CADE - Cadence Bank: Another Regional Bank Worth Considering

2023-07-10 05:42:05 ET

Summary

- The banking sector, particularly Cadence Bank, is an attractive investment opportunity due to its solid financial health and low share price.

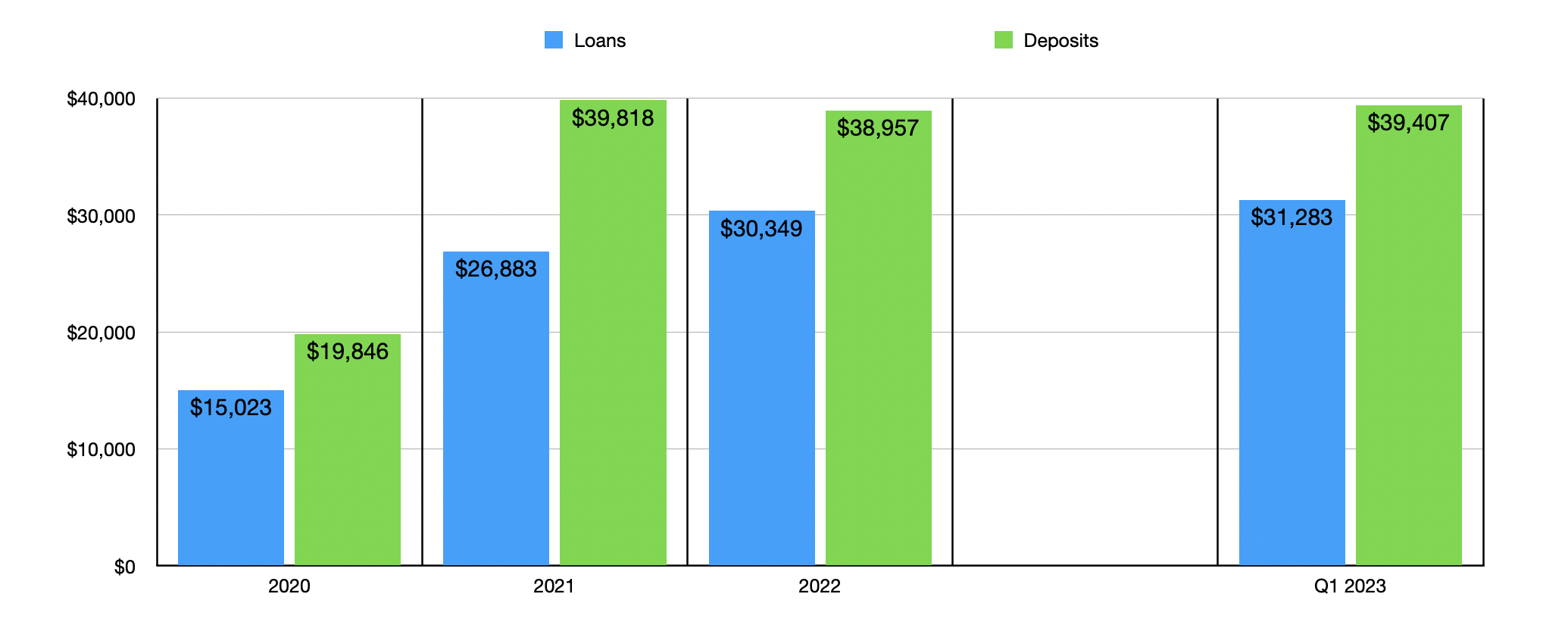

- Cadence Bank's loan portfolio has doubled from $15 billion to $30.3 billion between 2020 and 2022, largely due to mergers, and its deposit base remains stable.

- Despite a rough bottom line for the first quarter of 2023, the bank's overall financial performance has been strong in recent years and shares are cheap enough to warrant optimism.

