CXBMF - Calibre Mining: Valuation Continues To Improve

Summary

- Calibre Mining released its Q2 financial results earlier this month, continuing to over-deliver on promises, a rarity among the junior/mid-tier space.

- The company remains on track to meet production and cost guidance, and given exploration success, we should see some improvement in costs next year with additional high-grade feed.

- Based on a current fully-diluted market cap of ~$357 million, Calibre trades at one of the cheapest valuations sector-wide, sitting at ~2.4x FY2023 cash flow estimates and ~0.50x P/NAV.

- Given the company's ability to continuously meet targets and continued exploration success, I would view any pullbacks below C$0.78 [US$0.62] as buying opportunities.

It was a mixed Q2 Earnings Season for the Gold Juniors Index ( GDXJ ), and while output came in near budget, cost performance left a lot to be desired. This was largely out of the control of most producers, leading to negative guidance revisions related to impacts from inflationary pressures (diesel, labor, cyanide, power). However, true to form, Calibre Mining Corp. (CXB:CA)( CXBMF ) managed to buck the trend, sticking with its track record of guiding conservatively and seeing benefits from a grade lift at its Nicaraguan operations.

The good news is that while Nicaragua's improved grades helped the company maintain similar all-in-sustaining cost [AISC] margins year-over-year, further grade improvements are on deck. In fact, recent exploration success suggests that head grades at its operations could be even better than previously anticipated, setting the company up to pull costs back below $1,175/oz post-2023. So, given Calibre's consistency and ability to meet targets in a sector where this is in short supply, combined with an attractive valuation, I would view pullbacks below C$0.78 [US$0.62] as buying opportunities.

El Limon Drill Core (Company Presentation)

