BZZUF - Buzzi: Trading At Just 4 Times EBITDA Going-Private Candidate

2024-01-09 04:30:00 ET

Summary

- Buzzi, an Italy-based cement producer, expects stable results, but we expect a weaker demand in Q4 2023 and Q1 2024.

- The company's financial performance remained strong in the first nine months of 2023, thanks to government-mandated construction activities.

- Buzzi has a strong balance sheet with a net cash position of almost 700M EUR, allowing it to navigate through volatile times.

Introduction

The cement sector has outperformed my expectations in 2023 and in a recent article I published on Titan Cement (TTCIF), I explained that although the first nine months of 2023 were strong, some companies started to warn of a weaker demand in Q4 2023 and Q1 2024. Buzzi is a bit more upbeat as the company anticipates that government-mandated construction activities will mitigate the impact of lower demand from residential construction activities. Buzzi ( BZZUF ), an Italy-based cement producer where the Buzzi family owns in excess of 50% of the shares, expects a pretty stable result going forward. And that’s not necessarily a bad thing as I think the company is trading at a pretty attractive valuation even if there is no immediate growth to be expected. I previously discussed this company in 2019 in my ‘Focus on Europe’ article series .

{kind=link}

Buzzi’s primary listing is on Euronext Italy where it is trading with BZU as its ticker symbol on the Milan stock exchange. The average daily volume is almost 190,000 shares, making the Milan exchange by far the most liquid exchange to trade in the company’s securities. The Milan listing also has options available. The company currently has 185 shares outstanding, resulting in a market capitalization of approximately 5.3B EUR. I will use the Euro as the base currency throughout this article.

The European cement sector remains very strong

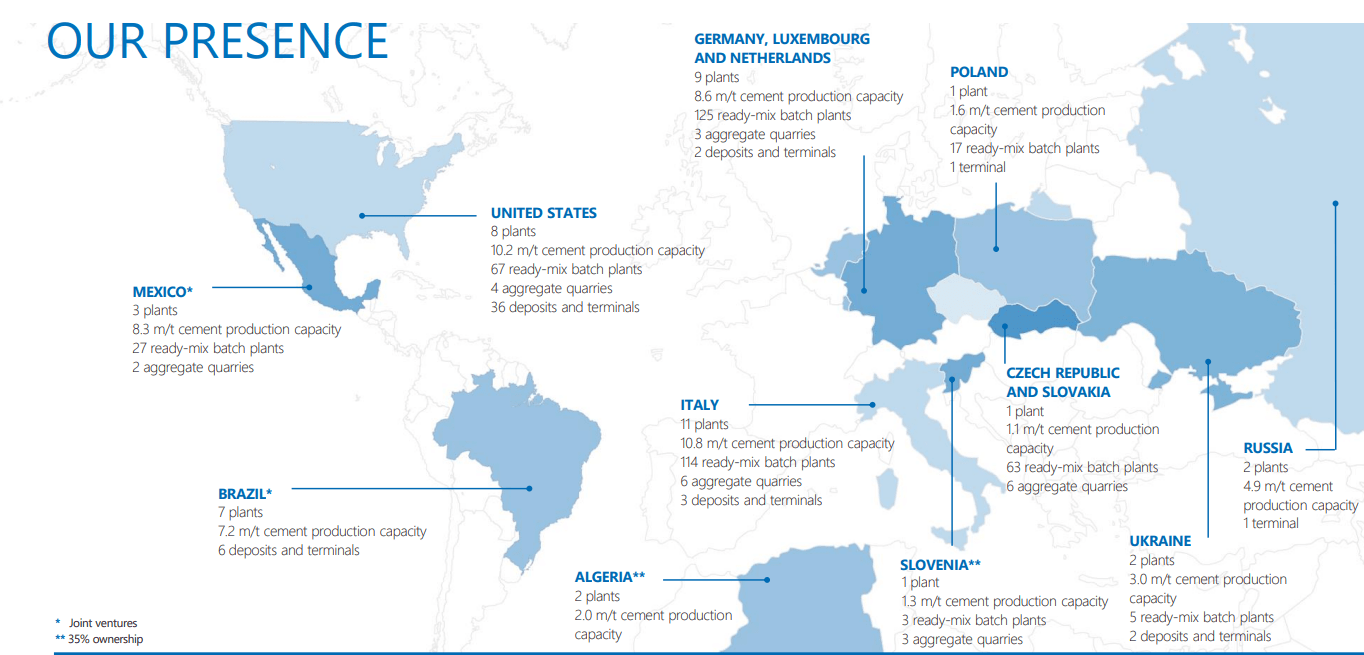

As explained in my recently published article , Titan Cement’s financial performance was pretty strong in the first six and nine months of the year and although Buzzi mentioned the ‘global economic activity continued to be penalized by the persistence of inflation’, its financial performance remained remarkably strong during the first nine months of the year. Fortunately, the company has a worldwide presence which helps to mitigate the impact of some economies being weaker than others.

