CRGY - Buybacks Or Dividends? What Worked Better So Far

Summary

- As oil and gas companies have shifted from survival to cash generation mode, their capital return strategies have come into focus.

- Some U.S. independents prioritize buybacks while others rely on dividends; few companies employ a mix of both strategies.

- I explore if there is a systematic relationship between capital return policies and stock price performance based on 43 American independent producers.

- The market may be sophisticated enough to see through the capital return framework.

In 2022, many oil and gas producers shifted their focus from fixing their balance sheets to returning capital to the shareholders. However, the capital return strategies have varied. Among the larger caps, Marathon Oil ( MRO ), APA Corporation ( APA ) and Occidental ( OXY ) have prioritized buybacks. On the other hand, EOG Resources ( EOG ), Devon ( DVN ) or Pioneer ( PXD ) have emphasized variable or "special" dividends. Fewer companies such as ConocoPhillips ( COP ) have pursued a mix of both strategies.

The article investigates if the capital return strategy had a systematic effect on stock price performance based on a group of 43 independent American-based oil and gas producers ( XOP ). While 2022 was the year when everything related to energy went up, I expect that in 2023 we may see more differentiation in relative performance. A company's capital return policy may potentially be one of the differentiating factors.

The financial theory is mixed

In 1961 Miller and Modigliani famously argued that, in a world without taxes, transaction costs or asymmetric information between management and the shareholders, the dividend policy should be irrelevant for valuations. In the MM world there is no meaningful distinction between dividends or buybacks either; investors can always generate a "homemade dividend" by selling shares. The only thing that really matters is the quality of the company's future investment opportunities.

In practice, however, the MM conditions don't hold true. Taxation will be a significant factor for many investors. Transaction costs aren't zero and selling a volatile stock doesn't provide the same income stability as a dividend. Asymmetric information may also lead to a preference for dividends as the regular payout puts a constraint on management's ability to invest in negative present value projects.

Empirically, there is no conclusive evidence that dividend policy affects value either, given that valuations depend on so many other factors. However, as a general rule, the companies that pay greater dividends tend to be more mature businesses with limited reinvestment opportunities. Dividend paying companies also typically come from less cyclical industries.

What worked better for E&P companies so far?

To explore the capital return question more systematically, I looked at a group of 43 independent U.S. based oil and gas exploration and production (or E&P) companies. I came up with this group using Seeking Alpha's stock screener and including U.S. based E&P companies with minimum market cap of $200 million. I disregarded royalty companies and a couple offshore producers, such as Talos Energy ( TALO ), which are focusing on growth rather than returning cash. That left me with mostly U.S. shale players ranging by market cap from the smallest pick, Evolution Petroleum ( EPM ), all the way to largest one, ConocoPhillips.

As many companies haven't reported 2022 Q4 yet, I looked at the returns of capital from 2021 Q4 through 2022 Q3 and stock price appreciation during the calendar 2022.

Observation #1: Fixed dividends aren't the norm

Dividend payers proliferate in less cyclical sectors, and E&P is certainly not among them. Energy companies (XLE) known for their dividends are typically midstream stocks ( AMLP ) that rely on long-term take-or-pay arrangements to stabilize their cash flows. Even the majors Exxon ( XOM ) and Chevron ( CVX ) can afford a more generous fixed dividend because their midstream and downstream segments hedge to some extent their upstream production.

Of the 43 tickers I looked at, only 3 perhaps depart from the norm:

| Company |

| SA dividend yield |

| Stock price in 2022 |

| Evolution Petroleum |

| 6.88% |

| + 59% |

| Crescent Energy ( CRGY ) |

| 5.08% |

| - 2% |

| Devon |

| 4.03% |

| + 51% |

| All companies average |

| 1.43% |

| + 45% |

Data: Seeking Alpha. The yields may deviate from the time of writing.

For most E&Ps, the decision to avoid large fixed dividends is probably a wise one because the cyclical exposure to the commodity price will always be there. A big fixed dividend can't mask this, and there will inevitably be situations when the company needs to lever up to maintain the dividend. The recent crash in natural gas prices ( NG1:COM ) illustrates the point well. The fact that the top fixed dividend players didn't differentiate themselves much from the rest of the pack may be showing that the market understands this too.

