CRC - California Resources: Carbon Capture And Potential Separation From Oil Production

2023-09-13 07:21:55 ET

Summary

- California Resources Corporation expects FCF growth in 2023 and is focused on carbon management and energy transition, which could attract investors interested in ESG practices.

- CRC has significant proven reserves and current production capacity, suggesting that the stock could be undervalued.

- The company's solid balance sheet and strategic options, including the possible separation of its businesses, further support the potential for increased stock valuation.

California Resources Corporation (CRC) recently delivered guidance that included FCF growth in 2023 as well as efforts in carbon management and energy transition. Considering proven reserves and current production capacity, I believe that CRC could trade a bit more expensively. Besides, we may see a lot of stock demand coming not only from the stock repurchase program, but also from investors interested in ESG practices and the growth of the carbon capture and storage market.

California Resources Corporation

California Resources Corporation is an independent oil and natural gas exploration and production company with sole operations in California. Its mission is to provide affordable and reliable energy in a safe and responsible manner to improve the quality of life for Californians and local communities.

CRC is noted for having some of the most carbon-intensive production in the United States, and is committed to the energy transition through its carbon management business, Carbon TerraVault. In addition, It has established a joint venture to develop carbon capture and storage projects.

CRC seeks to create value for its shareholders, and is considering strategic options, including the possible separation of its businesses. Considering this information, I believe that California Resources Corporation could be worth a bit more than what the market currently reports.

Over time, we intend to conduct our carbon management business on a stand-alone basis. We expect that this will provide greater flexibility to consider strategic options, including the potential separation from our E&P business. Source: 10-k

California Resources Corporation's business model centers on the extraction of crude oil, natural gas, and NGL, which it then sells to traders, refiners, and other buyers with access to transportation and storage facilities. CRC is highly dependent on demand and prices for energy products, and its ability to sell is influenced by unpredictable external factors.