In my opinion, one of the most attractive areas for investors to consider at this moment in time is the banking sector. After being slammed earlier this year by the fallout associated with Silicon Valley Bank and the other financial institutions that ultimately collapsed, share prices of many of these companies have not fully recovered. One really good example of this can be seen by looking at Cadence Bank ( CADE ). After CADE stock fell by 34.8% from the end of February until it reached its bottom point during the crisis, you would expect new data that showed stability to be welcomed by a surge in the share price. But as of today, the stock is still trading 22.7% below what it was at the end of the second month of this year. This would be understandable if the fundamental picture of the business was worsening materially. But when you dig under the hood, you find that the company is in pretty solid shape right now. Because of this, and because of how cheap the stock currently is, I have no problem rating it a ‘buy’ at this time.

Understanding Cadence Bank

According to the management team at Cadence Bank, the company was originally chartered in 1876. Since then, it has grown into a sizable regional commercial bank and financial services company that operates over 400 commercial banking, mortgage, and insurance locations throughout. It also has one location in Illinois and a loan production office in Oklahoma. Over the years, the company has grown to offer a wide variety of services. For instance, through its commercial lending operations, it provides commercial loan services like term loans, lines of credit, equipment and receivable financing solutions, and more. The company offers residential consumer lending solutions, such as fixed and adjustable-rate residential mortgage loans that it originates. Through its non-residential consumer lending business, the company also provides loans for things like automobiles, RVs, boats, and more.