Observation #2: Buybacks and variable dividends are common but few companies use both

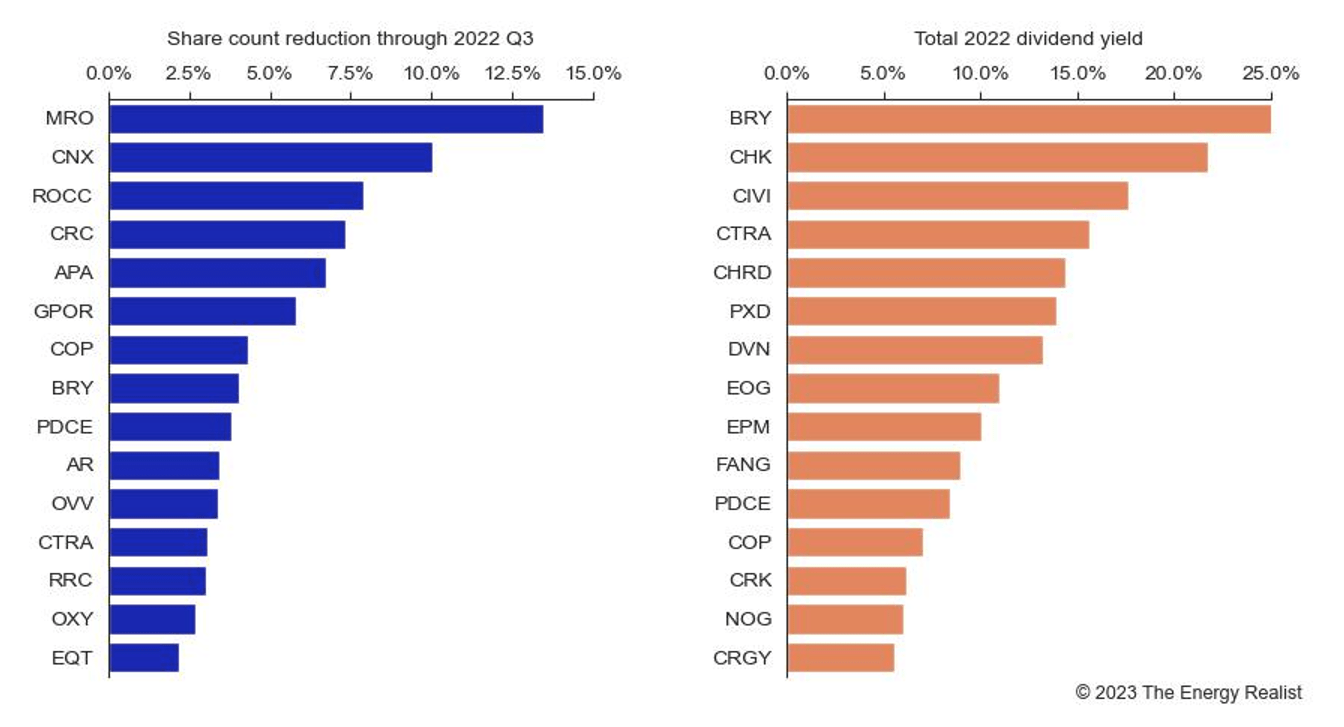

While large fixed dividends are the exception, there was no shortage of variable dividends and buybacks to top up the fixed payouts. I summarized the Top 15 companies by share count reduction (through 2022 Q3) and total dividends paid (2021 Q4 to 2022 Q3):

{kind=link}

While some companies issued shares in the context of acquisitions, for example, Earthstone Energy ( ESTE ), I think the share count reduction is still a reasonable metric here. What is interesting is that few companies balance their policy. Only Conoco and Coterra ( CTRA ) are in both Top 15 lists as they appear to be pursuing a mix of these strategies.

I don't have a good theory for what drives these choices. My guess is that managements may be trying to match the preferences of their largest investors. If that is the case, these distribution strategies should also be fairly persistent over time.

