WHD - Cactus Is Sufficiently Balanced To Absorb The Topline And Margin Pressure

2023-09-13 11:02:44 ET

Summary

- Cactus is facing challenges in the energy industry downturn, particularly in its Pressure Control segment.

- Inflationary pressures on input costs are receding, and supply chain diversification can lower WHD's cost structure.

- It has increased dividend and repaid debt related to the FlexSteel acquisition.

WHD Is Internally Sturdy

Cactus ( WHD ) designs and manufactures engineered wellhead, pressure control, and spoolable pipe technologies. It also provides field services related to the equipment's installation, maintenance, and handling. WHD is wading through the rough weather when US drilling activity is on a downhill. Specifically, its Pressure Control segment will be prone to the energy activity downfall, leaving a hole in its operating margin. So, the company's new FY2023 capex guidance reflects the moderation of onshore industry capex.

On the other hand, the inflationary pressures on input costs are receding, which can offset the negative impact on the margin. Supply chain diversification can lower its cost structure. The acquisition of FlexSteel would augment the speed of installation and reduce cost. With improving working capital and ample liquidity, the balance sheet is robust. The stock is reasonably valued versus its peers. I suggest investors "hold" WHD stock for moderate medium-term returns.

Business And Brief History

WHD was incorporated in February 2017. It manufactures and sells Cactus SafeDrill wellhead systems and frac stacks. It also produces SafeClamp and SafeInject systems, Cactus SafeLink monobore, zipper manifolds, and production trees. It operates through 15 US service centers, three service centers in Eastern Australia, and manufacturing & production facilities in China.

In February 2023, it acquired FlexSteel Holdings – a manufacturer of differentiated onshore spoolable pipe technologies- increasing WHD's topline significantly. WHD's management structure has recently changed. Bruce Rothstein stepped down as its Chairman, and Scott Bender, the CEO, assumed the additional role of the Chairman.

Industry Drivers And Cost Factors

{kind=link}

Baker Hughes

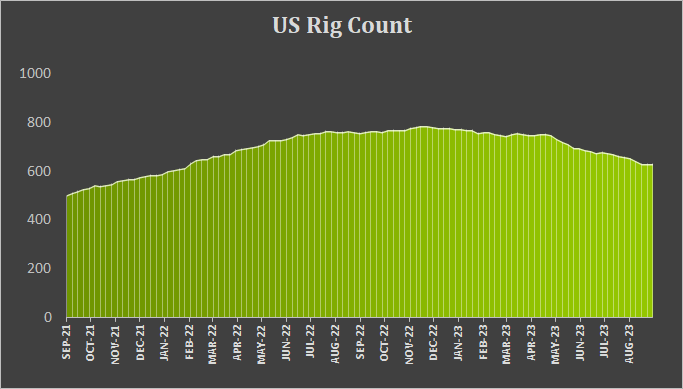

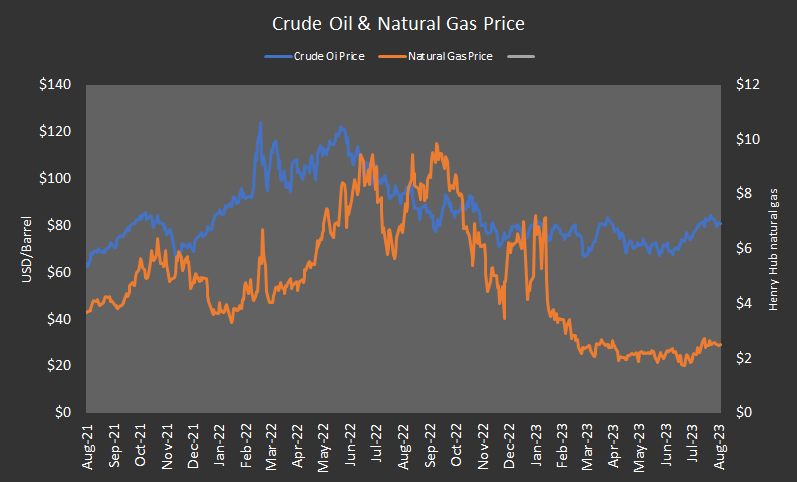

WHD's relatively large-sized customers invest through the commodity cycles. So, its revenue will likely outperform the US rig count shortly, especially when the rig counts are declining. From Q1 to Q2, the crude oil price declined by 5%. During this period, the US rig count decreased by 11%. Since the start of Q3, the crude oil price has been up-trending (24% up until the first week of September). I think that if commodity prices do not slip, customer activity will remain flat in Q3 and Q4.