{kind=link}

As Buzzi only publishes detailed financial results, I will first have a look at the detailed financials provided in the H1 2023 report before taking a step back and look at the Q3 trading update (which does not contain a detailed income statement or cash flow statement).

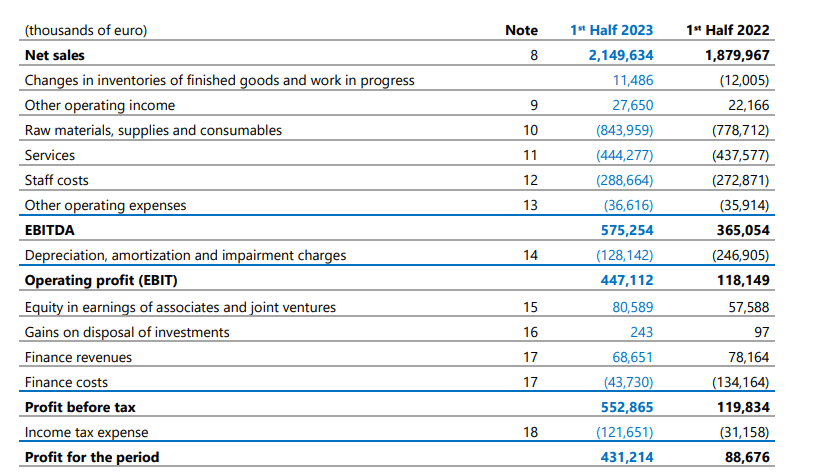

During the first half year of 2023, Buzzi reported a total revenue of 2.15B EUR, a nice increase compared to the 1.88B EUR in the first half of 2022. The EBITDA jumped by in excess of 50% thanks to the company being able to keep its COGS under control (these increased by less than 10%) while the SG&A expenses increased by just over 3.2%.

{kind=link}

The very strong EBITDA result obviously also resulted in a very strong net result. As the income statement above shows, the EBIT came in at 447M EUR which was almost four times higher than the H1 2022 EBIT but that’s not a fair comparison as Buzzi reported a nine-digit impairment charge during the first semester of 2022.

In any case, Buzzi’s bottom line shows a pretty impressive result with a net profit of 431M EUR for an EPS of 2.33 EUR. A very impressive result thanks to the margin expansion. Whereas Buzzi reported an EBITDA margin of 19.4% in the first half of 2022, this increased to almost 27% in the first half of the current financial year.

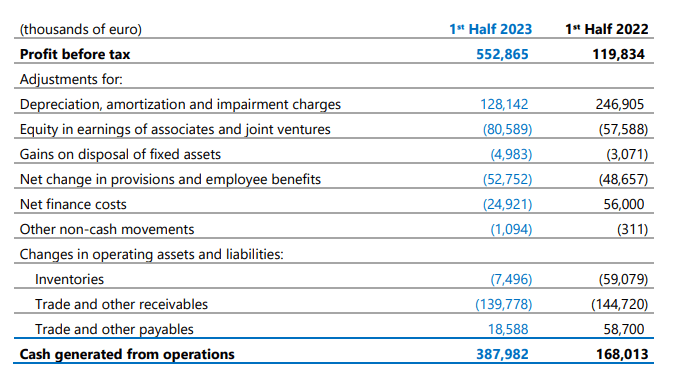

And the cash flow statement confirms these weren’t just paper profits as Buzzi benefits from a very strong cash inflow as well. The starting point of the cash flow statement is the ‘cash generated from operations’ which came in at 388M EUR but fortunately, the footnotes to the financial results contain more details on how the company obtained this result.

