BWXT - BWX Technologies: Valuation Isn't Justified By Growth Opportunities

2023-05-26 12:12:40 ET

Summary

- BWXT should benefit from a robust order backlog, which should lead to revenue growth in the near term.

- In the medium to long term, BWXT should benefit from the trilateral agreement, a comprehensive 30-year shipbuilding plan, increased naval spending, and advancements in nuclear medicine.

- Based on my DCF calculation and relative valuation, I have a neutral rating on the stock.

BWX Technologies ( BWXT ) manufactures nuclear components and is a pioneer in the development of nuclear technologies, encompassing nuclear reactors, propulsion systems, fuel, especially for the Navy, and even advancements in the medical field. The company operates through two distinct reporting segments, catering to both government and commercial clients.

In its government sector, BWXT's expertise lies in designing and manufacturing top-notch equipment, renowned for its close tolerance and high-quality attributes, specifically tailored for nuclear applications. On the other hand, for commercial customers, BWXT's capabilities extend to producing a wide range of commercial nuclear steam generators, heat exchangers, pressure vessels, reactor components, and auxiliary equipment. Expanding beyond its traditional scope, BWXT has diversified into the realm of medical advancements. The company manufactures medical radioisotopes, radiopharmaceuticals, and medical devices, actively collaborating with life science and pharmaceutical companies to develop groundbreaking drugs.

Recently, BWXT reported better-than-expected first-quarter FY23 financial results. The revenue in the quarter increased by 7.1% Y/Y to $568.4 million, which is above the consensus estimate of $558.2 million. The adjusted EPS in the quarter increased by 2% Y/Y to $0.70, which is above the consensus estimate of $0.61. The demand for BWXT’s technology is high as government and commercial customers use nuclear solutions to solve problems such as clean energy, national security, and medical development.

BWXT’s Government operations

BWXT's government operations segment plays a crucial role in the company's revenue generation, accounting for approximately 81% of its total revenue. The segment's revenue grew by 6.9% year-over-year in Q1 FY23, reaching $460 million. This growth can be attributed to the increased volume of naval nuclear components and microreactors. However, the order backlog witnessed a decline of 25% year-over-year, amounting to $3.1 billion. This decrease was primarily a result of extended negotiation periods caused by inflationary pressures on labor and commodity prices. Despite this decline, I am optimistic about the future, as the government business should benefit from its healthy order backlog and new contract wins.

In April, BWXT achieved significant milestones by securing two major contract awards. The first contract, valued at $428 million, was awarded by the National Security Administration for Phase 2 of uranium conversion and purification services. The second contract, awarded to the BWXT-led joint venture H2C, was a substantial 10-year contract worth $45 billion. H2C, comprising BWXT, Amentum, and Fluor subsidiaries, secured the prestigious Hanford integrated tank disposition contract from the Department of Energy (DoE).

Moving forward, the government operations segment is poised to benefit from several favorable factors. These include the trilateral security agreement known as AUKUS , the U.S. Navy's ambitious 30-year shipbuilding plan , and a robust naval spending environment. AUKUS, formed by the United States, the United Kingdom, and Australia, aims to enhance security cooperation among the three nations. In March 2023, AUKUS partners announced plans to develop a nuclear-powered submarine capability in Australia, which will involve the procurement of Virginia-class submarines in the early 2030s, followed by the SSN-AUKUS submarine class.

The FY2024 30-year shipbuilding plan, released in April 2023, outlines three potential shipbuilding profiles: PB2024, Alternative 2, and Alternative 3. Alternative 3, assuming some real growth in shipbuilding funding, envisions the navy expanding to 356 manned ships by FY 2042 and further increasing to 367 manned ships by FY 2053. The Department of the Navy's FY 2024 President's Budget Request amounts to $255.8 billion, reflecting a 4.5% increase from the FY 2023 enacted budget. This budget will support the resourcing of the second Columbia-class submarine and two Virginia-class submarines.

With its strong position in the government sector, BWXT is well-positioned to capitalize on its robust order backlog, secure new contracts, and leverage the opportunities presented by AUKUS, the U.S. Navy's shipbuilding plan, and the steady naval spending landscape.

