USAS - Calibre Mining: Steady Growth In Reserves Per Share

2023-07-07 15:46:10 ET

Summary

- Calibre Mining Corp. has outperformed its peers in 2023, with its stock up over 63% year-to-date helped by a track record of growth in production, reserves, and cash flow per share.

- The company reported a 6% increase in gold reserves year-over-year, with a significant increase in reserve grade, and has grown its resource base by 200% from year-end 2020 to year-end 2022.

- Given the company's continued exploration success across its portfolio, strong balance sheet, and consistent per share growth, I would view pullbacks below US$0.84 as buying opportunities.

2023 has been another rollercoaster ride of a year for investors in the VanEck Gold Miners ETF ( GDXJ ), with the index briefly up over 15% year-to-date in both years before slipping back into negative territory in the weaker seasonal period post April. However, one name has massively outperformed its peer group, up over 63% year-to-date, and it was one of the few names in the sector to hit new 52-week highs earlier this year.

This company is Calibre Mining Corp. ( CXBMF ). The stock's outperformance is certainly justified, with it being one of the few small-cap names that continues to steadily grow its production, reserves, and cash flow per share. In this update, we'll look at the company's 2022 Reserve/Resource update and whether the stock has moved into a low-risk buy zone after its recent correction.

Calibre Mining Operations (Company Website)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

2022 Reserves

Calibre Mining released its 2022 Reserve/Resource update earlier this year, reporting an increase in grades for its Nicaraguan reserve base, as well as total ounces. The addition of its new Pan Mine in Nevada, a maiden reserve at its new Panteon North discovery at El Limon, and a slight increase in ounces at Eastern Borosi Underground, offset moderate mining depletion at its Pavon Open Pit, its El Limon open-pit material and stockpiles, and a decline in its stockpiles at Libertad/Pavon. The result was that the company ended the year with ~1.08 million ounces of gold reserves, or a 6% increase year-over-year (2021: ~1.01 million ounces), and a significant increase in reserve grade, with grades soaring from 4.62 grams per tonne of gold to 5.18 grams per tonne of gold for its Nicaraguan reserve base.

El Limon & Libertad Reserves & Reserve Grade (2013-2022) (Company Presentation)

{kind=link}

Looking at the above chart, we can see the progression in reserves since the acquisition of B2Gold's ( BTG ) Nicaraguan assets. As is clear, the company has done an exceptional job growing its reserve base at higher grades. The maiden reserve base of 244,000 ounces at 9.45 grams per tonne of gold at Panteon North has certainly contributed nicely to the increases in total reserves and reserve grade, as has the successful conversion of resources to reserves at Eastern Borosi, a high-grade spoke that began ore deliveries ahead of schedule earlier this year.