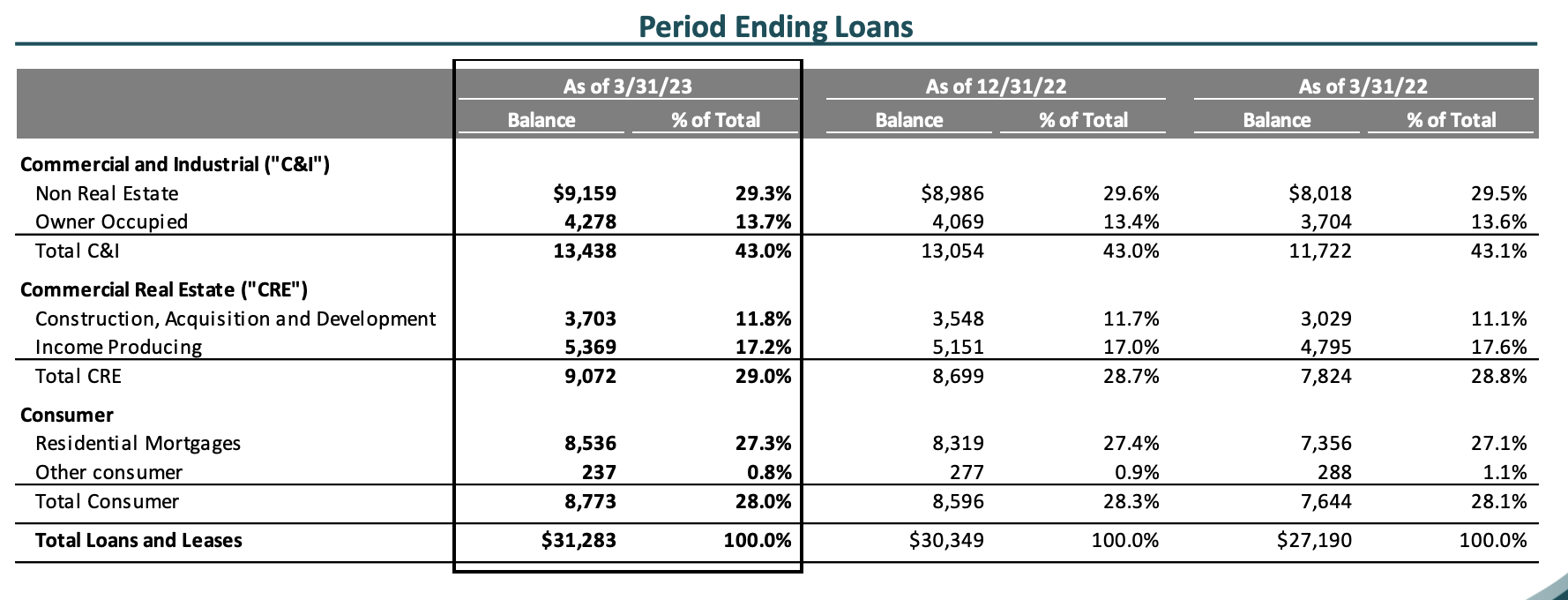

From 2020 through 2022, the company saw the value of the loans on its books approximately double, climbing from $15 billion to $30.3 billion. Much of this increase was driven by mergers, including three that it completed in 2021. By the first quarter of the 2023 fiscal year, its loan book had grown even further to $31.3 billion. Approximately 43% of its loans by value involve commercial and industrial loans. Its greatest exposure on this front it's to the energy sector, with 5% of its total loan value dedicated to that market. The rental and leasing of real estate comes in at about 5% as well, or $1.4 billion. Other major categories for the commercial and industrial space include restaurants, retail firms, the healthcare sector, and financial and insurance companies.

