CDRE - Cadre Holdings Is Gearing Up For The Offensive

2023-11-13 02:49:41 ET

Summary

- Cadre Holdings stock warrants a buy rating due to its solid fundamentals, growth potential, and capacity for additional acquisitions.

- The company is well-positioned to be a key supplier for global customers, increasing market share from large cap competitors.

- Growing international demand for protective equipment presents a significant opportunity for Cadre Holdings.

Investment Thesis

Cadre Holdings ( CDRE ) warrants a buy rating due to its solid fundamentals, growth potential, and capacity for additional acquisitions. While domestic law enforcement is expected to see only modest growth over the next 10 years, international demand for protective equipment is expected to see strong growth. The fundamentals of Cadre Holdings posture the company to be a key supplier for global customers, thereby increasing market share from even large cap competitors.

Company Overview and Primary Competitors

Cadre Holdings has been a leading provider of safety and survival equipment for first responders for the past 55 years . The company has multiple sub-brands and affiliates including Safariland, mostly focused on body armor and holsters, and Med-Eng, predominantly geared towards explosive ordnance disposal. Cadre is a small cap company with a market cap of just over $1B. The company held its initial public offering in November 2021.

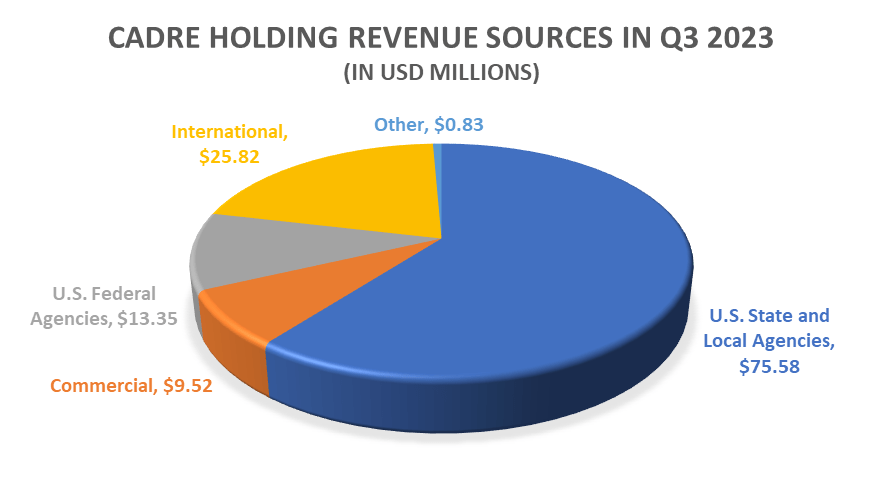

Cadre Holdings estimated that the annual market for its primary equipment consists of $870 million in body armor, $245 million in explosive ordnance disposal equipment, and $360 million in holsters. It also estimated that there are 9.7 million law enforcement personnel outside of the United States. The company’s latest Q3 2023 earnings demonstrated a total of $125.1 million in net sales. These sales comprise of U.S. state and local agencies (60.4%), international (20.6%), U.S. federal agencies (10.7%), commercial customers (7.6%), and other (0.7%).

{kind=link}

Importantly, CDRE’s international customer base is relatively small but growing. CDRE sells to 100 countries globally and its portion of international sales has grown from approximately 16% to over 20% over the past year. This is a major positive point for the company given international demand. I will cover more on the impact of growing international demand later.

Cadre Holdings Growth of International Sales

| Q4 2022 |

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| International Sales |

| $18.26M |

| $20.43M |

| $22.94M |

| $25.82M |

| Total Sales |

| $111.55M |

| $111.75M |

| $121.09M |

| $125.11M |

| International as Percentage of Total Sales |

| 16.4% |

| 18.3% |

| 18.9% |

| 20.6% |

Source: SEC filings

CDRE’s competitors that also focus on first responder safety and survival equipment are a mix of private and small publicly-traded companies. These include Point Blank Enterprises (private), Avon Protection ( OTCPK:AVNBF ), Central Lake Armor Express (private), and the Blackhawk Division of Vista Outdoor ( VSTO ). VSTO has a market cap of $1.44B and is similarly sized to CDRE. However, Visto saw negative YoY revenue growth over the past three quarters. Additionally, VSTO’s share price has been flat YTD.

Other large companies that have body armor and other supplies as a small portion of their business are Honeywell International ( HON ) and BAE Systems ( OTCPK:BAESY ). However, while these companies are both larger than CDRE, they are not expected to see strong growth in coming years. HON saw only 4.2% YoY revenue growth recently, 50% below its sector average. YTD, HON’s share price is -13%. Furthermore, its P/E GAAP ((TTM)) is 15% higher than its sector average. BAE Systems saw EPS diluted growth ((FWD)) of 4.1%, 56% lower than sector. Also, BAESY’s EBITDA growth ((FWD)) was only 2.87%, 69% lower than its sector.

