BWXT - BWX Technologies: Top-Down Analysis Supports Buy

2024-01-08 07:48:42 ET

Summary

- The Industrials sector and A&D industry are recommended for investment over the next 12 months.

- The US military and defense budget is expected to provide significant investment opportunities.

- BWX Technologies is identified as a buy due to its strong position in the aerospace and defense industry and potential for growth.

Investment briefing

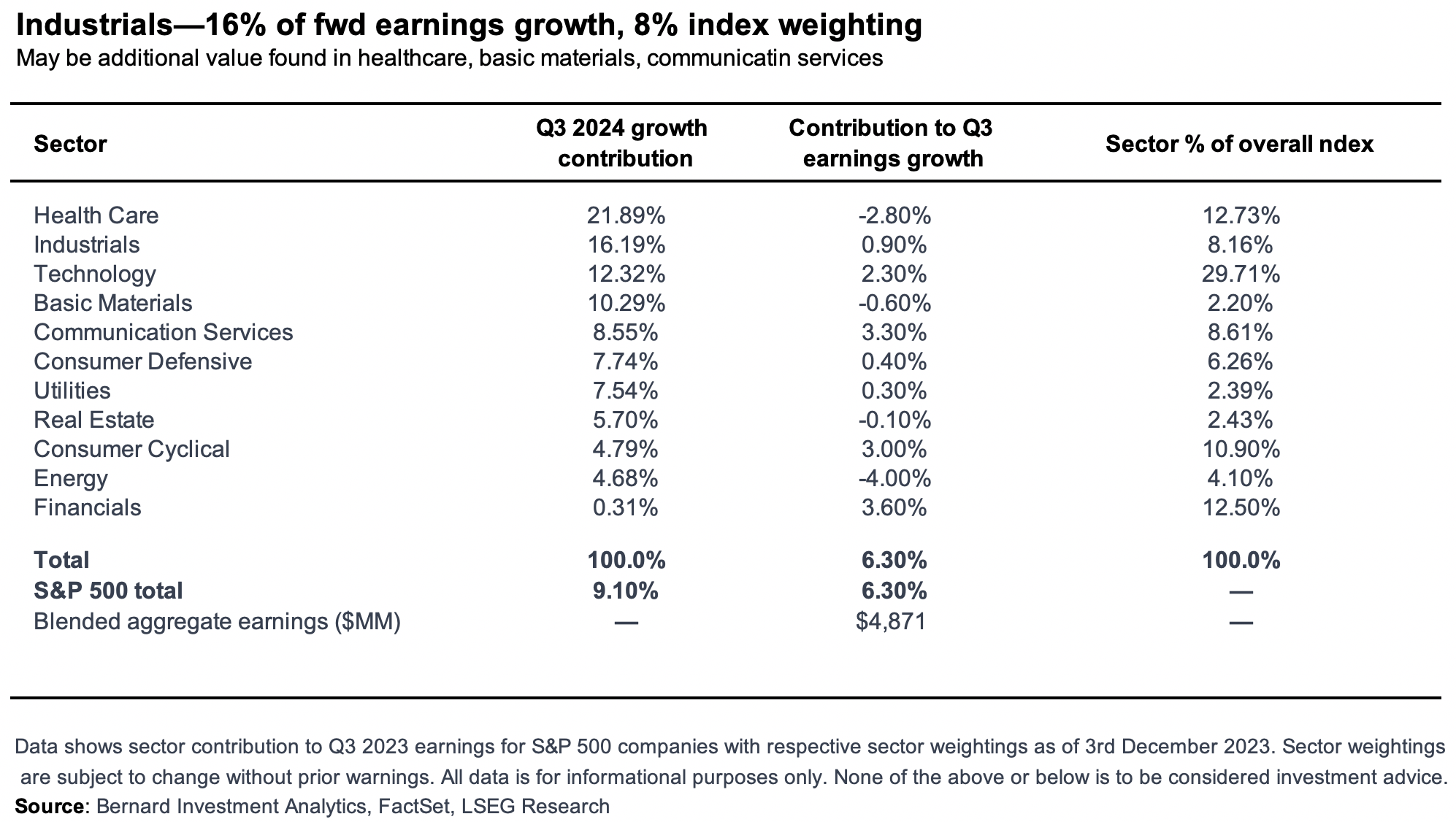

Top-down sector and security selection should be concentrated towards the industrials and basic materials sectors over the next 12 months in our opinion. Our analysis reveals that investment returns for the next 12 months in the industrials sector are bolstered by the fact that, by the end of Q3 FY'23:

(i). The industrials sector held 8.16% notional value of the market capitalization-weighted S&P 500 index (Figure 1),

(ii). At the same time, it is forecast to contribute 16.2% of the index's projected earnings growth in the coming 12 months.

On this basis, the axis of growth/value is well supported in allocating toward the industrials sector, as valuations are compressed relative to earnings growth prospects.

Figure 1.

