CSTE - Caesarstone: Healthy Prospects At A Cheap Valuation

2023-03-16 12:02:01 ET

Summary

- Caesarstone’s revenue in 2023 should be impacted due to volume declines, partially offset by the carryforward pricing.

- I believe the company's profitability, which has been declining in recent years, should begin to improve.

- Based on my DCF calculations and relative valuation, the stock is undervalued.

Investment Thesis

Caesarstone ( CSTE ) should continue to experience weak demand in the residential market, which should impact revenues in 2023. Despite these challenges, the company's margins, which have been in decline in recent years, should improve in 2023 and beyond. The margins should benefit from several cost-saving measures, such as reducing headcounts, managing SG&A costs, and automating processes through technology. Additionally, the company is adjusting its production levels to meet the current demand environment, which should improve productivity.

The company's focus on cost-saving measures and improving margins, along with its strong brand reputation and quality products, should help drive future growth and enhance shareholder value. Therefore, I believe that CSTE is a good buy for investors looking to invest in a high-quality, undervalued company with growth potential.

Top-line analysis and outlook

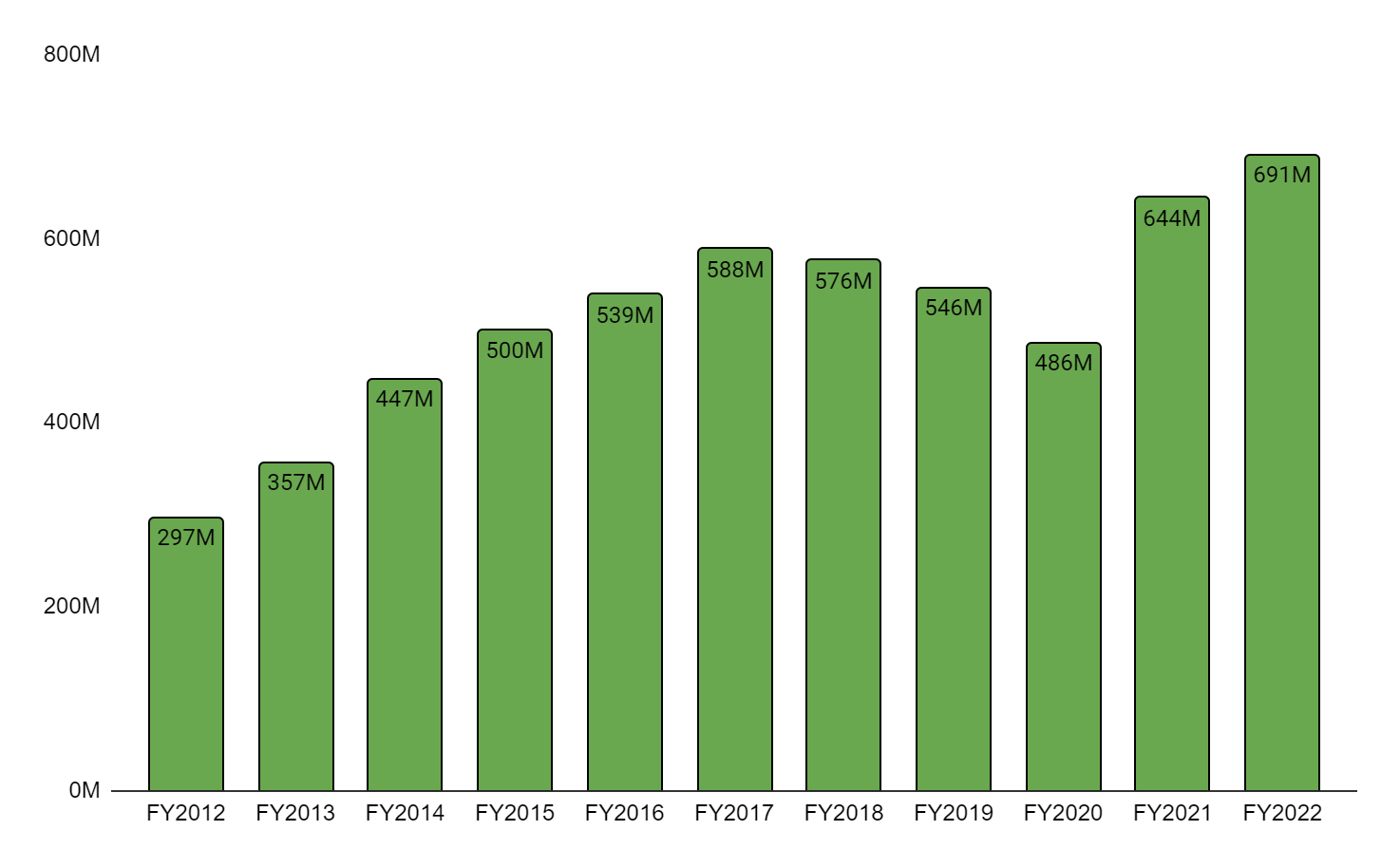

Caesarstone’s revenue growth chart (Created by DzD Analysis by taking data from CSTE)

