ESLT - BWX Technologies: Upside From Here Should Be Limited

2023-03-08 13:02:24 ET

Summary

- BWX Technologies has done well from a sales perspective, but bottom line results have been under pressure.

- Even with this being the case, guidance for 2023 is encouraging, but this doesn't make the company a great prospect.

- Shares have done well, but upside is limited from here based on how shares are priced today.

Every investor has deficiencies in their investment process. One of my biggest is that I tend to underestimate the upside potential that companies have. One really good example of this can be seen by looking at BWX Technologies ( BWXT ), a business that focuses on the production of nuclear components and that also provides engineering and in-plant services for nuclear power utility customers and the government. From a purely fundamental perspective, recent performance achieved by the firm has been a bit mixed. Sales continue to climb, but bottom line results have trended a bit lower. On top of this, shares aren't exactly the cheapest on the market, though I definitely wouldn't call them expensive. Even so, the stock has moved comfortably higher in recent months, with some of that upside experienced even after I revised lower the rating that I had on the firm. With new data now out, I felt it would be a good idea to re-evaluate my prior call. Although I recognize that I was a bit too conservative in my assessment of the business, I still am comfortable with the ‘hold’ rating that I most recently assigned BWXT stock.

Great upside on mixed results

Since I initially rated BWX Technologies a ‘buy’ back in February of 2022, shares of the company have generated a return for investors of 40.5%. That compares to the 9.2% decline the S&P 500 saw over the same window of time. This would be great if it weren't for the fact that I later downgraded the stock to a ‘hold’. My most recent rating on the company was issued in September of last year. In that article , I talked about how the fundamental performance of the company had been solid leading up to that point and I discussed that the firm looked healthy. I felt as though the long-term picture for the company was also favorable, but I viewed upside potential from that point as being more limited in nature. Unfortunately, since the publication of that article, shares have seen upside of 16.7% compared to the 4.5% rise the S&P 500 saw.