{kind=link}

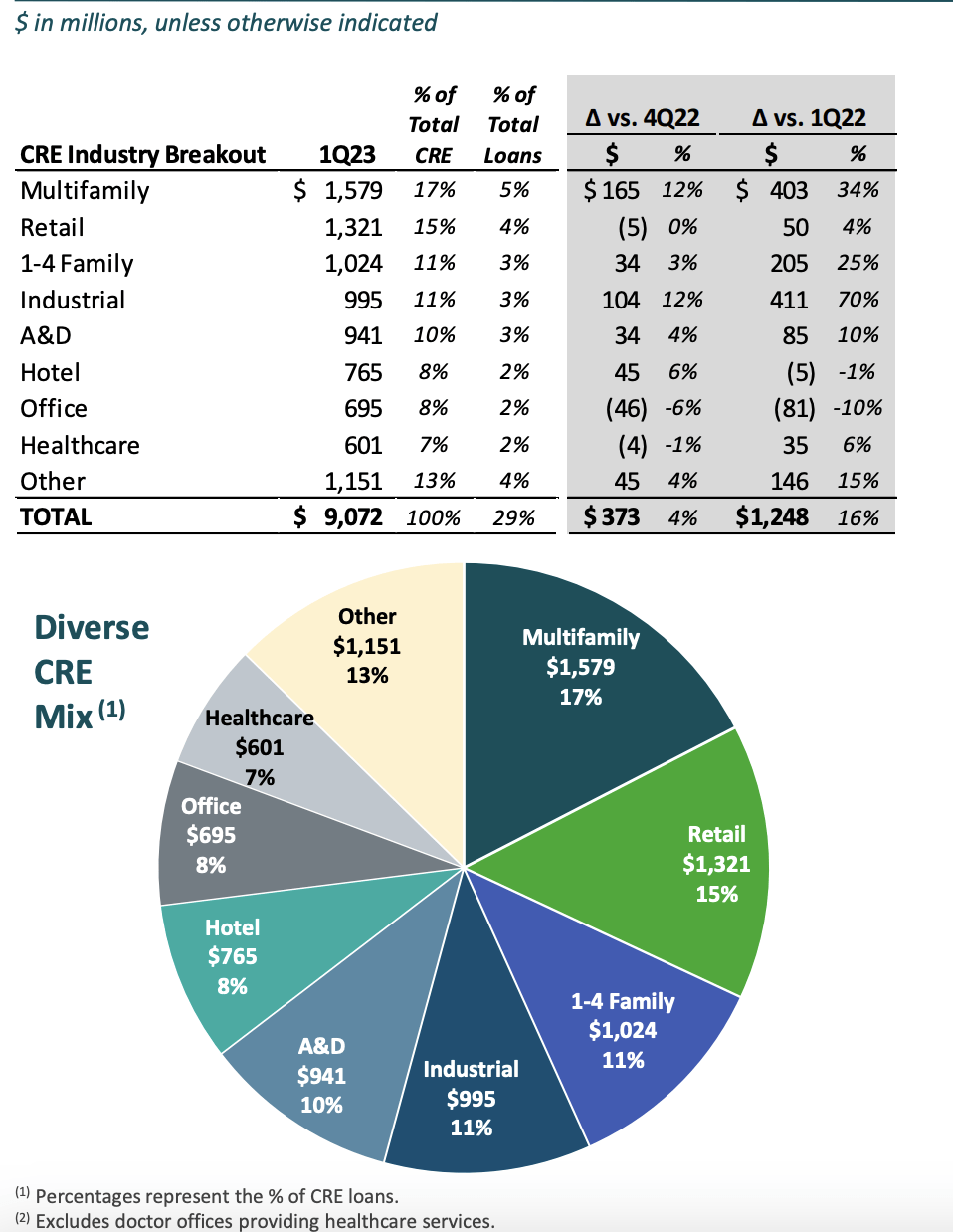

In addition to the commercial and industrial loans that the company gives out, it also has a rather sizable commercial real estate footprint. As of the end of the most recent quarter, about $9.1 billion of its loans, or 29% in all, are dedicated to commercial real estate. I understand that many investors at this time are concerned about office properties and the impact high occupancy rates and potential defaults could have on the banking sector. The good news is that only $695 million, or about 2%, of the loans on the company's books fall under this category. Its greatest exposure in the commercial real estate space is the multifamily sector, followed by the retail market. And finally, the remaining 28% of its loans fall under the consumer category, with the vast majority there involving residential mortgages.

{kind=link}

It is worth mentioning that, of its loan portfolio, 28% by value is in the form of fixed loans. 21% is in the form of floating loans that reprice every 30 days. And 51% of loans are variable by nature. This is pretty solid because it indicates that a rise in interest rates should be bullish for the company since it allows the enterprise to collect even more money from its customers in this environment. Of course, the downside to this is that a rise in interest rates increases the risk of default. But so far, that has not been much of an issue. As of the end of the most recent quarter only 0.33% of its loans were non-performing.