{kind=link}

Q2 Production

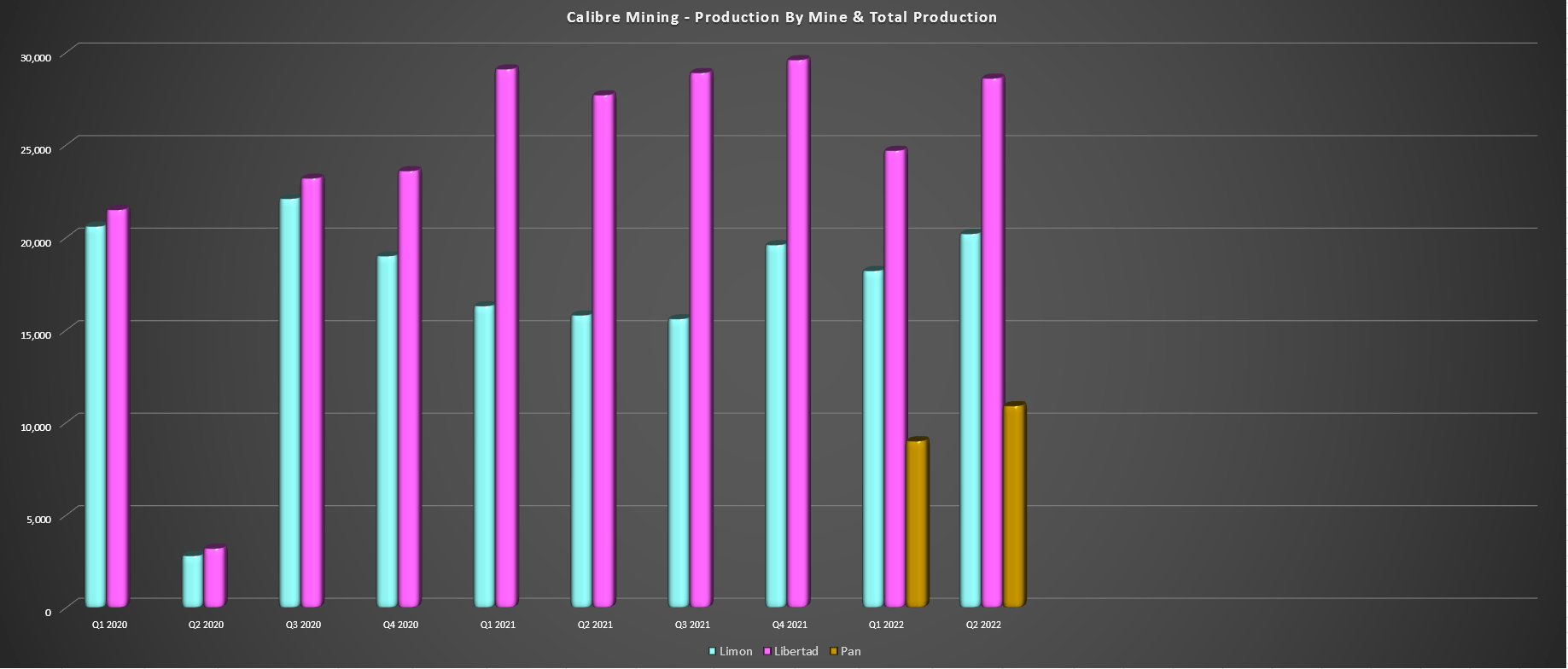

Calibre Mining released its Q2 results earlier this month, reporting record quarterly gold production, record revenue, and a sharp increase in operating cash flow. While the record production is not surprising with the addition of a new mine that did lead to some share dilution (Fiore acquisition), the company delivered a near-record quarter at its Nicaraguan operations as well, producing ~48,800 ounces, just shy of the ~49,200 ounces produced in Q4 2021. This was helped by higher grades at both Limon and Libertad, with mined grades up more than 20% year-over-year and feed grades up sharply at both operations.

Calibre Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

Digging into operations a little closer, Libertad had another phenomenal quarter, producing ~28,600 ounces, just below its record levels of ~29,600 ounces (Q4 2021). However, the most impressive metric was that the asset delivered this production and its 3% growth year-over-year despite a sharp decline in tonnes processed. In fact, tonnes processed declined to ~232,700 vs. ~334,400 in the year-ago period. The offset was a significant increase in grades, with Libertad's feed grades improving to 3.60 grams per tonne of gold, a 31% increase from 2.74 grams per tonne of gold in Q2 2021, helped by the high-grade Pavon Norte Mine that was put into production last year.

At Limon, grades also increased considerably, improving to 5.56 grams per tonne of gold, up from 4.06 grams per tonne of gold in Q2 2021, benefiting from higher grades at Limon Central. This more than offset the ~3% decline in throughput, allowing the asset to produce ~20,200 ounces, a nearly 30% increase year-over-year, and its best quarter since Q3 2020. Year-to-date, Limon has produced ~38,400 ounces. So, combined with Libertad's year-to-date production of ~53,300 ounces and a small contribution from Pan (~19,900 ounces), Calibre is tracking well against FY2022 guidance - ~111,600 ounces produced year-to-date vs. guidance of 228,000 ounces at the mid-point.

Libertad - Tonnes Processed, Current Capacity, Head Grade (Company Filings, Author's Chart)

{kind=link}

Before moving to costs, it's important to point out that while Calibre is on track to meet guidance of ~228,000 ounces and Libertad is on track to produce over 100,000 ounces this year, this operation is running at less than half of its true potential. This doesn't mean that we'll see an immediate double in production at Libertad. Still, as new sources of ore come online (Eastern Borosi, Pavon Central), we could see a significant increase in production from relatively low capex growth (idle capacity is sitting at the Libertad Mill).

From a longer-term standpoint, once multiple spokes are in development, Libertad could be a 215,000-ounce producer on its own at ~2.0 million tonnes per annum and a head grade of 3.75 grams per tonne gold. This would still leave 200,000 tonnes per annum of capacity at the mill and could be a conservative grade estimate with the benefit of 6.0+ gram/tonne material from Eastern Borosi. So, while Calibre has meaningful growth from exploration success at Limon, the potential development of Gold Rock, and possibly better mines at Pan (Nevada), Libertad has significant gas in the tank and, in a perfect world, could allow for ~70% production growth from current levels.

