CDRE - Cadre Holdings: An M&A Powerhouse Buy

2023-12-24 06:07:30 ET

Summary

- Cadre Holdings is a global provider of safety and survivability products for first responders and federal agencies.

- The company operates through various brands and has been expanding its business through M&A activity.

- Cadre Holdings has strong growth potential and is attractively valued, with a price target of $36.25 to $40.33.

I am continuously looking to expand coverage for aerospace and defense companies, and at times that leads me to covering companies that I would normally not cover and in some cases had never heard of before. The aim to provide the broadest aerospace and defense coverage available brings me to such a name: Cadre Holdings (CDRE).

The stock has a 1-year return of 57%, so I am quite sure that makes many investors - myself included - wish they would have found this name before. In this report, I will be discussing what Cadre Holdings business includes, assess the most recent earnings, the ranking Cadre Holdings has amongst peers and I will provide a stock price target using my own valuation tool.

What Does Cadre Holdings Do?

Cadre Holdings describes itself as follows:

Cadre Holdings is a premier global provider of trusted, innovative, high-quality safety and survivability products for first responders, federal agencies, and outdoor/personal protection markets. Cadre Holdings is a public company with corporate offices in Jacksonville, FL.

That might not directly ring a bell of the company’s activities, and that is not odd given how broad the product portfolio is. The company has a variety of brands in its portfolio providing anything from holsters to body armor to uniforms to firearms to lubricants for firearms to fingerprinting products to chemical lights.

Just to give you an idea how diverse the product portfolio is. Just looking at body armors, there is hard armor plates, concealable armor, soft armor and helmets. Soft armor can again be divided in subgroups such as ballistic armor, spike protection and multi-threat protection. So, chances are that armors or uniforms provided to military and first responders are manufactured by Cadre Holdings.

Cadre Keeps Expanding Its Business

What immediately becomes clear when taking a look at Cadre is the fact that it operates through various brands. It doesn’t operate a single brand, and that is the direct result of Cadre Holdings growing its business through M&A activity without unifying all brands under a single Cadre umbrella. Even at the time of writing, I received a news item in my inbox as Cadre Holdings acquired ICOR Technology, a manufacturer of EOD robots.

Cadre Holdings: A Top 10 Aerospace and Defense Pick

Cadre Holdings without doubt is a lot different from the typical aerospace and defense suppliers I usually cover. Cadre Holdings is not an aerospace company, but a defense company focused on first responders. The company ranks #10 in the Top Aerospace and Defense Stocks scoring 4.04 (Buy) in the Quant Rating , 4.50 (Strong Buy) amongst Seeking Alpha analysts and a 4.50 (Strong Buy) amongst Wall Street analysts , who have an average price target of $34 for the stock, a high price target of $40 and a low price target of $27.

Cadre Holdings: Strong Growth But Little Explanation on Growth Drivers

{kind=link}

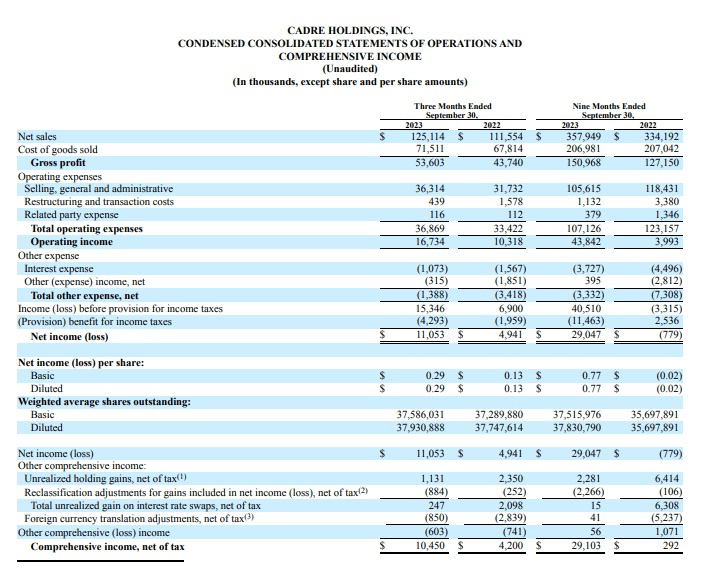

In the third quarter, Cadre Holdings posted $125.1 million in revenues. US State and local agencies accounted for 60% of the revenues, followed by 20% international exposure, 11% for US Federal agencies with the remainder accounted for by commercial and other parties. Year-over-year, revenues increased in 12.1% while gross profit increased 22.5% and operating income even jumped 62% to $16.7 million. Adjusted EBITDA grew from $20.7 million to $23.7 million. Having read the 10-Q filing, the management presentation and discussion of results as well as the company press release for the third quarter earnings, there is one thing that I am absolutely not thrilled about and that management did not even address drivers of growth. I would like to have seen how much of the growth was organic and where the strength and weaknesses are, but the company did not provide anything on that end, which is disappointing. It makes looking at results somewhat less useful, and I can’t comprehend why a company that has such a broad product portfolio and an M&A pipeline for growth does not do more to detail its results.