{kind=link}

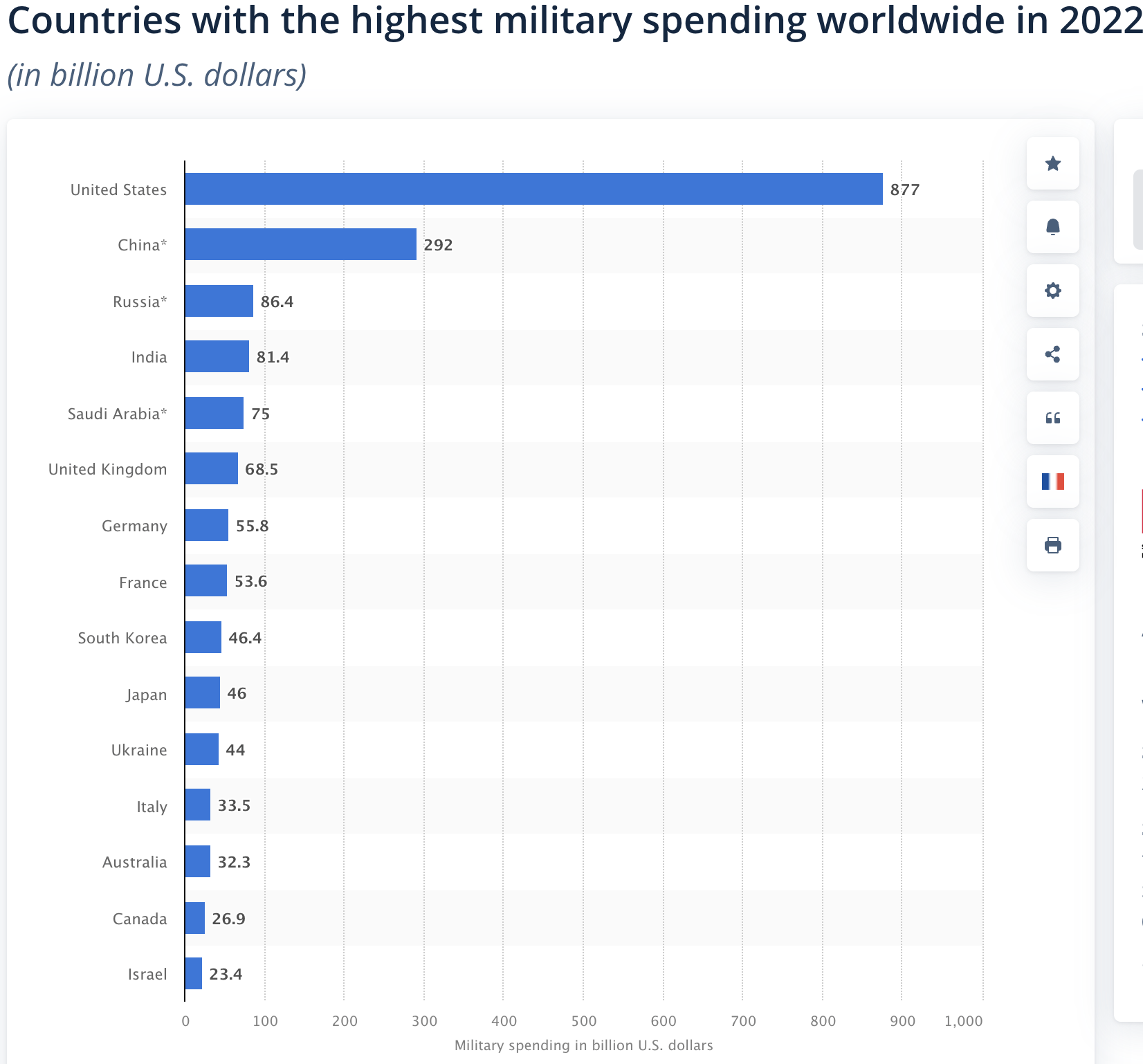

Tactical allocations within the sector cannot ignore the gargantuan U.S. military and defense budget(s) outlined since 2021, with more than $1 Trillion of investment budgeted for the industry from 2021-'24. The U.S. now has the largest military expenditure of any country by far (Figure 2) with another $886Bn passed into the legislature in December 2023. As a footnote, more than 2/3 of the U.S. House of Reps voted in favour of the bill, a positive for capital allocation in the industry.

Figure 2.

