BWG - BWG: This International Bond Fund Looks Good If You Can Stomach The Volatility

2023-10-19 08:13:25 ET

Summary

- BrandywineGLOBAL - Global Income Opportunities Fund offers a high level of income and international exposure with a 13.22% yield.

- The fund has underperformed certain bond indexes, but its large distribution offsets price declines and provides a respectable overall return.

- The fund's use of leverage and high-risk strategy may deter some investors, but its attractive valuation makes it worth considering.

- The fund did manage to fully cover its 13.22% yield in the first half of its fiscal year, but it had to rely on unrealized gains to do it.

- The fund has an enormous discount on net asset value.

BrandywineGLOBAL - Global Income Opportunities Fund ( BWG ) is a globally oriented fixed-income closed-end fund that investors can use to obtain a very high level of income from the assets in their portfolios while gaining international exposure. As is the case with many global fixed-income funds, this one has a remarkably high yield, with shares boasting a 13.22% yield at the current price. That is obviously one of the highest yields available in the market today, but unfortunately, that yield is also at a level where there is some concern over its stability. After all, for most of the past decade, assets only ended up with a double-digit yield when the market was expecting a distribution cut. However, that is less applicable today than it was a few years ago due to the simple fact that the yields on everything are much higher than they used to be. In addition, funds that invest in foreign assets frequently have higher yields than funds that invest only in the United States simply because there are many foreign countries in which interest rates are a lot higher than they are in the domestic market.