Revenue will be adversely affected in WHD's Pressure Control segment. The company has started diversifying geographically in the Middle East but remains at trial. It expects to finalize its investment structure and record its first customer order in late 2024. In the near term, lower revenue can also hurt the margin through lower operating leverage. However, supply chain costs have been deflating after a long period of inflationary pressures on input costs. So, this can mitigate the negative effects in Q3 and intensify in Q4. On the operating margin side, the adverse effects of high-cost inventory in Q1 appear to be over for the company.

The Acquisition Benefits

In the Spoolable Technologies segment, product diversification related to FlexSteel (in March) should keep the topline steady in Q3. The initial response to FlexSteel products' introduction to WHD's existing customers has been strong. The supplementary product suite of FlexSteel will increase the speed of installation, reduce the cost of ownership, and improve efficiency in field operation, reducing emissions. It has also integrated its sales organizations in the US and internationally.

The spoolable technologies offer multiple growth opportunities, including increased customer penetration for larger-diameter gathering, under-pad applications for wellhead, midstream applications, and the future possibility of participating in carbon capture & underground storage (or CCUS) technology.

Near-Term Outlook

{kind=link}

WHD's Filings and Q2 Transcript

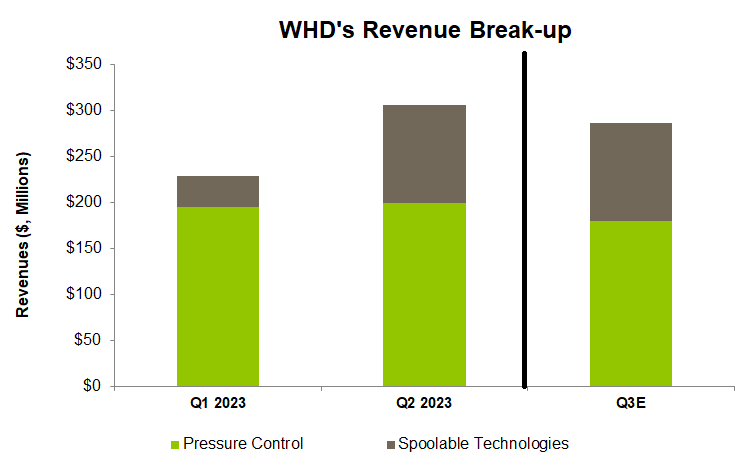

The company's management estimates that revenues in the Pressure Control segment can decrease by 10% in Q3 compared to Q2, while it can remain unchanged in the Spoolable Technologies segment. It also expects the adjusted EBITDA margins in the Pressure Control segment to decrease by 140 basis points (at the guidance mid-point).

The adjusted EBITDA margin of Spoolable Technologies can deflate by 260 basis points, according to the company's estimates. Overall, its consolidated revenues can decrease in Q3, although the in-process supply chain diversification can lower its cost structure and result in a competitive advantage for the company.

