MGDPF - Calibre Mining: Adding Marathon's Tier-1 Jurisdiction Ounces At An Attractive Price

2023-12-07 10:00:00 ET

Summary

- Calibre's announced its proposal to acquire Marathon Gold last month for ~$250 million in an all-share deal.

- The acquisition (if succesful) would turn Calibre into a ~500,000-ounce producer and reduce its overall risk with less of its NAV and annual cash flow generation tied to Nicaragua.

- In this update we'll look at the deal in a little more detail, what it means for Calibre & how the price paid stacks up relative to past deals.

While it's been a quieter year than some might have hoped for M&A among gold developers given the rising gold price against a backdrop valuation extremes (valuations at the lowest levels in years for some names), the trend of M&A has continued with a new deal announced in mid Q4. This was the proposed acquisition of Marathon Gold ( OTCQX:MGDPF ) by Calibre Mining ( OTCQX:CXBMF ) for a ~$250 million price tag based on 0.6164 Calibre shares per share of Marathon or an implied value of US$0.61. Overall, the deal is a brilliant move by Calibre and it will go down as one of the most counter-cyclical deals of the past decade in the sector if successful, with it being a win for multiple reasons that include:

1. a re-rate opportunity given the increased scale (~500,000 ounces), improved margins (~$1,200/oz AISC), transition to being a tri-asset producer, plus meaningful growth in total net asset value and free cash flow generation.

2. a lower-risk investment thesis for Calibre investors without the bulk of NAV/cash flow tied to Nicaragua

3. a significant growth in resources and NAV per share given the attractive price being paid for Marathon because of Calibre's patience

In this update we'll look at the deal in a little more detail, what it means for Calibre if successful, and how the price paid stacks up relative to other Tier-1 jurisdiction acquisitions:

Marathon Gold Mining - Company Presentation

{kind=link}

All figures are in United States Dollars.

Calibre Acquiring Marathon Gold

Just over three weeks ago, Calibre announced that it would be acquiring Marathon Gold in an all-share deal valued at ~$250 million or US$0.61, with Calibre also agreeing to purchase ~66.7 million shares at US$0.45 to give it ~14% ownership following the closing of the concurrent private placement. Calibre's major shareholder B2Gold ( BTG ) has entered into a voting support agreement to vote their shares in favor of the deal, and with nearly 30% locked up, this looks like a done deal unless another suitor comes in over the top (but historically bidding wars have been rare, even in Tier-1 jurisdictions).

So, why Marathon?