{kind=link}

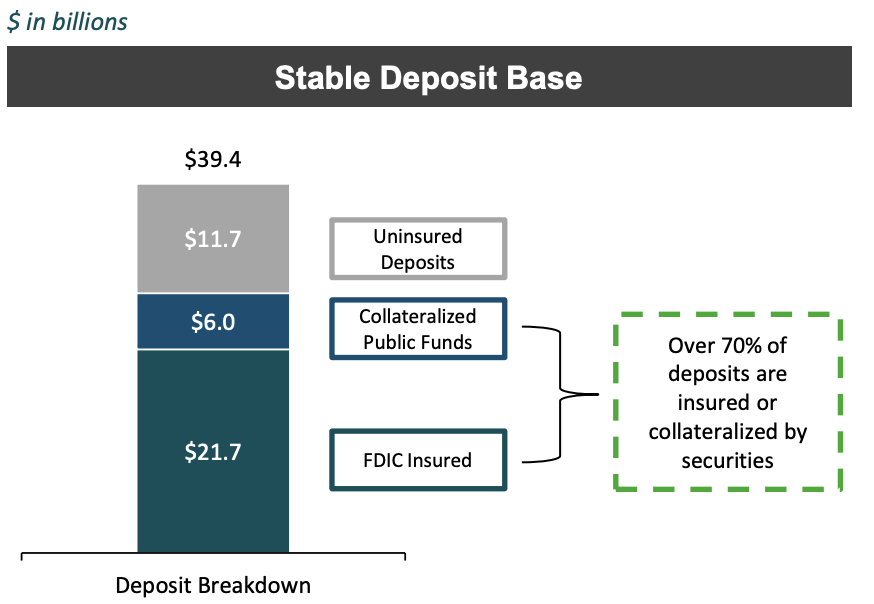

Even more important than the loan picture is the deposit picture. After all, it was the considerable fear that deposit outflows would drain certain banks that caused the crisis to begin with. The good news is that overall deposits for the company continued to grow from the end of 2022 through the first quarter of this year. They expanded from just under $39 billion to $39.4 billion. But not all deposits are equal. The real problem has been the amount of deposits that are uninsured. From the end of last year through the end of the first quarter of this year, this number did actually decrease. It fell from $19.4 billion to $17.7 billion. Though if we remove from this deposits that are collateralized, we would have seen it drop from about $12.5 billion to $11.7 billion. As of the end of the most recent quarter, 44.9% of the deposits on the company's books are uninsured. This is a fairly lofty amount. But again, if we remove those that are collateralized from the equation, it drops to a much more comfortable 28.9%.