{kind=link}

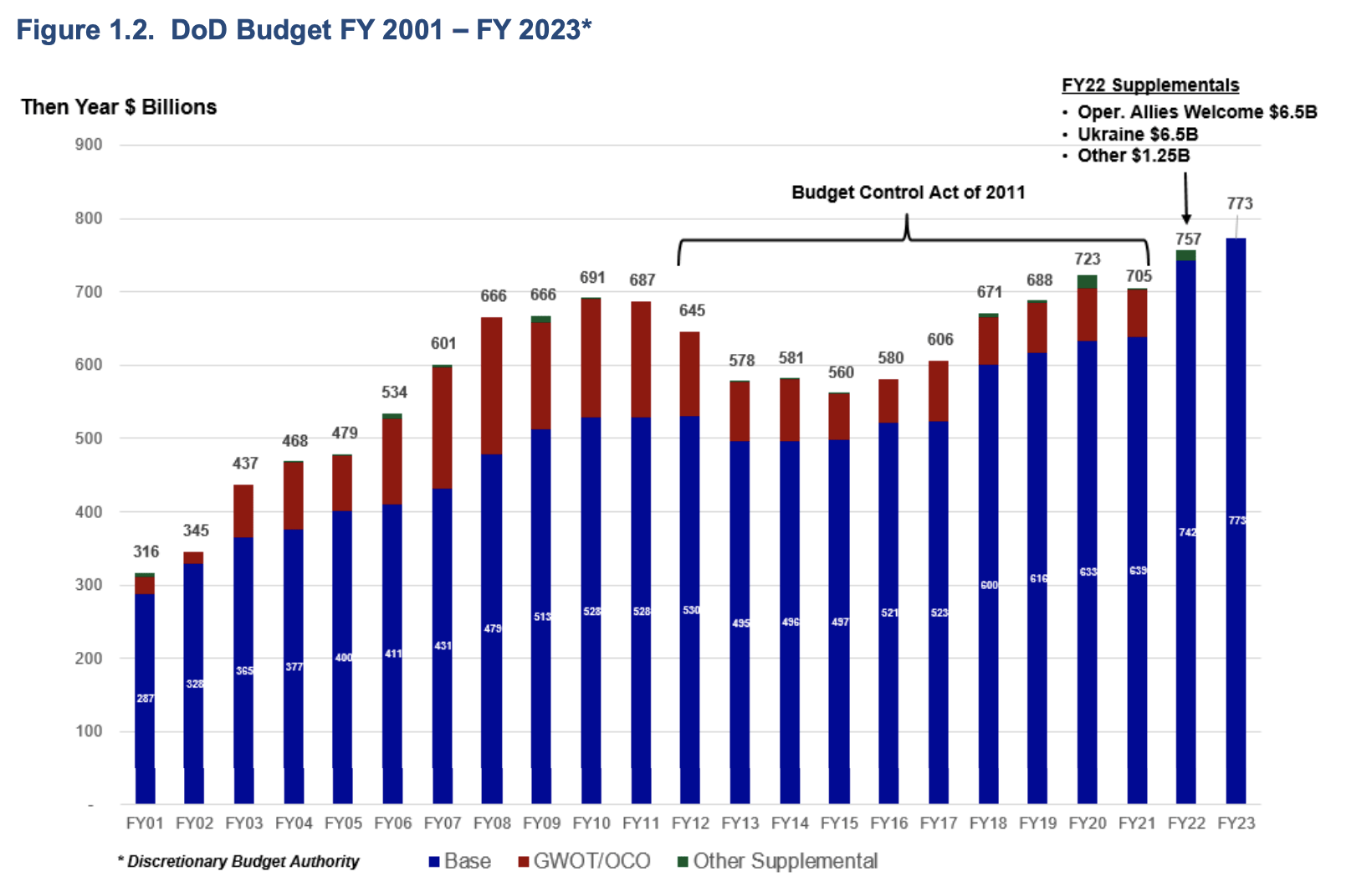

U.S. Military spending has now surpassed previous record levels seen in FY'10-'11, as illustrated by the DoD's most recent Defense Budget Overview (Figure 3). The trend of budget allocation has increased in near-linear fashion since 2014, with the annual budget increasing from lows of $560Bn in 2015 to the $886Bn just recently legislated.

Figure 3.