Analyzing Q2 Drivers

{kind=link}

Seeking Alpha

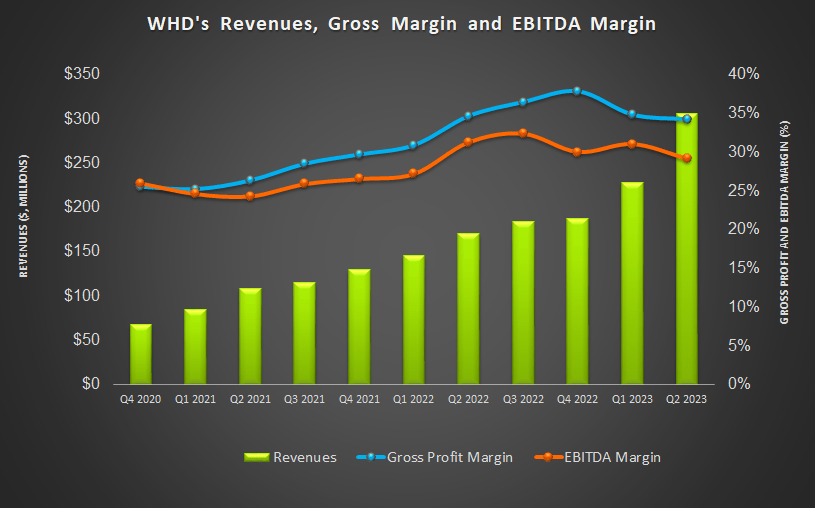

From Q1 to Q2, WHD's revenues in the Pressure Control segment increased by a modest 2.3% despite the decline in US onshore activity. Operating margin expanded by 200 basis points due to lower transaction expenses.

In Spoolable Technologies, revenues increased by 2.1x following the revenue addition from the FlexSteel acquisition. The adjusted EBITDA also increased handsomely here due to the depletion of higher-cost materials and improved operating leverage. However, the operating income turned to a loss in Q2 due primarily to the step up in value of inventory cost and the remeasurement of the earn-out expenses with the FlexSteel acquisition.

Cash Flows and Balance Sheet

Cactus's cash flow from operations improved sharply in 1H 2023 compared to a year ago. Higher revenues and lower working capital requirements following decreased purchases of inventories to the cash flow rise. Free cash flow also increased significantly compared to a year ago. Its FY2023 capex guidance is $35 million-$45 million. Much of the investments are related to low-cost supply chain diversification, although its investments in the Middle East have been deferred to 2024.

WHD's debt-to-equity ratio (0.06x) is much lower than its peers' ([[CHX]], [[THNPY]], [[NOV]]) average of 0.33x. As of June 30, 2023, its liquidity was $257 million. It has also repaid $155 million of debt raised to finance the FlexSteel acquisition. So, robust liquidity ensures little financial risks. In August, it increased its dividend by 9%. Plus, it has authorized $159,000 of share repurchase.

Relative Valuation And Wall Street Rating

{kind=link}

Author Created and Seeking Alpha

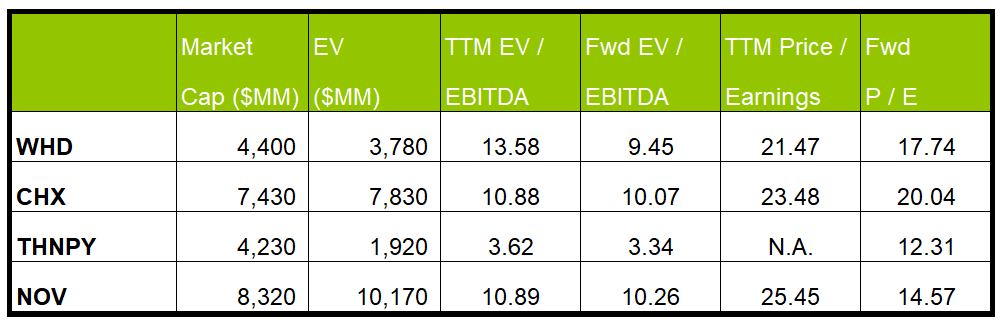

WHD's forward EV/EBITDA is expected to contract versus the current EV/EBITDA multiple. The rate of contraction is steeper than some of its peers. This typically results in a higher EV/EBITDA multiple. The company's EV/EBITDA multiple (13.6x) is much higher than its peers' (CHX, THNPY, NOV) average (8.5x).

The current multiple is slightly below its five-year average EV/EBITDA of 13.5x. So, the stock appears to be reasonably valued compared to its peers. In my opinion, based on the company's fundamental strength, its EV/EBITDA can expand modestly, resulting in 3%-5% returns in the near-to-medium term.