{kind=link}

CSTE experienced healthy demand for its products in 2021 and the first half of 2022 due to the strong residential and commercial markets. However, the demand environment started to weaken in the second half of 2022 due to rising interest rates, pressured housing starts, and higher remodeling expenses. This impacted the company’s sales in Q3 and Q4 of 2022, particularly its U.S. and Israeli businesses. Consequently, there has been a reduction in inventory levels at the company's channel partners, which has resulted in a decline in volumes. Despite these challenges, CSTE's revenue grew by 7.3% YoY in 2022, supported by price increases and the strong demand witnessed in the first half of the year, offset by negative FX translation effects.

As we look ahead to 2023, CSTE is likely to continue benefiting from the pricing actions taken in 2022 as well as the recent price increase. The company has already implemented an annual price increase of low single digits in February 2023 to counter some of the inflationary pressures. However, despite these measures, the declining demand is likely to have an adverse effect on the company's volumes, which would partly offset the positive impact of pricing. Nevertheless, Caesarstone's strong position in the repair and remodel market, which accounts for 60-70% of its revenue, should provide some stability and cushion against the volatility of the new construction market.

Profitability

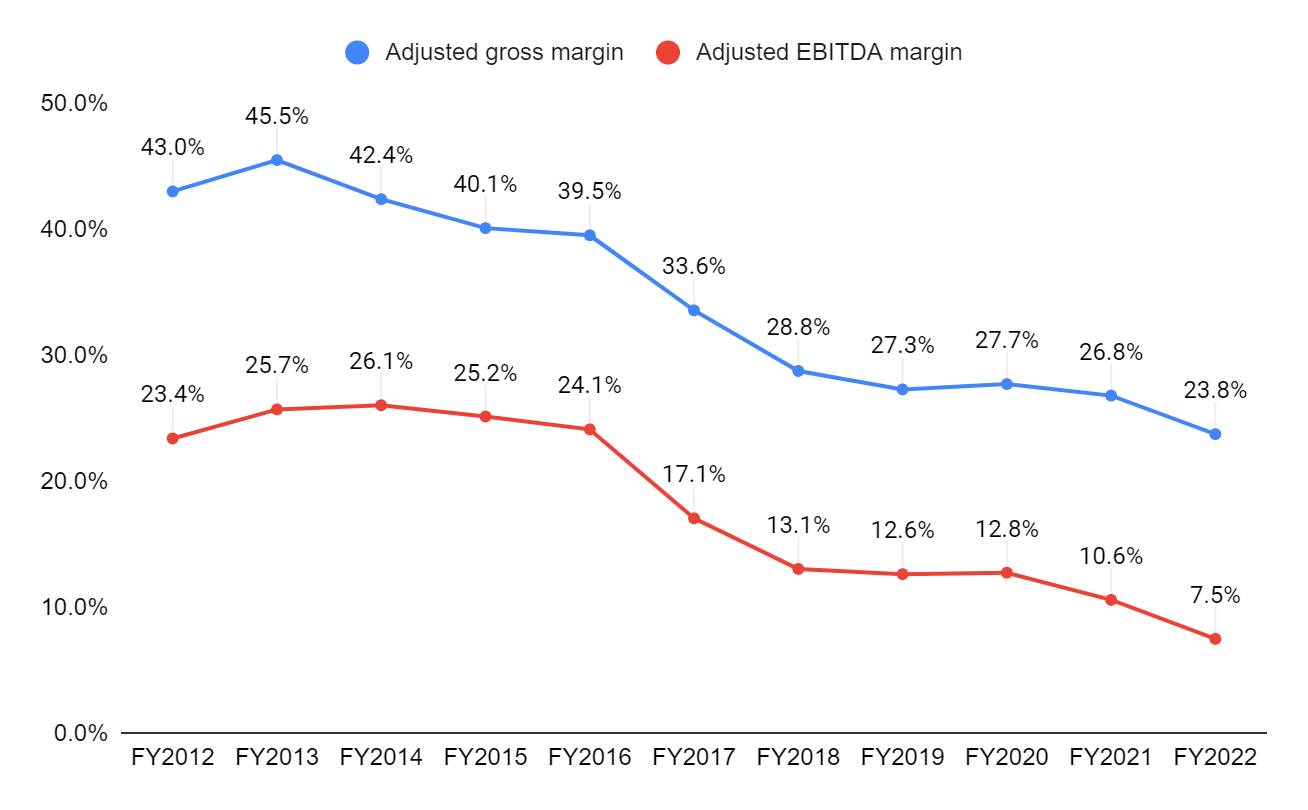

CSTE’s adjusted gross margin and adjusted EBITDA margin (Created by DzD Analysis by taking data from CSTE)

{kind=link}

CSTE's margins have been under pressure since 2016, primarily due to production issues and rising raw material costs. In 2022, the margin decline continued, driven by a combination of lower volumes and increased raw material costs. Specifically, the adjusted gross margin fell by 300 basis points YoY to 23.8%, mainly due to lower fixed cost absorption (270 bps), higher raw material prices (250 bps), unfavorable foreign currency exchange rates (300 bps), and increased shipping prices (210 bps). However, the decline was partly offset by a favorable product mix and higher selling prices (700 bps). Similarly, the adjusted EBITDA margin declined by 310 basis points YoY to 7.5%, driven by the lower gross margin.