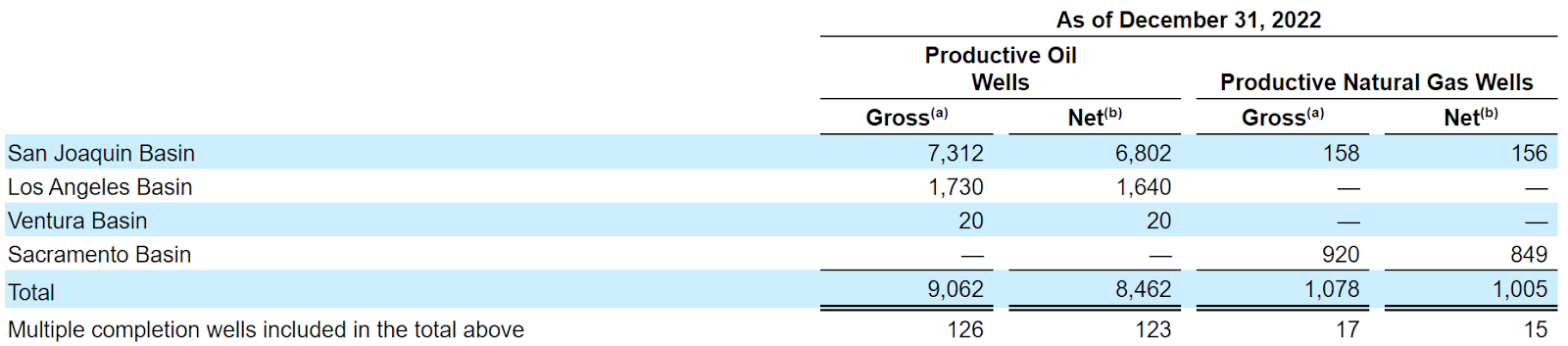

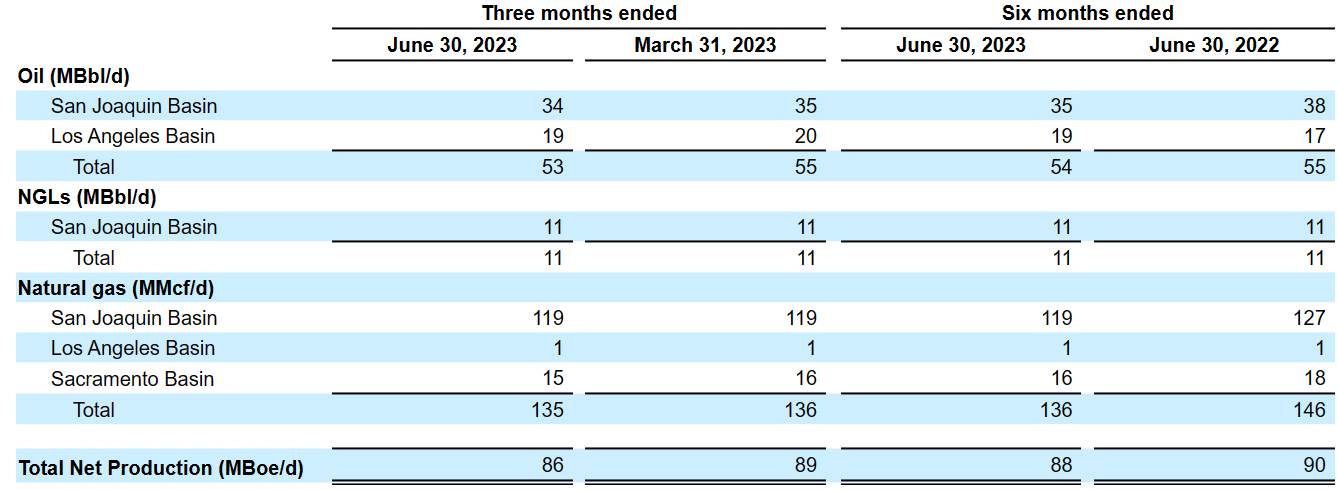

In the last annual report, the company reported a total of 8,462 net productive oil wells and 1078 productive gas wells. In the six months ended June 30, 2023 , the company reported total net production of close to 89 MBoe/d, which is approximately the same reported in the same period in 2022. Under my DCF model, I assumed that production will likely remain relatively stable.

{kind=link}

{kind=link}

With that about what the company currently produces, I believe that the most interesting are the plans for the next decade. Management noted that Sacramento Basin includes close to 9 MMBoe, San Joaquin Basin includes 287 MMBoe, and Los Angeles Basin would have close to 107 MMBoe. Hence, we would be talking about close to 403 MMBoe in total. The company expects to continue production for the next 13 years. However, in my model, I assumed that California Resources will most likely acquire new assets in new territories, so production will most likely continue.

Source: Investor Presentation

The calculation of the PV-10 in a recent presentation stood at close to $5.9 billion. The market capitalization is close to $3.8 billion, so I believe that there is significant room for improvement in terms of stock valuation.

Source: Investor Presentation

It is also worth noting that management gave impressive figures for the year 2023, including 91-85 MBoe/d and 2023 FCF close to $380-$460. I used some of these figures in my cash flow model, so I assumed that investors may want to have a look at them.

Source: Investor Presentation

Solid Balance Sheet

As of June 30, 2023, the company reported cash and cash equivalents worth $448 million, which is significantly larger than what the company reported in 2022. Trade receivables stood at $183 million, with inventories of $69 million and total current assets worth $867 million. The current ratio is larger than 1x, so I do not see a liquidity issue here.

Net property, plant, and equipment stood at $2.7 billion, with total assets of close to $3.900 million. The asset/liability ratio is larger than 1x. In sum, I believe that the balance sheet stands in very good shape.

