WHD - Cactus Earmarks CapEx For International Expansion

2023-04-04 14:48:10 ET

Summary

- Cactus, Inc. reported its Q4 2022 financial results on February 23, 2023.

- The firm provides wellhead equipment to the oil and gas industry.

- Revenue and profits have risen in recent quarters, and Cactus' management is expecting to begin funding its international expansion efforts in 2023.

- My discounted cash flow calculation indicates Cactus' stock may be fully valued here, so I'm on Hold for Cactus in the near term.

A Quick Take On Cactus

Cactus, Inc. ( WHD ) reported its Q4 2022 financial results on February 23, 2023, missing revenue but beating EPS consensus estimates.

The firm manufactures pressure control products for oil and gas drilling, completion and production for both onshore and offshore environments.

Given the firm's additional expenditures for its international expansion plans, which may take some time to bear fruit, and its apparent full valuation at around $43.00, I'm on Hold for Cactus, Inc. in the near term.

Cactus Overview

Houston, Texas-based Cactus was founded in 2011 to design and manufacture wellheads and pressure control equipment for the oil and gas industry.

The firm also rents or sells various types of high-pressure equipment related to fracking well completion operations.

Management is headed by CEO and Co-founder Scott Bender, who was President of Wood Group Pressure Control from 2000 to 2011 and has significant industry experience.

A number of Bender family members hold senior positions within the company.

Cactus has developed a line of products for pressure control, including:

-

Wellhead Systems

-

Frac Equipment

-

Flow Control Products

Market And Competition

According to a 2023 market research report by Market Data Forecast, the global wellhead equipment market for the oil and gas industry was an estimated $5.8 billion in 2020 and is forecast to reach $7.7 billion by 2028.

This growth would represent a CAGR of 4.85% from 2023 to 2028.

Cactus is focused on wellhead completion equipment. Potential hindrances to the market's growth include volatile oil and gas prices, which may slow capital allocation decisions as market participants seek to reduce risks.

Major competitive vendors that provide pressure control equipment include:

-

Delta

-

EthosEnergy

-

Integrated Equipment

-

Jereh Oilfield Equipment

-

Jiangsu Sanyi Petroleum Technologies

-

JMP Petroleum Technologies

-

Msp/drilex

-

Uztel S.A.

-

Sunnda Corporation

-

Weir Group

-

Others

Cactus' Recent Financial Results

-

Total revenue by quarter has risen per the following chart:

Total Revenue History (Seeking Alpha)

-

Gross profit margin by quarter has trended materially higher:

Gross Profit Margin History (Seeking Alpha)

-

Selling, G&A expenses as a percentage of total revenue by quarter have been trending lower, except for the most recent quarter:

Selling, G&A % Of Revenue (Seeking Alpha)

-

Operating income by quarter has moved substantially higher in recent quarters:

Operating Income History (Seeking Alpha)

-

Earnings per share (Diluted) have also risen markedly:

Earnings Per Share History (Seeking Alpha)

(All data in the above charts is GAAP.)