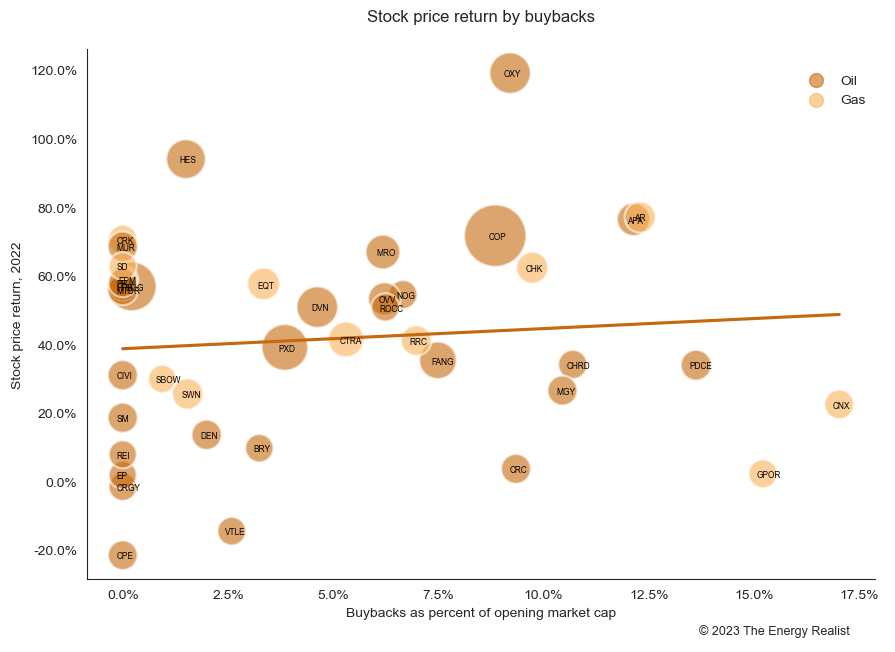

Observation #3: Buybacks had a modest correlation to stock price return

I correlated the cumulative amount spent on buybacks (2021 Q4 through 2022 Q3), scaled by the opening market cap, to the 2022 stock price return:

{kind=link}

The bubble sizes correspond to the opening market cap and I marked separately gas and oil-focused producers. The amount spent on buybacks was a driver of stock price performance but probably a rather modest one. OXY and Hess ( HES ) stand out as the two tickers that significantly outperformed the rest of the group.

Observation #4: Total dividend payouts were also modestly correlated to stock price returns

A similar plot shows the relationship between the total dividend payout (fixed plus variable dividend) and the stock price:

{kind=link}

The relationship appears a bit stronger than the buybacks one. However, there is a lot of dispersion in the lower end of the dividend spectrum as many smaller companies paid no dividend whatsoever.

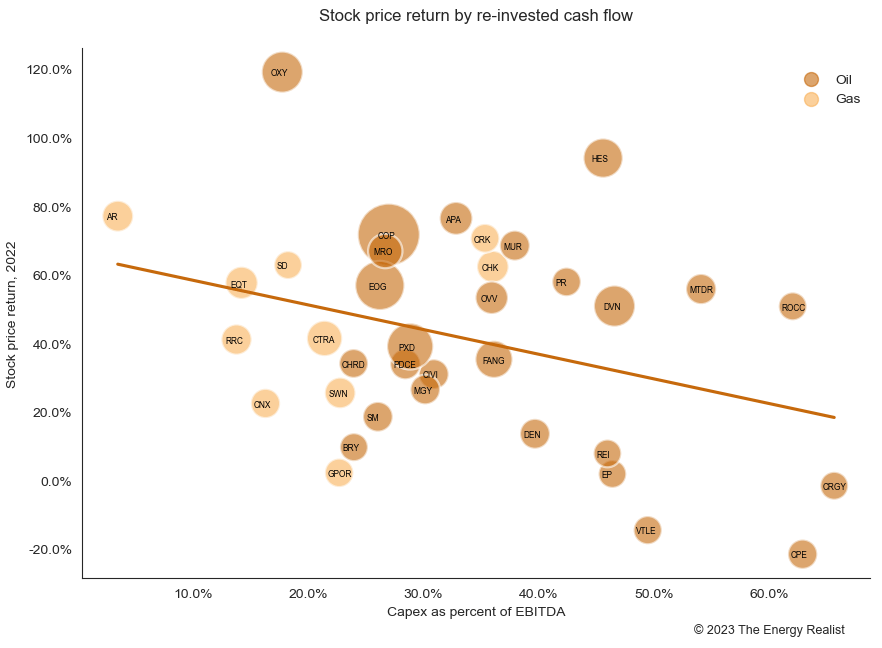

Observation #5: The overall capital returned may matter more than the return mechanism

I next combine Observations #3 and #4 by looking at how much of EBITDA was re-invested into capex. The amount not re-invested is a proxy for the amount available for capital returns so this should be an inverse relationship:

{kind=link}

This is indeed the strongest relationship so far as it implies a 40% reduction in stock price performance going from the companies that re-invested least to those that did so the most. Interestingly, the gassy companies mostly showed lower capex to EBITDA percentages, which makes sense given 2022 was also the year of the natural gas windfall. These statistics may look very different at the end of 2023 though if gas prices remain suppressed.

