WHD - Cactus Inc.: Concerns Regarding Future U.S. Oil Rig Demand

2023-09-24 04:15:17 ET

Summary

- Cactus has a dominant 41.8% market share in the US surface equipment industry, driven by innovative technology and agile manufacturing.

- The US oil rig count is declining, making a return to historical highs unlikely, which could constrain WHD's growth prospects.

- WHD's future growth in the US market is closely tied to fluctuations in the US rig count.

Investment action

Based on my current outlook and analysis of Cactus, Inc. ( WHD ), I recommend a hold rating for the company. My assessment is based on the expectation that U.S. oil rig counts are unlikely to reach historical highs, given the current decline in oil prices compared to the levels observed following the Russian-Ukraine conflict. Additionally, given WHD's significant market share in the US, its growth opportunities in established US segments seem limited and closely tied to fluctuations in the US oil rig count.

Basic Information

WHD specializes in the design, manufacturing, and sale of wellhead and pressure control equipment. Its product range primarily caters to onshore unconventional oil and gas wells, playing vital roles in the drilling, completion, and production stages of its customers' well operations. In addition to selling products, the company provides extensive field services for all its offerings, including rental items and assistance in the installation, maintenance, and safe operation of wellhead and pressure control equipment. Furthermore, WHD offers repair and refurbishment services for these products.

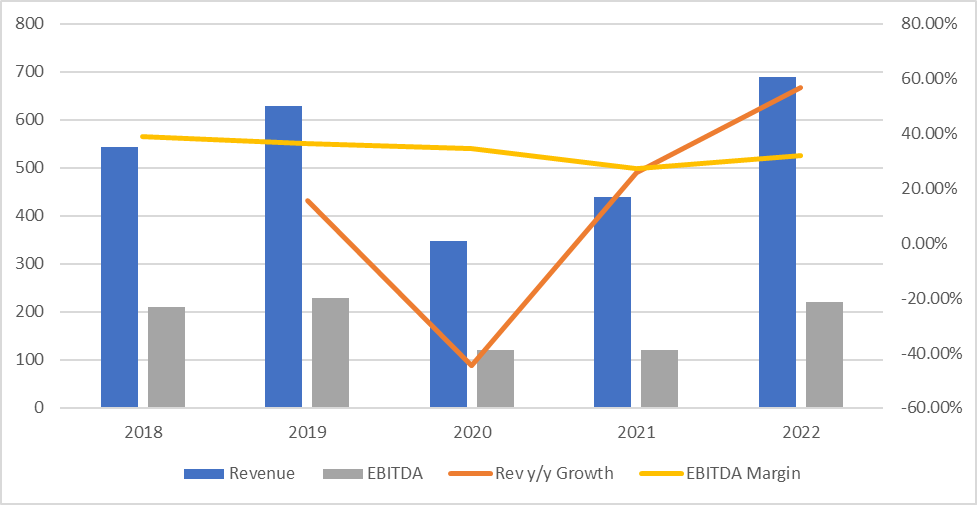

Over the past five years, the company has experienced a gradual revenue recovery to levels seen prior to the COVID-19 pandemic. In 2022, the company's revenue reached $688 million, a notable increase compared to the $544 million recorded in 2018. Given the impact of the pandemic, it's worth examining the CAGR, which provides a smooth average annual growth rate. WHD has achieved a CAGR of 4.81% in revenue over this period.

Regarding its adjusted EBITDA margin, the company has maintained consistency, with a median margin of 34%. However, it's important to note that there is a noticeable declining trend in this margin over time, as it fell to 32% from 39% in 2018.

WHD holds the top position in the US market with a strong market share . Its market dominance has surged, rising from a modest 0.8% in 2011 to an impressive 41.8% by 2021. Moreover, WHD boasts substantial growth prospects through geographic expansion. Presently, WHD's equipment services are accessible in just 24% of the world's total geographic expanse, leaving a substantial 76% of untapped potential for business expansion.

{kind=link}

Review

WHD holds the coveted position of industry leader in US surface equipment. The company has significantly expanded its presence in the US market, witnessing an impressive climb in its US market share from a mere 0.8% in 2011 to a commanding 41.8% by 2023. This remarkable growth can be attributed to WHD's innovation in wellhead technology and its agile manufacturing processes, which have found favor among US shale-oriented Exploration and Production (E&P) customers when compared to larger competitors.