{kind=link}

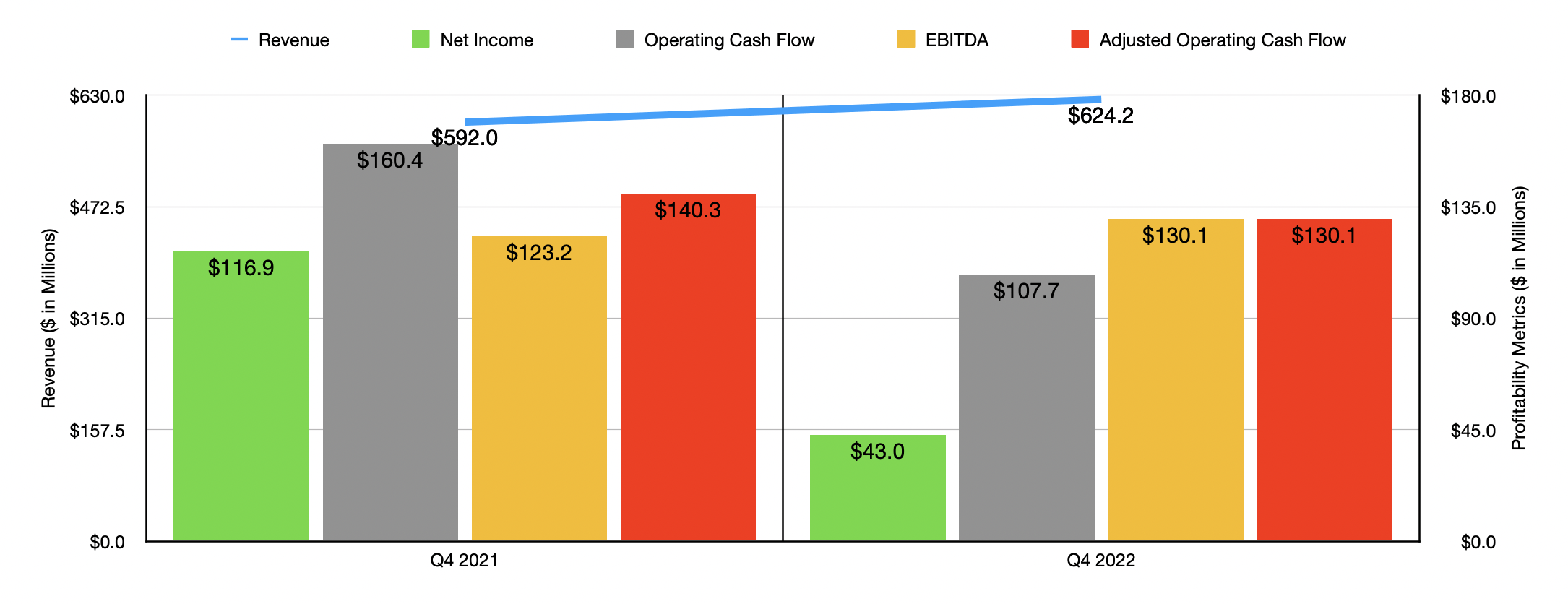

Looking at the fundamental data, I understand where I made a mistake, but I also believe that shares probably should not have risen as much as they did. To see what I mean, we need to only look at data covering the final quarter of the company's 2022 fiscal year. During that time, revenue came in at $624.2 million. That's 5.4% higher than the $592 million the company reported only one year earlier. All of that upside and more came from a roughly 8% increase in sales associated with the company's government operations. This rise, management said, was driven by higher microreactor volume, uranium processing, and an acquisition the firm made. Meanwhile, the commercial operations of the company pulled back around 6% because of lower commercial nuclear power, primarily fuel volume, that the company experienced.

Although the rise in revenue was great to see, profits for the company shrink materially. Net income dropped from $116.9 million in the final quarter of 2021 down to $43 million in the final quarter of 2022. The picture would have been better had it not been for some pension and other related losses. That impacted the company's bottom line to the tune of $35.7 million. On an adjusted basis, net profits for the company came in at $85.7 million. That was down only marginally from the $88.2 million reported one year earlier. Other profitability metrics, however, also experienced a pullback. Operating cash flow, for instance, shrank from $160.4 million in the final quarter of 2021 to $107.7 million in the final quarter of 2022. If we adjust for changes in working capital, it still would have fallen from $140.3 million to $130.1 million. In fact, the only profitability metric to improve year over year was EBITDA. It actually managed to rise from $123.2 million to $130.1 million.