Source: 10-Q

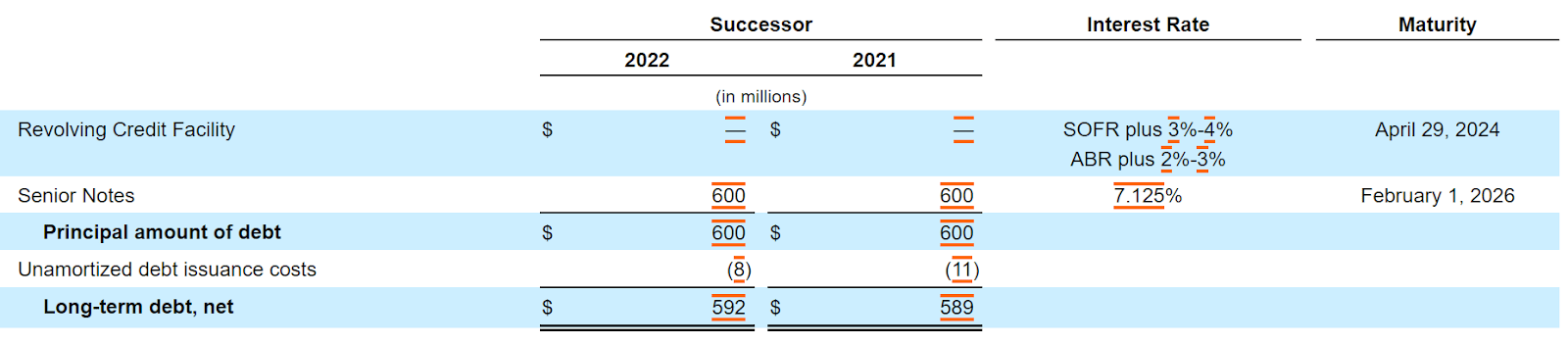

The list of liabilities does not seem worrying at all. Long-term debt stands at about $593 million, with asset retirement obligations of $411 million. With 2023 Forward FCF close to $380 and cash in hand of about $448 million, I believe that the debt does not represent a problem.

Source: 10-Q

CRC has a $602 million senior revolving facility agreement with the potential to augment it with additional lender commitments. The credit facility also includes a $200 million sublimit for letters of credit. The income from the line is used for working capital needs and other purposes. Lenders have a first priority lien on CRC assets, and interest rates are based on SOFR or ABR plus a variable spread. There are no scheduled amortization payments, and the indebtedness base is reviewed semi-annually.

{kind=link}

Decarbonization And Energy Transition Industries Could Accelerate Net Sales Growth, And Bring Significant Demand For The Stock.

California Resources Corporation expects to continue to execute its strategy focused on the development of oil and natural gas assets, while also seizing opportunities in the decarbonization and energy transition industries. In this regard, the company delivered several developments that may accelerate the demand for the stock. I am talking about the storage-only CDMA with Verde Clean Fuels or the class VI permit to the EPA for a reservoir in the Sacramento Basin.

Source: Investor Presentation

Considering the expectations for the carbon capture and storage market, which is expected to grow at close to 16%, I think that more investors may be interested in CRC.

Carbon Capture and Storage Market to Grow at CAGR of 16.49% through 2032. The rise in investments and advancements in technology is driving the growth of the carbon capture and storage market. North America region emerged as the most significant global carbon capture and storage market, with a 38.82% market revenue share in 2022 due to rising oil and gas industry demand and the strict government rules aimed at lowering carbon emissions. Source: Carbon Capture and Storage Market

More ESG Practices Could Also Accelerate The Visibility Of California Resources Corporation

The company expects to focus on improving profitability and maintaining its commitment to safety, sustainability, and ESG practices. Additionally, it will most likely continue to lead the transition to a cleaner, more sustainable energy future. With this in mind and the growth of the global sustainable finance market, I believe that California Resources Corporation may receive more liquidity to run its operations. The global sustainable finance market is expected to grow at close to 22% CAGR in the coming years.

The global sustainable finance market size was estimated at USD 519.88 billion in 2022 and is expected to grow at a compound annual growth rate of 22.6% from 2023 to 2030. The sustainable finance Asset Under Management was valued at USD 37.80 trillion in 2022. Source: Sustainable Finance Market

The Repurchase Of Shares Will Most Likely Have A Beneficial Effect On The Demand For The Stock

I would expect further demand for the stock as a result of the stock repurchase program executed by CRC. Management acquired shares at around $42 and $39 per share. My assumption here is that the company would not buy its own shares at an expensive valuation.