However, despite this substantial market share growth, the overall US oil rig count is experiencing a downward trajectory due to low oil prices , which have yet to recover to the levels seen following Russia's invasion of Ukraine. Since the beginning of 2023, the oil rig count has consistently declined from 621 to 513, marking a significant 17% decrease. The surge in oil rig counts witnessed after the invasion has not been sustained, and with current oil prices nowhere near the levels seen during the initial stages of the conflict, a return to historical high rig counts is unlikely.

Aside from the sales of surface equipment in the US, WHD's field service also contributes to ~20% of revenue. Revenue from field services is closely linked to the volume of product sales and equipment rentals. The decreasing number of oil rigs in the US, which will affect the sales of surface equipment, is expected to also have a downstream impact on field service revenue, therefore bringing more headwinds to WHD’s revenue growth outlook.

Essentially, all service sales are provided to E&P customers in conjunction with a product sale or rental, primarily involving the assembly, maintenance, and repair of on-site equipment. The majority of service revenue comes from labor crews, and there were concerns about labor shortages in 2022.

Despite these challenges, WHD consistently achieved some of the highest margins in the Oilfield Services [OFS] sector. Over the past five years, the company has maintained an impressive average adjusted EBITDA margin of 34%, surpassing competitors like Schlumberger and TechnipFMC, whose margins typically linger around 27%. This strong margin is fueled by the unique products WHD offers within each of its categories and contributions from the Spoolable Technologies segment, whose field service revenue is grouped under. Considering the labor shortage, I find it challenging for WHD to attain its 5 years historical median margin of 34%. Therefore, I expect the margin to stay around its current level of approximately 32%.

“On a stand-alone basis, each of Cactus and FlexSteel set records for both quarterly revenue and adjusted EBITDA. This strength reflects the highly differentiated offerings in each of our segments. Adjusted EBITDA margin for the quarter was 37.7% of revenues, an increase from the first quarter due to operating leverage and higher contribution from the Spoolable Technologies segment” 2Q23 call.

Valuation

I believe WHD will grow by 18% in FY25 due to the declining number of oil rigs in the US. Despite the increase in its US market share, the total count of oil rigs in the US has been consistently declining due to the ongoing slump in oil prices, which have not yet recovered to the levels observed following Russia's invasion of Ukraine. Since the start of 2023, there has been a continuous decrease in the oil rig count, amounting to a significant 17% decline. The surge in oil rig counts witnessed after the invasion is unlikely to be repeated, given the current oil price levels. Consequently, I do not anticipate the oil rig count returning to historical highs. With regard to profit margins, I expect WHD to maintain its current levels, thanks to its distinctive offerings within each of its business segments and contributions from the Spoolable Technologies segment.

WHD is presently trading at a forward EV/EBITDA multiple of 9.43x. This valuation is in line with its peers, such as Schlumberger and TechnipFMC, which trade at a median multiple of 9.43x. I expect the market to assign WHD a higher multiple of 10x, aligning it closer to Schlumberger, which trades at 10.71x given that WHD boasts higher margins at 34%, compared to peers' medians of approximately 27%. Considering these factors, At this multiple, my target price for WHD is $53.95, representing a potential 11% upside.

Author's work

Risk and final thoughts

WHD's robust presence in the U.S. onshore market is a testament to the company's engineering prowess and its well-established reputation among E&P customers. Nevertheless, larger-cap competitors such as Schlumberger have access to greater financial resources and a more extensive range of services. This advantage could potentially result in a faster pace of technological innovation and heightened competition stemming from bundled service offerings. Considering WHD's dominant US market share, its future growth prospects in its established US segments appear relatively constrained and are largely contingent on fluctuations in the U.S. rig count.

WHD has emerged as a leading player in the US surface equipment industry, with its US market share surging from a mere 0.8% in 2011 to a dominant 41.8% by 2023. This impressive growth is attributed to WHD's innovative wellhead technology and agile manufacturing, favoured by US shale-oriented E&P customers over larger competitors.

However, despite this remarkable market share gain, the US oil rig count faces a continuous decline due to decreasing oil prices, which is far from the levels seen after Russia's Ukraine invasion. Since early 2023, the rig count has plummeted by 17%, making a return to historical highs unlikely. Considering WHD's dominant US market share, its future growth prospects in its established US segments appear relatively constrained and are largely contingent on fluctuations in the U.S. rig count. Therefore, I recommend a "hold" rating given headwinds in US oil rig demand.

For further details see:

Cactus, Inc.: Concerns Regarding Future U.S. Oil Rig Demand