Source: U.S. DoD Defense Budget Overview

{kind=link}

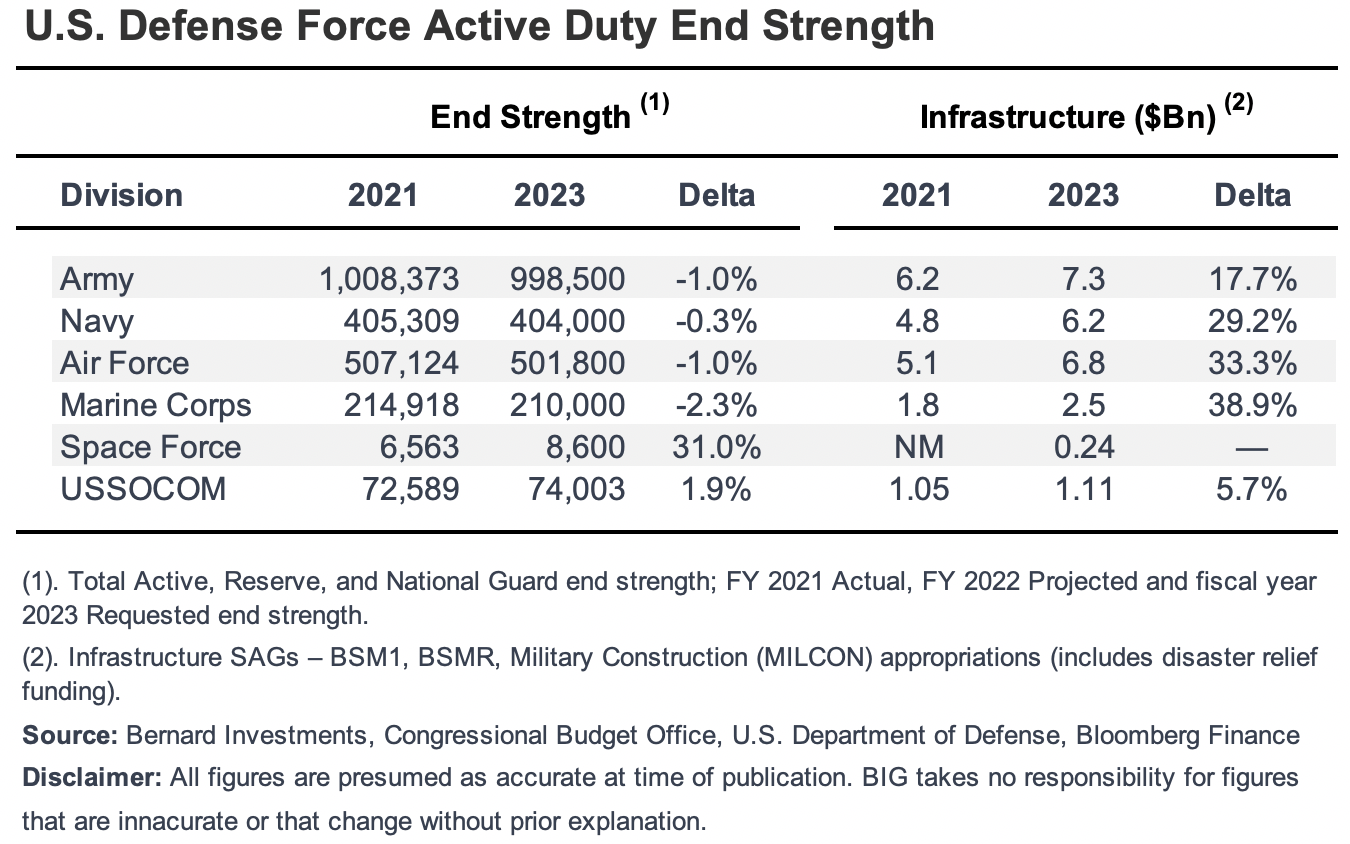

Within the budgetary outlines and forward estimates are critical data on infrastructure and active duty end strength. Figure 4 outlines the deltas in both domains since 2021. Notably, end strength has decreased across most divisions except space travel and the United States Special Operations Command ("USSOCOM"), although, the changes are statistically negligent. Still, the Navy will have grown end strength by over 15,000 personnel since 2018.

As expected, however, infrastructure assets and funding have increased double digits across the board. The majority of the uptick is observed in the Navy, Air Force and Marine Corps. This is critical information for individual security selection into the space.

Figure 4.

{kind=link}

Opportunity

BWX Technologies (BWXT) is an insulated offering that provides investors differentiated exposure to, among other growth factors, the U.S. Navy's defense budget.

My estimation is that cash will be sloshing around the defense circles for years to come, meaning capital is primed for allocation to long-standing, predictable, U.S.-domiciled aerospace and defense names.

All of the neutral or bearish reports on BWXT fail to recognize the sheer size of the budget allocation over the coming years, and just how well-primed the company is to capture this downstream.

BWXT was founded in 1867 and thus has its roots deeply embedded into American soils, employing 7,000 employees at the time of publication. It put up $590mm in Q3 FY'2023 revenues, up 13% YoY, on earnings of $0.67/share.