{kind=link}

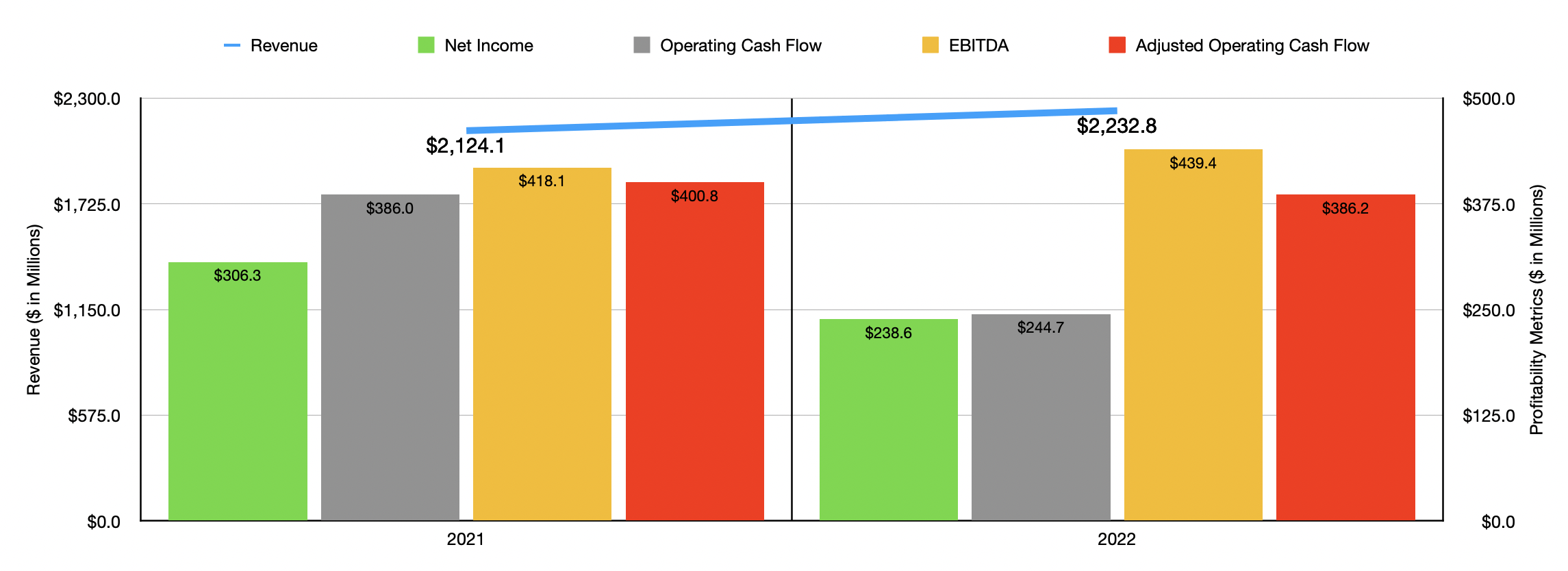

Results experienced during the final quarter of the year were similar in relation to the prior year period to what the company saw for the year as a whole. For instance, revenue still managed to increase year over year, rising from $2.12 billion to $2.23 billion. Even so, net income dropped from $306.3 million down to $238.6 million. Operating cash flow declined from $386 million down to $244.7 million, while the adjusted figure for this dipped from $400.8 million to $386.2 million. And finally, EBITDA for the company increased from $418.1 million to $439.4 million.

When it comes to the 2023 fiscal year, management expects growth to continue. Revenue, for instance, should come in at around $2.40 billion. The firm is forecasting adjusted earnings per share of between $2.80 and $3. At the midpoint, this would translate to net profits of $221.1 million. Management is also forecasting EBITDA of roughly $475 million. Based on my estimates, this would translate to adjusted operating cash flow of roughly $417.5 million. Using these figures, I was easily able to value the company.

