CRC - California Resources Corporation: Making Moves And Delivering Value

2023-10-11 03:54:26 ET

Summary

- California Resources Corporation is an oil and natural gas company facing regulatory challenges in California but still appealing due to rising share prices and potential earnings growth.

- CRC focuses on providing affordable and dependable energy while embracing cleaner and more sustainable solutions, including investing in renewables.

- The company's solid earnings performance, stable production, and potential for strong return on investment make it an attractive investment option.

Investment Rundown

Investing into oil and natural gas may not seem that out of the ordinary, but when the company is located in California, one of the most regulated states in the US when it comes to emissions it may seem odd. California Resources Corporation ( CRC ) may be facing a lot of regulatory issues and challenges, but I don't think that is enough to make the company that much less appealing. The share price has over the last few months risen quite significantly and now trades at a premium to the sector based on earnings. I do think that the rise in oil and gas prices in the last quarter is going to be displayed in the next quarterly report, and buying ahead of that seems like a good bet. Besides, CRC is distributing a decent dividend yield at 2% and has been buying back shares at a good rate for the last couple of years too.

Company Segments

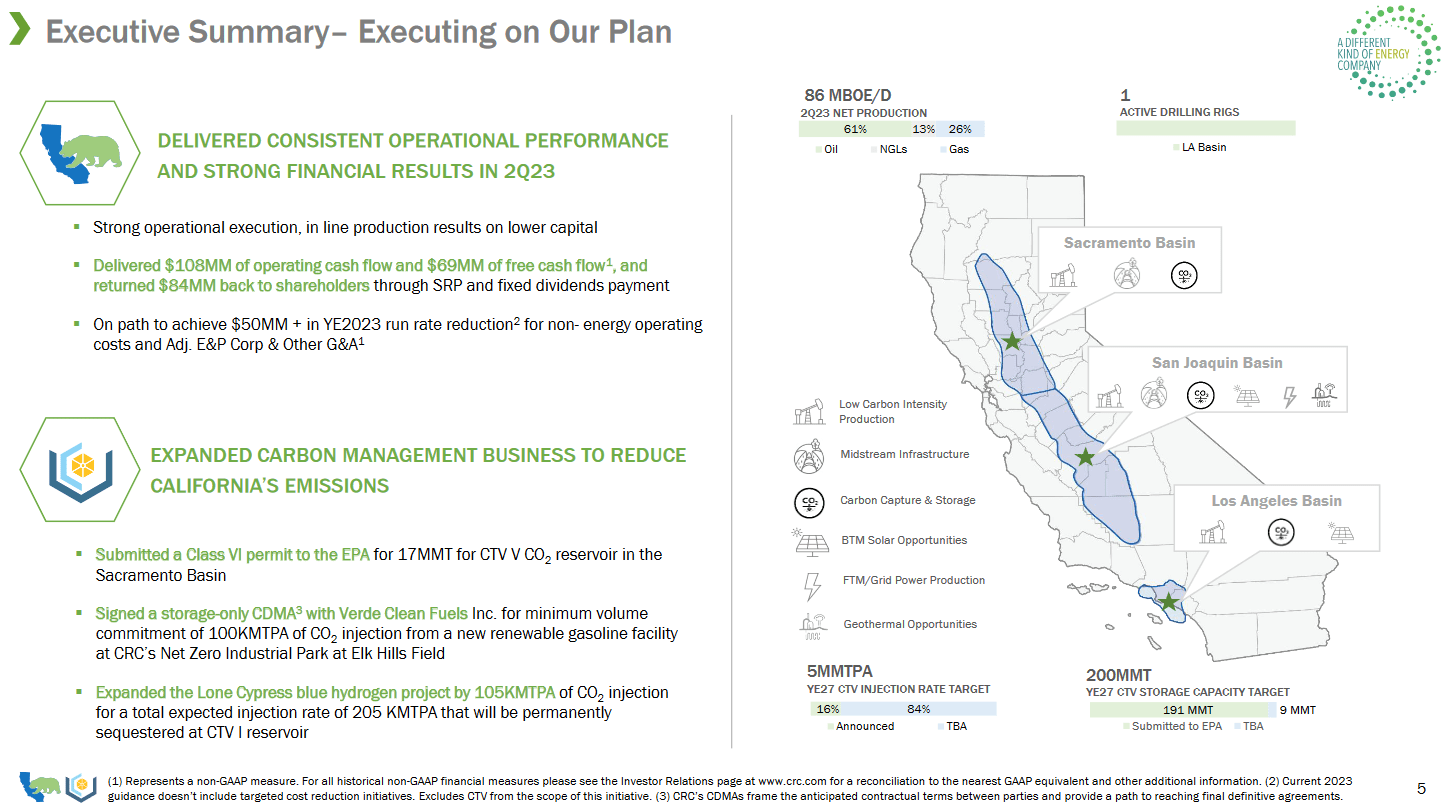

CRC is a dedicated independent player in the field of oil and natural gas exploration and production, with a unique focus on California as its exclusive operational territory. The company's core mission revolves around the provision of affordable and dependable energy, all while adhering to stringent safety and responsible operating standards. CRC's overarching objective is to enhance the quality of life for Californians and the local communities it serves.