{kind=link}

Cash Flow Expectations From Other Analysts, And My Expectations

Financial analysts out there made optimistic forecasts about California Resources Corporation, so I believe that readers may want to have a look at them. They expect 2025 Ev / revenue close to 1.78x, with EV / EBITDA around 5.05x and EV/ FCF multiple close to 19.8x.

Source: Market Screener

Other expectations from other analysts that I took into account in my cash flow model included 2025 net sales close to $2.184 billion, 2025 EBITDA of $769 million, 2025 net income of $386 million, and 2025 free cash flow of about $196 million.

Source: Market Screener

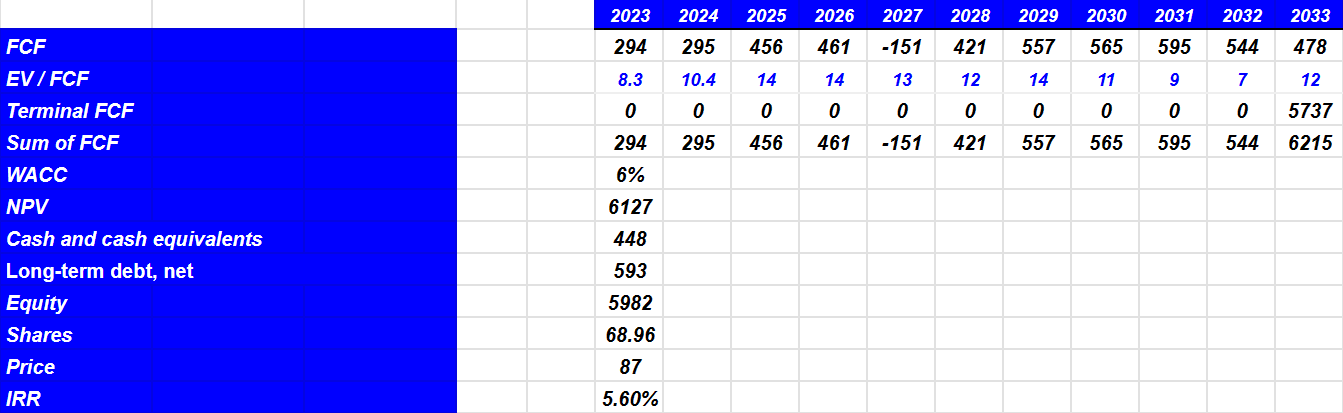

I assumed total production close to 446 MMBoe in the next ten years, with 2033 total net production of 39 MMBoe. 2033 Net sales would stand at close to $2.8 billion, with net income of about $202.02 million. Note that I assumed a net margin close to 11%-7% from 2024 to 2033, which is close to what I saw in the past. I believe that my numbers are quite conservative.

