CZR - Caesars Is Attractive As It Deleverages Its Balance Sheet

2023-11-15 21:20:58 ET

Summary

- Caesars Entertainment shares have underperformed but are now becoming interesting for investors.

- The company's Q3 earnings beat expectations, with revenue and adjusted EBITDA growth.

- With its free cash flow, Caesars can reduce debt and begin to reward shareholders with buybacks or dividends at the end of 2025.

Shares of Caesars Entertainment ( CZR ) have been a poor performer over the past year, losing about 13% of their value. They are also down over 60% from their post-COVID highs when there was significant optimism over the potential for sports betting, which has largely failed to materialize as a profit generator for the casino industry as a whole yet, given elevated promotional expense. This has combined with concerns over the durability of consumption, given the Federal Reserve’s tightening cycle. I do think shares are now beginning to get interesting though.

{kind=link}

In the company’s third quarter , Caesars earned $0.34, beating consensus by $0.09 as revenue rose by 3.4% to $3 billion. Casino revenue was up 1%, and hotel revenue up 2%. Alongside this revenue growth, the company generated adjusted EBITDA of $1.04 vs $1.01 billion last year, helping to boost free cash flow and continue the company’s journey to reduce its excessive debt load. The only major blemish was the 11% increase in food and beverage expense vs just an 8% increase in revenue, as higher wages and food prices reduced margins. If these results continue, the company is positioned to begin rewarding shareholders with either buybacks or a dividend around the end of 2025 in my view.

Caesars operates across three primary segments. First, Las Vegas revenues were up 4% to $1.12 billion as hotel occupancy rose 3% to 96.6%, which is about as good as it can be. If there is a travel slowdown, it is not appearing yet in Vegas. Adjusted EBITDA was up a more modest 0.4% as EBITDA margins declined to 43% from 44.6%. Increased wages, which was evidenced in food & beverage, reduced margins. There has also been construction around its property on the strip reducing non-hotel, walk-in casino customers.

Beyond Vegas, Caesars operates casinos around the country, owning 25 properties outright and leasing a further 22 in total. Regional revenues rose 2.3% to $1.57 billion with adjusted EBITDA up just 0.9%. Management sees “stable” guest demand here, except in areas like Chicago where new properties have added competition. As a consequence, margins were down by 60bp to 36.7% as that increased competition reduced table game drop by about 0.5% from last year.

Finally, digital revenue was up just 1.4%, which seems light given this is supposed to be the growth engine for the company and industry. There are a few things going on here. Sports betting actually rose by $291 million to $2.32 billion, over 14%, which is a pretty robust outcome. That growth was offset by the fact that Caesars’ hold declined from 7.9% to 6.5%. By definition, gambling margins are going to have some volatility month to month and quarter to quarter. Colorado football’s surprising wins earlier in the college football season in particular were a negative for industry sportsbooks.

Caesars targets a 7.5-8% over time, which it continues to believe is achievable by 2025. Over the past year, its hold has run closer to 5.5%, with a lower hold functioning in part like a promotional tool to sign up more users, akin to how auto companies may offer below market financing rates to support car sales. CZR has also pulled back some of its promotional spending as its gained scale, with operations now in thirty states. As a consequence, digital generated $2 million of adjusted EBITDA in Q3, up from a $38 million loss last year. Still, there was a net income loss of $29 million, though this was halved from last year’s $63 million loss.

Management is targeting $5 billion in EBITDA by 2025, or nearly $850 million above its current level, with $500 million coming from digital. By increasing its hold to 7.5% across digital, CZR can generate $200-250 million incremental EBITDA off of its current customer base. Holding expenses constant, which means CZR will need to increase gaming by about 10-15% from current levels to achieve the remaining $250 million. This is not an unreasonable growth rate in my view, at just 6% per year for a relatively new product.

There is also the potential to expand beyond 30 states with much of the South yet to legalize online sports betting. Florida, Texas, and California remain the three primary opportunities with Florida’s effort to give the Seminole Tribe exclusive rights, leading to legal challenges. If one of these big three states opens to Caesars, we will likely see EBITDA deteriorate from the digital operation as CZR ramps up promo activity to win those customers. In the long run, given the substantial boost to the potential betting population, this would be a significant positive. In other words, if these states legalize, I expect 2025 EBITDA to come in below $500 million, but long run EBITDA to be higher.