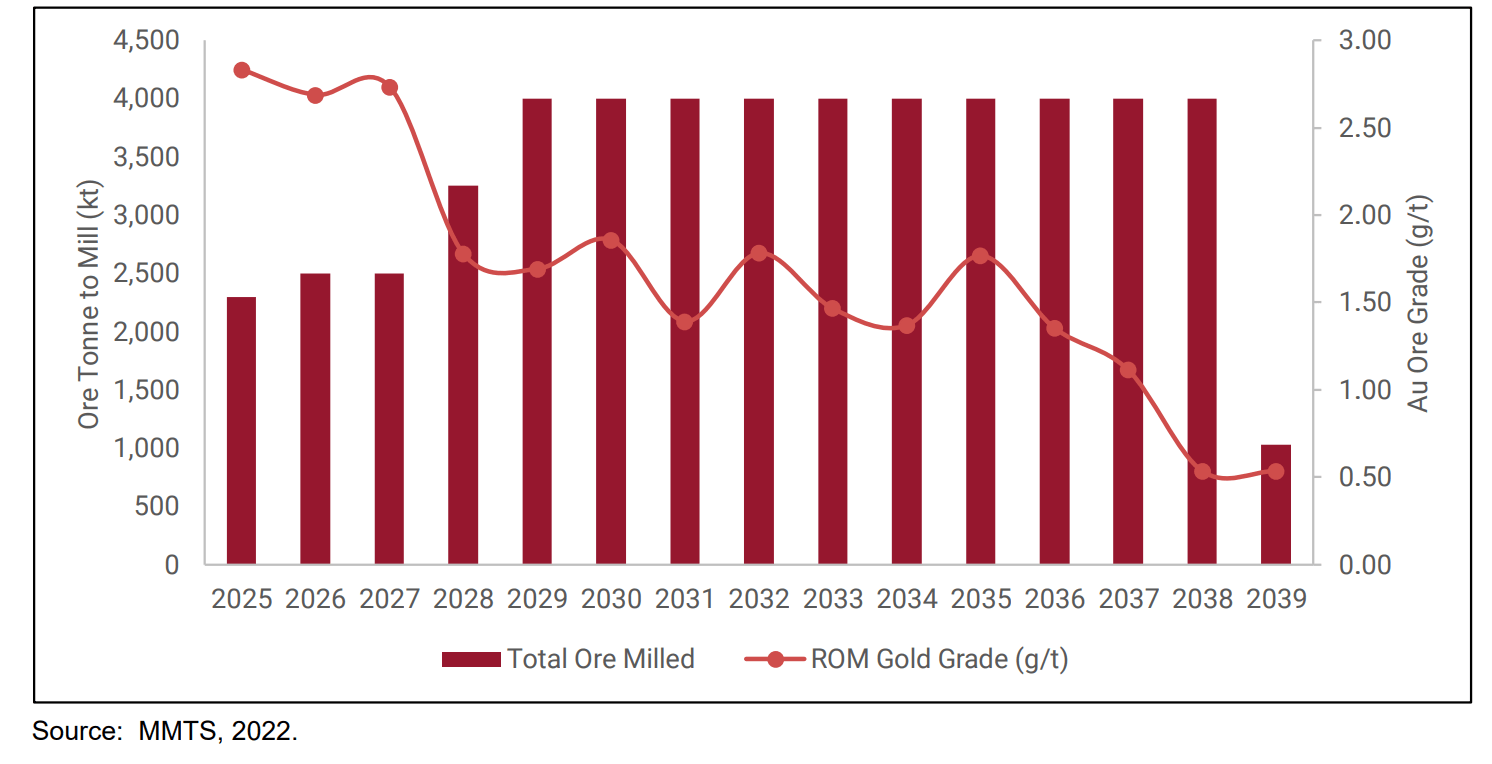

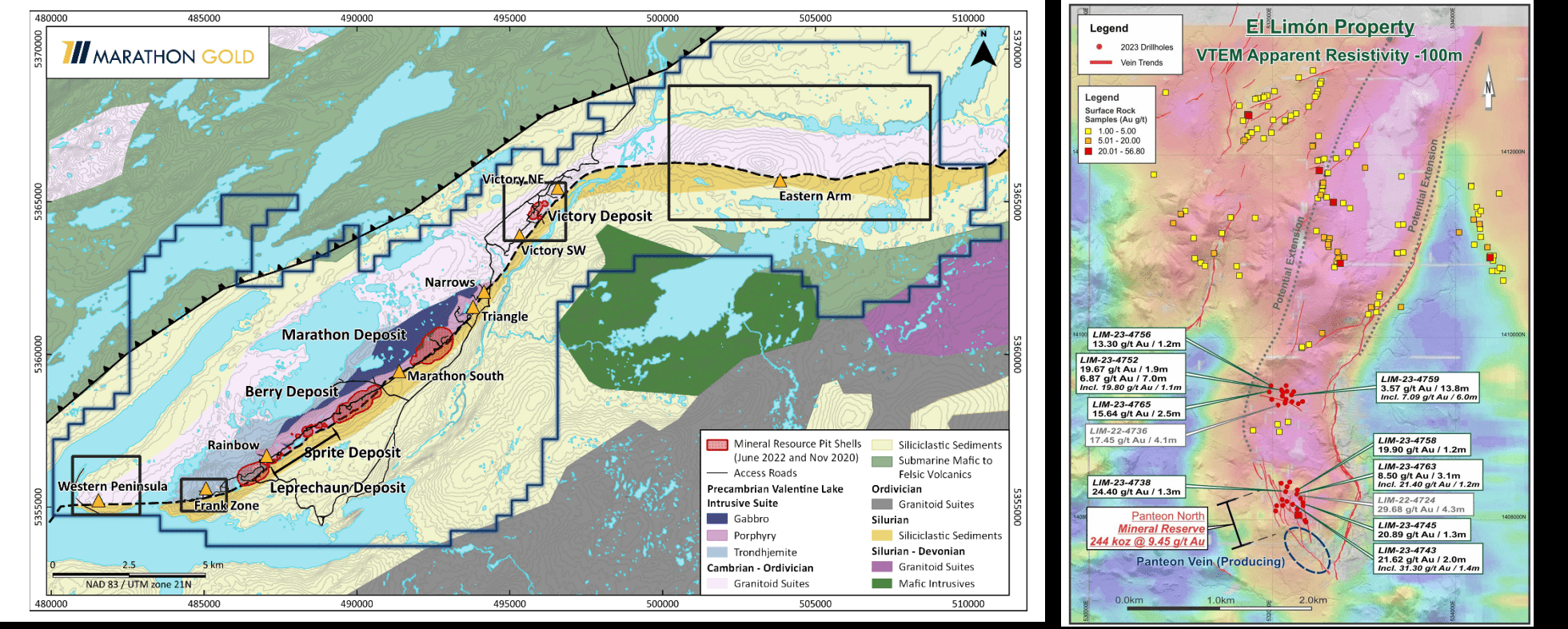

As highlighted in past updates, Marathon's Valentine Gold Project is one of the best undeveloped gold projects in North America not held by a major, capable of producing just shy of 200,000 ounces in its first five years at sub $1,100/oz all-in sustaining costs (adjusted for inflationary pressures). These costs would be ~20% below the industry average of ~$1,400/oz (2024 estimates), and this would be one of the 15 largest gold mines in production in its first ten years of production [similar size to Young-Davidson, Lamaque, and Musselwhite, and similar to Equinox's ( EQX ) 50% share of Greenstone]. As for Valentine, it's a relatively simple above-average grade (for Canada) open-pit project (three pits which include Marathon, Leprechaun, and Berry) in Newfoundland that's expected to process ~4.0 million tonnes per annum at an average grade of 1.62 grams per tonne of gold with 95% recovery rates.

Valentine Gold Throughput & Grade - 2022 TR

{kind=link}

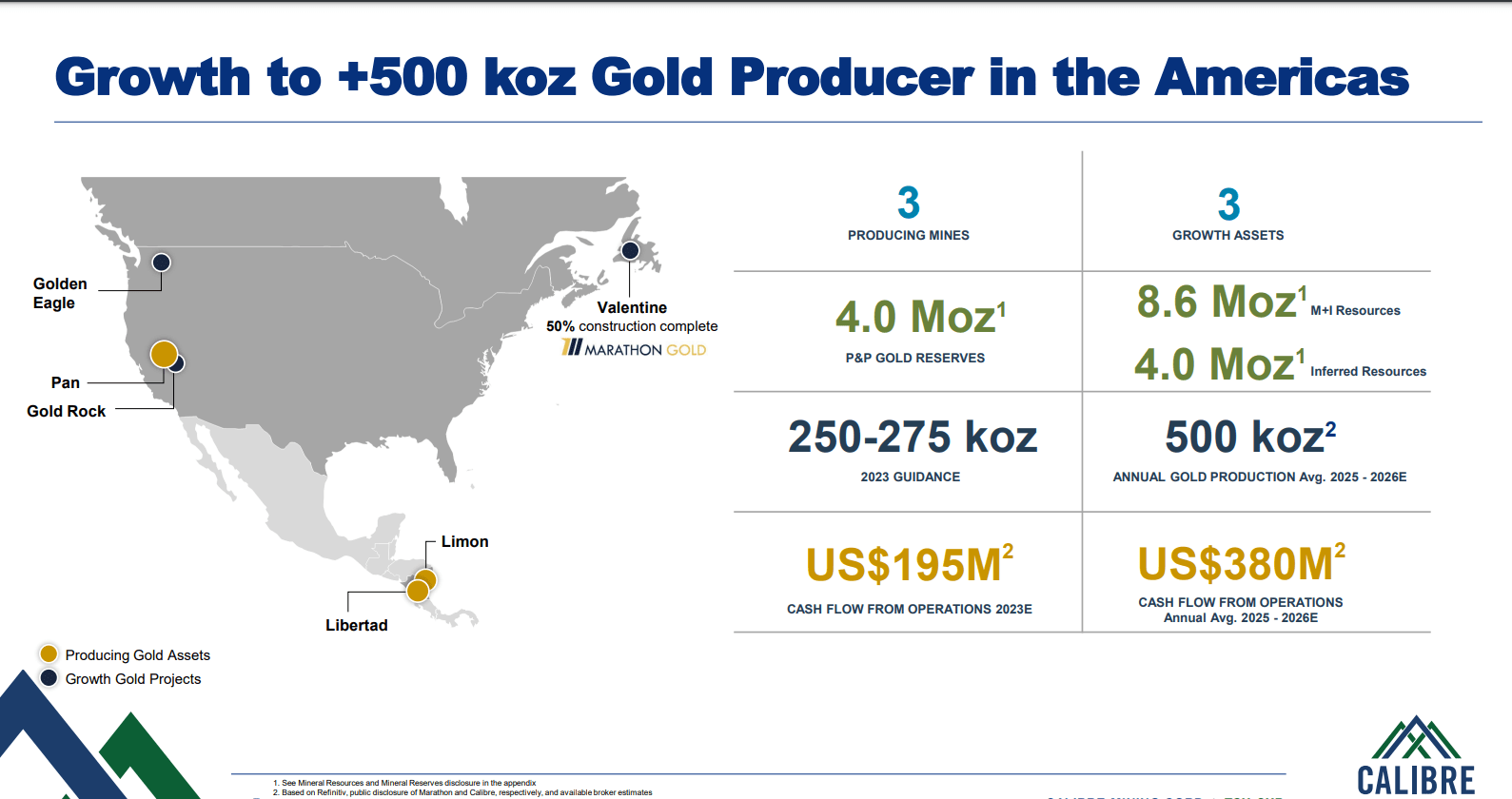

Most importantly, though, this deal transforms Calibre from a primarily Tier-3 jurisdiction producer to a primarily Tier-1 jurisdiction producer with its NAV tied to Nevada and Newfoundland above that of its NAV attributed to Nicaragua. And for a company that has historically traded at a low single-digit cash flow multiple and a huge discount to its peers, this could be one way to finally achieve a re-rating.