{kind=link}

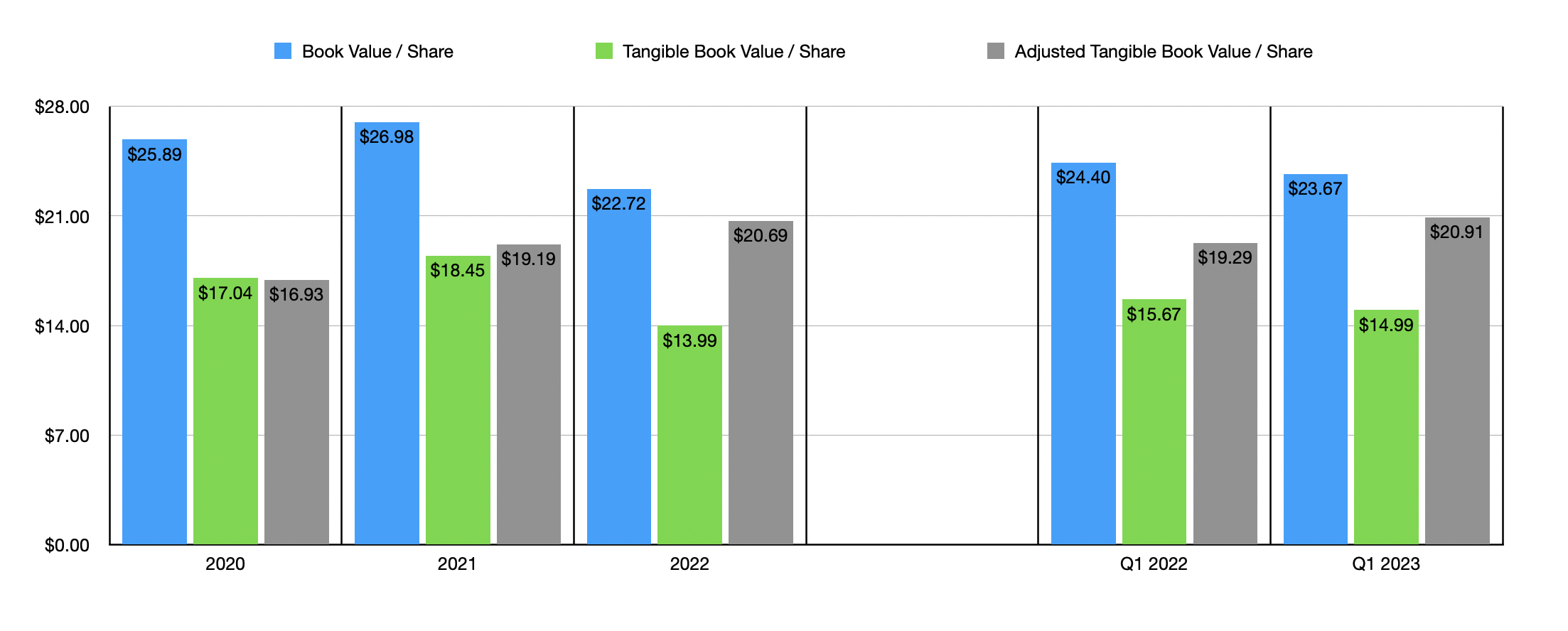

This makes the company look quite solid in the grand scheme of things. To make things even better, we have the fact that the adjusted tangible book value per share for the company also continues to grow. The same can be said of the overall book value per share. It increased from $22.72 to $23.67 in the course of a single quarter, while the adjusted tangible book value per share inched up from $20.69 to $20.91. To put this in perspective, shares today are priced at only $20.10. It is true that, on a non-adjusted basis, the tangible book value per share is lower at $14.99. But the difference between this and the adjusted number is the accumulated other comprehensive income that includes, amongst other things, fluctuations in the value of loans that are classified as available for sale.