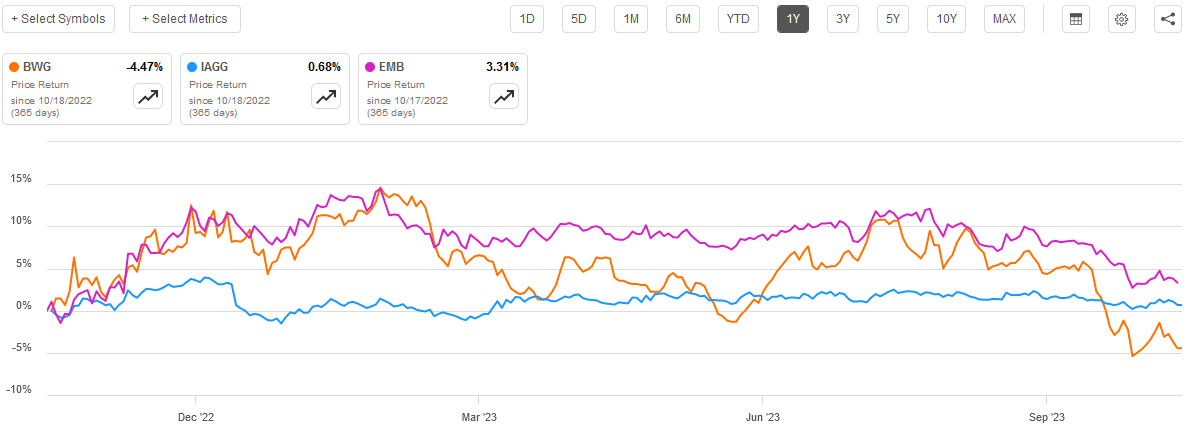

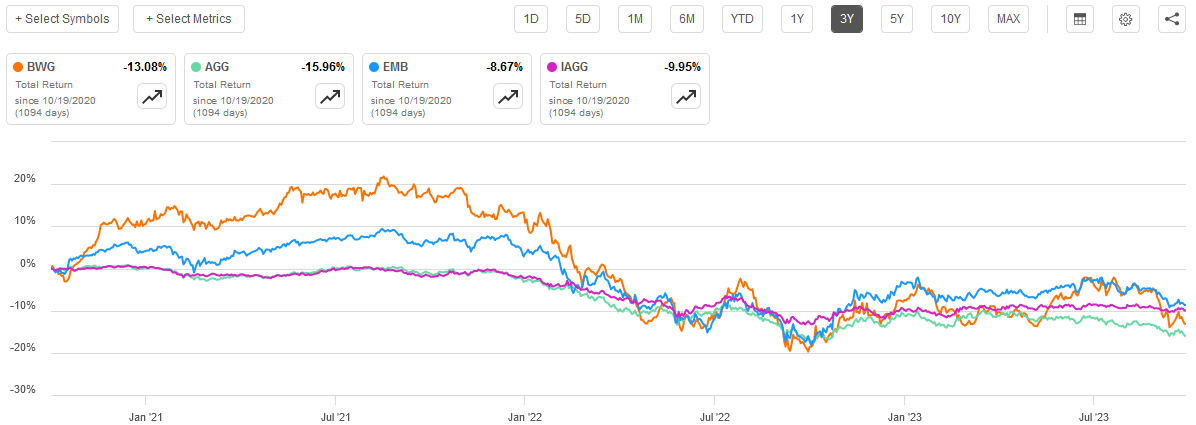

Unfortunately, the recent performance of the BrandywineGLOBAL - Global Income Opportunities Fund has been quite disappointing. As we can see here, the fund has underperformed both the iShares Core International Aggregate Bond ETF ( IAGG ) as well as the iShares J.P. Morgan USD Emerging Markets Bond ETF ( EMB ):

{kind=link}

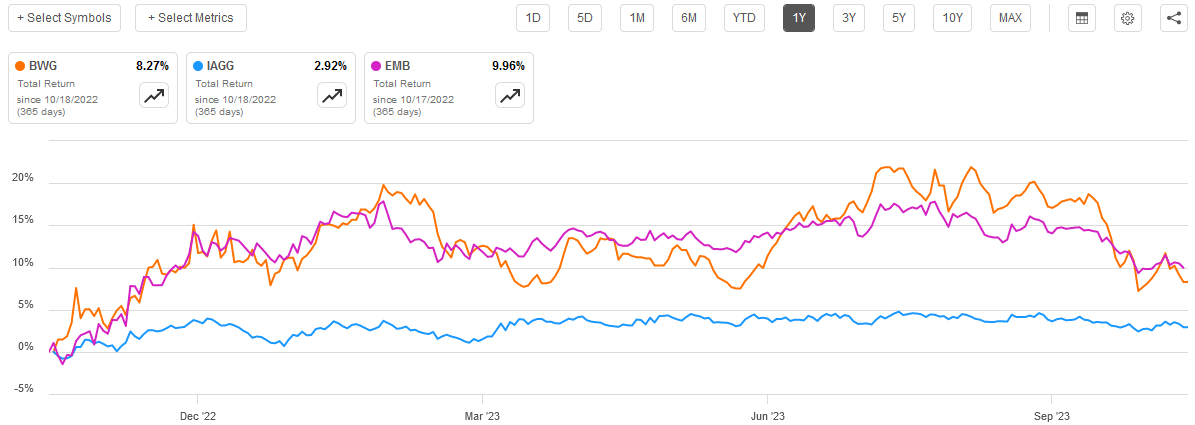

This is quite disappointing, especially since this fund underperformed the emerging markets bond index. After all, this fund does invest fairly significantly in emerging market debt securities. However, the portfolio contains a number of other things too, so this is not exclusively an emerging markets fund. Fortunately, it does a lot better when we consider the impact that the fund’s incredibly large distribution has on its overall return. We can see that not only do the distributions completely offset the fund’s price decline, but they also give it a total return that beats the international bond index by quite a lot:

{kind=link}

This certainly helps endear the fund to investors, but the price decline over the period might still scare some people off. Overall, though, the fund’s performance has been pretty respectable.

Naturally, the big question on everyone’s mind is whether or not it makes sense to buy the fund today. Let us investigate this.

About The Fund

According to the fund’s webpage , BrandywineGLOBAL - Global Income Opportunities Fund has the primary objective of providing its investors with a very high level of current income. This is not surprising considering that this is a fixed-income fund, as already mentioned. As we have discussed numerous times before, fixed-income securities are primarily an income vehicle since they have no inherent link to the growth and prosperity of the issuing company. In the case of bonds, these securities also have no net capital gains over their lifetimes, as bonds are both purchased and mature at their face value.