In 2023, CSTE is taking several steps to improve its profitability. The company is adjusting its production levels and SKU mix to align with the current demand environment, which should help to improve its margins. Additionally, CSTE is reducing its headcount globally, closely monitoring SG&A costs, investing in technology, and evaluating its supply chain to identify areas for improvement. The company has already successfully reduced its headcount by 9% in the second half of 2022. CSTE is also investing in technology through its innovative CS Connect platform, which is designed to enhance customer engagement and improve the overall customer experience. Furthermore, the company is reinvesting some of the savings from its headcount and working capital reductions in marketing initiatives and expanding its distribution footprint in promising markets.

CSTE has also been expanding its relationships with OEM manufacturers in Asia, which has increased the proportion of its products produced in low-cost countries. This should help to improve its margins in the long term. Overall, I believe that the company's margins in 2023 should improve as a result of the pricing initiatives, lower headcounts, optimization of manufacturing facilities, and reduction in SG&A costs. The margins should also benefit from the gradual decrease in higher raw material costs and shipping costs throughout the year.

CSTE under the new leadership

Caesarstone recently announced the appointment of Yosef Shiran as its new CEO. Mr. Shiran is no stranger to the company, having served as its CEO from 2009 to 2016, during which time Caesarstone experienced remarkable revenue growth and increased margins. However, the company's growth rate has been stagnant, and margins have declined in recent years. With Mr. Shiran returning to lead the company, there is great optimism that Caesarstone will once again achieve its previous levels of profitability and experience healthy growth. His deep understanding of the industry and proven leadership skills should have a significant positive impact on the company's future success.

Balance Sheet and Cash flow Analysis

At the end of 2022, CSTE had a healthy cash position, with cash and cash equivalents amounting to $74.3 million, and a total current asset value of $408.5 million. The company's current liabilities at the end of its fiscal year 2022 were $183.3 million, indicating that it has adequate liquidity to meet its near-term liabilities. Additionally, CSTE's balance sheet shows that it does not have a significant amount of debt, providing it with flexibility and the opportunity for mergers and acquisitions (M&As) to expand its business.

Balance sheet data (10-K)

Balance sheet data (10-K)

Risks to my thesis

I am assuming that the strong carryforward pricing should partially offset the impact of volume declines on revenue. However, if the volume decline is more than anticipated, the revenue decline in 2023 should be mid single digit. This should offset the benefits of cost-saving actions, impacting margins in the fiscal year 2023.

