WHD - Cactus: Falling Rig Counts A Risk But Shares Undervalued Amid Strong Growth Trends Ahead

2023-06-26 15:14:46 ET

Summary

- US oil rig counts have declined, posing a challenge for oil service and wellhead equipment firms.

- Cactus, Inc. remains a buy due to its strong free cash flow yield and growth outlook.

- The company's valuation and growth outlook outweigh the lackluster chart setup.

- I outline key price levels to monitor as its August earnings report nears.

US rig counts are on the decline. After peaking in late 2022, operational US oil rigs have dropped significantly, according to the weekly Baker Hughes report. That is a headwind for oil service and wellhead equipment firms. Still, I have a buy rating on Cactus, Inc. (WHD).

Downtrending US Crude Oil Rig Count

The Daily Shot

According to Bank of America Global Research, WHD is a pure-play wellhead and pressure control equipment provider for the U.S. market. It also designs, manufactures, and sells a range of wellheads and pressure control equipment in Australia, China, and the Kingdom of Saudi Arabia.

The Houston-based $3.1 billion market cap Oil and Gas Equipment and Services industry company within the Energy sector trades at a near-market 18.4 trailing 12-month GAAP price-to-earnings ratio and pays a modest 1.1% dividend yield, according to The Wall Street Journal.

Back in May, WHD reported a bottom-line beat while revenue also topped analysts’ estimates. With net sales rising more than 56% YoY, operating EPS more than doubled from the same period a year earlier. More good news came in early June when Cactus shares jumped 10% following the announcement of a new share repurchase program and updated revenue guidance to the good side.

The positive earnings revision was good enough for Goldman Sachs to earmark WHD as a top EPS revision name that is flying under the radar. I don’t think that its historically high P/E in the 30s is warranted any longer, though. Falling US rig counts and efficiencies and softer international wellhead markets are headwinds in the coming years.

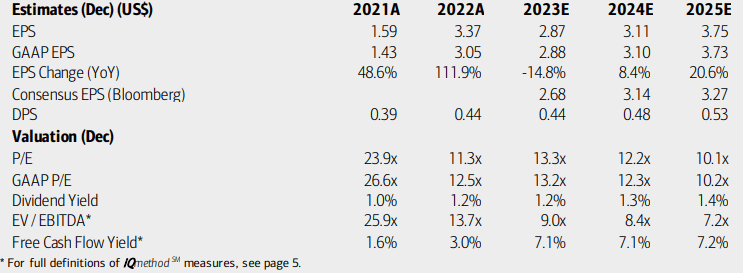

On valuation , analysts at BofA see earnings falling sharply this year before per-share profits bounce back in 2024 and ‘25. The Bloomberg consensus forecast is about on par with what BofA projects. Dividends, meanwhile, are seen as rising at a steady clip through the next several quarters.

With operating earnings multiples in the low to mid-teens currently, shares trade at a discount to the broad market but at a slight premium to the sector median. WHD’s EV/EBITDA ratio is modest compared to the S&P 500’s average and what is particularly appealing about Cactus is its strong free cash flow yield.

WHD: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

While the Quant Rankings give WHD an F on valuation, I assert the situation is much less bleak. With the company seeing a near-term drop in EPS, the P/E appears high. Consider, though, that its 5-year average multiple is about 32.5. A more modest valuation premium is warranted, though. If we assume a normalized EPS of $3 and use just a 19 multiple (near the SPX average), then the stock should be near $57.

Cactus: A Valuation Premium to the Energy Sector

Seeking Alpha

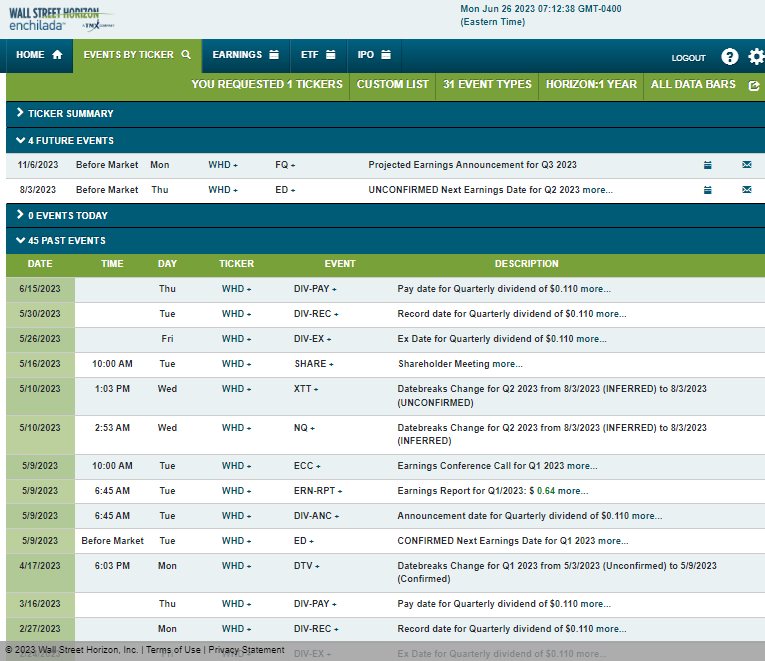

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2023 earnings date of Thursday, August 3 BMO. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

