TVTX - Calliditas Q1 Earnings: Buy The Dip On This GARP Commercial Biotech

2023-05-30 06:54:18 ET

Summary

- Patient and Prescriber Uptick: Despite Q1 2023's slightly disappointing earnings, Tarpeyo saw robust growth in new patient enrollments and prescriber numbers.

- Competitive Edge: Recent Phase 3 DUPLEX FSGS readout from Travere showing non-stat significant eGFR stabilization could potentially boost Tarpeyo's sales.

- Marketing Momentum: Calliditas' increased marketing investment, despite impacting EPS, is seen as a beneficial strategy for long-term sales.

- Path to Profitability: Despite potential commercial risks, strong prescriber momentum, Tarpeyo's distinctive dataset, and a healthy cash reserve suggest Calliditas could turn profitable by the end of 2023.

- We maintain a buy rating as we are bullish on Calliditas' a) Tarpeyo sales ramp in 2023, and b) bearish on Travere's PROTECT readout.

Key thesis update

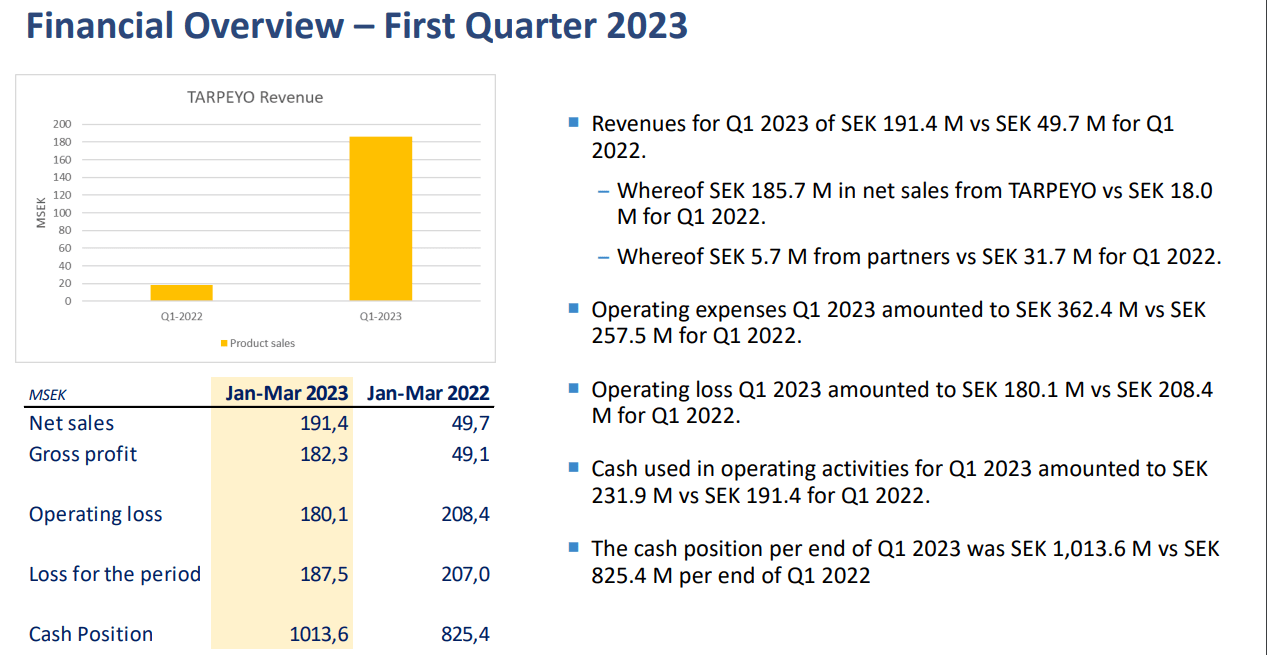

Calliditas Therapeutics ( CALT ) reported Q1 2023 earnings on May 16, where the company announced slightly disappointing earnings, lower than the street consensus (Tarpeyo sales of SEK 185.7M), and the stock has sold off ~30%, and we believe the current valuation is highly attractive for long-term investors.

{kind=link}

Financial Overview – First Quarter 2023 (Company IR deck)

We remain positive as new patient enrollment and Tarpeyo prescribers showed impressive growth, indicating a positive future sales ramp trajectory. We believe the Phase 3 NegIgArd data has also likely contributed to these increased enrollment numbers, demonstrating the drug's efficacy in modifying the trajectory of the IgAN. We remind readers that Calliditas's TARPEYO is the only drug approved that showed meaningful eGFR stabilization. Furthermore, we believe the recent disappointing phase 3 DUPLEX FSGS readout from Travere (that showed non-stat sig eGFR stabilization) should provide some degree of positive momentum to Calliditas's sales ramp as some prescribers may decide to forgo using sparsentan and initiate Tarpeyo as they want to start a disease-modifying therapy as soon as possible to prevent patients getting end-stage renal diseases (ESRD).

One of the biggest worries of some investors was around the potential market dilution of Sparsentan. We believe there is a high probability that the phase 3 PROTECT trial of Sparsentan would show no eGFR benefit over RAS inhibitors (irbesartan in the case of PROTECT trial (expected in Q4 2023)), similar to sparsentan's DUPLEX study, and that could jeopardize the full approvability of Sparsentan. If sparsentan gets pulled out of the market in YE 2023, we believe that should be a big catalyst for Calliditas and expect the stock to move meaningfully to the upside.