{kind=link}

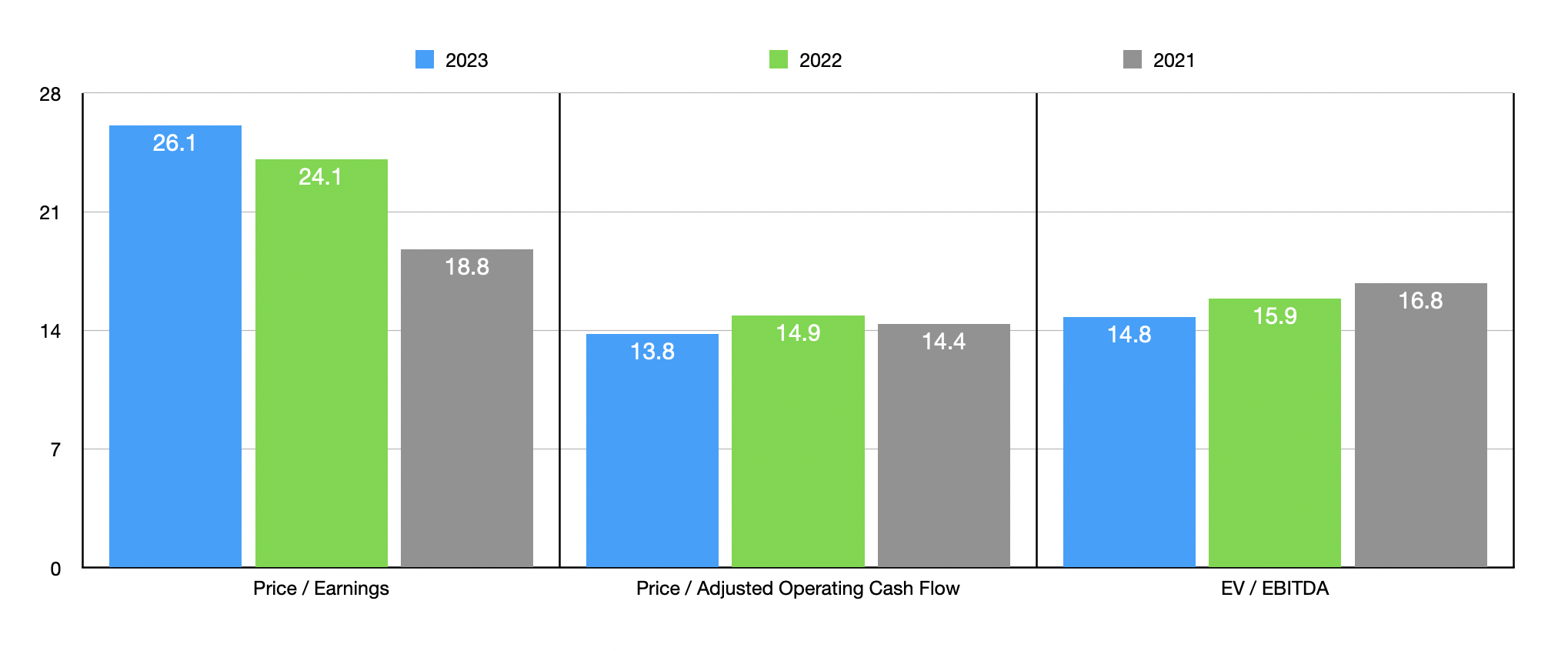

On a price-to-earnings basis, the company is trading, using the forward estimates, at a multiple of 26.1. This is up from the 24.1 reading that we get using data from 2022. The forward price to adjusted operating cash flow multiple should be 13.8. This is actually down from the 14.9 reading that we get using data from 2022. Meanwhile, the EV to EBITDA multiple should come in at 14.8. That stacks up against the 15.9 reading that we get using data from last year. For context, in the chart above, I also put valuation data for the 2021 fiscal year. As part of my analysis, I also compared the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 16.8 to a high of 51.3. Three of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range was from 10.6 to 25.6. Only one of the five firms was cheaper than our target. And finally, when it comes to the EV to EBITDA approach, we get a range of between 8.8 and 17.1. Four of the five firms were cheaper than our prospect here.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| BWX Technologies |

| 24.1 |

| 14.9 |

| 15.9 |

| Parsons Corporation ( PSN ) |

| 51.3 |

| 21.6 |

| 17.1 |

| Raytheon Technologies ( RTX ) |

| 28.4 |

| 20.6 |

| 15.1 |

| Elbit Systems ( ESLT ) |

| 16.8 |

| 25.6 |

| 8.8 |

| Curtiss-Wright Corp. ( CW ) |

| 23.2 |

| 23.2 |

| 14.2 |

| Textron ( TXT ) |

| 18.4 |

| 10.6 |

| 11.1 |

Takeaway

At present, the management team at BWX Technologies has optimistic expectations regarding the 2023 fiscal year. This, combined with continued sales increases, are likely the reason why the stock continues to rise nicely. In the long run, I have no doubt that the firm would do quite well for itself. I also don't think that shares are anywhere close to being overvalued. In retrospect, I did probably jump the gun on downgrading the company. But given where shares are priced now, I think that it's a ‘hold’ still. Though if management can come in and deliver on expectations without the price of the stock rising all that much from where it is today, I could become a bit more bullish on it again.

For further details see:

BWX Technologies: Upside From Here Should Be Limited