Solid Fundamentals

The first reason why CDRE is a buy is due to its strong fundamental factors. In contrast to some of CDRE’s large peers that also produce body armor, the company has seen very positive results. In Q3 2023, CDRE saw $53.6 million in gross profit, a 22% increase YoY. Both state and local agencies as well as international segments of CDRE’s business have grown consistently in all quarters this year.

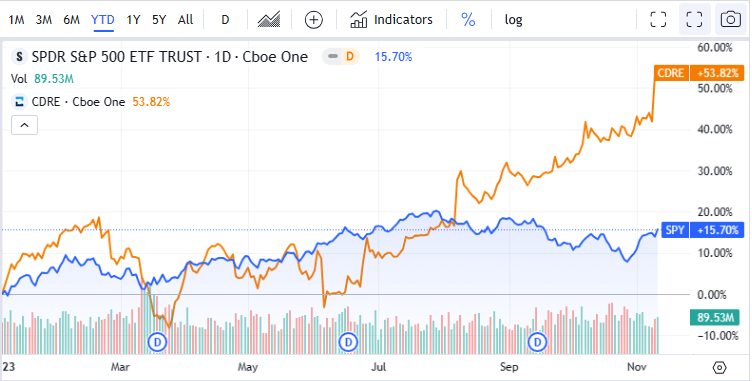

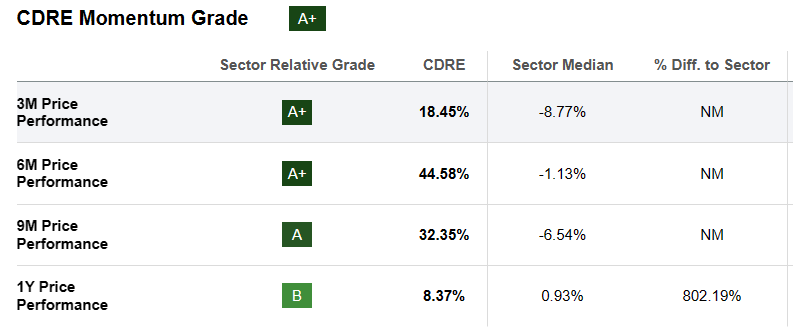

Furthermore, CDRE demonstrates strong profitability. CDRE saw net income in Q3 2023 of $11.1 million, a 123% YoY increase. Cadre also saw EPS growth of 123%. As a result of consistently strong performance, CDRE’s share price has risen over 50% YTD, compared to the S&P 500 index which has risen about 15% YTD.

{kind=link}

International Demand

The second key reason why CDRE is a buy is due to growing international demand. Domestically, police and detective personnel are expected to grow 3 percent from 2022 to 2032. The U.S. White House announced just earlier this month $334 million in funding for state and local governments to hire an estimated 1,700 additional law enforcement personnel, boosting this market segment. State and local agencies, an area of solid growth, represent the largest percentage of revenue for CDRE.

At the federal level, smaller growth is expected. The U.S. Federal Bureau of Investigation (FBI) is expected to increase less than 1% while the Department of Homeland Security ((DHS)) is expected to increase about 1.5% . While federal customers will require new equipment to replace aging supplies, the federal U.S. government is likely the smallest growth area.

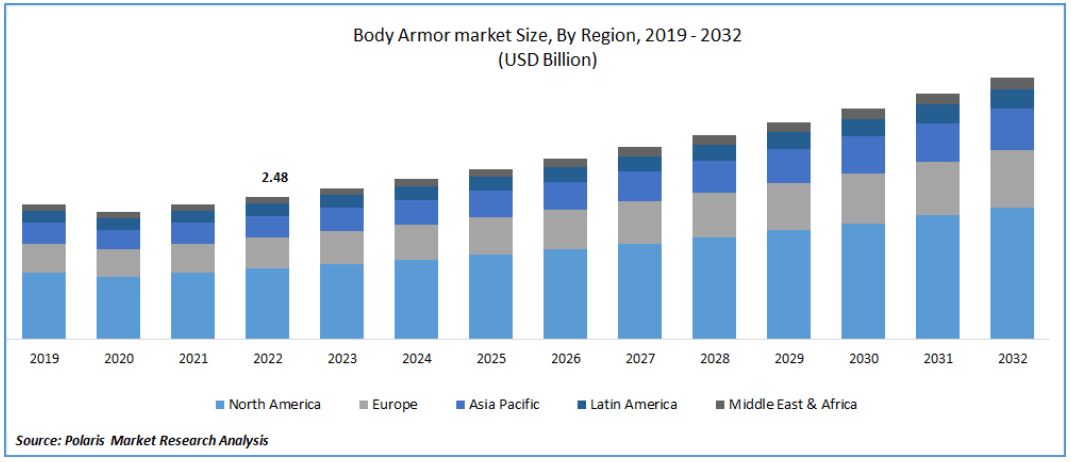

The shining point for demand is the international market. Internationally, body armor demand alone is expected to grow at a CAGR of 6.3% through 2032. This does not include holsters, helmets, and other explosive disposal equipment. CDRE already supplies 100 countries and has sales personnel internationally to keep this number rising. With conflicts in the Middle East and Eastern Europe, there are no shortage of crises to generate future customers.

