DSL - BWG: Monthly Payer Global Bond CEF 12.7% Yield

Summary

- BrandywineGLOBAL - Global Income Opportunities Fund Inc is a global fixed income CEF.

- The fund has a managed distribution policy and a 12.7% dividend yield.

- The CEF runs a high leverage ratio of 42%, achieved via both preferred shares as well as Repo/TRS funding transactions.

- This vehicle displays a -13% discount to net asset value, discount which is in the middle of the average rate observed in the past decade.

- This article covers CEFs.

Thesis

BrandywineGLOBAL - Global Income Opportunities Fund Inc ( BWG ) is a fixed income CEF. As per its literature, BWG:

Offers investors a leveraged global, flexible portfolio that targets sovereign debt of developed and emerging market countries, U.S. and non-U.S. corporate debt, mortgage backed securities and currency exposure

The fund is currently overweight sovereign debt, which represents 51% of the portfolio, followed by global high yield corporate bonds at 27%. Do not interpret sovereign debt as 'AAA' rated U.S. Treasuries, but rather holdings in local currency government bonds from Brazil, Mexico and India. The fund hedges most of the foreign exchange risk, but has the flexibility to run currency exposures.

The CEF runs a high leverage figure of 42%, achieved via both Repo/TRSs and preferred shares. The high leverage ratio amplifies returns both on the upside as well as on the downside. The main risk factor for the fund is represented by global rates, followed by credit spreads. With rates higher across the globe in 2022 the fund lost -21%. The U.S. dollar (as measured by DXY), was also up significantly last year, but the fund hedged most of its exposure.

Historically the fund's performance follows the global interest rate cycle, and we would not characterize this name as a true buy-and-hold vehicle. After a deeply negative 2022 the fund will experience a much brighter 2023. We feel global interest rates are topping out in our opinion, with inflation starting to subside. This will translate into bond prices firming up and starting to gain traction as the year progresses. Credit spreads are going to be a drag, with another bout of risk-off still expected from our end.

Analytics

AUM: $0.14 billion.

Sharpe Ratio: -0.25 (5Y).

Std. Deviation: 12 (5Y).

Yield: 12.7%.

Premium/Discount to NAV: -13%.

Z-Stat: -0.5.

Leverage Ratio: 42%

Holdings

The fund is overweight government/sovereign debt:

Portfolio (Fund Fact Sheet)

Please note that the "Government" bucket mainly contains international sovereign debt in local currency, debt which is not rated 'AAA' by the major U.S. Rating Agencies:

Sovereign Bonds (Annual Report)

We can see this credit risk even better from the credit rating parsing table:

Ratings (Fund Fact Sheet)

Most of the underlying collateral is rated 'BBB' and 'BB', which shows us the fund taking a significant amount of credit risk, mitigated in part by the sovereign guarantee from the 'government' bucket.

The fund is truly a global bond fund, with most of the exposures sitting in EM jurisdictions:

Country Segmentation (Fund Fact Sheet)

The fund purchases many slices of its underlying holdings in the local currency:

Currency Exposure (Fund Fact Sheet)

The CEF does hedge many of the FX exposures though, but has a flexible mandate in terms of running currency exposure:

Fx Hedges (Annual Report)

Performance

The CEF is down during the past year on the back of higher interest rates:

{kind=link}

We can see the fund having a performance largely in line with the much better known DoubleLine Income Solutions Fund ( DSL ). Higher rates and wider credit spreads have negatively impacted all global funds.

On a 5-year timeframe the performance chart is fairly similar, but with VGI underperforming:

{kind=link}

BWG and DSL have a similar total return profile, while VGI lags significantly.

Premium/Discount to NAV

The fund has generally traded at deep discounts in the past decade:

{kind=link}

We can see from the above table, courtesy of Morningstar, that BWG usually trades at a -12% discount to net asset value. Outside a brief period in 2012, the vehicle has always traded at a discount to NAV. We expect this to persist.