The 80% production growth assumes ~215,000 ounces from Libertad, ~80,000 ounces from Limon, ~45,000 ounces from Pan, and 50,000 ounces from Gold Rock. Importantly, this is all relatively low capex growth.

Costs & Margins

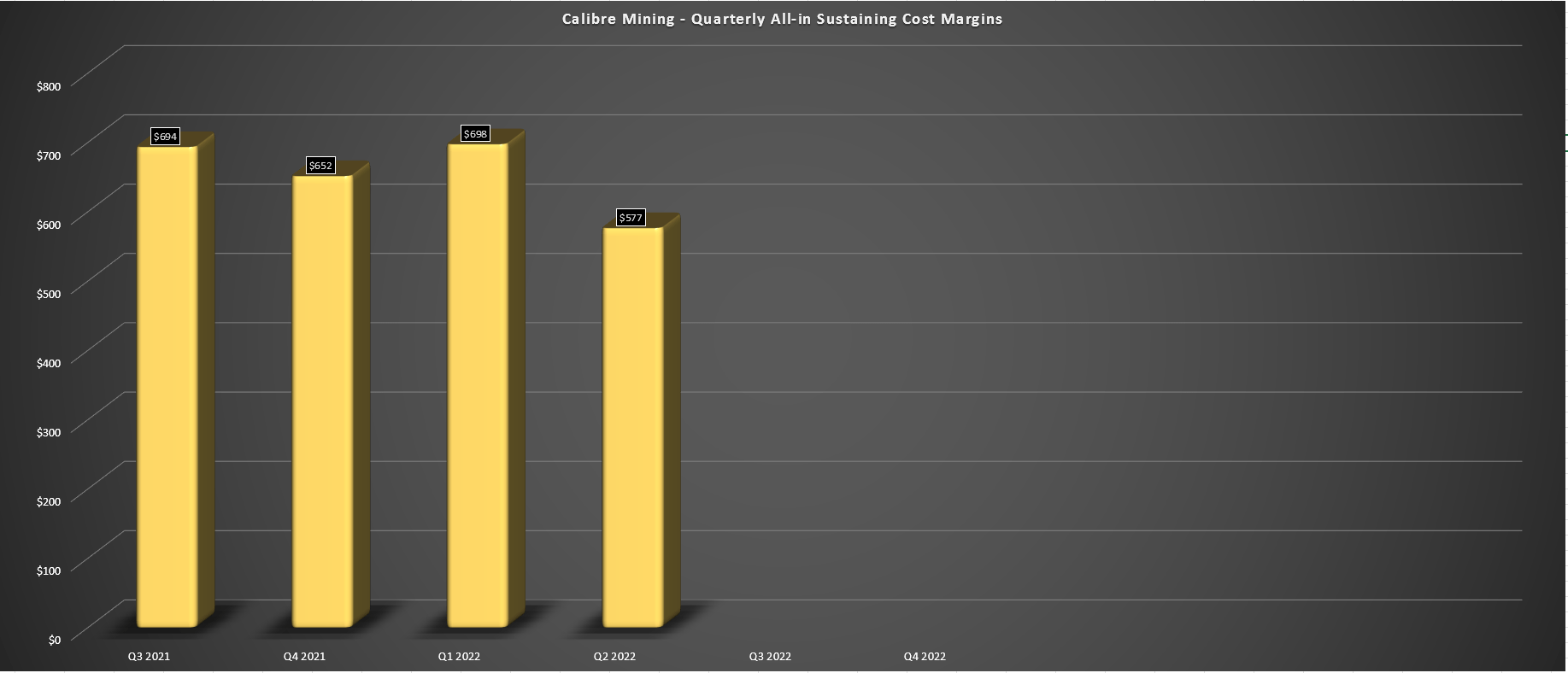

While the production results were solid, the bigger focus this year has been on costs, with negative cost guidance revisions becoming the norm. However, while Calibre's costs were up in Q2 2022 to $1,284/oz (Q2 2021: $1,216/oz), this was not anywhere near the price increases we've seen from other producers like Argonaut ( ARNGF ) at ~20% year-over-year. This doesn't mean that Calibre was immune to inflationary pressures, and diesel prices impacted costs. However, with a sharp increase in grades and fewer tonnes processed, this helped considerably from a cost standpoint.