Summary of IgAN drugs:

Drug Company Description Status Reduction in proteinuria Tarpeyo Calliditas Oral formulation of budesonide Approved (accelerated); eGFR data reported Mar 2023 34% (31% pbo-adjusted) in ph3 Nefigard Filspari (sparsentan) Travere Oral endothelin type A & angiotensin II type 1 inhibitor Approved (accelerated); eGFR data due Q4 2023 50% (35 points adjusted for irbesartan control) in ph3 Protect Narsoplimab (OMS721) Omeros Anti-MASP2 antibody Ph3 Artemis-IgAN ; proteinuria data due mid-2023 64% (no control arm) in ph2 Atrasentan Chinook Oral endothelin A receptor inhibitor Ph3 Align ; proteinuria data due H2 2023 55% (no control arm) in ph2 Affinity Iptacopan (LNP023) Novartis Oral complement factor B inhibitor Ph3 Applause-IgAN ; proteinuria data due H2 2023 23% pbo-adjusted in ph2 * Sibeprenlimab (VIS649) Otsuka Anti-April antibody Ph3 Visionary ends Dec 2026 43% pbo-adjusted in ph2 ** *At highest dose (200mg BID); **pooled data with IV doses 2mg, 4mg & 8mg monthly. Source: Evaluate Pharma & clinicaltrials.gov. Source: Evaluate Pharma

Continued investment in sales and marketing

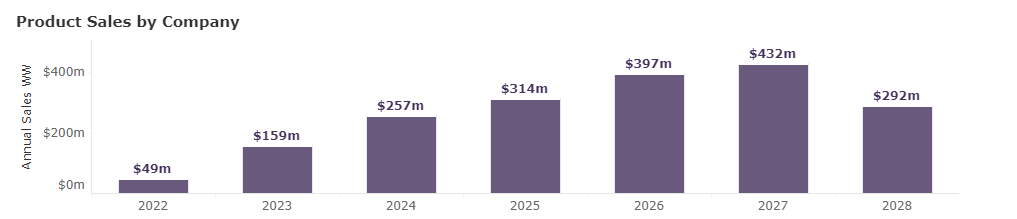

Furthermore, we note that the company is spending more on sales and marketing than expected, highlighted by lower EPS than the street consensus, SEK -3.49 vs. SEK -3.44. We believe aggressive investment in sales and marketing, and market access should be a net positive for the long-term sales ramp. Therefore, although Q1 2023 sales were slightly underwhelming, we stick with our estimate around 2023 FY revenue of +$120m (lower range of the company's guidance of $120m-$150m) considering the cyclicality of the inventory management (of distributors) and increasing prescriber momentum that we have observed in Q1 2023. We believe the stock should trend higher if the FY2023 sales surpass anywhere above $100m, considering the modest valuation of the company (enterprise value of $446m) and compelling peak sales estimate of ~$400m. Using a conservative peak sales multiple of x3 (commonly used in biotech valuation), the stock should be trading around $1.2Bn.

Street consensus on TARPEYO sales

{kind=link}

WW indication sales (Evaluate Pharma data)

Risks

-

Increased Competition: Calliditas's primary product, Tarpeyo, is currently one of only two approved treatments for IgA nephropathy (IgAN). However, the market for IgAN therapies is becoming increasingly competitive, with new treatments being developed that may have more targeted and potentially superior clinical profiles. This could potentially affect Tarpeyo's long-term market share and profitability.

-

Dependence on Tarpeyo Success: The company's future financial performance is heavily reliant on the success of Tarpeyo. Any setback in sales or issues regarding safety, efficacy, or regulatory approval could significantly impact the company's stock price and overall business performance.

-

Regulatory Risks: As a biotech company, Calliditas faces inherent regulatory risks. While Tarpeyo is approved for use in the treatment of IgAN, any changes in regulatory standards or unexpected regulatory issues could disrupt the sales of Tarpeyo, impacting the company's revenue.

-

High Marketing Costs: Calliditas reported higher-than-expected selling and marketing costs in its 1Q23 report. While these costs are part of the company's strategy to ensure the successful launch and uptake of Tarpeyo, continued high expenses may negatively impact the company's bottom line if sales growth does not meet expectations.

Conclusion

We maintain a buy rating even with slightly underwhelming Q1 2023 sales due to a) growing prescriber momentum shown (just except for Jan 2023), b) competitor product sparsentan's phase 3 DUPLEX data showing no stat sig eGFR, and c) updated Phase 3 NegIgArd data slowly, but steadily driving prescriber momentum, which we believe will continue considering Tarpeyo's differentiated dataset on hand. We believe the company's $97m cash is reassuring, and we believe it would (at least) provide ~2+ years of the runway (~$20m cash burn/quarter), and considering the trajectory of Tarpeyo's sales ramp, we expect the company to reach profitability by YE 2023.

For further details see:

Calliditas Q1 Earnings: Buy The Dip On This GARP Commercial Biotech