{kind=link}

Furthermore, CRC has ventured into a collaborative joint effort aimed at advancing carbon capture and storage projects. These initiatives underscore CRC's dedication to embracing cleaner and more sustainable energy solutions, aligning its operations with the evolving landscape of environmental consciousness and responsibility. What I find the most appealing about the company is the fact that they are moving quite heavily into investing in renewables whilst also benefiting from having an existing asset base exposed to oil and gas that is bringing in consistent FCF growth over the long term.

Earnings Highlights

{kind=link}

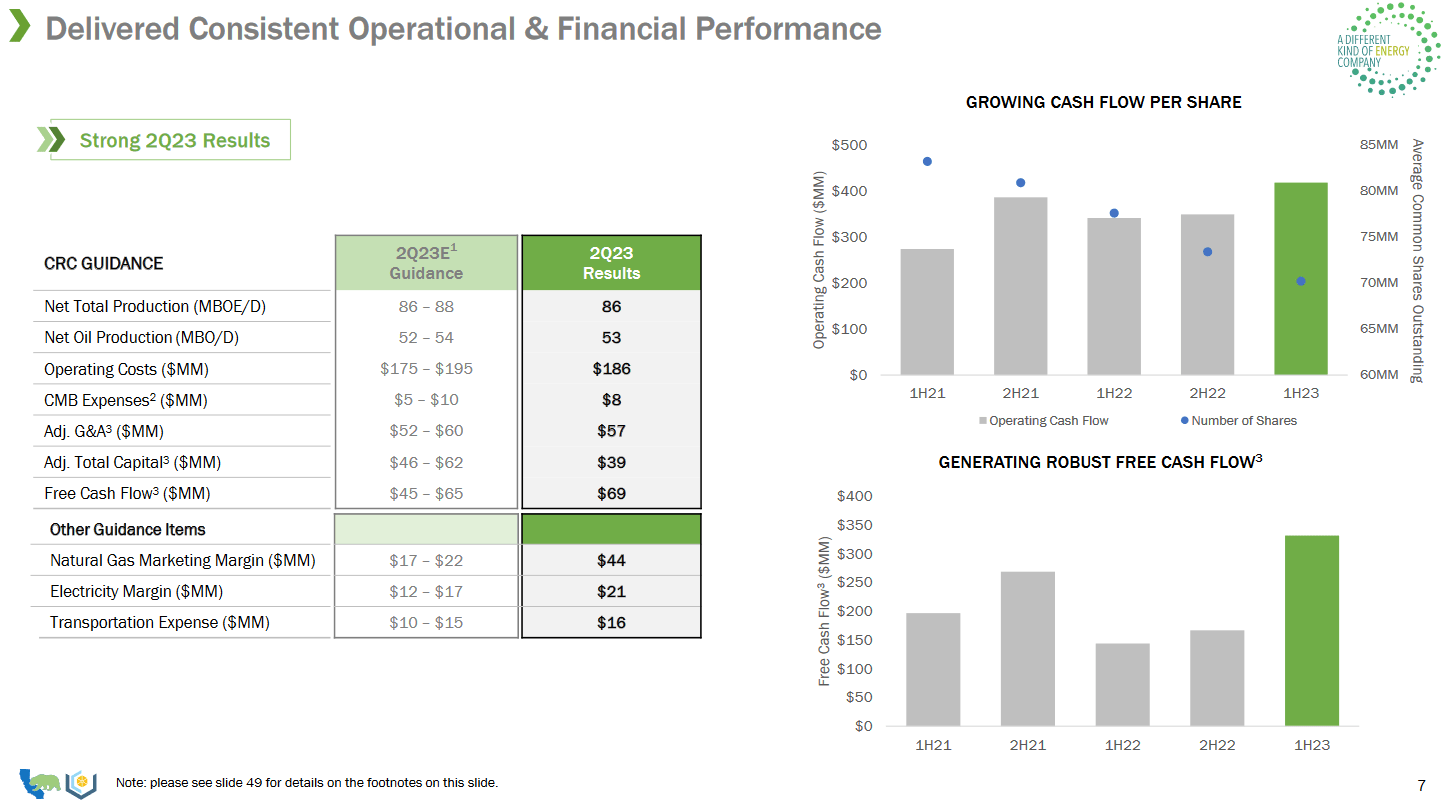

Looking at the last quarter from CRC I think the results are quite frankly very solid. The FCF per share has been growing despite some of the challenges that are mentioned in the risk segment. Furthermore, since the first half of 2021, the FCF has risen quite sharply. The price of oil has been rising very well over the summer and is quickly approaching $100. I think that there is a case to be made that oil will or could continue to rally to the end of the year as the need and demand for it usually rises during the winter months. How this will be reflected on CRC I think will come in the shape of growing earnings and higher FCF as well.

Investor Presentation

With more earnings, the company can continue on its path to returning large amounts of capital to its shareholders through both buybacks and dividends. So far around 60% of the FCF are used for these practices and I don't see it switching anytime soon either. Production for the company remains very stable and this means they can continue to generate positive FCF at least. What could upset it though would be a significant deterioration of oil and gas prices, but for that to happen I think a major event would have to occur, like an announcement of significantly more outputs and production rates.

2023 Guidance (Investor Presentation)

Guidance for 2023 includes around $360 - $460 million of FCF. If 60% is returned to shareholders that is around $276 million on the higher end of that estimate spectrum. This amount is enough to right now buy back nearly 10% of the outstanding shares for the business right now. I think these numbers underscore the potential that lies in CRC for delivering strong ROI for investors.

Valuation

As I have been quite bullish on the company throughout the article it may be good to give some targets as to when I think it constitutes a buy. Right now CRC trades at a FWD p/e of around 10, which is more or less in line with the rest of the sector. I would, however, be comfortable buying still at a p/e of 11 which is roughly 10% over the sector average. The reason is the quality of the business. This leaves a price target of $60 for CRC right now. Seeing as the price is below that it constitutes a buy right now. On an FCF basis, CRC is trading at a near 11% premium already, p/fcf 5.69 right now. Seeing as CRC has been able to so successfully deliver strong FCF growth over the years that should come with a higher multiple. A p/fcf of up to 6.5 is where I would consider CRC still a buy. All in all, the company continues to deliver a strong shareholder return through buybacks and dividends, and under $60 per share it remains a solid buy in my opinion. Should they manage to accelerate their margin expansion I can see a price target of up to $65 even in the short term.