What we do know is that for the first nine months of the year, tactical soft armor sales were up 47% and on the consumer side there was 5% growth in duty gear sales. Perhaps, I am looking for way too much information than I should, but I find management comment to be extremely limited.

Cadre Holdings Grows More Positive On 2023 Earnings

{kind=link}

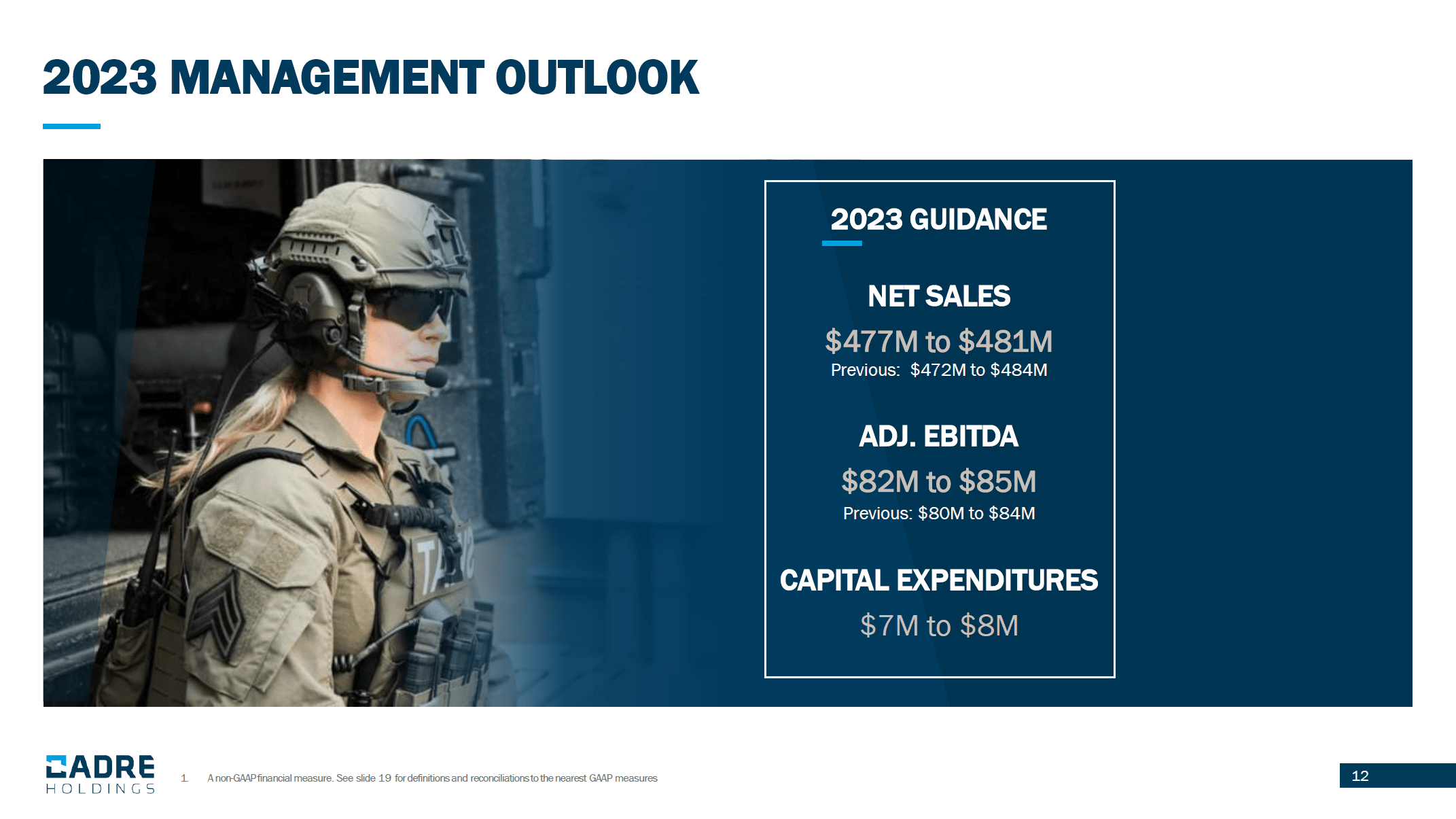

For 2023, Cadre Holdings is now expecting $477 million to $481 million in sales, which is a $3 million to $5 million improvement compared to the previous guidance and would indicate 5% sales growth at the midpoint. While Adjusted EBITDA is now guided in the $82 million to $85 million range up $1 million to $2 million providing 10% Adjusted EBITDA growth compared to 2022.

Overall, I would say that Cadre Holdings is not a high growth company in the sense that its existing brands and businesses are only able to generate 5% growth for the year, leaving the impression that for higher growth they are highly dependent on M&A for which the company like many others is experiencing some challenges regarding financing as lenders have increased lending standards.

Is Cadre Holdings Stock A Buy?

