BYRN - Byrna Is Expensive As Advertising Bans Continue To Bite (Rating Downgrade)

2023-12-05 03:31:39 ET

Summary

- In Q3 FY23, the company’s net revenues slumped by 43% to $7.09 million due to advertising bans on several social media platforms.

- In October, Byrna secured a $6 million order in Argentina, but this is unlikely to turn the tide for sales growth.

- Cash is falling fast, and Byrna is starting to look expensive, with the market valuation rising by over 50% since my previous article on the company.

Introduction

I've been following US non-lethal weapon maker Byrna Technologies (BYRN) closely and I've written 4 articles about it on SA to date. The latest of them was in July when I said that the company had a strong balance sheet and that I expected net revenues to improve over the coming months due to rising international and dealer sales.

In October, Byrna secured a $6 million order in Argentina, but I’m concerned that sales remain depressed due to advertising bans. With the market capitalization growing by 52.9% since my previous article, I now feel comfortable with cutting my rating on the stock to sell. I think the company is starting to look overvalued, and that this could be a good time to take profits. Let’s review.

Overview of the recent developments

If you aren't familiar with the company or my earlier coverage, here's a short description of the business. Byrna focuses on the design, manufacturing, and sale of non-lethal self-defense guns, and ammo and its product offering also includes pepper spray, body armor as well as personal safety alarms. The company serves both the consumer and security professional markets and its core products include the Byrna SD launcher, the Byrna LE edition launcher, and the less lethal 12-gauge rounds. It has two manufacturing plants – a 30,000 square foot facility located in Fort Wayne, Indiana, and a 20,000 square foot manufacturing facility situated in the city of Pretoria in South Africa. In addition, Byrna has a 51:49 joint venture company in Uruguay that was created in January 2023 to expand its presence in Latin America. As you can see from the chart below, Byrna’s sales have been growing rapidly over the past few years thanks to an expanding product line and the company was expecting to grow by about 20% in 2023.

Byrna

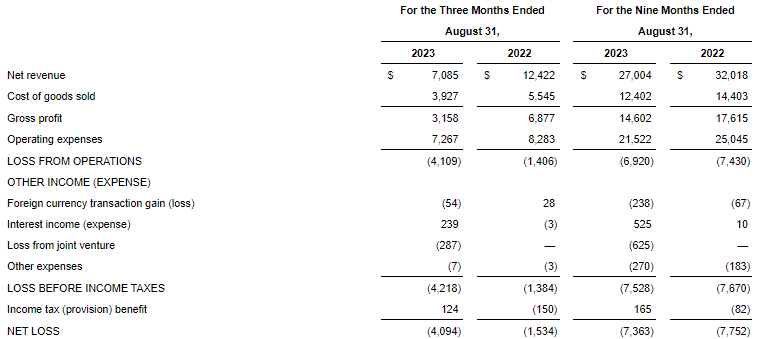

Unfortunately for investors, FY23 is shaping up as a weak year for the company and I think that net revenues are likely to fall over 20% compared to 2022. In Q1 FY23, sales were negatively affected by supplier issues and production problems. And as I explained in my previous article on the company, Q2 financials were put under strain due to an advertising ban by the social media platforms of Meta (META) and Alphabet's ([[GOOG]] [[GOOGL]]) Google after they classified Byrna’s items as contraband products. The bans started in late March and months later, Twitter (now X) also banned advertising by the company. These three bans led to a significant fall in orders and revenues in Q3 FY23. Looking at the financial results for the quarter, we can see that net revenues slumped by 43% year on year to $7.09 million while the operating loss almost tripled to $4.11 million. E-commerce sales through Byrna’s website and Amazon (AMZN) went down by $3.3 million to just $4.8 million (see page 20 here ). During its Q3 FY23 earnings call , the company said that daily sales declined by 20% compared to the month of March to just $44,000. International sales slumped to just $0.2 million from $2 million a year earlier while sales to domestic dealers/distributors decreased to $1.7 million from $1.8 million.

{kind=link}

Looking at the balance sheet, I think the situation is deteriorating rapidly as the net cash position was down to $13.7 million at the end of August compared to $20.1 million in November 2022 as free cash flow was negative $6 million for the first nine months of FY23.

Looking at what to expect for the future, I think that Q4 FY23 net revenues could be flat compared to a year earlier as average daily sales in September rose to $77,500 thanks to high advertising spending. Yet, this doesn't seem sustainable in the long run as the return on ad spend (ROAS) was about 2.5x. Byrna's international sales are usually characterized by infrequent but large orders and on October 26, the company announced a $6 million order with the Córdoba Provincial Police force in Argentina. This deal includes 4,000 launchers and is the largest order in its history. Yet, this contract accounts for just one eight of FY22 sales and I think it’s unlikely that sales growth will be back to positive territory in FY24 unless the advertising bans are lifted. They have been in place for several months now and there is no indication if or when they could end. And even if they were lifted today, it would likely take at least two months for e-commerce sales to regain momentum. Overall, I think it’s becoming clear that the business of Byrna could be unsustainable without advertising on social media and the valuation of the company is starting to look stretched as the enterprise value approaches $120 million. In my view, the share price rally over the recent months seems unjustified and this could be a good time to take profits. In addition, Byrna is starting to look like a good short selling opportunity as data from Fintel shows that the short borrow fee rate stands at just 1.28% as of the time of writing. There are around 900,000 shares available for short selling and buying call options for hedging purposes is relatively cheap at the moment, with June 2024 options trading at $0.55.

{kind=link}

Looking at the upside risks, I think that the major one is that a lift of the ban on advertising by any of the three social platforms could provide a significant short-term boost for the share price. The market valuation of Byrna could also gain momentum from additional international orders and it’s hard to predict those as they seem sporadic.

Investor takeaway

Byrna recently secured its largest order, but its sales have been weak over the past two fiscal quarters, and I think the business looks close to worthless without a lift of the bans on advertising by the major social media platforms. The company’s business model relies on e-commerce sales and there is no clear path to profitability without them growing significantly with a high ROAS. Cash is diminishing fast and Byrna is starting to look expensive. In my view, risk-averse investors should avoid this stock.

For further details see:

Byrna Is Expensive As Advertising Bans Continue To Bite (Rating Downgrade)