Distribution

The fund has adopted a managed distribution policy:

The Fund has adopted a managed distribution policy (the "Managed Distribution Policy"). Pursuant to this policy, the Fund intends to make regular monthly distributions to common shareholders at a fixed rate per common share, which rate may be adjusted from time to time by the Fund's Board of Directors. This policy has no impact on the Fund's investment strategy and may reduce the Fund's NAV. The Fund's manager believes the policy helps maintain the Fund's competitiveness and may benefit the Fund's market price and premium/discount to the Fund's NAV.

The fund has historically utilized a ROC figure around 30%:

{kind=link}

We can see from the above table, extracted from the fund's Section 19.a, that for the fiscal year ending in October 2022, the CEF utilized a 33% ROC percentage. There seems to be some cash-flow mismatching occurring, as well as an increase in overall holdings yields, because the latest fund report has a 0% ROC figure:

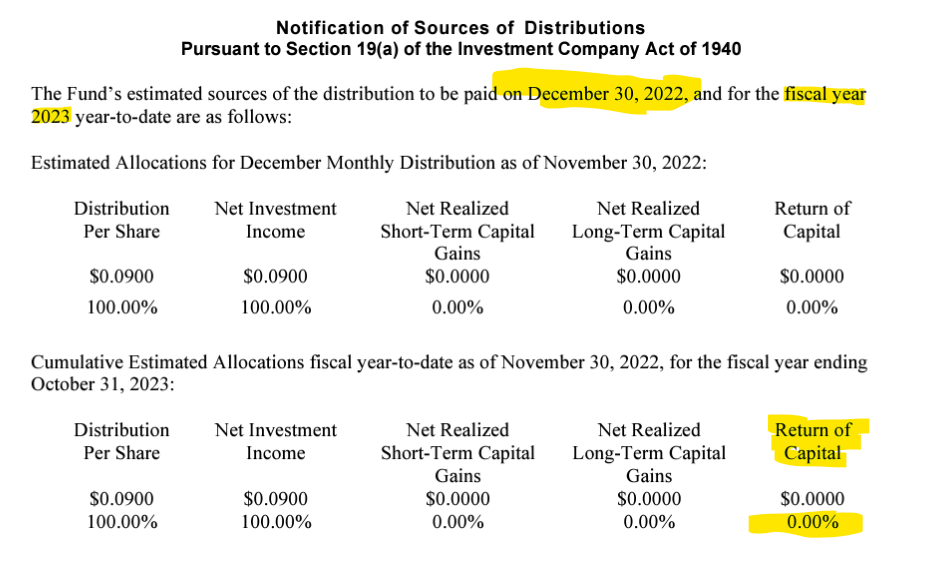

{kind=link}

Think of this CEF as a true yielder in the 8% to 9% range, with the rest made up of ROC. As the 2023 fiscal year progresses we are going to see the ROC figure for the fiscal year increase in the fund's Section 19.a notices.

Conclusion

BWG is a global bond closed end fund. The vehicle runs a high leverage ratio of 42%, achieved via both preferred shares as well as Repo/TRS funding transactions. The fund is overweight government/sovereign debt (51% of the portfolio) in the form of local currency paper. The CEF hedges most of the FX exposure, although it has a flexible mandate to run currency risk. The second largest exposure in the fund is constituted by global high yield bonds, at 27% of the portfolio. The CEF has a -13% discount to NAV which we expect to persist. The vehicle has almost always traded at a discount in the past decade, with the average around the current level. The fund's managed 12.7% yield is not fully covered, with our estimation of current ROC figure at around 20% to 30%. The vehicle has uneven cash-flow timing, making ROC distributions uneven month to month. After a very tough 2022, BWG will see a much brighter 2023 with global rates peaking.

For further details see:

BWG: Monthly Payer Global Bond CEF, 12.7% Yield