Risks

CRC faces a unique set of challenges primarily stemming from the stringent regulatory environment in California. The state's regulatory framework imposes significant taxes and operational costs on companies operating within its borders. To navigate this landscape successfully and maintain robust FCF, CRC recognizes the imperative need to enhance its margins. Right now it seems that the FCF has been taking a hit as the rise in "other operating activities" has impacted it. Right now it sits at $308 million using the last 12 months' numbers and is putting a pin in CRC's ability to generate strong FCF.

Operating Activies (Seeking Alpha)

{kind=link}

CRC has embarked on an ambitious sustainability journey, with a clear commitment to achieving full-scope Net Zero emissions by the year 2045. While these sustainability goals align with the growing global emphasis on environmental responsibility, they are not without their complexities and risks. One of the primary challenges CRC faces in realizing these goals is the intricate web of operational, reputational, financial, and legal risks that accompany such a transformation.

Net Income (Seeking Alpha)

Operational challenges arise from the need to implement cleaner and more sustainable practices across its operations, which often involves significant capital investments and operational adjustments. Should there be a significant rise in projects halting or being set back on time I think investors' sentiment around the company may turn quite sour and the growth prospects adjusted, resulting in a drop in the share price.

Financials

Debt Levels (Seeking Alpha)

The debt levels of CRC have been decreasing quite quickly over the last few years and right now sit at the lowest point in a decade. That is a fantastic result as the company is generating stronger net incomes than a decade ago as well. With appreciation commodity prices I think that CRC could finance more debt build out more into the renewable space and secure market share here in California. With a lot of effort already going into it, adding more debt could accelerate that switch. With nearly 2x as much EBITDA as debt, I think CRC can afford to be a little bit more leveraged as well.

Final Words

CRC has been growing steadily over the years and has a better financial state than ever before. I think that the company will maintain its very shareholder-friendly practices like a significant amount of buybacks, but also a growing dividend yield. Despite the company rallying over the last few months, I think that it looks decently cheap still, given that the next report could very well display significant earnings growth because of the rise in both oil and gas prices. I am bullish on the business and will be giving it a buy right now.

For further details see:

California Resources Corporation: Making Moves And Delivering Value