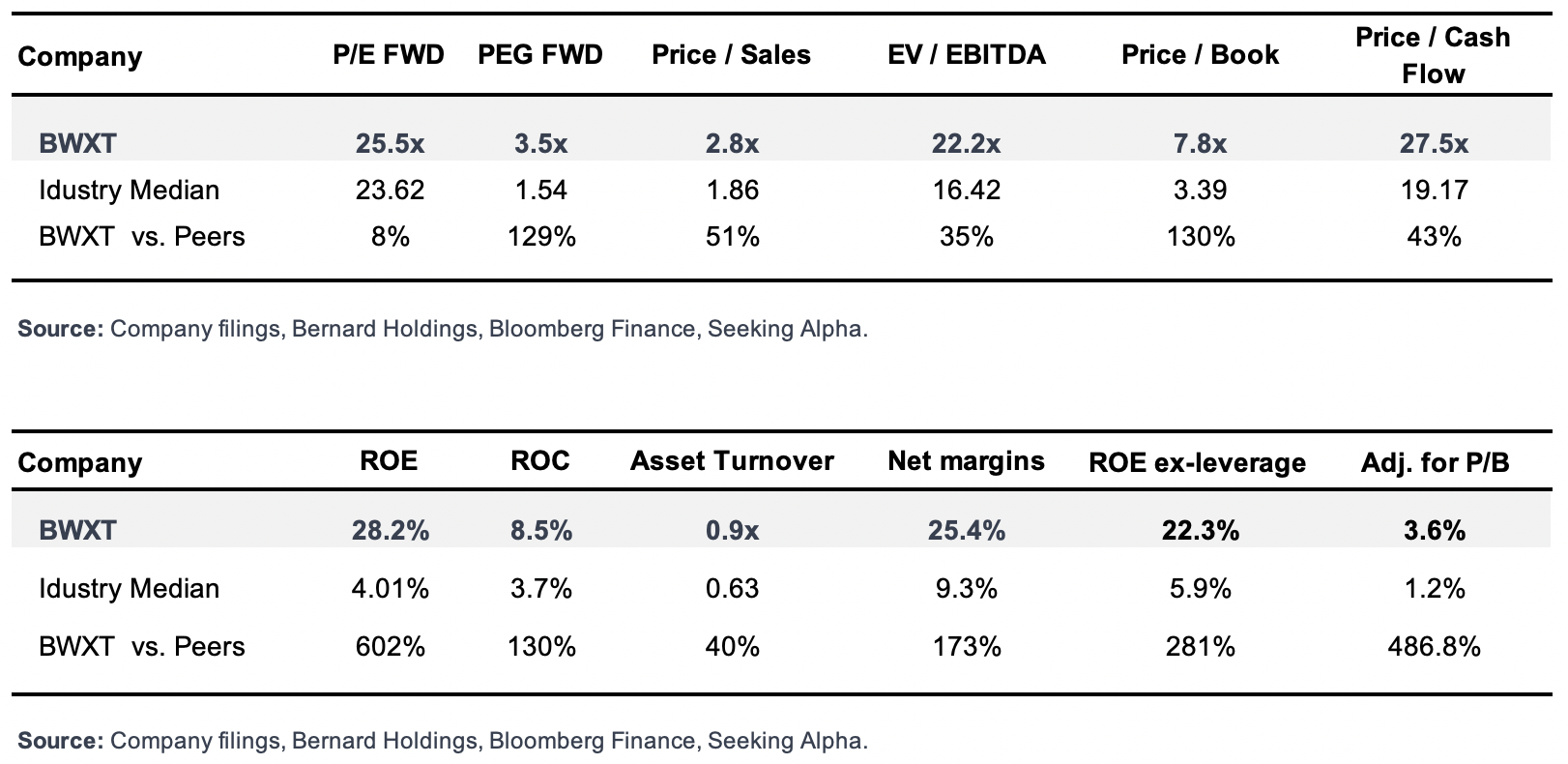

The company sells at 25x forward earnings and 7.8x book value, substantial premiums to the industry median of 23x and 3.4x respectively (Figure 5). This alone is no reason to ignore BWXT. One must critically analyze the notion of price and value here.

For instance, BWXT sells high to peers, however:

- It put up a trailing ROE of 28.2% vs. 4% for the industry,

- This is still 22.3% stripping leverage effects vs. 5% for the industry,

- Asset turnover and net margins are above average,

- Adjusted for multiple of book value, BWXT still commands a higher return on shareholder equity than the industry's 1.2%.

Clearly, there is objective support in allocating to BWXT within the aerospace and defense industry.

I am therefore initiating the company as a buy aiming for an $87/share initial price objective This report will illustrate the supportive reasons why.

Figure 5.

{kind=link}

Critical investment facts

The case for owning BWXT today is supported in the following arguments, presented below. We are advocating to buy the company with a 1-5+ year investment horizon.

- Investment returns coming 12-months

BWXT sells richly at 25x forward earnings which adjusts to 3.5x forward when factoring in growth projections. These are high absolute and relative multiples that may compress investment returns over the next 12 months. Investors-especially those with a short-term horizon-should recognize this is a potential price risk. More so returns for the coming 12 months after asset purchase are heavily impacted by starting multiples.

The company's dividend of $0.92/share (current 1.2% forward yield) should also be factored here. However, the prospect of trading higher from 25x earnings would ideally be denominator-driven, i.e. by earnings growth. For instance, presuming an efficient market:

- Current multiple: $75.06 per share / $2.94 EPS = 25.5x P/E

- FY'24 YoY Earnings growth = 5.2%

- At the same multiple: 25.5x (2.94x1.052) = $77.32/share.

Still, we are advocating to own BWXT with a >12-months horizon in mind given the statistical disadvantage under this duration presented by starting valuations.

- Investment returns coming 1-3 years

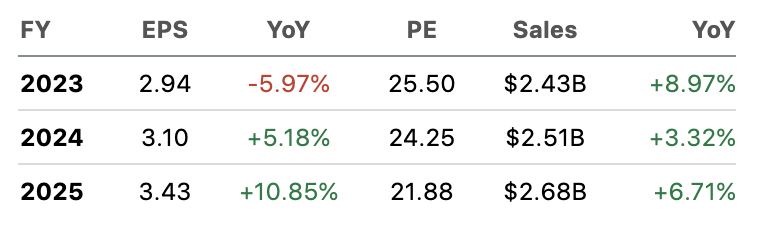

BWXT is a mature company with minuscule percentage growth prospects in terms of sales and earnings. Consensus is eyeing 6-8% sales growth out to FY'25 on 5-10% earnings growth at the same time (Figure 6).