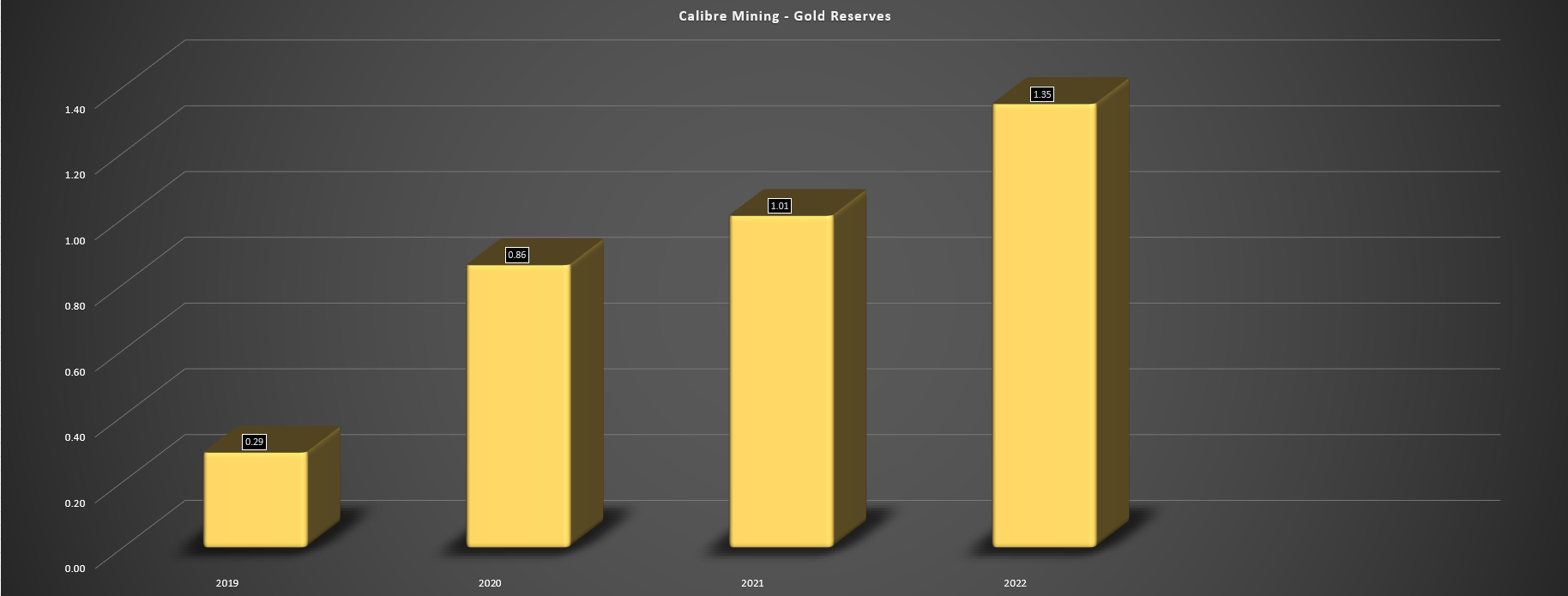

Meanwhile, from a consolidated standpoint, reserves have grown further through the addition of the high-volume and low-grade Pan Mine in Nevada, even if the asset has seen a slight decline in reserves from Fiore's pre-acquisition reserve statement (~264,000 ounces vs. ~291,000 ounces). Calibre's consolidated reserves (Nicaragua and Nevada) are shown below, and hit a new high of 1.35 million ounces of gold in 2022.

Calibre Mining - Gold Reserves (Company Filings, Author's Chart) Calibre Mining - Reserve Grade by Asset (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Based on ~19.8 million tons of material and assuming an annual throughput rate of ~5.5 million tons per annum, Pan's mine life has declined to just four years, which is certainly on the lower end for open-pit operations sector-wide. That said, the company continues to have exploration success near-mine (Pegasus, Dynamite, and Dune), and has also made a new discovery three kilometers south of the Pan South open pit at Coyote. Plus, Calibre continues to have one of the more aggressive exploration programs among its peer group. So, while Pan's mine life is relatively low, especially considering that it's using a gold price assumption of $1,600/oz, which is above the industry average, I am optimistic about resource growth and reserve replacement and don't think it unreasonable that Pan could remain into production past 2030 despite its ~4-year mine life.

El Limon Drill Highlights & Panteon North (Company Website)

{kind=link}

Digging into the company's Nicaraguan operations, Calibre currently has ~6.3 million tonnes of material in reserves. So, if we assume a throughput rate of ~1.8 million tonnes per annum for El Limon and Libertad combined, this also represents a relatively short mine life based on solely reserves. However, the company has easily replaced reserves net of depletion to date, and it continues to hit high-grade intercepts north of Panteon North (within further room to step out along the potential extension), and it also recently released solid results from its Talavera Extension, just 3 kilometers from the Limon Plant. Therefore, like Pan, and given the company's large Nicaraguan resource base backing up reserves (~3.0+ million ounces outside of reserves), I don't see any reason to worry about the shorter mine life (implied by solely reserves) at its Nicaraguan assets either.