Thanks to these solid results and rationalized spending, CZR has generated about $570 million in free cash flow this year, excluding working capital movements, up from just $100 million last year. CZR is using this cash to boost its balance sheet with net debt down $400 million to $11.6 billion. Its net debt to EBITDA leverage is 3.9x. By falling below 4x, it saves 25bp in interest on its credit facility. Despite lower debt levels, there has been 2% increase in interest expense to $581 million. This is because Caesars carries $3.2 billion of floating rate debt. As the Fed raised rates, this increased the company’s interest burden. With the rate hiking cycle largely, if not completely finished, this headwind should be fully in the results.

Importantly, the company does not have its next bond maturities until 2025. This means it does not have to immediately refinance debt in today’s higher interest rate world. These bonds have an average yield of about 6.125%, so if this rate environment persists, its interest rate may rise somewhat, but in a manageable way. We are also likely to see the company use free cash flow to pay down these maturities, rather than refinance existing debt in its entirety.

At today’s business level, the company is generating about $700-800 million in free cash flow. If it can achieve its $5 billion target, free cash flow would be closer to $1.4 billion. Given the obligations on its leased properties and the cyclicality of its business, CZR wants debt to EBITDA closer to 2x before allocating capital to shareholders. At its current $4.1 billion EBITDA level, CZR could carry about $8.2 billion in debt, so that $3.4 billion reduction could take four years, too far away for the stock to rally much, in all likelihood.

At a $5 billion run-rate, debt can be $10 billion; if this ramp occurs by the end of 2025, CZR will generate $2.1-$2.5 billion in free cash flow during this period, meaning debt reduction will be at a point by the middle 2025 where it can start to focus on rewarding equity holders as it only needs to reduce debt by $1.6 billion.

Given the above discussion on a normalized hold in digital driving such gains, I view that $500 million in EBITDA gains as credible. That means its physical footprint needs to boost EBITDA by $380 million or about 4.5%/year. Right now, the company is seeing flattish demand relative to last year from consumers, so there needs to be some acceleration.