Calibre Mining 2.0

As for how the new company will look, Calibre will have a producing mine in Newfoundland (Canada), Nevada (United States), and multiple mines feeding two plants with a Hub & Spoke model in Nicaragua. Meanwhile, annual production will increase to 500,000 ounces in 2025/2026 with potential upside in Nicaragua (Paneton North/Panteon North Extension) and excess capacity at the Libertad Plant as well as potential upside from Gold Rock in Nevada (small development project). And as for costs, we should see see the company's consolidated AISC improve to ~15% below the industry average at sub $1,180/oz in 2026 given that Valentine should produce at sub $1,025/oz costs in its first several years even adjusting for sticky inflationary pressures. And this portfolio should generate upwards of $225 million in annual free cash flow in 2026, with Valentine capable of producing ~$130 million on its own in its 2026/2027.

Calibre 2.0 Snapshot - Company Presentation

{kind=link}

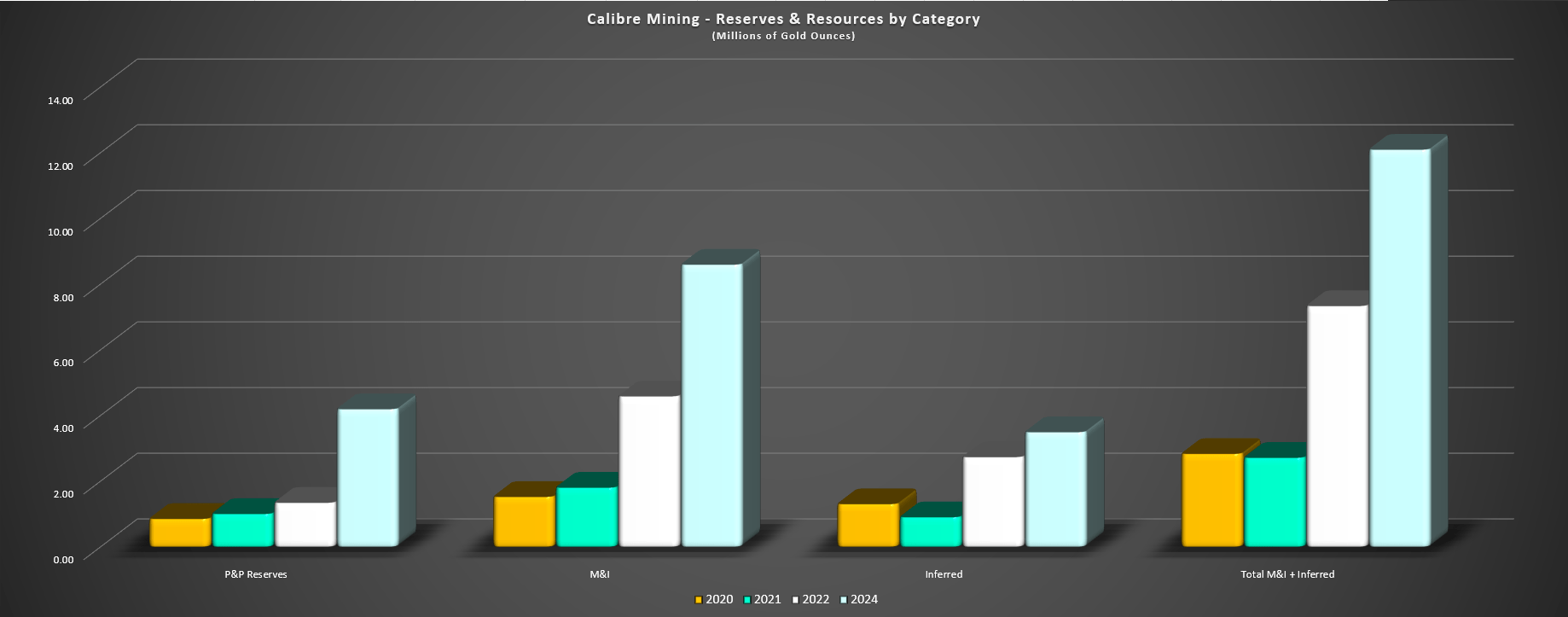

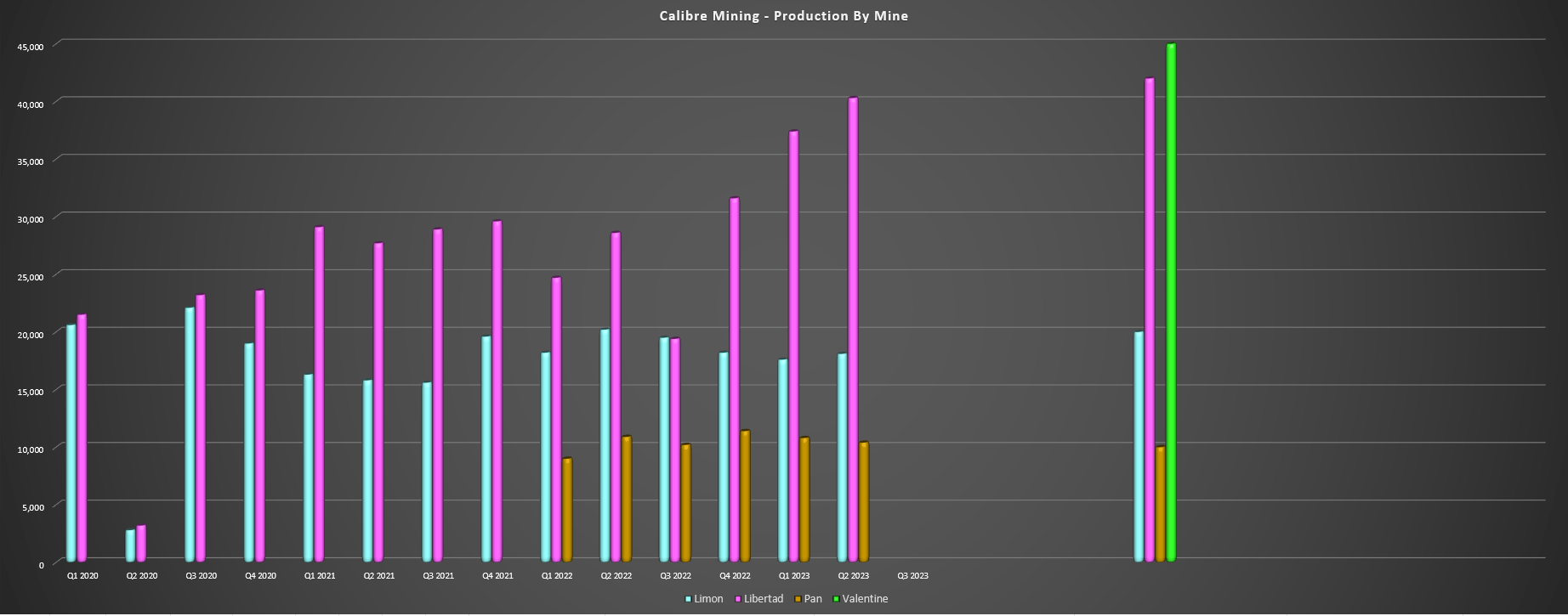

As for how this will impact Calibre's resources and reserves, Marathon's ~5.1 million ounces of total resources will provide a nice boost to Calibre's total resource base of ~7.3 million ounces, growing Calibre's total resource base to 12.0+ million ounces assuming the deal closes. Meanwhile, Calibre's reserves will triple from ~1.35 million ounces to ~4.05 million ounces. Finally, digging into production, we should see Calibre's quarterly production soar to ~120,000 ounces by Q3 2025 once Valentine is in commercial production, with just less than half of this production coming from Tier-1 ranked jurisdictions. The below chart shows Calibre's production currently (blue and pink bars highlight production coming from Nicaraguan) and we can see that the two-year forward outlook will be much different from a geographical standpoint.

Calibre Mining - Reserves & Resources by Category - Company Filings, Author's Chart Calibre Mining - Quarterly Production by Mine (Current vs. Q3 2025) - Company Filings, Author's Chart & Estimates