Critically, revenue growth in the aerospace and defense industry from 2021-'22 was 3%, so BWXT clearly took market share over this time. Moving forward, the industry's growth is also poised to grow at 2.4% to 7.8% by 2028-30. It would appear BWXT is therefore primed to grow alongside or ahead of the market in the next 3 years by my estimation.

Figure 6. BWXT Consensus Sales + Earnings Projections

{kind=link}

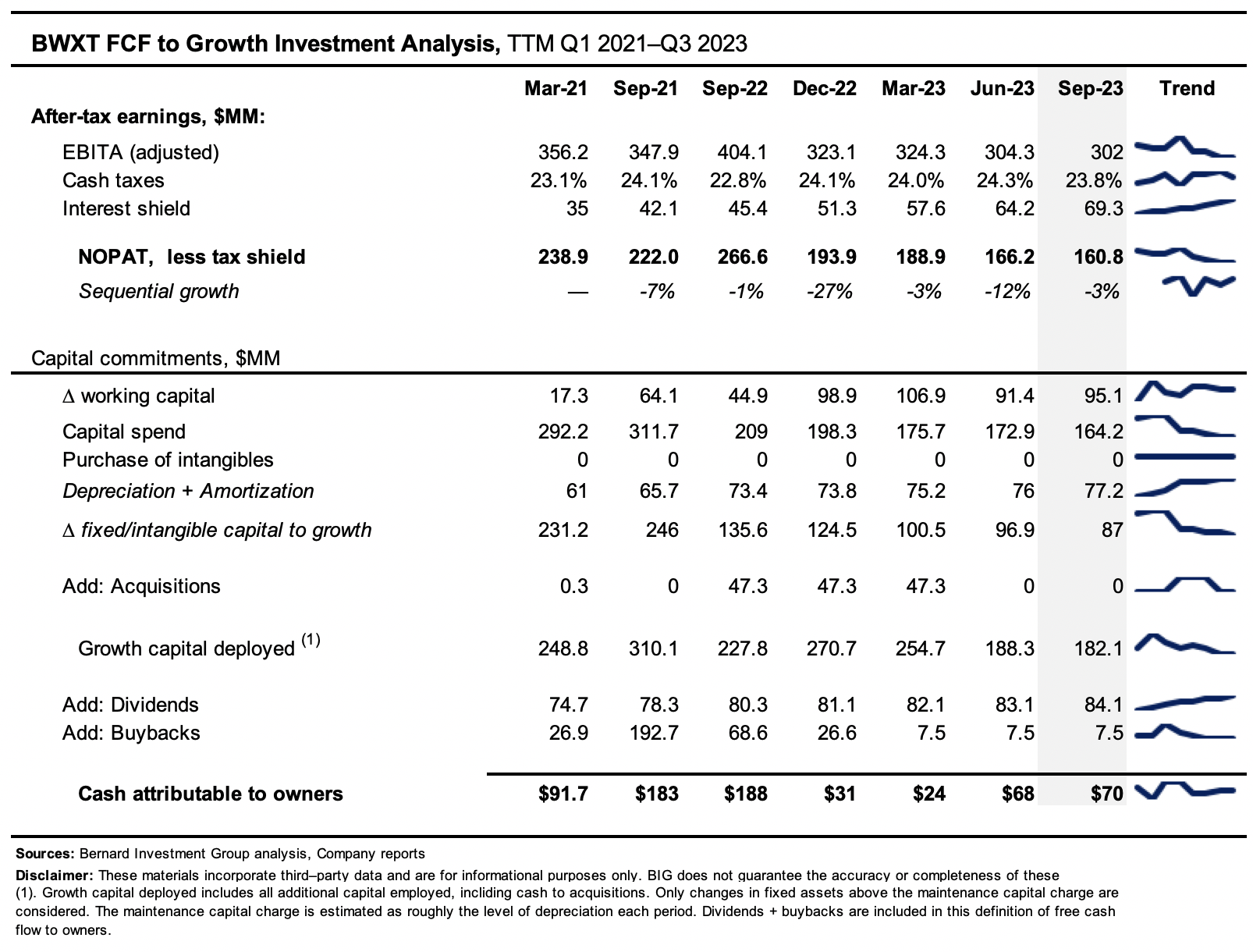

Critically, the outlook for the company's earnings quality is heavily impacted by the piles of cash BWXT has been plowing into its growth operations. As seen in Figure 6a, it has recycled $182mm-$310mm as growth capital per TTM cycle since Q1 2021. Only the capital spend above the maintenance investment is considered a 'growth' investment. Maintenance capital is approximated as the level of depreciation and amortization each period.

