CALT - Calliditas: Q2 Earnings De-Risk This Biotech Play 2024 Expected To Be Inflection Point

2023-09-03 04:26:46 ET

Summary

- Calliditas Therapeutics downgrades Tarpeyo sales guidance due to slower-than-expected sales growth and market access challenges.

- Potential growth drivers include full-label expansion of Tarpeyo and addressing the educational gap about the duration of treatment.

- Delays in the TRANSFORM trial of setanaxib pose risks, but management remains optimistic about potential partnering discussions.

- We reiterate our non-consensus buy rating moving into 2H 2023 and see 2024 as a potential inflection point for the stock.

Reason for the update: Q2 earnings and change to our thesis moving forward

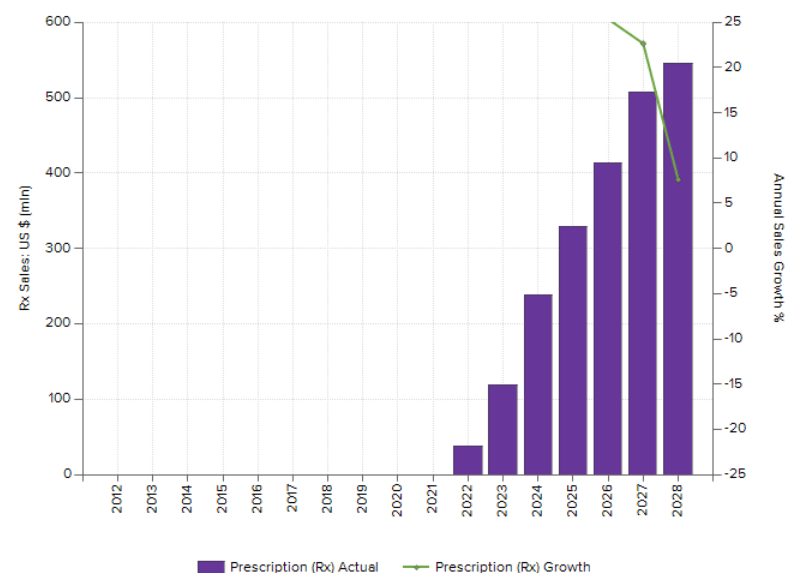

Calliditas recently announced Q2 2023 earnings; during the call , Calliditas Therapeutics ( CALT ) management reported a downgrade in Tarpeyo sales guidance from $120-150M to $100-120M. This alteration was attributed to the slower-than-expected sales growth of Nefecon (marketed as Tarpeyo in the U.S.). Market access friction was identified as a chief impediment, with 15-20% of prescribed patients still awaiting payer approval and an estimated 5-15% potentially opting out of Tarpeyo treatment due to challenges with their payers. Though these numbers were below expectations, CALT made promising strides in commercial success, adding a significant 422 new patients and 232 new prescribers within the quarter, which we find highly reassuring.

For Calliditas, several potential growth drivers loom on the horizon. Anticipation surrounds the full-label expansion of Tarpeyo, particularly if the PDUFA slated for December 20, 2023, grants full approval. Such approval could expand the label to include patients with UPCR>0.8g/g, mitigating current market access challenges and strengthening its foothold. Furthermore, we believe addressing the educational gap about the Tarpeyo duration of treatment is key. While the average duration currently sits at roughly eight months, management emphasized that with better familiarity, physicians might extend treatment, and recurrent treatment cycles could further bolster topline growth over time. We believe the results of the ongoing physician detailing will result in better-than-expected earnings during 2024 and see 2H 2023 as a buying opportunity, especially at the current "depressed" valuation.

{kind=link}

Pipeline expansion optionality is not valued appropriately by the market.

Another crucial update revolves around the TRANSFORM trial of setanaxib, which experienced delays. Originally anticipated for 1H 2024, the readout is now pushed to mid-2024 due to slower study enrollments and subsequent regulatory discussions. Despite the setback, management remains optimistic, expecting the data to guide the next stages of the trial and open doors for potential partnering discussions. Additionally, data from the Ph2 evaluation of setanaxib in HNSCC is scheduled for 1H24, with a PoC study targeting Alport syndrome set for 2H23 initiation.

Sufficient Funding for Operations

At the end of 2Q23, Calliditas reported approximately SEK866M in cash and cash equivalents, and considering that the company burnt SEK255.2M during the first six months of 2023, we believe the company to have at least 1-2 years of cash runway, which is highly assuring. Furthermore, considering the continued, slow but steady ramp of Tarpeyo, we believe that the company shouldn't need to raise capital anytime soon and the dilution risk remains low at this point.

Risk to thesis

However, potential risks in investing in CALT are undeniable. The slower ramp in Tarpeyo sales and the revised lower share in IgAN impact the company's peak sales projections. Current challenges with payer friction and market access, if unresolved, could continually plague the growth trajectory of Tarpeyo, even with full approval.

Conclusion

In summary, our core thesis hinges on the undervaluation of CALT. The market has exhibited a strong knee-jerk reaction to the lowered sales print. Yet, given the prospective levers the company can engage, particularly with the potential full approval and label expansion of Tarpeyo, we forecast 2024 as a turning point. Sales are predicted to ascend, surpassing consensus, especially since analyst projections are expected to continuously turn conservative due to current updates moving into Q4 2023. Furthermore, we believe the company's mid-stage clinical developments have not been properly priced into the valuation.

For further details see:

Calliditas: Q2 Earnings De-Risk This Biotech Play, 2024 Expected To Be Inflection Point