{kind=link}

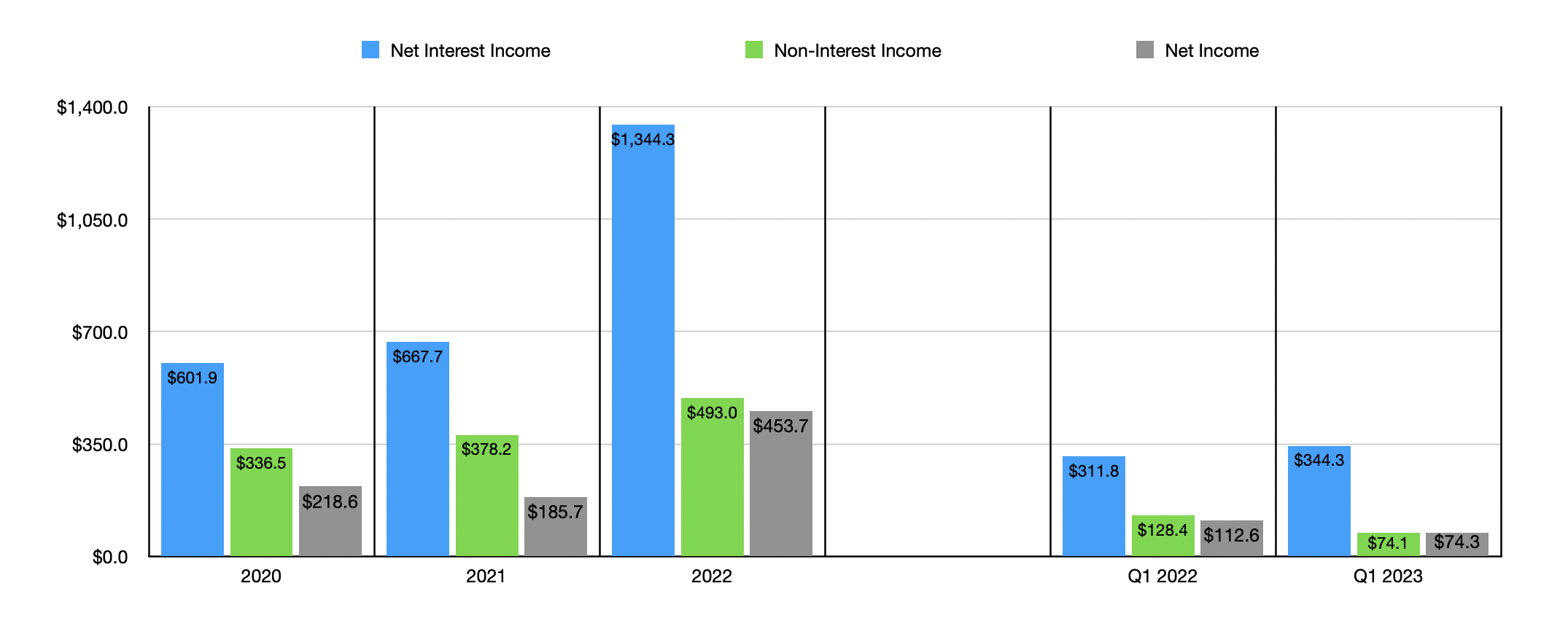

Over the past few years, management has done really good when it comes to the financial performance of the enterprise. Net interest income expanded from $601.9 million in 2020 to $1.34 billion in 2022. Again, much of this was driven by the aforementioned mergers. Non-interest income during this window of time expanded from $336.5 million to $493 million, while net income for the company grew from $218.6 million to $453.7 million. You can see, in the chart below, how revenue for the business continued to grow in the first quarter of 2023 compared to the same time last year. But we have seen a pullback when it comes to non-interest income and net profits. Non-interest expenses for the company managed to grow 9.5% year over year, driven by the increased size of the organization. In fact, this growth was slower than the 10.4% increase seen by net interest income. The real pain for the company on the bottom line, then, is largely associated with the fact that the firm booked a $51.3 million security loss compared to the $1.1 million loss reported one year earlier. Management attributed this to a $15.7 million decrease in revenue associated with its mortgage banking operations and to initiatives aimed at optimizing the firm's balance sheet. More likely than not, this should be considered a one-time event.

{kind=link}

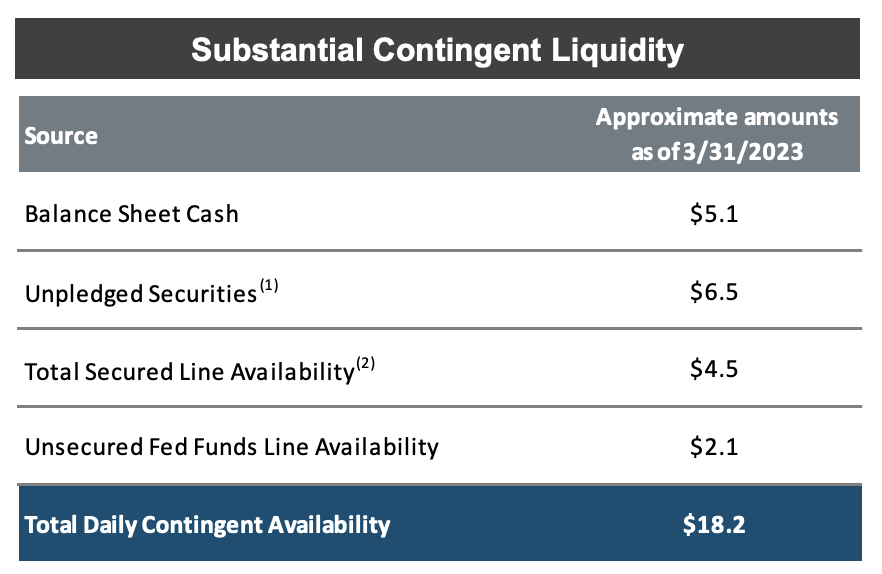

Besides the rough bottom line for the first quarter of 2023, the only negative that I see regarding the company involves its total borrowings. At the end of the most recent quarter, the company owed lenders nearly $6.2 billion. That was up from the $3.6 billion reported at the end of 2022. The good news is that the company has $18.2 billion worth of liquidity. Of this, $5.1 billion is in the form of balance sheet cash, while another $6.5 billion involves unpledged securities. So even though management may not want to part with some of the capital that's on its books, it would have the ability to reduce this debt rather quickly if need be.

{kind=link}

Takeaway

All things considered, I believe that Cadence Bank is a solid company. The enterprise has a stable deposit base and, when you factor collateralized deposits into the mix, its overall amount of uninsured deposits is reasonable. The company is trading around tangible book value and it is also trading at a price to earnings multiple, using data from 2022, of only 8.1. All of these things combined make me feel as though the firm should offer some decent upside potential. As such, I've decided to rate it a ‘buy’ at this time.

For further details see:

Cadence Bank: Another Regional Bank Worth Considering