This level of investment in growing the business has not gone unnoticed. It aligns with 1) the increased budget, and 2) the expected growth of the industry. The market has rewarded BWXT with $32/share of additional market value off its lows in February 2022, well before the October 2023 broad market rally started. This may be due to the fact that, despite this enormous level of investment-equal to 90-140% of revenues from 2021-'23-the company has still thrown ofof piles of cash to its shareholders, notwithstanding all dividends paid up and debt interest (Figure 6a).

Consequently, investment returns for the coming 1-3 years are well supported in BWXT's projected sales + earnings outlook, alongside the extraordinary level of investment completed by the company in the previous three years.

Figure 6a.

{kind=link}

- Investment returns 3 years+

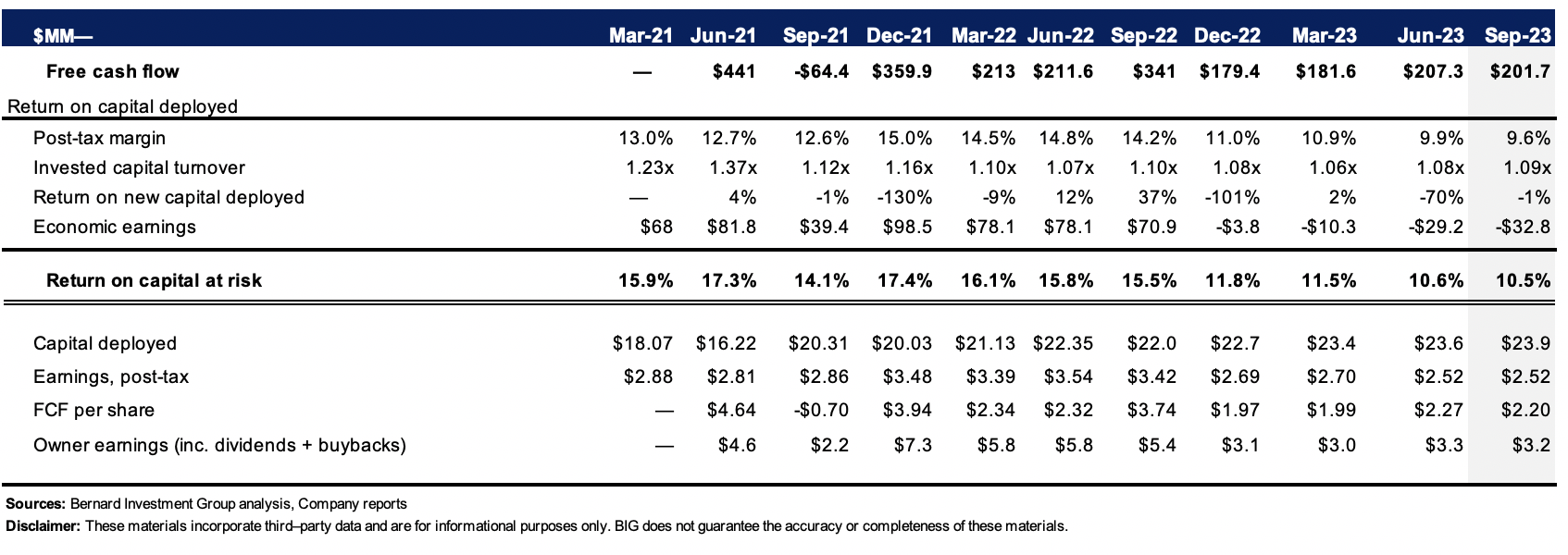

For a 3-year-plus horizon, the economic factors do the talking for BWXT's investment debate. Whilst the company's offerings are differentiated, they are capital-intensive and have large running costs to produce, thereby crimping post-tax margins. BWXT is thus a high-capital turnover business, rotating every $1 of investment to >$1 of sales. In the last 3 years, each $1 of capital invested has brought back an average of $1.10-$1.20 in sales (Figure 7), illustrating the firm's capital efficiency. This is critical in an inflationary environment when asset replacement costs are soaring for fixed capital.

As a result of this mechanism, the company has invested an additional $4/share of capital to the business, spinning off $2-$4/share in free cash flow and $3-$5 per share in owner earnings (inc. dividends and buybacks) each rolling TTM period.

Recall the discussion on the company's capital allocation from earlier, and how this may impact the business going forward. At $1.10 in sales per $1 investment, a collective $625mm of TTM investment made in the last 3 quarters could translate to $687mm in revenues long-term.

As a bedrock to position against going forward, these are the kind of economics to search for by my view. Predictable, stable earnings + cash flows that are present even with the enormous sums of reinvestment to growth. BWXT can reinvest as much capital as possible without jeopardising owner earnings, and vice versa, quite the position to be in. Further, as inflation inputs begin to normalize, my estimation is BWXT will realize growth at the margin, driving the return on existing capital back above our 12% threshold.

Consequently, looking beyond the 3-year horizon, BWXT exhibits the kind of characteristics that are defensive to drawdowns and large macroeconomic cycles. As a contribution to portfolio Sharpe's, my recommendation is to consider names such as this to reduce the equity risk budget.

Figure 7.