Valuation

WACC Calculation (Created by DzD Analysis using Alpha Spread)

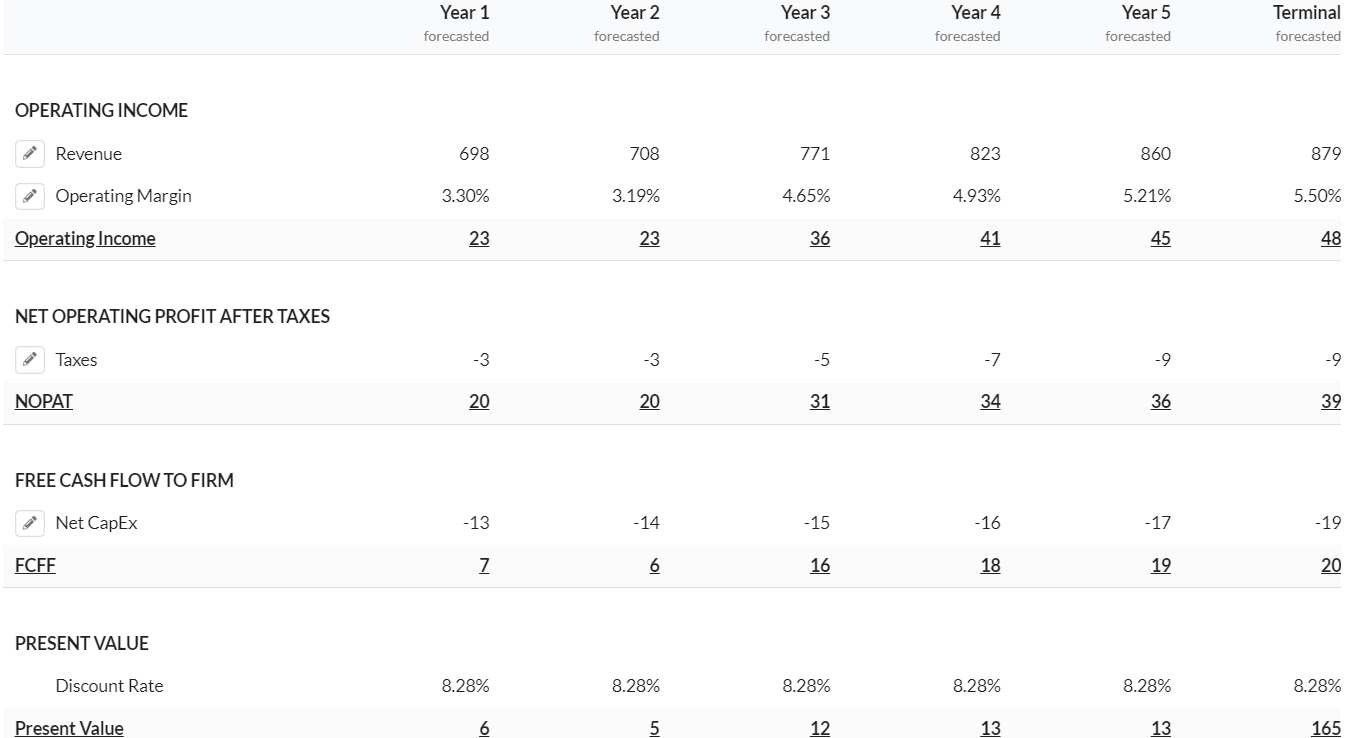

DCF Calculation (Created by DzD Analysis using Alpha Spread)

{kind=link}

I arrived at the conclusion that Caesarstone is currently undervalued by conducting a DCF analysis and using the relative valuation. In my DCF analysis, I assumed revenue would be slightly negative in 2023 due to the weak residential demand, partially offset by pricing initiatives, and should grow in the mid-single digits beyond 2023. I believe that the operating margins should continue to improve due to the company’s cost-saving initiatives discussed in the profitability section. The capital expenditure should increase in the coming years as the company invests in technology. I used a discount rate of 8.28% by using the cost of equity of 8.47%, which is below the industry level of 11.47%, and arrived at a fair value of $7.88 for CSTE.

Using the relative valuation, the stock is currently trading at 10.28x FY23 consensus EPS estimate of $0.46 and 7.69x FY24 consensus EPS estimate of $0.62, which is at a significant discount to its five-year average forward P/E of 22.77x.

Conclusion

Overall, I believe the company’s revenue in 2023 should be slightly impacted by declining volumes due to lower demand. CSTE’s profitability, which has been declining over the last few years, should improve given the cost-saving initiatives. This includes headcount reductions, managing SG&A costs, investing in marketing and technology, and adjusting its production levels to meet the current demand. Additionally, CSTE has rehired its former CEO, Yosef Shiran, who was in charge from 2009 to 2016. The company had performed well in the past, and I believe it should be able to regain its profitability under the new leadership. Hence, I am optimistic about CSTE's growth prospects.

For further details see:

Caesarstone: Healthy Prospects At A Cheap Valuation