{kind=link}

{kind=link}

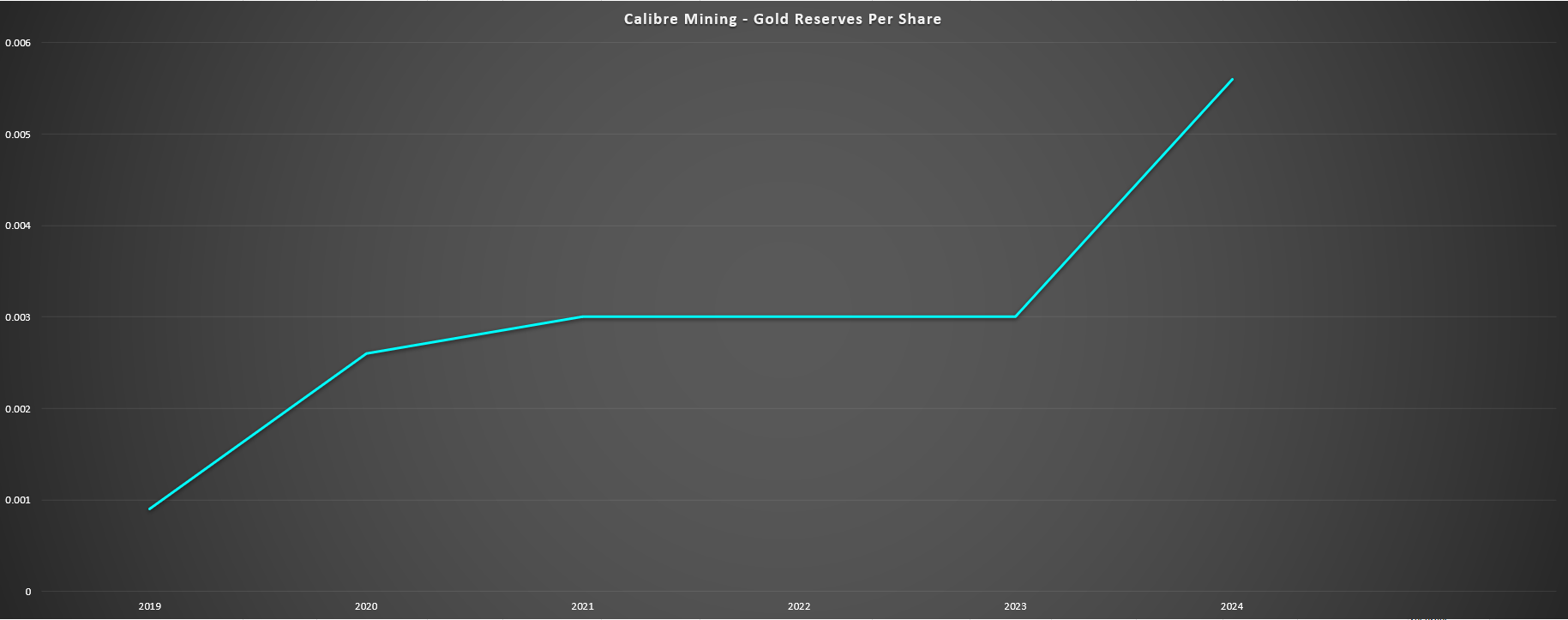

Finally, while adding ounces, production, cash flow, and growing NAV is important, the key is for this to be accretive on a per share basis or it's mcuh less meaningful for shareholders. And in Calibre's case, we can see that despite share dilution from the deal (~50%), gold reserves per share are set to double, giving Calibre one of the best reserve/resource growth trends sector-wide if the deal is succesful. Hence, this is a home-run for Calibre if it can pull this deal off successfully, and it certainly is a great example of how much per share growth can be achieved by being disciplined and waiting for fire-sale opportunities in the market vs. growth simply for the sake of growth like we've seen in many other transactions.

Calibre Mining - Gold Reserves Per Share - Company Filings, Author's Chart & Estimates

{kind=link}

Price Paid Relative To Other Acquisitions

Looking at the deal a little closer, Calibre paid a price of ~$250 million for Marathon, translating to ~0.42x estimated NPV (8%) of ~$590 million, less than 2x average FY2026/FY2027 mine-site free cash flow of ~$130 million, and just ~$63/oz on M&I resources and ~$50/oz on total resources. To put these figures in perspective, Kinross ( KGC ) acquisition of Great Bear came at an acquisition price of ~$1.46 billion, which was ~1.10x NPV (8%) and over $170/oz on M&I ounces (assuming 8.5 million ounces are proven up). Plus, the Great Bear was at least seven years from initial production at the time of the acquisition and would still cost at least $1.1 billion when considering drilling, permitting and overall construction costs.

This is the difference between acquiring a company at the peak of the 2021 bull market for juniors when it's up ~1400% in the past three years, and acquiring a stock in a violent down cycle for the sector when it's down over 80% over the past three years.