{kind=link}

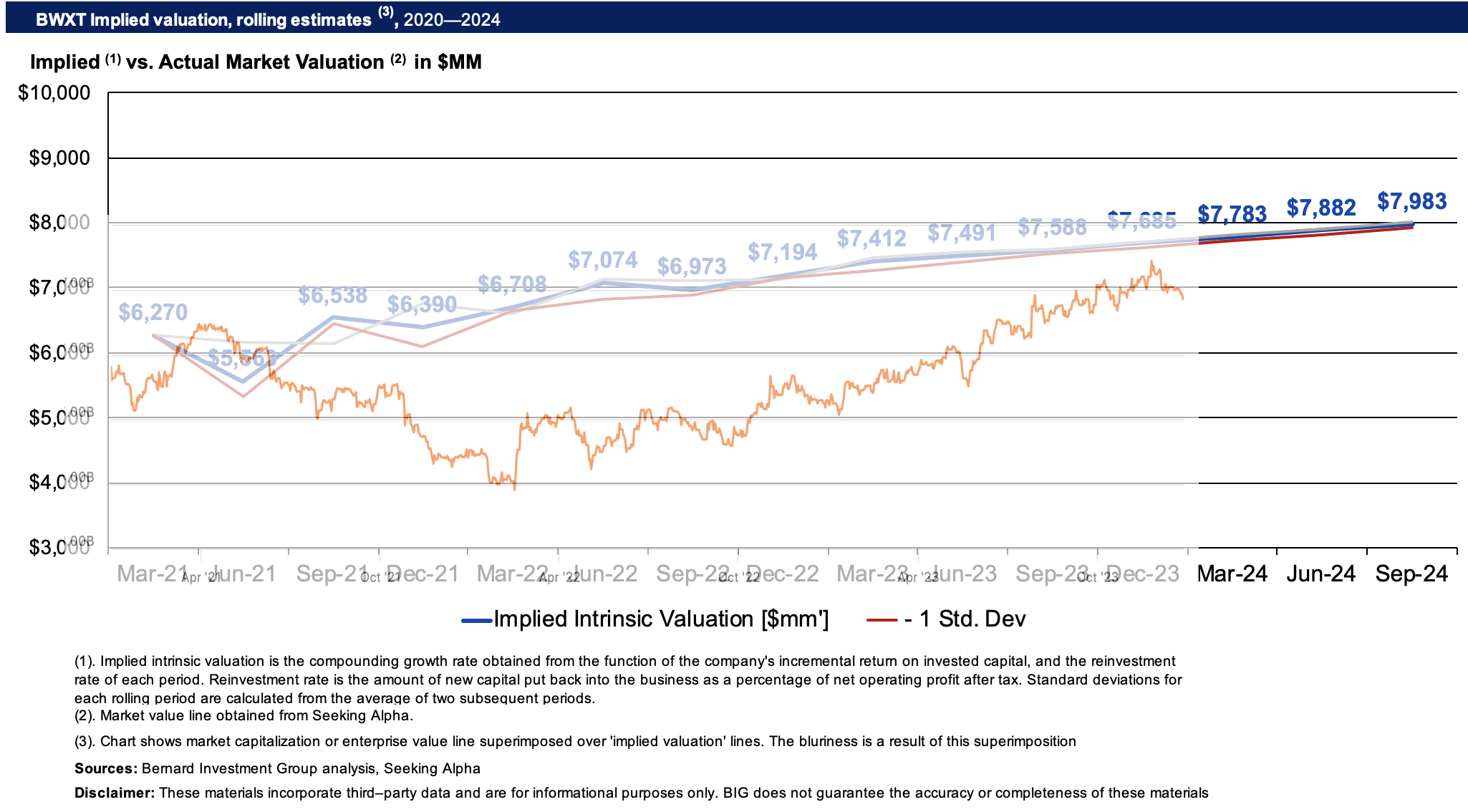

Valuation and conclusion

The stock sells at rich multiples, and this will have a bearing on the next 12 months' returns as discussed earlier. More thought than relative multiples is needed, however, as we illustrated the relative value to the industry on offer as well.

Compounding BWXT's implied intrinsic value at the function of its reinvestment rates and ROICs since 2021, we estimate the company has been selling below fair value for this duration. It has been converging to fair value over the last 12 months at least, and may push to $7.98Bn market value by Q3 '24 at the current trajectory, a 16% upside potential (presuming an efficient, rational market). This equates to $87/share or 29.6x forward earnings.

This supports a buy rating on valuation grounds as well. In that vein, my recommendation is to buy BWXT in the $75-$79s with an initial objective of $87/share or 16% return potential over the coming 3 quarters. Key risks to the thesis include:

1. Potential macro risks from Fed rates policy and/or geopolitical risks

2. The industry may suffer asymmetrical downsides given the high sums of capital being thrown around and high valuations

3. There is price risk in the next 12 months given the high relative and absolute valuations BWXT trades at too. These must be factored in.

Figure 8.

{kind=link}

For further details see:

BWX Technologies: Top-Down Analysis Supports Buy