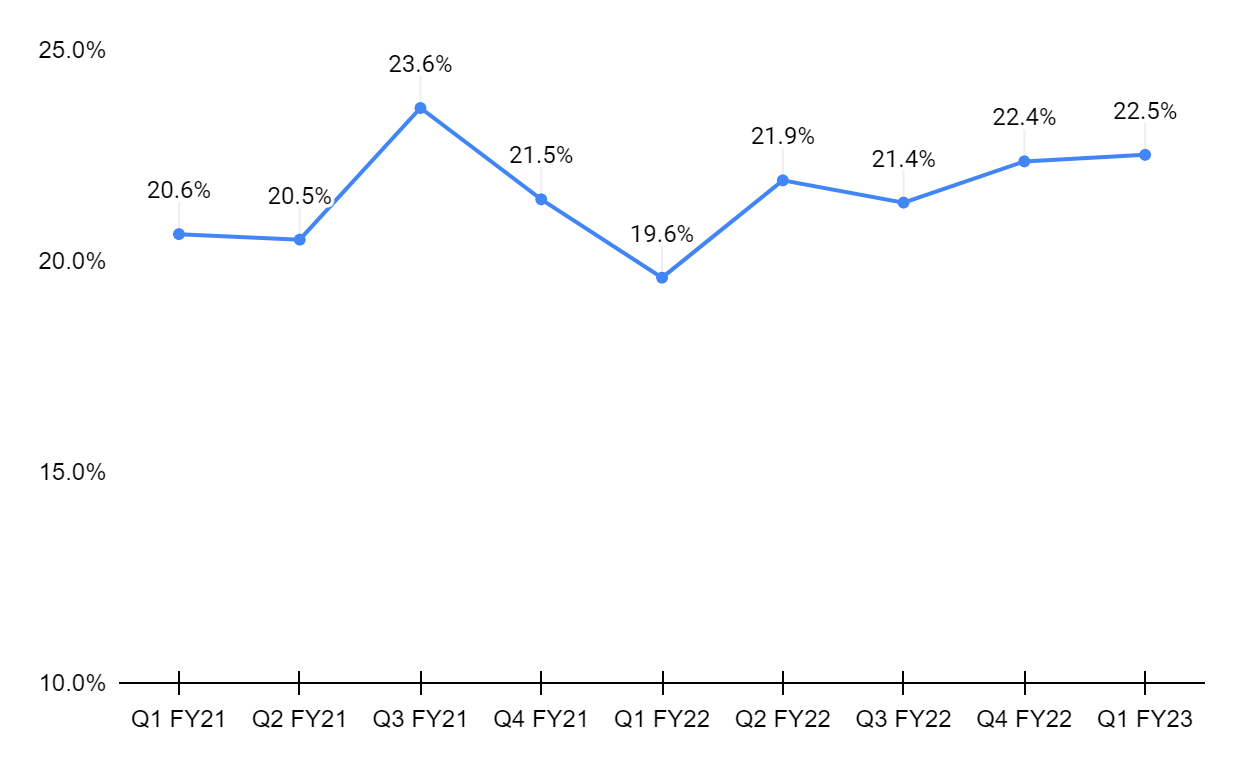

Government segment's adjusted EBITDA margins (Created by DzD Analysis by taking data from BWXT)

{kind=link}

Despite facing labor challenges, the government operations segment has demonstrated a positive trend in adjusted EBITDA margins over the past four quarters. This improvement can be attributed to two key factors: increased revenue and a more favorable project mix with higher margins.

In the near term, I believe that the segment's margin should remain relatively stable. While the higher-margin project mix continues to provide a positive impact, the margin growth should be offset by ongoing labor challenges. However, the long-term outlook is more optimistic, as the segment's margins are poised to benefit from various factors. Projects such as the Hanford tanks, which possess higher margins, should contribute positively to the segment's profitability in the long run. Additionally, BWXT's focus on streamlining operations and optimizing efficiency will further enhance margins over time.

BWXT’s Commercial operations

The segment experienced a remarkable 9% year-over-year increase in revenue, driven by higher component sales and increased field service activity in both the commercial nuclear and medicine sectors. Although the commercial business backlog witnessed an 11% year-over-year decline, amounting to $665.7 million, the segment is well-positioned for growth opportunities. The commercial operations should benefit from a healthy order backlog, growth in modular advanced reactors, emerging demand for radioisotopes, and the market's need for contract drug manufacturing.

Over the past few quarters, BWXT has reaped the rewards of refurbishment and life extension projects on several reactors within the Canadian fleet. Notably, the government of Ontario announced an operating extension for Units 5 through 8 of the Pickering nuclear plant until the end of September 2026. Moreover, the government is initiating a feasibility study to explore the potential refurbishment of these reactors, which could extend their operational life by another 30 years. The Pickering plant currently accounts for 14% of Ontario's electricity production. Additionally, BWXT secured an engineering contract for the nuclear reactor pressure vessel of GE Hitachi's BWRX-300 small modular reactor. This nuclear reactor pressure vessel has garnered interest from organizations such as Ontario Power Generation, the Tennessee Valley Authority, SaskPower in Canada, and Synthos Green Energy in Poland.