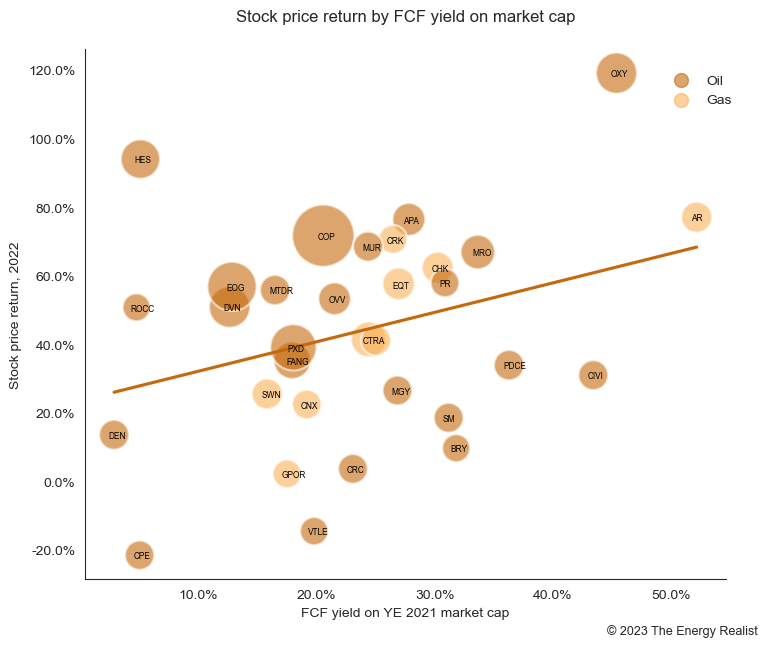

Observation #6: Starting valuations matter too

Two strong predictors of performance weren't related to capital returns, though. First, the starting valuation, measured below as free cash flow (or FCF) yield on the opening market cap was an important factor:

{kind=link}

Again, OXY and HES performed way above the trendline.

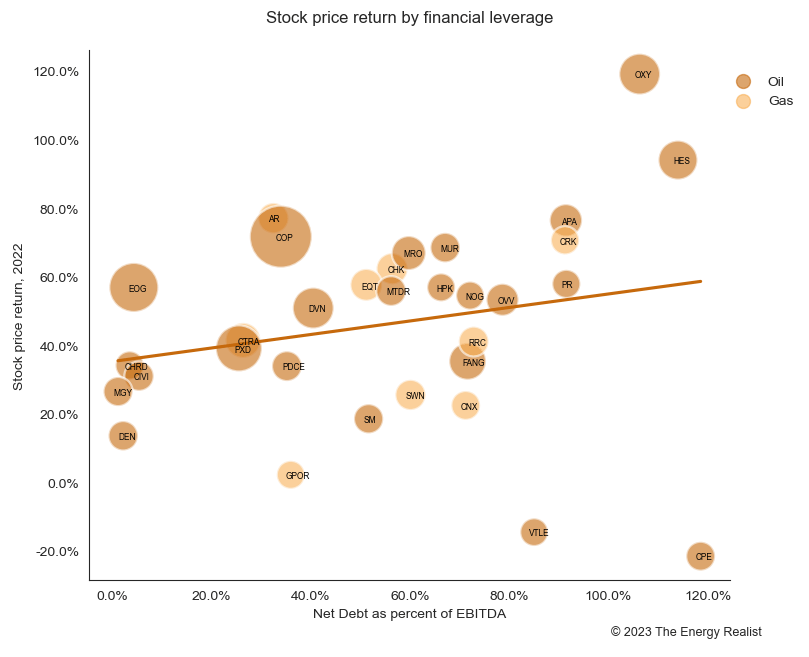

Observation #7: Leverage magnifies the equity returns

Lastly, more leveraged companies outdid their financially stronger peers:

{kind=link}

This actually makes a lot of sense in a Miller-Modigliani world, but is somewhat counter-intuitive as oil companies have been working hard to improve their balance sheets. Yet, that improvement will only yield a benefit when oil prices ( CL1:COM ) turn downward and perhaps, in anticipation, reward them with a better valuation multiple. However, during a price strengthening environment, the more levered players do exhibit more "torque."

A few takeaways

Every company is unique so any approach that tries to compare a large number of companies based on a couple of standardized financial metrics will miss facts that are important to the individual stories. For example, HES and OXY have exhibited stock price returns way above where any of the driving factors explored here would have predicted them to be.

For Hess, I am convinced this is the Guyana growth story, which also shows that the market is willing to wait a few years for capital returns if the promise is sufficiently appealing. Occidental was one of the companies with highest leverage so to some extent that may explain its stock price movement, but it could also be the Buffett factor or the carbon capture presence - who knows.

Nonetheless, some of the patterns identified based on 2022 may be important for investors to pay attention to in the future. While company choices between buybacks or special (or even fixed) dividends may not have been that consequential so far, how much of the generated cash is re-invested does matter. Ultimately, I think that in 2023 this will come down to the quality of inventory as companies that may be running out of profitable acreage will have to increase capex relatively more to maintain production.

In that regard, Miller and Modigliani may be right after all, and the market isn't really rewarding the decision to return cash to the shareholders itself, but is rather penalizing companies that have poor re-investment opportunities due to diminishing inventory quality.

I am considering updating this article after all 2022 data is available, or perhaps after 2023 Q1 when we have a better idea which way this year's capex is heading. If you have suggestions on more analytics related to this topic that you think may be informative to see, please feel free to post your ideas in the comments.

For further details see:

Buybacks Or Dividends? What Worked Better So Far