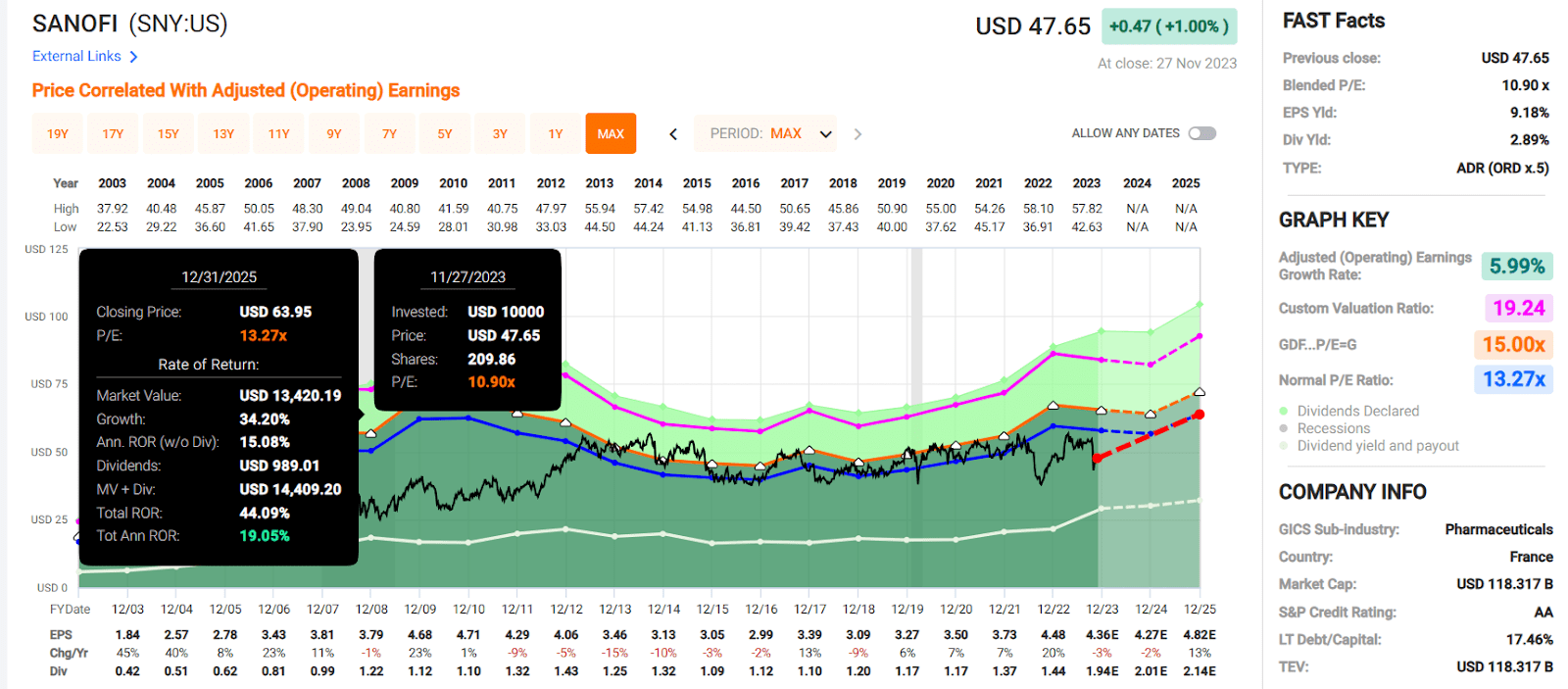

Sanofi: A Pharmaceutical Giant With A Deep Product Portfolio And Pipeline

Statista

More politically astute readers have probably heard the cliché from the French philosopher Auguste Comte that demography is destiny. Well, this can also be applied to investing. Aside from investing in high-quality businesses, it helps to pick businesses that have demographics on their side.