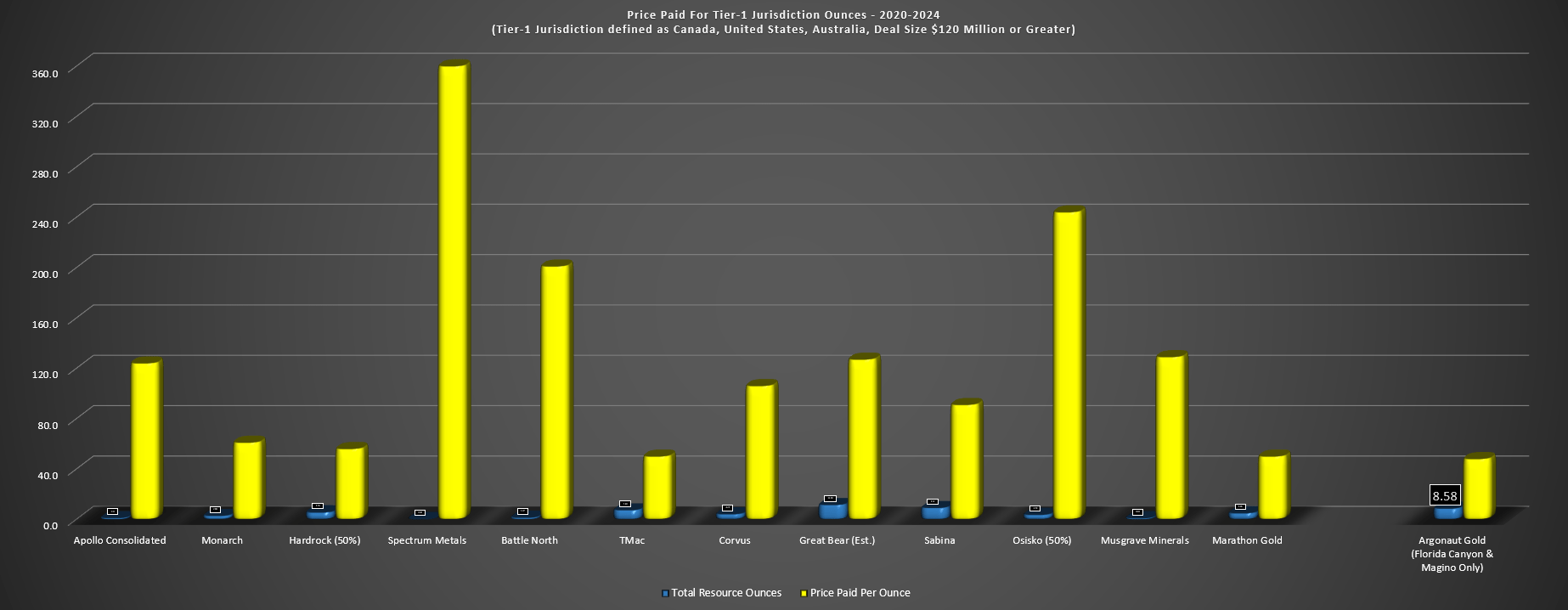

Price Paid For Tier-1 Jurisdiction Ounces (2020-2024) - Company Filings, Author's Chart