{kind=link}

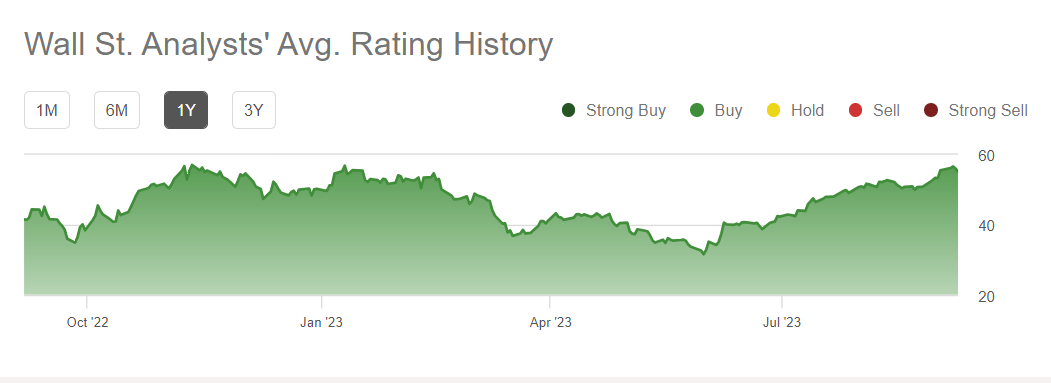

Seeking Alpha

In the past 90 days, four sell-side analys ts rated WHD a "buy" (including "strong buy"). Five analysts rated it a "hold," while one rated it a "sell." The consensus target price is $56.9, suggesting a 3% upside at the current price.

Risk Factors

{kind=link}

Seeking Alpha

Demand for WHD's products and services depends significantly on energy prices, which, in turn, affect oil and gas industry activity and upstream capex levels. Energy prices, especially natural gas, have been volatile recently. Over the past year, natural gas prices have crashed by ~65%, while crude oil prices have been steady (~1% up).

The periodic downturns have diminished demand for the company's offerings and put downward pressure on its product pricing. A weakened natural gas price can further reduce energy operators' capital budgets and drilling activity, keeping the company's topline and cash flow under pressure in the near term.

What's The Take On WHD?

{kind=link}

Seeking Alpha

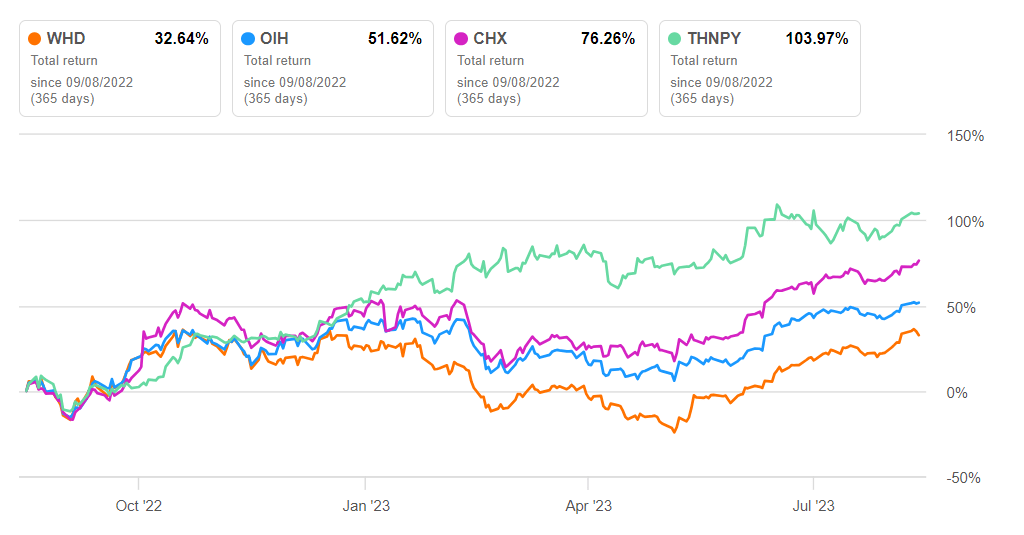

Lower rig count affected WHD's topline and put pressure on the cost through weaker operating leverage. So, the stock underperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year. Therefore, the company has placed significant emphasis on improving the cost structure. The supply chain costs have been deflating, releasing the pressure of high-cost inventory on the working capital. It plans to diversify in the Middle East and expects to finalize its investment structure and record its first customer order in late 2024.

To maintain a light cost structure, it has deferred its investments in the Middle East to 2024. The company's cash flows improved sharply in 1H 2023, with lower capex and inventory cost reductions. Its balance sheet is robust, with ample liquidity. Given the relative valuation multiples and the impact of the multitude of factors, to "hold" the stock would be a good ploy for the investors.

For further details see:

Cactus Is Sufficiently Balanced To Absorb The Topline And Margin Pressure