As one of the planet’s biggest pharmaceutical companies with hit products like the immunology drug Dupixent, influenza vaccines, and polio/pertussis vaccines, Sanofi is a business that fits this mold. Few industries have more favorable demographics than pharmaceuticals. Though there are exceptions, people tend to require more medicines and medical treatment as they age. As shown above, the median global age is expected to rise steadily from around 31 to over 41 by the end of this century.

Sanofi and its admirable portfolio of medicines/vaccines aren’t just built for the immediate term. As of its most recent update, the company had 24 projects in phase 1 clinical trials, 32 in phase 2 clinical trials, and 22 in phase 3 clinical trials within its development pipeline . In other words, Sanofi is a well-balanced pharmaceutical that looks poised to overcome the patent cliffs common with its industry. That is why FactSet Research forecasts the company’s earnings will rise by 5.2% annually over the long haul.

Sanofi’s 4.1% dividend yield also seems to be sustainable. The company’s 44% EPS payout ratio is below the 60% rating agencies like to see. This dividend is further supported by an 18% debt-to-capital ratio, well under the 40% rating agencies view as viable for Sanofi’s industry. That is why the company possesses an AA credit rating from S&P on a stable outlook. This suggests Sanofi’s 30-year probability of bankruptcy is just 0.51%. Put another way, in 195 out of 196 scenarios, rating agencies don’t envision the company defaulting on its debt through 2053.

Topping off the buy case for Sanofi, the stock is 22% undervalued relative to its $60 fair value estimate from Dividend Kings. If the company meets growth expectations and reverts to fair value, here are the returns it could produce:

-

4.1% yield + 5.2% FactSet Research annual earnings growth consensus + 2.5% annual valuation multiple upside = 11.8% annual total return potential or a 205% 10-year cumulative total return vs S&P 134%.

{kind=link}

Prologis: Cashing In On A Thriving Industrial Real Estate Market

Investor Presentation

Owning and leasing over 5,000 industrial properties globally, Prologis is the most dominant industrial REIT. Since the world relies on industrial real estate tenants more each day for basic daily needs, life upgrades, and online shopping, this is a very enviable space to operate. As the demand for the goods moved through the company’s warehouses has risen, this has created a favorable supply and demand dynamic for Prologis.

That was evidenced by a 97%+ occupancy rate in its third quarter and sizable rent growth on lease renewals in key markets during the quarter. These trends will likely continue due to the defensive nature of daily needs and the secular growth of e-commerce. This is why FactSet Research estimates that the company will grow core funds from operations ("FFO") per diluted share by 8% annually.

Prologis’ 3.1% dividend yield is also covered, with a 78% payout ratio. This is about in line with the 75% preferred by rating agencies. The company’s 34% debt-to-capital ratio is less than the 50% rating agencies desire. This is why Prologis’ debt is rated an A on a stable outlook from S&P.

Finally, the company trades at a 16% discount versus Dividend Kings’ $133 fair value. If Prologis can match the growth consensus, here are the returns that it could deliver:

-

3.1% dividend yield + 8% annual growth + a 1.8% annual valuation multiple boost = 12.9% annual total return potential or a 236% 10-year cumulative total return vs S&P 134%.

{kind=link}

Summary: 3 Cheap Dividend Stocks That Could Come Roaring Back

Dividend Kings Zen Research Terminal

I believe Caterpillar, Sanofi, and Prologis are three of the highest-quality dividend stocks that money can buy. Each of the businesses has solid growth prospects and first-rate balance sheets.

Together, they are 23% discounted relative to fair value. Their 3.1% yield, 10.2% annual growth, and 2.7% annual valuation multiple expansion could produce 16% annual total returns through the next ten years. That’s considerably better than the 9% annual total return that the S&P 500 is predicted to generate over that time.

The trio could deliver nearly 350% cumulative total returns in the next ten years, 2.5X the S&P.

For further details see:

Buy These 3 Deep Value, A-Rated Dividend Stocks Hand Over Fist