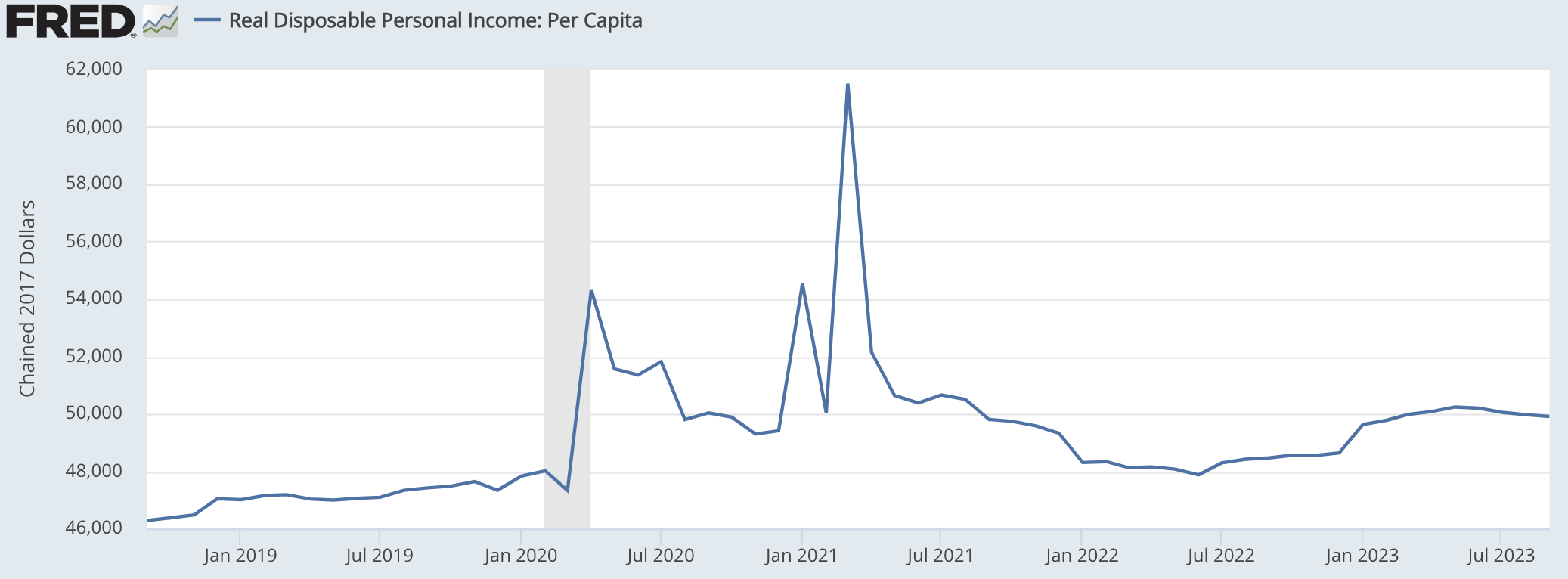

I think this is driven by the fact that real per capital disposable income has essentially been flat this year, as inflation has converged towards wages. Disposable income is higher than last year though, as energy prices have come down. If we see disposable income continue to rise, implying the Fed can bring down inflation further without causing a large rise in unemployment, this revenue growth could occur.

{kind=link}

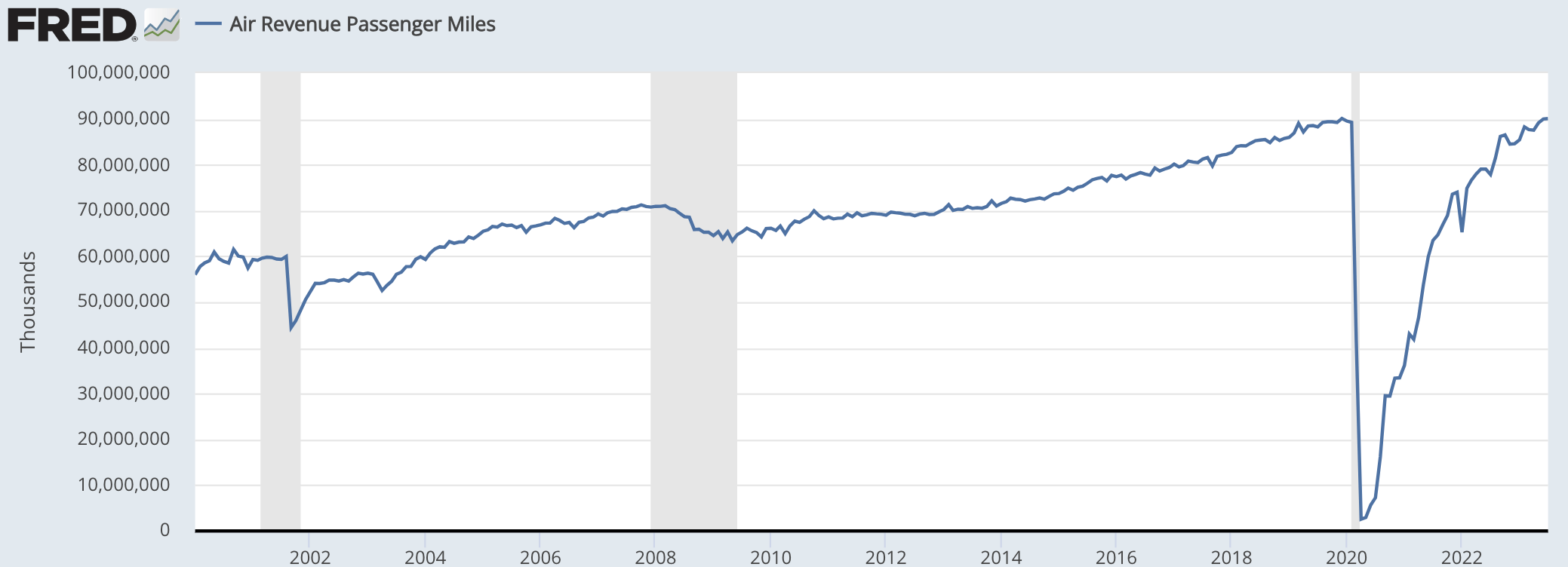

I also think it is important to emphasize that despite all of the discussion around how much travel boomed since COVID, travel activity does not seem inordinate. For example, air travel is only back to where it was pre-COVID. However, it had been growing steadily prior, given an increasing population in the country. To only get back to where it was four years later means air travel is still about 5% below trend. We may never get fully back to the past trend, but this does not indicate unsustainable levels of travel today.

