CLTEF - Calliditas: Riding The Setanaxib Wave And Betting On Tarpeyo's Triumph

2023-07-20 18:36:07 ET

Summary

- We maintain a buy rating due to promising interim data from the Phase II trial of setanaxib in patients with squamous cell carcinoma of the head and neck and potential Q2 earnings from Tarpeyo's sales.

- Despite promising interim data, the market has yet to appreciate the potential of setanaxib, which could impact the company's short-term stock performance. The company's cash holdings are robust.

- Calliditas is investing heavily in the Tarpeyo launch; we believe the Tarpeyo sales could hit consensus estimate of ~$120m in 2023.

- Current depressed valuations offer an attractive entry point for long-term investors, before the Q2 2023 earnings release.

Purpose of this update: new clinical data and pre-Q2 earnings update

We maintain a buy rating on Calliditas Therapeutics (CALT) due to a) recent interim data from the proof-of-concept Phase II trial with setanaxib in patients with squamous cell carcinoma of the head and neck (SCCHN) and b) the growth potential (potential earnings surprise for Q2) from Tarpeyo's sales.

Please read our previous article discussing our optimism about Tarpeyo's sales moving forward.

New interim data on Setanaxib is likely not appreciated by the market

We believe the new interim data from the Phase II trial of setanaxib appears promising, with early clinical progression-free survival ((PFS)) results supporting the presumed anti-fibrotic mode of action of setanaxib. The transcriptomic analysis displayed treatment impact on fibrosis-related signaling pathways, providing encouraging evidence for setanaxib's potential effectiveness against SCCHN. Despite the small sample size and patient population heterogeneity, these findings should stimulate some degree of investor interest, offering substantial potential upside for Calliditas if the drug proves successful in the ongoing TRANSFORM study.

selleckchem (selleckchem)

We believe it is noteworthy that GKT137831 stands out as an innovative and exciting first-of-its-kind compound that inhibits both NOX1 and NOX4 enzymes. Studies indicate that Nicotinamide-adenine dinucleotide phosphate (NADPH) oxidases, known as NOX enzymes, come in seven variants and are responsible for producing reactive oxygen species ((ROS)). ROS can inflict tissue damage and alter critical biological pathways, potentially contributing to a variety of diseases, including metabolic, cardiovascular, pulmonary, and neurological conditions. In the context of the kidney, NOX4 is the predominant NOX enzyme expressed.

BTVI's pointer form summary of the new data published on July 13:

Design

- The trial is a Phase II, double-blind, randomized, placebo-controlled, proof-of-concept investigation.

- The trial evaluates the efficacy of 800mg setanaxib twice a day in combination with 200mg pembrolizumab IV every three weeks, which is a standard treatment protocol for SCCHN.

- A minimum of 50 patients with moderate or high CAF-density tumors are involved in the study.

- Tumor biopsies are performed before treatment initiation and after nine weeks of treatment.

- Treatment continues until the toxicity becomes intolerable or there is tumor progression, as per typical oncology trial procedures.

Results

- The interim analysis involved 20 patients with recurring or metastatic SCCHN, 16 of which had assessable tumor size and PFS data.

- Pre and post-treatment tumor biopsies were available from 12 patients for the biomarker analysis that included transcriptomic analysis and evaluation of pathology markers such as SMA, Foxp3 regulatory T cells, and PDL-1 CPS.

- The small sample size and diverse patient population necessitate caution in interpreting the interim analysis findings.

- The transcriptomic analysis revealed the treatment influenced two fibrosis-related signaling pathways, endorsing the proposed mode of action related to activated fibroblast modulation.

- Pathological examination showed initial signs of increased immunological activity within the tumors treated with setanaxib, alongside beneficial changes in Foxp3 and PDL-1 CPS. Clear conclusions about setanaxib's impact on SMA reduction remain elusive due to unbalanced baseline SMA levels and small biopsy samples.