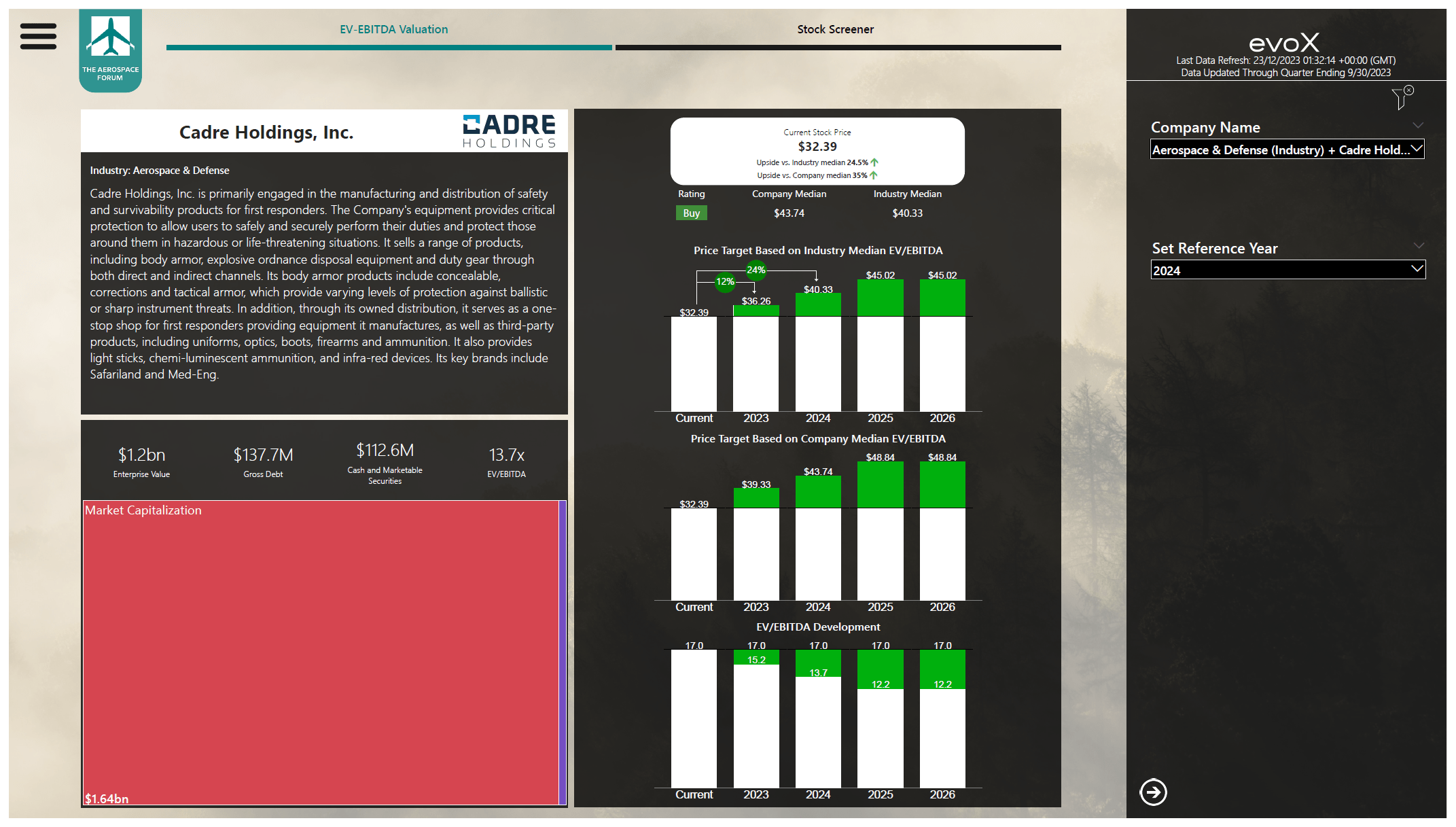

Stock price valuation for Cadre Holdings using evoX Stock Screener (The Aerospace Forum)

{kind=link}

When looking at the company’s scores, what caught my eye was that its valuation was rather steep from P/E perspective, and I would have expected that on EV/EBITDA valuation principles, this could have led to a soft rating. The contrary, however, is true. Valuing Cadre Holdings in line with industry peers, there is 12% upside for 2023 to $36.25 and 24% upside to $40.35 for 2024. So, I believe that the stock has some upside at current levels with a conservative price target of $36.25 and $40.33 at the high end more or less coinciding with the high end of the price targets set by Wall Street analysts.

Conclusion: Cadre Holdings Is Attractively Valued

Cadre Holdings still has upside with 2023 earnings in mind on an industry valuation basis, and also for 2024 there seems to be upside. The results provide a rather difficult basis for comparison as the M&A is important to the company’s growth, but the company does not provide a breakdown of organic and inorganic growth which I believe is very important to do as I want to see how much the company does depend on M&A to grow its results. For now, I am assigning a buy rating, but I do hope that management will better detail sources of growth in the future.

For further details see:

Cadre Holdings: An M&A Powerhouse Buy