{kind=link}

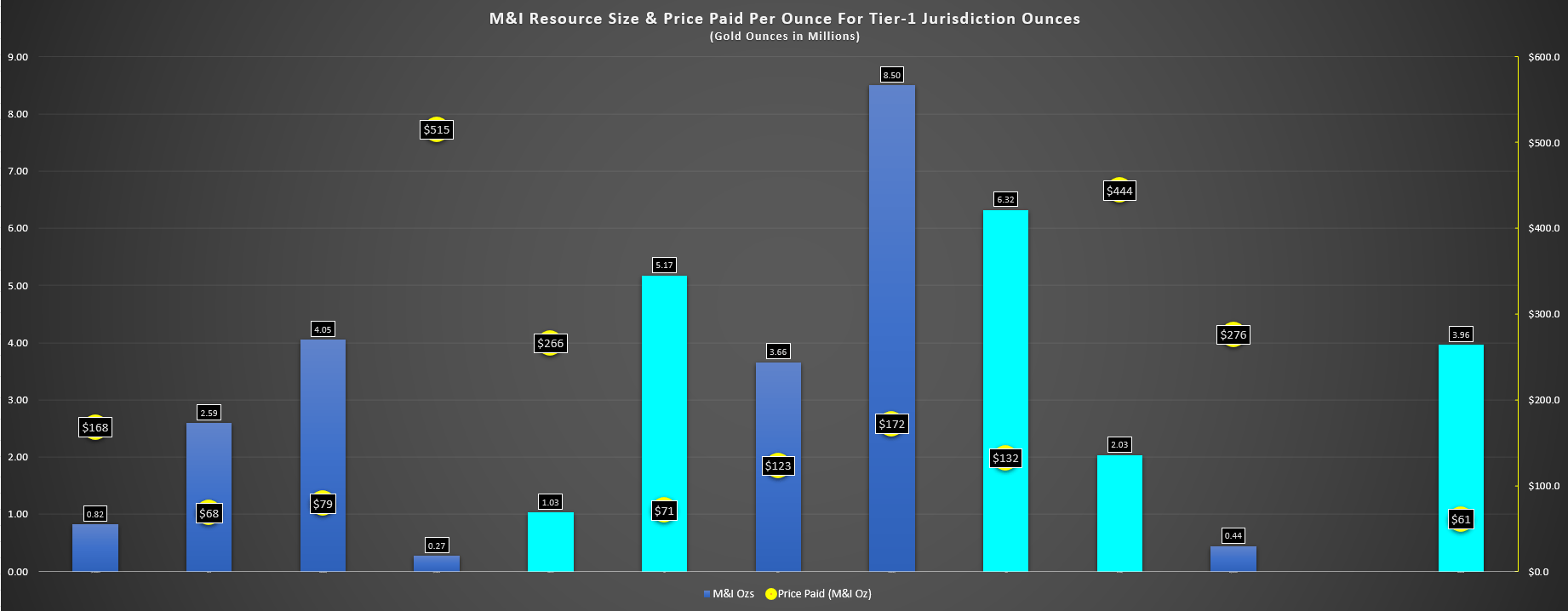

If we look at a larger sample size, we can see that Calibre's implied price paid of ~$50/oz per ounce of resources compares quite favorably to the median price of ~$106/oz and average price paid of ~$140/oz, especially considering that most of these Tier-1 jurisdiction assets did not have existing infrastructure (Valentine is already half built). And it certainly compares favorably to another expensive acquisition done by First Majestic ( AG ) even with the benefit of AG's strong currency with it paying ~$253 per resource ounce and with this asset since heading into care and maintenance. Finally, from an M&I resource standpoint, this was the lowest price paid since 2020, beating out the ~$50/oz to ~$65/oz paid for high-grade ounces in Nunavut ( TMAC ), permitted ounces in Canada (Greenstone), and underground bulk mineable ounces at 2.0+ grams per tonne of gold at Wasamac (Monarch).

M&I Resource Size & Price Paid For Tier-1 Jurisdiction Ounces (Ounces of Gold In Millions) - Company Filings, Author's Chart

{kind=link}

Perhaps the most impressive part about this deal, though, as highlighted earlier, is that Calibre is buying a project that will generate over $130 million in free cash flow in 2026. This enables a quick payback relative to other assets like Wasamac (2029), Great Bear (2029), Railroad-Pinion (2026) that are still up to three years away from production. Hence, this deal is more similar to B2Gold's ( BTG ) brilliant acquisition of Sabina, with it adding a partially constructed, near-production and high-margin asset with the benefit of a relatively quick payback. That said, while B2Gold got a good price for Sabina and Back River is higher quality than Valentine (larger scale, higher grades, and better margins), Calibre is getting a phenomenal price for Valentine with a similar first pour (Q1 2025) and in a less challenging jurisdiction from a logistics standpoint. So, with a massive gold belt that's relatively unexplored, I certainly wouldn't rule out a 6.0+ million ounce resource here long-term, especially with Calibre's impressive track record of drill success in Nicaragua, making a significant discovery at Limon (Panteon North/PN Extension).

Valentine Gold Project & Panteon North Discovery - Calibre/Marathon Presentations

{kind=link}

Summary

While there have been many deals done at the right price and many deals done on the right asset, there are few deals that have managed to accomplish both simultaneously. Three names that have stood out in this category for consistently getting great assets at great prices are Alamos ( AGI ), Agnico ( AEM ) and Kirkland Lake, with Richmont, Aurico, Lynn Lake and Mulatos in Alamos' case, Goldex, Riddarhyttan (Kittila), Cumberland (Meadowbank), Osisko (50% Malartic), TMac Resources (Hope Bay), Kirkland Lake Gold (KL), and Detour/Fosterville in Kirkland Lake Gold's case. However, Calibre is certainly punching above its weight on this recent counter-cyclical deal if Valentine works out as expected, with the lowest price paid in several years per M&I ounce for a project already benefiting from infrastructure, and the lowest price paid for any Tier-1 jurisdiction asset since 2020 (above $120 million deal value).

The result of this acquisition (if successful) is that Calibre might finally have a shot at a meaningful re-rating given its increased scale, improved margins and upgrade to its jurisdictional profile and due to acquiring counter-cyclically, the company will see considerable growth per share in NAV, resources, production, cash flow, and reserves. In addition, the combined company will generate over $225 million in free cash flow, allowing it to continue drilling aggressively and support its next leg of growth later this decade (whether organic or another acquisition) with minimal share dilution given that its improving balance sheet could support a cash deal or growing production within existing jurisdictions. To summarize, I see this deal as a major win for Calibre shareholders, and I now see the stock as investable given that the stock has finally been de-risked with improved diversification from a NAV standpoint.

For further details see:

Calibre Mining: Adding Marathon's Tier-1 Jurisdiction Ounces At An Attractive Price