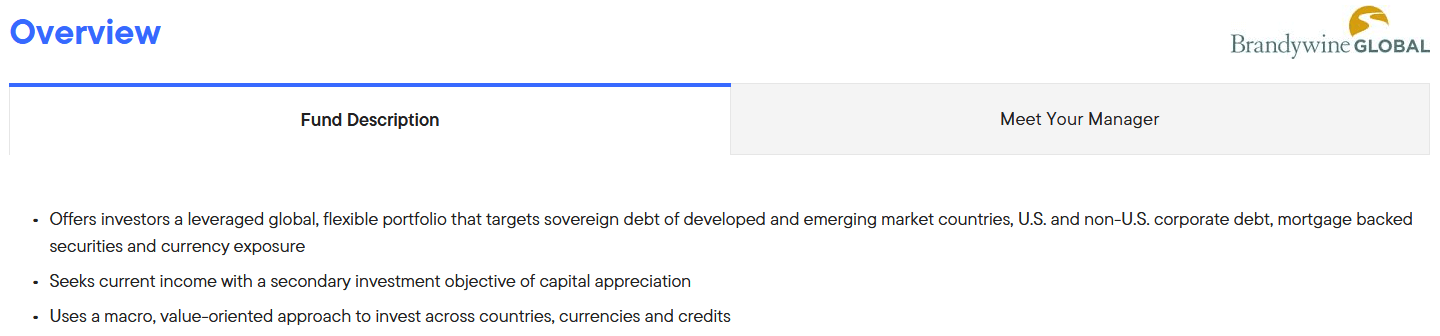

This fund employs a somewhat different strategy in order to achieve its objective than many other fixed-income funds, however. We can see this here:

{kind=link}

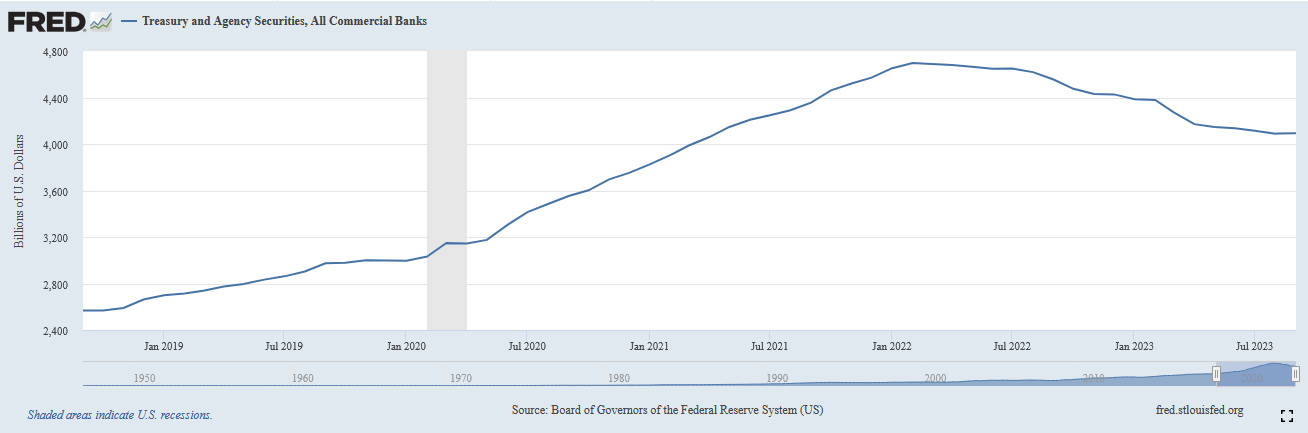

As the description states, the fund might invest in both domestic and foreign corporate debt, foreign sovereign debt of both developed and emerging market countries, and even some mortgage-backed securities. In fact, the only thing that is not specifically mentioned here is U.S. Treasury securities, which the fund will normally have extremely limited exposure to. This is actually a good thing for American investors who might hold other bond funds (or non-Americans who might have an American bond fund in their portfolios). This is because the United States federal government is the largest issuer of bonds in the nation, and naturally just about every American bond fund is going to have significant exposure to them. As we have discussed in numerous previous articles, the finances of the American federal government are not especially good at the moment, so it is only natural that bond investors will want to reduce their exposure to these securities. After all, as we can see here, even American commercial banks have begun to reduce their exposure to U.S. Treasuries:

{kind=link}

As this fund does not invest in U.S. Treasury securities, including it in a portfolio that contains other funds that do invest in these debt offerings will reduce your overall exposure to American Federal Government debt.