International Demand Growth for Body Armor (Polaris Market Research)

{kind=link}

Growth Potential

The third reason for buying CDRE is due to its growth potential. Cadre Holding’s profit margin has been steadily increasing since Q2 ’22. The company achieved its highest FCF of $16M in Q3 2023. Furthermore, its cash growth was 91% YoY for Q3 2023.

Cadre Holdings announced just last month a dividend payout for the first time of $0.32 per share annually or a current yield of 1.04%. This dividend is sustainable with room for growth at a payout ratio of about 33%. Additionally, Cadre holds an assets-to-liabilities ratio of 1.8 and maintains low debt. Given the high cash flow and low dividend yield, CDRE is primed for additional growth.

Capacity for Additional Acquisitions

The fourth reason for a buy rating is due to its capacity for additional acquisitions. In 2021, Safariland LLC, a Cadre Holdings subsidiary, acquired Radar Leather Division . Radar Leather Division, based in Italy, develops high-quality holsters and expands CDRE’s footprint in Europe. Cadre Holdings also acquired Cyalume Technologies in May ’22 for $35M, adding chemical stick lights and electronic lights to its inventory. Because of its strong FCF, cash growth, and relatively low payout ratio for its dividend, CDRE has the capacity to acquire more companies. Given expected international demand, I believe the company will continue focusing on additional international acquisitions to streamline supply chains.

Valuation

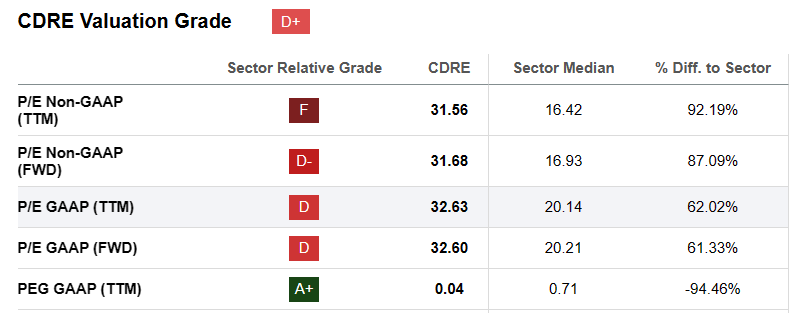

CDRE is currently trading at $30.81 at the time of writing this article, roughly at its all-time high price. This price is also around the target some analysts proposed back in August. Additionally, CDRE’s P/E GAAP ((FWD)) is 87% higher than its sector median. Therefore, I argue that the strong Q3 2023 earnings are mostly priced in already.

{kind=link}

While CDRE’s current price may not necessarily represent a value buy, the company’s potential for growth cannot be understated. CDRE saw a 53.8% YTD increase in share price and 27.2% CAGR since 2021. Therefore, it is reasonable to think given CDRE’s current pricing, an increase of another 20% could be seen in 2024, well surpassing its all-time high. This would represent a price target of $36.97. Pending any unexpected disruptions, CDRE will likely continue its momentum over the next year.

{kind=link}

Risks to Investors

In 2021, following the death of George Floyd in Minnesota, strong sentiments existed surrounding defunding police departments. While police budgets were reduced by an average 5.2% in 2021 for some U.S. cities, a recent study showed that this trend has since reversed. In 2022, 83% of cities examined had increased their police budgets since 2019. Furthermore, the study found that defunding never took place in many U.S. cities. While domestic and international demand for first responder equipment is expected to increase in coming years, political and anti-police sentiments are always possible. Any actions aimed at defunding law enforcement will likely result in a drop in share price for CDRE. Furthermore, budget deficits at the federal level will likely mean that increases to FBI, DHS, and other federal agencies that require CDRE’s products are unlikely.

Despite the risks above, global demand presents a strong case for investment in CDRE. Multiple conflicts in 2023 have demonstrated that there will unfortunately be a continued need for weapons-related protective equipment. A total of 79 countries witnessed increased level of conflict in 2023, ranging from Ukraine to Israel to Africa.

Concluding Remarks

Cadre Holdings represents a buy rating due to its solid fundamental metrics, capacity to satisfy international demand, and growth potential. While large cap companies exist that also supply of body armor and other protective equipment, Cadre Holdings is uniquely positioned as an international supplier due to its focus on the market segment and strong recent growth.

While federal demand is expected to remain relatively flat, state and local government as well as international demand is expected to grow considerably. Cadre Holdings already sells to 100 nations and is making acquisitions that expand its international market share. CDRE likely is already priced to account for its strong Q3 2023 earnings. Therefore, while not a value buy, its strong growth potential over coming years indicates that its performance will likely beat the market overall.

For further details see:

Cadre Holdings Is Gearing Up For The Offensive