{kind=link}

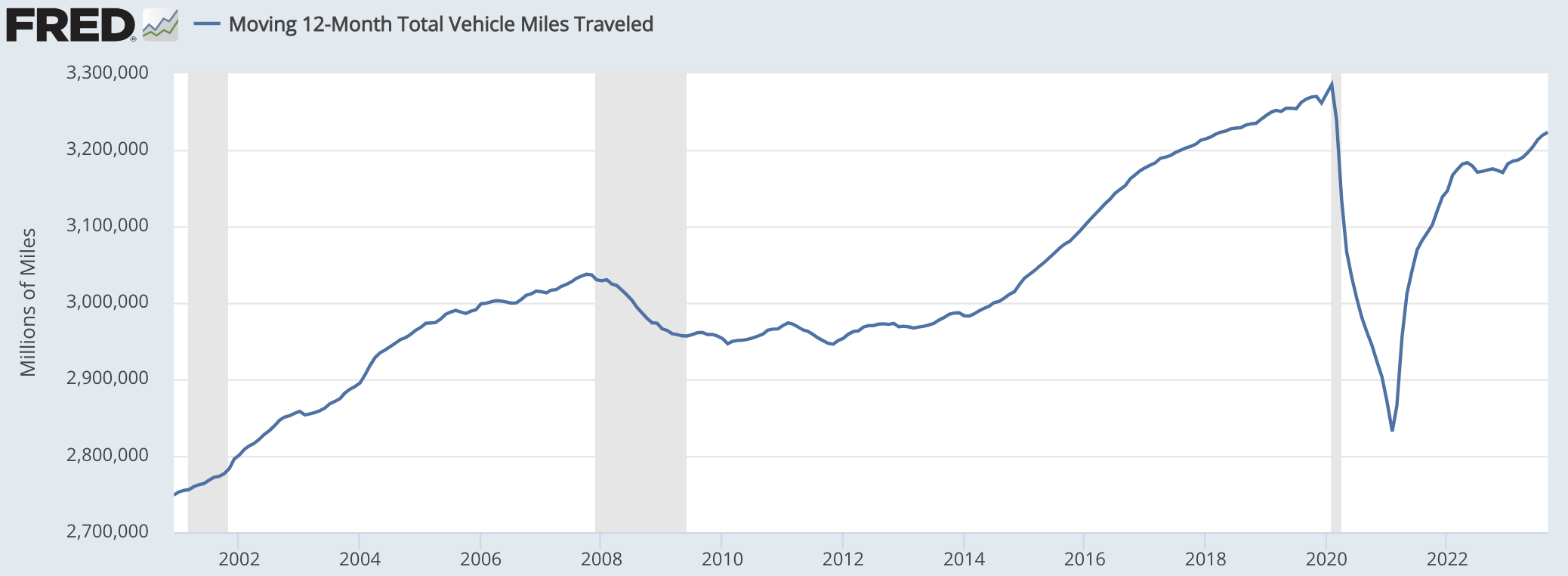

Similarly, auto travel is still well below pre-COVID levels. Now with many people now working remotely or in a hybrid setting, there may be less commuting going on than in the past. So, this is likely an indicator that never fully recovers. When I combine the fact though that air travel is below trend with that fact vehicle miles are below pre-COVID levels, I do not feel the current level of travel and associated discretionary spending is unsustainable.

{kind=link}

These are all arguments for why casino-related activity does not need to decline. That said, with company revenue up just 3% over the past year, I do think assuming 4.5% growth through 2025 is ambitious, given the economic backdrop probably is not going to improve, unless one expects unemployment to fall below 3%. To be conservative, I am going to assume no incremental growth from its physical operations, rather that they sustain current cash flow generation, while assuming the growth in digital occurs as that is more tied to reduce promo activity than economic growth.

That will leave Caesars with about $4.65 billion in 2025 EBITDA, leaving it with about $9.3 billion in debt capacity and $2.3 billion in needed debt reduction. With this level of EBITDA, over the next nine quarters (i.e. through year end 2025), CZR will generate about $1.9-$2.2 billion of free cash flow, getting right to the edge of that threshold. That leaves the company positioned to announce a capital return program by the end of 2025.

With about $1.15 billion in run-rate free cash flow, this program can be quite significant. Assuming an 8% free cash flow yield to reflect the cyclical nature of the business and low growth profile of its assets, shares would be worth $67 at the end of 2025, for a two-year return of 45%, or a 20% annualized return. With this return potential, I think patient investors will be reward for starting to accumulate positions in CZR today, and as capital returns move closer in sight, I expect to see the stock move meaningfully higher, into the mid-$50s in a year and about $67 in two years.

For further details see:

Caesars Is Attractive As It Deleverages Its Balance Sheet