Calibre - Quarterly AISC Margins (Company Filings, Author's Chart)

{kind=link}

Moving to AISC margins, we saw a 2% decline year-over-year to $577/oz, but this isn't surprising given that Calibre added a higher cost with Pan, and costs were higher due to increased waste movement in Q2 at the asset. However, Calibre has noted that costs should improve with higher grades in H2, allowing the company to deliver into its guidance of $1,200/oz - $1,275/oz AISC in FY2022. Looking ahead to FY2023, I expect costs to dip below $1,220/oz with the benefit of higher-grade feed and assuming inflationary pressures don't worsen.

Calibre Mining - Quarterly & Trailing Operating Cash Flow (Company Filings, Author's Chart)

{kind=link}

Given the solid cost controls and strong production, Calibre had a phenomenal quarter from a financial standpoint, reporting record revenue of $111.3 million and operating cash flow of $43.2 million. This has pushed Calibre's trailing twelve-month cash flow above $110 million, an impressive figure for a company with a sub $300 million enterprise value. However, as noted above, Calibre is at an inflection point from a growth standpoint, and there is a path to 330,000 to 390,000 ounces medium-term and long-term from its existing assets, assuming Gold Rock (south of Pan) is green-lighted. So, I would expect a meaningful increase in cash flow per share over the next few years, even if gold prices continue to hang out below $1,800/oz.

Valuation & Technical Picture

Based on ~498 million fully diluted shares and a share price of US$0.73, Calibre Mining trades at a market cap of ~$363 million and an enterprise value of ~$271 million. This is a dirt-cheap valuation for a company with an industry-leading growth profile, with Calibre now trading at ~2.5x FY2023 cash flow estimates (~$145 million) or below 2.0x cash flow on an enterprise value basis. On a P/NAV basis, the valuation is also extremely attractive, with Calibre trading at a multiple of 0.50 vs. an estimated net asset value of $725 million. These are among some of the lowest valuation multiples sector-wide, which makes little sense given that one could argue Calibre is in the top quartile from a growth and track record of meeting targets standpoint.