2022 Resources

Moving over to Calibre's resource base, we've seen significant growth here as well, with measured & indicated ounces increasing from ~1.53 million ounces at year-end 2020 to ~4.59 million ounces at year-end 2022 (200% growth). Meanwhile, the company's inferred resource base has also more than doubled to 2.74 million ounces, up from ~1.31 million ounces at year-end 2020. While Calibre achieved most of this resource growth through M&A with the addition of Pan, Gold Rock, and Golden Eagle (Fiore Gold acquisition), it accomplished this at a relatively low cost from a share dilution standpoint, helping to maintain its trend of resource growth per share. And even if we exclude the Golden Eagle Project (Washington), which is unlikely to head into production before 2030 and is in a less favorable jurisdiction than Nevada, the company's total measured, indicated, and inferred resource base (inclusive of reserves) still stands at ~5.2 million ounces of gold.

Calibre Mining - Reserves & Resources by Category (Company Filings, Author's Chart)

{kind=link}

This represents a significant resource base, especially considering that much of this material is in the vicinity of available infrastructure either in Nicaragua (Eastern Borosi, Limon & Libertad ore sources) or Nevada (Gold Rock) when it comes to material outside of reserves. Plus, the cut-off grades at high-grade ore sources like Pavon Norte/Central and Guapinol/Vancouver are quite reasonable at sub 2.0 grams per tonne of gold, pointing to a relatively low hurdle to adding new reserves from additional discoveries at these projects.

To summarize, Calibre's strong balance sheet (~$60 million cash), and its low discovery cost per ounce given how effective its drilling has been to date, point to a favorable setup for maintaining a 250,000-ounce production profile given that reserves should continue to trend higher from the current ~1.35 million ounce mark. The company has seen no shortage of new discoveries or processing capacity in Nicaragua to support near-term resource growth as well.

Reserves Per Share

Reserve growth is important, but far more important is reserve growth per share. This is because reserve growth that comes at the expense of significant share dilution means that investors are getting exposure to fewer ounces of gold per share held and the result is one is actually seeing their exposure to precious metals diluted by owning any precious metals producer that cannot maintain reserves per share. Therefore, an investor in any producer with this criterion is not getting their desired leverage to the silver and or gold price if reserves and or production per share are declining.

Obviously, this isn't ideal, since it makes little sense to own a producer that carries higher volatility and risk vs. a commodity (the metal itself) if it is not offering the leverage that one should get for taking on this added risk. Fortunately, Calibre has excelled in this category since year-end 2019, with only moderate share dilution related to its Fiore acquisition and the successful addition of reserves at its Nicaraguan mines.

Calibre Mining - Gold Reserves Per Share (Company Filings, Author's Chart)

{kind=link}

As shown in the chart above, we can see that Calibre Mining has more than doubled its reserves per share since 2019, with its total reserves up from ~290,000 ounces (solely El Limon) to ~1.35 million ounces in the same period that its share count has increased just 37% (~450 million shares vs. ~328 million shares). Importantly, Calibre should see further growth in reserves per share as it grows ounces at its new Panteon North discovery, where the company currently has just 244,000 ounces in reserves at industry-leading grades (9.45 grams per tonne of gold), but could ultimately double reserves from current levels to 500,000+ ounces.

In addition, the company looks to have upside to reserves at its Gold Rock Project in Nevada just south of Pan. Therefore, if investors are looking for a company with consistent reserve growth per share, Calibre is one of the few options in the small-cap space and certainly a better option than names like Coeur ( CDE ) and Americas Gold and Silver ( USAS ) that continue to dilute at a faster pace than they grow reserves.

Summary

Calibre Mining Corp. reported another material increase in its gold reserves in 2022, and it continues to have one of the better track records of reserve growth per share sector-wide. This certainly makes it stand out among its small-cap peer group, and favorable permitting timelines and excess processing capacity give Calibre an advantage vs. some peers with the company with its ability to turn resources into reserves with minimal difficulty.

That said, Calibre Mining Corp. stock has outperformed its peer group meaningfully over the past year, and for this reason I continue to see better relative value setups elsewhere in the sector. However, if Calibre were to dip below US$0.84 where it would trade at closer to 3.2x EV to FY2024 FCF estimates (~$120 million) on a fully diluted basis, I would consider starting a new position in the stock.

For further details see:

Calibre Mining: Steady Growth In Reserves Per Share