However, with that said, a sizable percentage of the issuers whose securities are represented in the fund’s portfolio are American entities. We can see that here:

Franklin Templeton

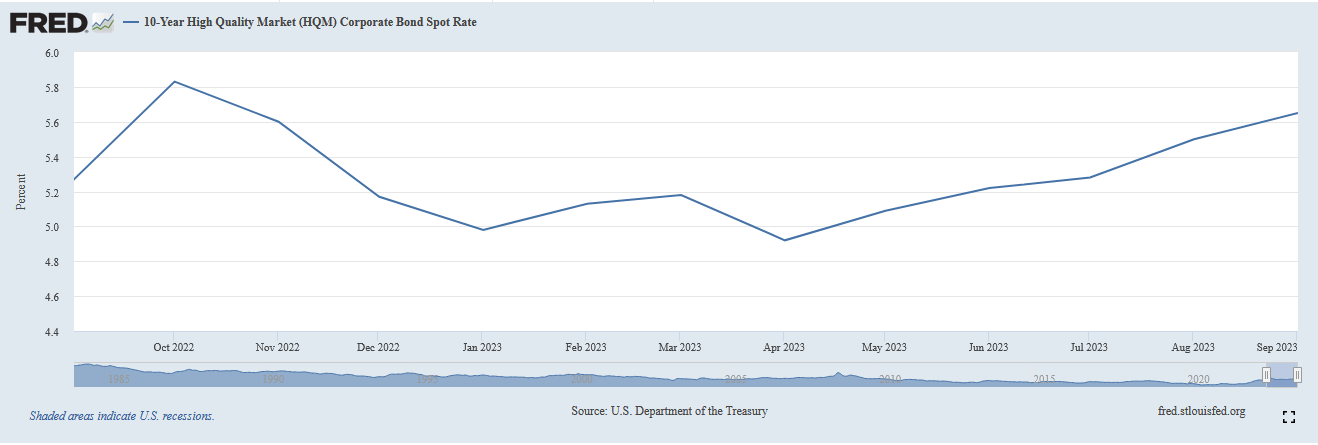

For the most part, these are American corporate bonds, not agency securities or other things that are implicitly or explicitly backed by the U.S. government. As such, they do carry some default risk, but they also have higher yields than U.S. Treasuries. As of the time of writing, the ten-year U.S. Treasury is at 4.906% but the ten-year high-quality corporate spot index is at 5.65%:

{kind=link}

The ten-year high-quality corporate spot index tracks the average yield of a portfolio consisting of a mixture of AAA, AA, and A-rated bonds with a maturity date ten years into the future. Thus, it is generally considered to be a reasonably good proxy to see where corporates are relative to U.S. Treasuries. The overall point here though is that the assets held by this fund are going to have significantly higher yields than federal government bonds in order to compensate investors for the fact that there is a risk of default.

In numerous articles about fixed-income closed-end funds, we discussed where interest rates are heading as part of our analysis of the fund. After all, interest rates are one of the most important factors for bond investors due to the simple fact that bond prices are inversely correlated with interest rates. However, the interesting thing about this fund is that there is a mixture of countries here, each with its own interest rate regime. For example, the European Union has not increased its benchmark interest rate to nearly the same level as the United States over the past two years. As of right now, the main refinancing rate, which is the equivalent of the federal funds rate for banks in the European Union, is at 4.50% versus a 5.33% effective federal funds rate. The Bank of Japan has not increased its benchmark rate at all since 2016. There are bonds from issuers in the European Union as well as bonds from Japanese entities contained in this fund. Those bonds will react based on the interest rate policies of their respective central banks, not the Federal Reserve. With that said, just under half of the securities held by this fund are from American entities and so the interest rate policies of the Federal Reserve are more important than the policies of any other individual central bank when evaluating the performance of this fund. This may be why this fund’s performance appears to have more correlation with the Bloomberg U.S. Aggregate Bond Index ( AGG ) than it does with any other bond index, even though it is hardly a perfect correlation:

{kind=link}

Thus, it does not appear that this fund will allow investors to fully escape from the monetary policies of the Federal Reserve, but it will probably do a better job than a pure domestic bond fund.