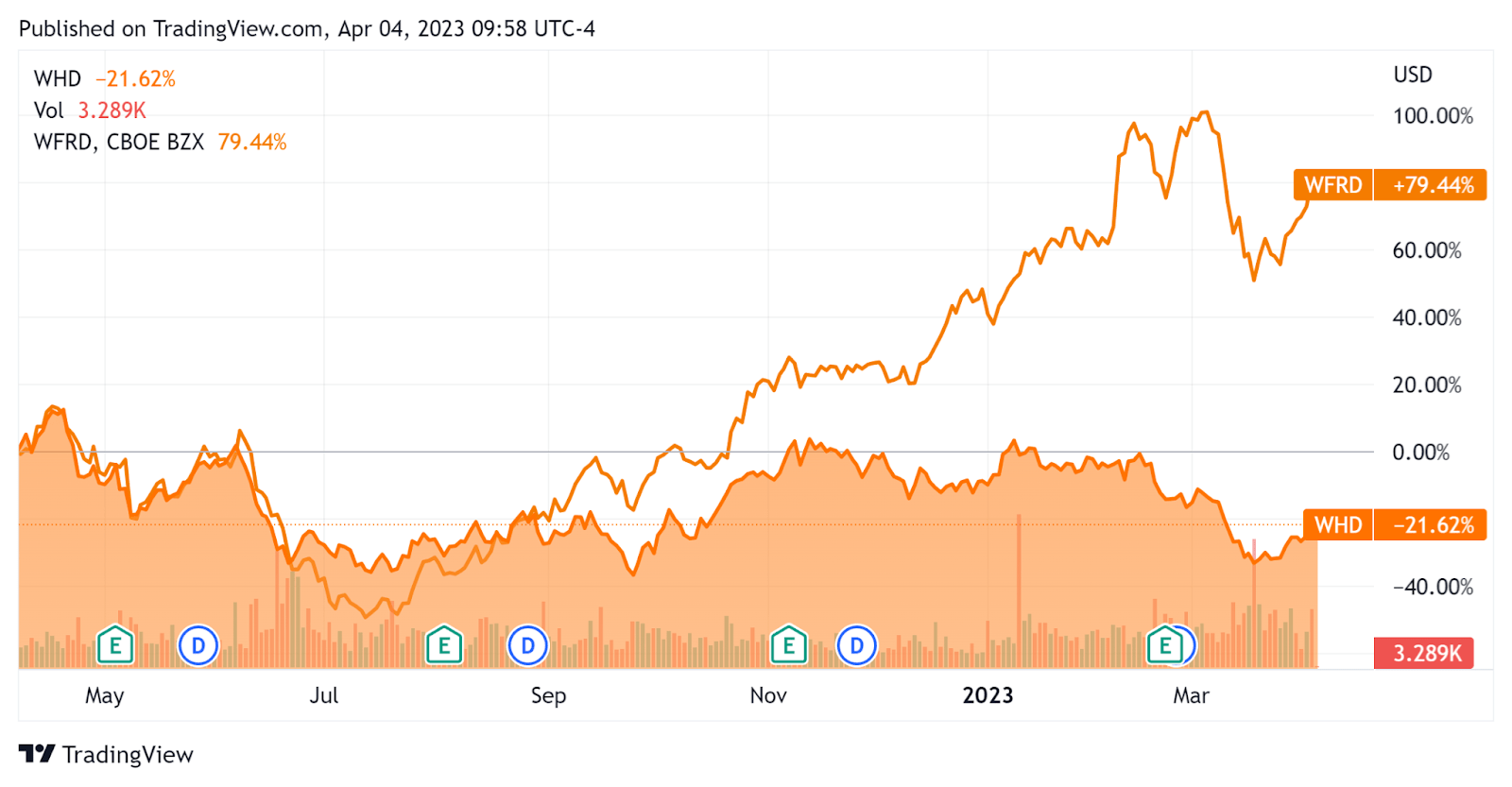

In the past 12 months, WHD's stock price has fallen 21.6% vs. that of Weatherford International's rise of 79.4%, as the chart indicates below:

{kind=link}

As to its Q4 2022 financial results , total revenue rose 44.6% year-over-year, and gross profit margin increased by 8.1 percentage points.

SG&A as a percentage of total revenue increased sequentially after several quarters of trending lower, while operating income remained elevated, as did earnings per share.

For the balance sheet , the company finished the quarter with $344.5 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was an impressive $89.6 million, of which capital expenditures accounted for $28.3 million. The company paid only $10.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Cactus

Below is a table of relevant capitalization and valuation figures for the company:

| Measure ((TTM)) |

| Amount |

| Enterprise Value/Sales |

| 3.6 |

| Enterprise Value/EBITDA |

| 11.9 |

| Price/Sales |

| 3.6 |

| Revenue Growth Rate |

| 57.0% |

| Net Income Margin |

| 16.0% |

| GAAP EBITDA % |

| 30.3% |

| Market Capitalization |

| $3,270,000,000 |

| Enterprise Value |

| $2,490,000,000 |

| Operating Cash Flow |

| $117,880,000 |

| Earnings Per Share (Fully Diluted.) |

| $1.79 |

(Source - Seeking Alpha)

As a reference, a relevant partial public comparable would be Weatherford International (WFRD); shown below is a comparison of their primary valuation metrics:

| Metric ((TTM)) |

| Weatherford Int'l |

| Cactus |

| Variance |

| Enterprise Value/Sales |

| 1.4 |

| 3.6 |

| 163.5% |

| Enterprise Value/EBITDA |

| 7.6 |

| 11.9 |

| 57.1% |

| Revenue Growth Rate |

| 18.8% |

| 57.0% |

| 202.6% |

| Net Income Margin |

| 0.6 |

| 16.0% |

| -73.3% |

| Operating Cash Flow |

| $349,000,000 |

| $117,880,000 |

| -66.2% |

(Source - Seeking Alpha)

Future Prospects For Cactus

In its last earnings call ( Source - Seeking Alpha ), covering Q4 2022's results, management highlighted its margin growth despite Q4 typically being a weaker quarter due to seasonal factors.

The firm expects to spend $40 million in 2023 on CapEx, which would be materially higher than 2022's result of $28.3 million. Included in this growth figure is $5 million to $10 million in growth capital dedicated to international (Middle East) expansion toward the end of the year.

Management also expects relatively robust 2023 growth from domestic business since its core customers tend to be larger public oil-focused companies whose plans are less subject to the ups and downs of price.

Regarding valuation, my discounted cash flow calculation indicates the shares may be fully valued at their current level, given the assumptions of the DCF, as shown below:

{kind=link}

The primary risk to Cactus, Inc.'s outlook is the volatile nature of oil markets since the Russian invasion of Ukraine and the recent sharp drop in the price of natural gas.

Given the firm's additional expenditures for its international expansion plans, which may take some time to bear fruit, and its apparent full valuation at around $43.00, I'm on Hold for Cactus, Inc. in the near term.

For further details see:

Cactus Earmarks CapEx For International Expansion