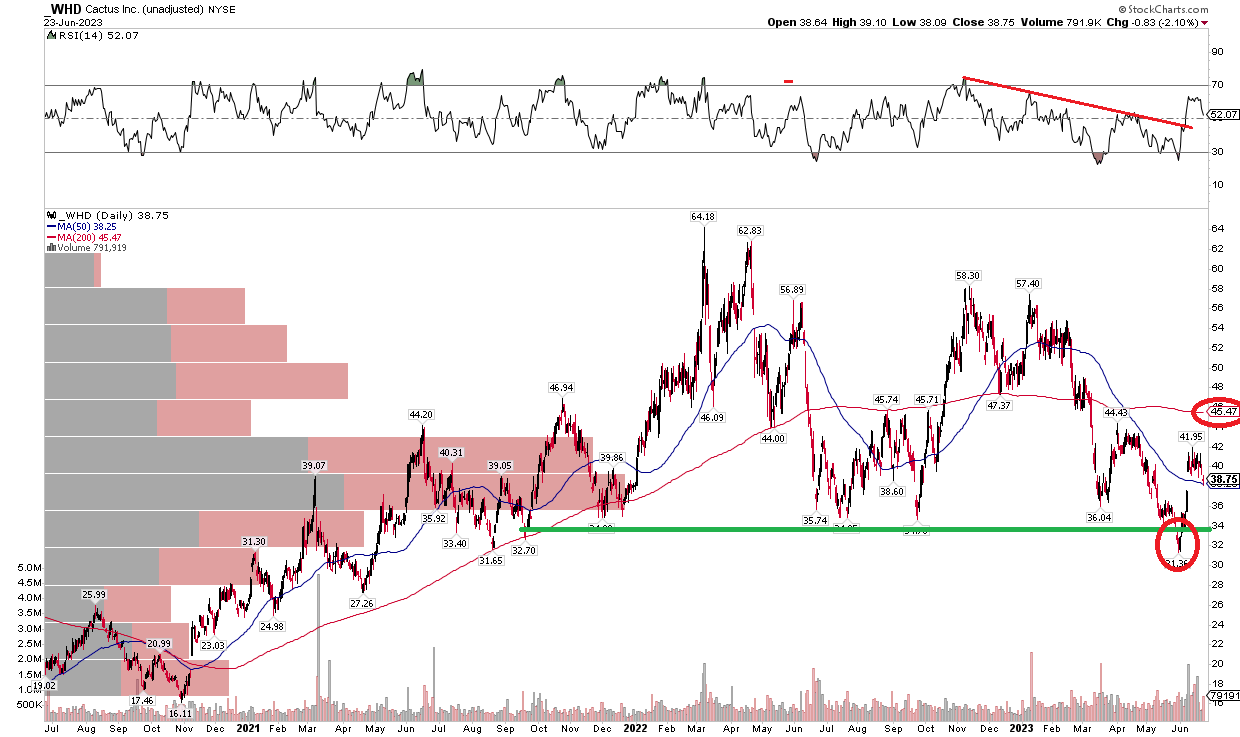

With shares on sale at the moment, the technical situation is less appealing. Notice in the chart below that Cactus spiked lower earlier this quarter, breaking below key support in the $34 to $35 range. That’s a bullish false breakdown, and the stock popped to $42 in short order. Sellers have regained some control, though, and a gap is appearing to be getting filled down to the $37 to $38 zone. With a flat 200-day moving average, there is an ongoing battle between the bulls and bears.

What’s encouraging, however, is that the RSI momentum indicator at the top of the chart sports a breakout above a downtrend line. We’ll see if that portends an upside share price move. For now, it is a sideways trend and the $45 to $47 range is key for the bulls to penetrate while the recent low of $31 is support. Also take a look at the volume by price indicator on the left-hand side of the chart – there's major congestion in the $35 to $44 range, implying this area may hold for some time. Overall, the technical situation is likewise a hold.

WHD: Bullish False Breakdown, Encouraging RSI Breakout, But Sideways Price Trend

{kind=link}

The Bottom Line

I assert WHD’s valuation and growth outlook outweigh the lackluster chart setup. I have a buy rating and look forward to what the August earnings report has in store.

For further details see:

Cactus: Falling Rig Counts A Risk, But Shares Undervalued Amid Strong Growth Trends Ahead