{kind=link}

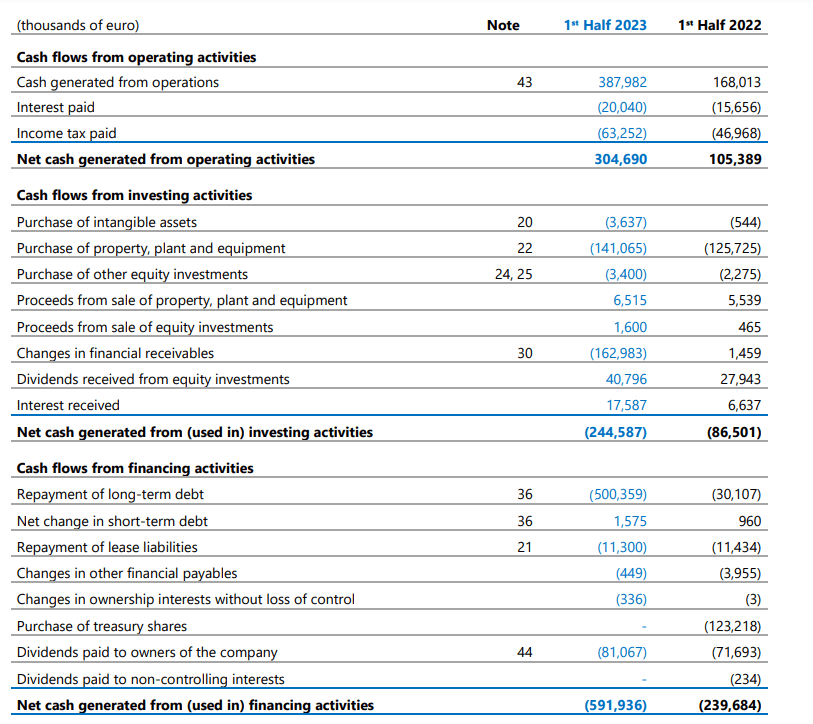

According to the footnote, the 388M EUR in cash generated from operations includes a 129M EUR investment in the working capital position. This means the operating cash flow before working capital adjustments wasn’t 305M EUR as shown below, but approximately 434M EUR. That being said, Buzzi only paid 63.3M EUR in cash taxes although it owed the tax man in excess of 120M EUR based on the H1 taxable income. I prefer to deduct the 58M EUR discrepancy and am also deducting the 11.3M EUR in lease payments. This results in an underlying operating cash flow of 364M EUR.

{kind=link}

The total capex was approximately 141M EUR, as shown below, but these investments were largely compensated by the 58M EUR in dividend and interest income. This means the underlying free cash flow in the first half of the year was approximately 281M EUR. Divided over a share count of approximately 185M shares, the FCFPS was 1.52 EUR. Lower than the reported net income but the explanation is pretty simple: Buzzi reported a total capex + lease payments of 153M EUR while the total depreciation and amortization expense was just 128M EUR. Additionally, the net equity earnings of associates and JVs exceeded 80M EUR but only 40.8M EUR was effectively paid out as a dividend.

In any case, Buzzi is in an excellent position to continue to benefit from a relatively stable demand for its cement products. And even if 2024 is a bit more uncertain, its exceptionally strong balance sheet should help the company to navigate through volatile times without too much of an effort. At the end of June, Buzzi had 787M EUR in cash on the balance sheet and just over 560M EUR in debt, resulting in a net cash position of almost a quarter of a billion euros.

The net cash position even improved in the third quarter as the company confirmed a net cash position of 673M EUR . This indicates the company’s third quarter was also pretty strong (and it is a pity no detailed financial results were published) while a portion of the working capital elements were likely converted into cash.

Investment thesis

Applying the Q3 net cash position, Buzzi’s enterprise value is just 4.7B EUR and with an anticipated EBITDA of 1.15B EUR (the midpoint of the official guidance) and an EBITDA of 1.13B EUR excluding lease amortization, the company is still trading at just over 4 times EBITDA which is pretty cheap for an established company without any financial sorrows. Looking at the consensus estimates, Buzzi’s EBITDA is expected to remain stable which means that the strong cash flows in combination with the relatively low dividend (0.45 EUR payable over FY 2022) will result in the net cash to increase by a nine-digit amount per year. The consensus estimates are pointing towards a net cash position of 1.8B EUR by the end of 2025 which would reduce the enterprise value to just 3B EUR and the EV/EBITDA to just 3.

This makes Buzzi an interesting candidate for a family-led take-private deal. There are only 83.2M shares that aren’t owned by the Buzzi family. This means the year-end net cash of 1.8B EUR by 2025 as well as adding some leverage to the balance sheet would result in the Buzzi family having the means to launch a go-private offer.

That is, however, not my base case scenario. I am just looking to establish a long position to hopefully benefit from a re-rating. Holcim ( HCMLF ) ( HCMLY ) and Heidelberg Materials ( HDELY ) ( HLBZF ) are currently trading at 6.5 and 5 times EBITDA respectively. If I would apply a multiple of 5.5 times the EBITDA of 1.2B EUR by the end of 2025, the fair enterprise value would be 6.6B EUR. Adding 1.6B EUR in net cash (which is about 12% below the consensus estimates net cash position) would then result in a fair market capitalization of 8.2B EUR which works out to 44 EUR per share. Discounting that back by 9% per year until now results in a fair value of 36-37 EUR per share versus the current share price of just under 29 EUR. This means I will likely initiate a long position in Buzzi in the next few weeks or months as I think any weakness in its share price could be a buy opportunity.

For further details see:

Buzzi: Trading At Just 4 Times EBITDA, Going-Private Candidate