- Regarding PFS, 7 out of 16 assessable patients showed no progression, with stable disease or partial response. Among these, six were on setanaxib, with six still receiving the study drug at the time of data read-out. The longest drug administration period reported was 21 weeks for a patient on setanaxib.

BTVI Conclusion: The analysis offers preliminary PFS results and supports setanaxib's presumed anti-fibrotic mode of action.

Financial

The company's ~ $ 97m cash holding is robust for a SMID cap biotech, and we believe this cash buffer could provide almost two years of the runway, considering that the company is burning approximately $20m per quarter. Furthermore, considering the trajectory of Tarpeyo's sales ramp, we believe the company will be able to reach profitability by year-end 2023 or 2024.

Risks

-

Clinical Risk: The interim results from the ongoing Phase II trial with setanaxib demonstrate promise but come from a small, diverse patient pool, which could lead to uncertain final outcomes.

-

Market Perception Risk: Despite promising interim data, the market has yet to appreciate the potential of setanaxib, which could impact the company's short-term stock performance.

-

Financial Risk: Though the company maintains a strong cash position, its burn rate is high at about $20 million per quarter, which might necessitate additional funding if revenue generation from Tarpeyo sales or other sources does not meet expectations.

-

Sales Performance Risk: After an underwhelming Q1 performance for Tarpeyo, there's a risk that the product might not achieve the expected uptake, impacting future revenue. If the anticipated growth in Tarpeyo's sales and the expected profitability by the end of 2023 or 2024 don't materialize, the company could face financial challenges.

Conclusion: The stock is trading at oversold territory

Net-net, the combination of promising trial data from Setanaxib (which the market is not appreciating at all, in our opinion), the upward trajectory of Tarpeyo's sales, and the significant ex-US market opportunities lead us to maintain a buy rating on Calliditas.

We remind readers that Calliditas sold off 37% after announcing underwhelming Tarpeyo's sales in Q1 2023. We believe this caused an exaggerated market reaction that we believe was unjustified. Even though the new patient enrollments started slower in January, they increased throughout the quarter, reaching a record of 408 new enrollments. This uptick signals the potential for a solid Tarpeyo uptake in the near future. Additionally, Calliditas is investing heavily in the Tarpeyo launch, a strategic move that we think is necessary for the product's longer-term success despite it resulting in a short-term increase in expenses. With the projected growth in patient numbers and physician awareness of the Phase 3 NefigArd data, we anticipate Tarpeyo's sales will continue to rise, providing substantial upside for the company. Considering the depressed valuation, we believe Q2 earnings could lead to a meaningful appreciation if the Tarpeyo sales hit consensus.

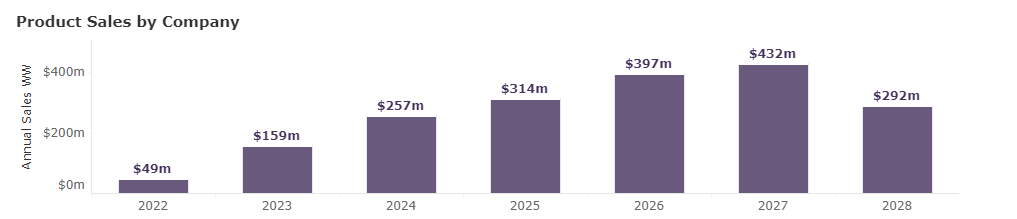

WW indication sales (Evaluate)

{kind=link}

On a full-year basis, we stand by our estimate of ~2023 FY revenue of +$120m, which is the lower range of the company's guidance of $120-$150m. Furthermore, we are a big fan of Tarpeyo's upside potential on ex-US opportunities, particularly in China, Europe, and Japan, through strategic partnerships/licensing agreements for Nefecon that Calliditas would be eligible for royalty payments. We believe the largest IgAN patient population is in China, where Nefecon is expected to achieve a first-to-market advantage, potentially generating substantial revenues in the near future.

For further details see:

Calliditas: Riding The Setanaxib Wave And Betting On Tarpeyo's Triumph