As mentioned in the introduction, emerging markets have a tendency to have significantly higher interest rates than developed markets. This is in spite of the fact that these countries typically have much better government finances. For example, Columbia, whose issuers represent the largest proportion of the fund’s assets other than the United States, currently has the following:

| Government Debt-to-GDP |

| 63.6% |

| Budget Deficit |

| 4.3% of GDP |

The United States has a current budget deficit of 5.8% of gross domestic product, so obviously its numbers are far worse than Columbia’s. The market generally allows the United States to borrow at a lower rate, though. The single largest holding of this fund is Columbian government bonds with a 7.25% coupon. It has certainly been quite a long time since U.S. Treasuries traded with a yield anywhere close to 7.25%!

Admittedly, some emerging market nations have a history of government instability, regime changes, coups, and similar things so there might be a certain amount of risk involved to obtain those yields. We can still clearly see though that emerging market debt securities in general could be a decent way to obtain a high level of current income considering that their government finances are not necessarily all that bad.

Leverage

One of the defining characteristics of closed-end funds such as the BrandywineGLOBAL - Global Income Opportunities Fund is that these assets employ leverage as a means of boosting their effective returns well beyond that of any of the underlying assets in the portfolio. I explained how this works in various previous articles. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase both domestic and foreign bonds, including bonds issued by entities located in emerging markets. As long as the yield that the fund receives from the purchased assets is higher than the interest rate that it has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged fund. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the BrandywineGLOBAL - Global Income Opportunities Fund has leveraged assets comprising 43.53% of its portfolio. This is quite a high level of leverage. In fact, it is one of the highest levels that I have ever seen a closed-end fund possess. As such, the fund is almost certainly going to be much more volatile than most global bond funds, and its downside risks are amplified in a worst-case scenario. While there may be some investors who are comfortable with a high-risk, high-reward strategy like this, that is probably not the profile of the typical income-seeking investor.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BrandywineGLOBAL - Global Income Opportunities Fund is to provide its investors with a very high level of current income. This is not surprising considering that the fund’s basic strategy is to purchase bonds from all over the world and then borrow money to buy even more bonds, taking advantage of the difference between the borrowing rate and the yield of the bonds. Many of the bonds, although certainly not all of them, come from nations in which interest rates are much higher than they are in the developed world. As the fund’s leverage amplifies the effective yield, we can assume that the actual amount of income that the fund brings in is a fairly high percentage relative to the net asset value of the portfolio. The fund collects all of these payments and then distributes them to its investors on a regular basis, net of the fund’s own expenses. It can probably be expected that this will give the fund’s shares a very high yield.