In the field of nuclear medicine, BWXT remains dedicated to the deployment of Tc-99, a widely used diagnostic imaging agent that aids in the detection of illnesses like cancer and heart disease. The FDA conducted a preapproval inspection meeting in Kanata, Ontario, in March, and a verdict is expected soon. Once approved, BWXT will be able to scale up the commercial production of Tc-99 in 2024. Furthermore, the company is witnessing an increased demand for key therapeutic active pharmaceutical ingredients, such as lutetium and actinium, which play a vital role in supporting pharmaceutical companies during critical clinical trials. Actinium-225 is utilized in alpha therapies for various tumors, while lutetium-177 is used in beta therapies for tumor treatment.

BWXT has a long-term contract drug manufacturing agreement with Boston Scientific to produce ThermaSphere, a cancer-treating drug. The company is making strategic investments in automating the production process to significantly enhance capacity and meet the growing demand for ThermaSphere.

With a strong focus on innovation, expansion, and meeting market demands, BWXT's commercial operations are poised for continued growth. The company's advancements in modular reactors, nuclear medicine, and contract drug manufacturing demonstrate its commitment to providing cutting-edge solutions and making a significant impact in various industries.

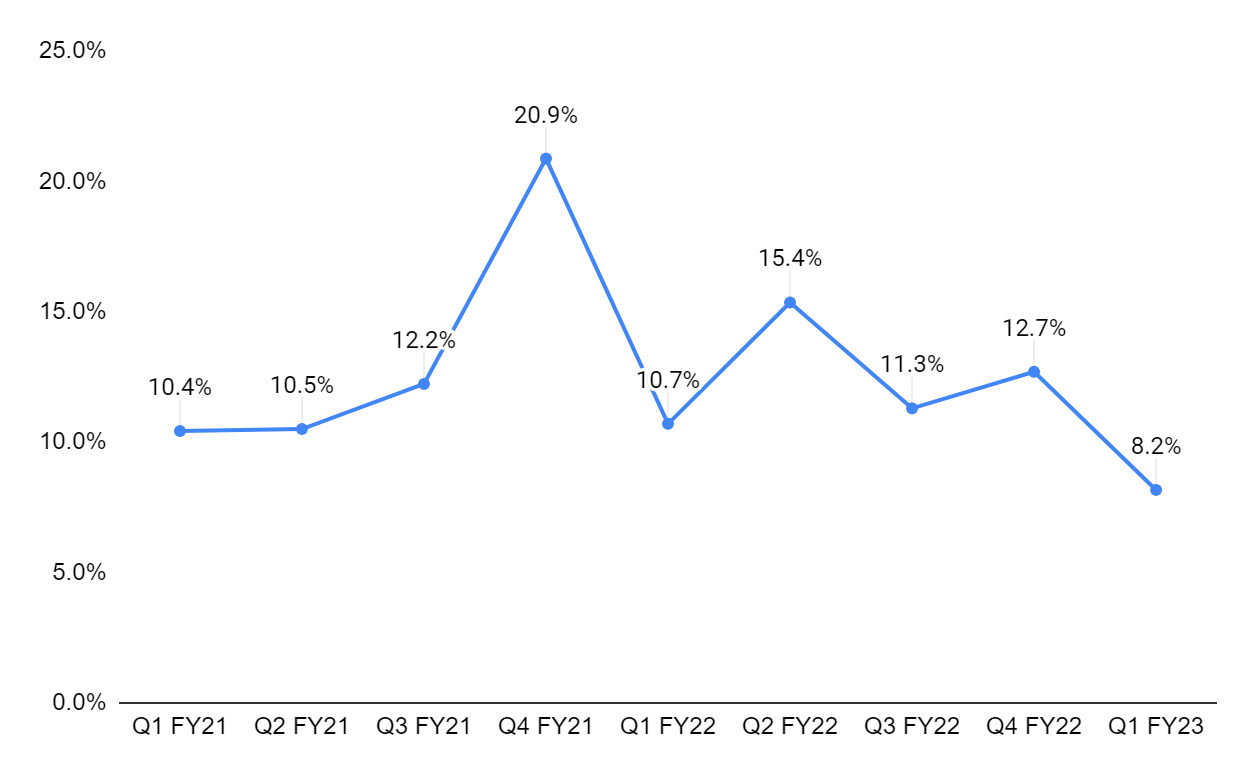

Commercial segment's adjusted EBITDA margins (Created by DzD Analysis by taking data from BWXT)

{kind=link}

The commercial business has experienced a decline in adjusted EBITDA margins recently, largely attributed to increased participation in lower-margin activities such as component manufacturing and field service refurbishment. However, BWXT is actively implementing cost-control measures within this business to enhance margins and drive long-term profitability. While I believe the margins in the short term should be under pressure, there are key factors contributing to this situation. One of these factors is the ongoing labor shortage, which poses challenges in meeting the increased demand for refurbishment activity. The need to address this demand amidst limited labor resources can impact margins in the near term.