Source: Ycharts

{kind=link}

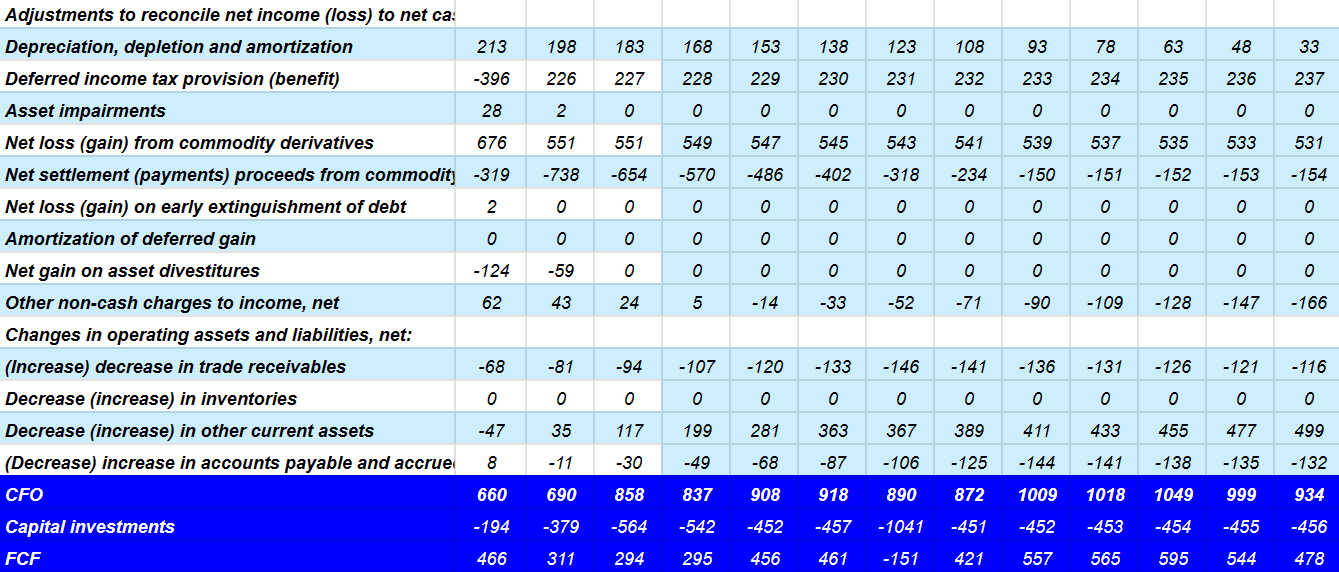

Adjustments to reconcile net income to net cash provided by operating activities were depreciation, depletion, and amortization of about $33 million, deferred income tax provision close to $237 million, and other non-cash charges to income of about $-166 million.

Besides, with changes in operating assets and liabilities including decrease in trade receivables worth -$116 million and changes in accounts payable and accrued liabilities of -$132 million, 2033 CFO would be $934.09 million. Finally, with 2033 capex of -$456 million, 2033 FCF was forecasted at $478.09 million.

{kind=link}

If we assume EV / FCF of 12x million and WACC of 12x, the implied forecasted NPV would be $6127 million. Adding cash and cash equivalents of $448 million, and subtracting long-term debt of $593 million, the implied equity would be $5982 million. Finally, my forecast price would stand at $86 per share with an IRR of 5%-6%.

{kind=link}

I ran a sensitivity analysis with an EV/FCF multiple of 8x-15x and a WACC of 5%-10%, which implied an IRR of 0.08% and 9%. I believe that the model does seem robust, and my results imply that California Resources Corporation could be a bit undervalued.

Source: DCF Model

Risk

California Resources Corporation has set ambitious sustainability goals, including a full-scope Net Zero goal by 2045. However, achieving these goals faces operational, reputational, financial, and legal risks. Uncertainty in estimating and managing scope 3 emissions is a major challenge. CRC's ability to achieve its goals is highly dependent on the success of its Carbon TerraVault business, which is subject to financial and regulatory risks.

Besides, the evolution of the commercial and regulatory environment may also impact the achievement of these objectives. CRC could face additional scrutiny from investors and stakeholders, which could affect its reputation and attractiveness as an investment. Failure to achieve goals could also have negative repercussions on the business and commercial relationships.

Competitors

California Resources Corporation faces diverse competition in the market in which it operates. Locally, it competes with independent and large international companies operating in California. It also competes with foreign companies due to the significant importation of oil into the state. CRC takes advantage of its proximity to California refineries to reduce transportation costs, and benefits from the compatibility of its crude oil with local refineries.

In addition, it competes for third-party services, and faces competition from renewable energy sources, such as wind and solar. In its carbon management business, it competes for the development of storage projects and agreements with emission sources.

My Opinion

California Resources Corporation is influenced by its focus on production as well as its efforts in carbon management and the energy transition. With FCF expectations and expecting a net zero full scope goal by 2045, I think that many investors may be interested in the company in the coming years. Besides, in my view, further global investment in companies conducting ESG practices like CRC could accelerate the demand for the stock. There are obvious risks because the business model relies heavily on the volatility of commodity prices, energy products, and competition in an evolving market. With that, only considering proven reserves and future production, I believe that the company appears a bit undervalued.

For further details see:

California Resources: Carbon Capture And Potential Separation From Oil Production