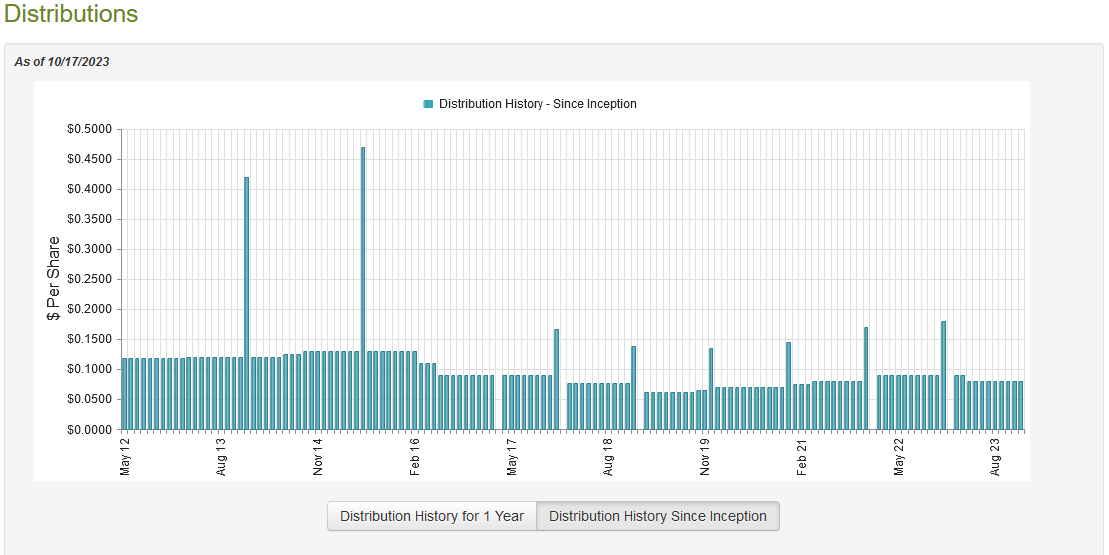

This is certainly the case, as the BrandywineGLOBAL - Global Income Opportunities Fund pays a monthly distribution of $0.08 per share ($0.96 per share annually), which gives the fund a very impressive 13.22% yield at the current price. The fund has unfortunately not been especially consistent with respect to its distribution over time. In fact, as we can see, the distribution has varied to a great degree since the fund’s inception:

{kind=link}

This is almost certainly going to prove to be a turn-off for any investor who is seeking a safe and stable source of income to use to pay their bills or finance lifestyle expenses. However, it is not especially surprising for a fixed-income fund considering that the assets held by these funds are incredibly sensitive to changes in interest rates. This could be especially true with this fund as it has exposure to a number of different countries, currencies, and central bank policies. We would normally expect a fund like this to vary its distribution over time to correspond to the overall performance of its investment portfolio. After all, we do not want the fund to pay out more than it manages to earn in investment profits since that would be destructive to the fund’s assets and prove to be unsustainable in the long term. Let us investigate the fund to figure out exactly what is going on here.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. This was certainly an interesting period for the United States, as investors were generally optimistic that the Federal Reserve might quickly pivot on its monetary policy and begin easing, as it has done for most of the past decade. As such, American stocks and bonds generally rallied, and yields fell. The same thing actually happened in emerging market bonds and the international bond market, although the degree of the rally varied from country to country. The fund may have been able to take advantage of this and generate some capital gains by selling appreciated assets.

During the six-month period, the BrandywineGLOBAL - Global Income Opportunities Fund received $10,345,418 in interest and $129,169 in dividends from the assets in its portfolio. After we subtract out the money that the fund had to pay in foreign withholding taxes, we see that it had a total investment income of $10,386,466 during the period. The fund paid its expenses out of this amount, which left it with $6,656,630 available for shareholders. Unfortunately, this was not enough to cover the $8,731,755 that the fund paid out in distributions during the period. At first glance, this is certainly going to be concerning as we normally like fixed-income funds to be able to completely cover their distributions out of net investment income.

However, there are other methods through which the fund can obtain the money that it needs to cover the distribution. For example, it might have been able to sell some appreciated securities into a generally friendly market in order to realize some capital gains. The fund had mixed results here, as it reported net realized losses of $14,937,278 but these were offset by $20.951,737 in net unrealized gains. Overall, the fund’s net assets went up by $3,939,334 over the period after accounting for all inflows and outflows. Thus, the fund technically did manage to cover its distributions during the period. However, it had to rely on unrealized gains to do that, and unrealized gains can be very easily erased by a market correction. Thus, it may have lost some of that money by now and its finances may not actually be as strong as they appear. We will have to wait a few months for the fund to release its annual report in order to know for certain.

Valuation

As of October 17, 2023 (the most recent date for which data is currently available), the BrandywineGLOBAL - Global Income Opportunities Fund has a net asset value of $8.55 per share but the shares currently trade for $7.16 each. This gives the fund’s shares a 16.26% discount on net asset value at the current price. That is an enormous discount that is substantially better than the 14.27% discount that the shares have had on average over the past month. Thus, the current price looks like a good entry point for the fund.

Conclusion

In conclusion, the BrandywineGLOBAL - Global Income Opportunities Fund is one of the few closed-end bond funds available that hold significant positions outside of the United States. This could be quite useful for investors who want to diversify their assets away from the United States. The fund’s incredibly high yield adds to its appeal, especially because it mostly managed to cover it during the most recent period. The biggest downside here is the fund’s use of leverage, as the fund is highly leveraged and appears to be using a high-risk, high-reward strategy. This gives it a great deal of volatility that some investors may not want to deal with. However, it does appear to be a very good fund with an attractive valuation if you can stomach the volatility.

For further details see:

BWG: This International Bond Fund Looks Good If You Can Stomach The Volatility