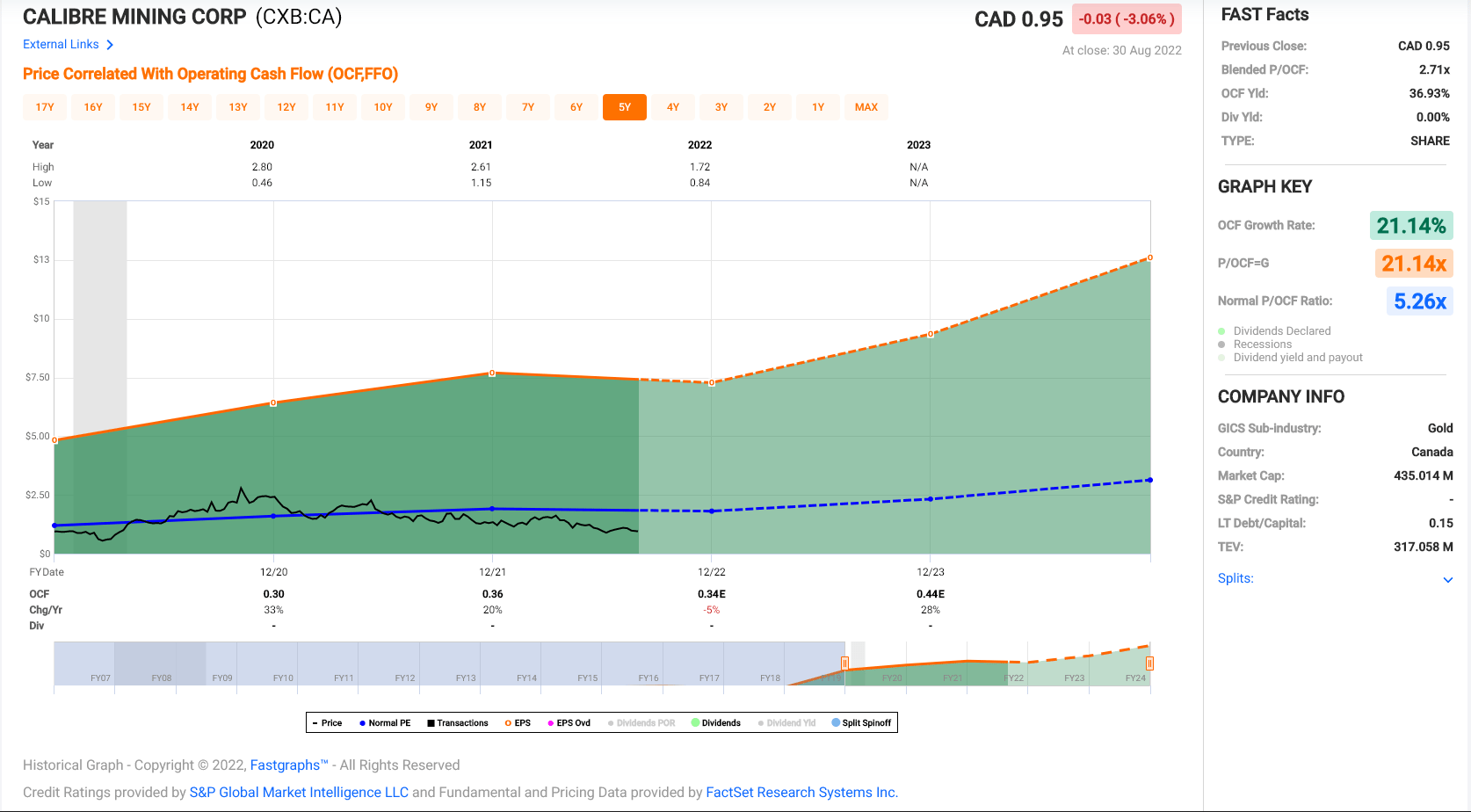

Calibre - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

Based on what I believe to be a conservative multiple of 0.75x P/NAV, which reflects its higher-risk jurisdictional profile offset by exploration success and growth, I see a fair value for the stock of US$1.09 per share. From a cash flow standpoint, I think a cash flow multiple of 4.25 is more than reasonable, translating to a fair value of US$1.24. So, regardless of how one values the stock, there looks to be a minimum 50% upside to fair value here. It's important to note that these price targets assume no improvement in the gold price (sub $1,800/oz) and are based on conservative multiples. Let's look at the technical picture:

CXBMF Daily Chart (TC2000.com)

{kind=link}

While Calibre's valuation is extremely attractive, its technical picture is not showing a low-risk buy point yet, with the stock still more than 10% above the area where it previously found support (US$0.64) and with resistance levels stacked overhead. This doesn't mean that the stock must trade lower, but when it comes to small-cap producers, I prefer to buy at or below support, with these stocks tending to undercut their lows.

So, while the current setup is more favorable than in May when I noted that the stock would likely have a tough time with the US$1.00 level, I don't see a low-risk buying opportunity just yet. That said, a pullback below US$0.62 would put the odds meaningfully in the bulls' favor from a fundamental/technical standpoint.

Summary

Calibre continues to fire on all cylinders operationally and has one of the simplest and lowest-capex growth profiles sector-wide. I believe this should translate to higher multiples than its historical average (~4x cash flow) in a market where some producers are drowning in debt trying to finance their aggressive high-capex growth. So, if one is patient and buys when there's blood in the streets (like now), I see them being handsomely rewarded from current levels. That said, I prefer to only buy at ultra low-risk buy zones, and this area comes in below C$0.78 [US$0.62] for Calibre, where I would strongly consider the stock for a medium-term swing trade.

For further details see:

Calibre Mining: Valuation Continues To Improve