Nonetheless, BWXT remains committed to improving profitability and operational efficiency within its commercial business. The company recognizes the importance of cost control and is undertaking initiatives to optimize expenses and enhance margins over time. By streamlining operations, implementing efficient processes, and closely managing costs, BWXT aims to mitigate the margin pressures caused by labor shortages and demand fluctuations. Looking ahead, I believe the company's efforts to control costs and improve margins should yield positive results in the long run.

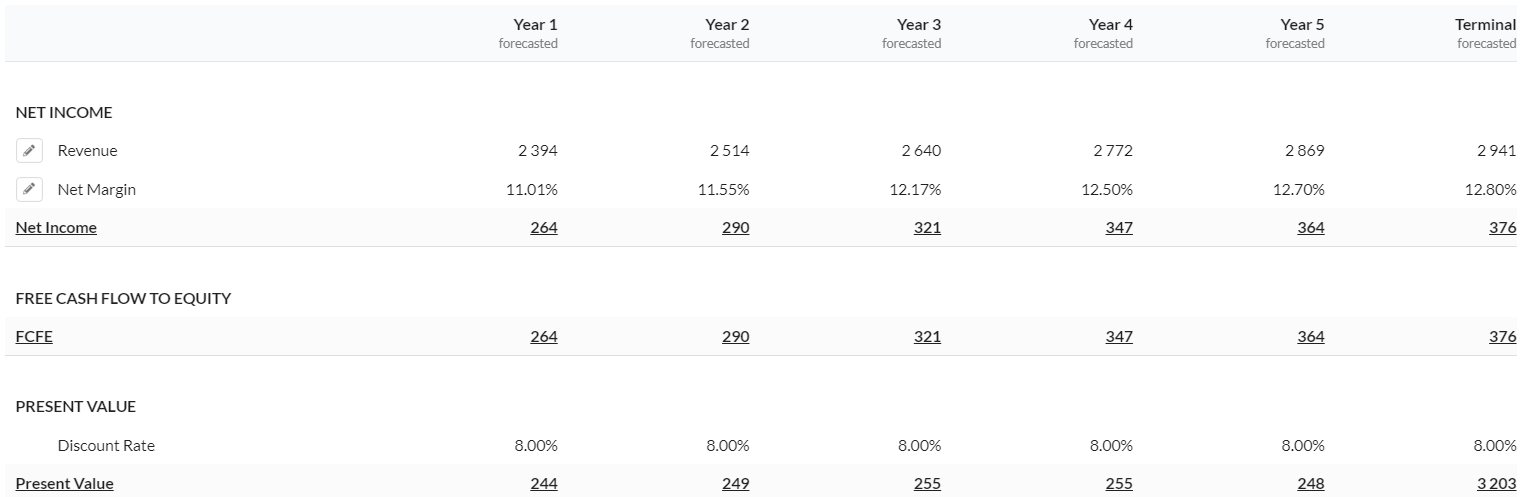

Valuation

{kind=link}

In my DCF calculations, I am assuming revenue growth to be in the mid-single digits in 2023, given the healthy order backlog and new contract wins. Beyond 2023, I have assumed growth to be in the mid-single digits, with a terminal growth rate in the low-single digits, as the company will continue to benefit from increased naval spending in the U.S., refurbishment of the nuclear plant in Canada, and commercialization of nuclear medicine. I used a discount rate of 7.00% and arrived at a fair value of $48.70 for BWXT.

Using the relative valuation, if we use a consensus EPS estimate of $2.89 for 2023, we get a price-to-earnings ratio of 22.34x, and if we use a consensus EPS estimate of $3.22 for 2024, we get a price-to-earnings ratio of 20.01x. These values are slightly above the five-year average forward P/E of 19.88x. Taking the FY24 EPS estimate and the average forward P/E, we arrive at a fair value of $64.04 for BWXT. Hence, I have a price target range of $48 to $64 for the company.

Conclusion

To conclude, while BWXT exhibits promising growth prospects, I maintain a neutral rating on the stock as it appears to have already reached its peak. In the near term, the company should benefit from a healthy order backlog. Furthermore, in the medium to long term, BWXT is positioned to capitalize on favorable market dynamics, including the trilateral agreement, a comprehensive 30-year shipbuilding plan, increased naval spending, advancements in nuclear medicine, and the refurbishment of nuclear reactors in Canada. Undoubtedly, BWXT is a commendable company with strong potential. However, the stock's current valuation suggests a slight overvaluation. Hence, I would prefer to wait on the sidelines until the stock reaches an appropriate price point that aligns with its intrinsic value.

For further details see:

BWX Technologies: Valuation Isn't Justified By Growth Opportunities