CLTEF - Calliditas Therapeutics: Undervalued Rare Disease Commercial Stage Biotech (Maintaining Buy)

2023-11-27 18:40:01 ET

Summary

- Q3 2023 sales for Calliditas Therapeutics' flagship drug Tarpeyo fell short of expectations but showed incremental growth.

- Despite challenges, the number of prescribers and improvements in market access for Tarpeyo indicate long-term success.

- 2024 is expected to be an inflection point for the company, with full approval of Tarpeyo and positive Phase III data.

- We maintain a buy rating on Calliditas Therapeutics.

Background

In our previous post-Q2 2023 earnings note , we maintained a buy rating on Calliditas Therapeutics AB (publ) (CALT) based on two key theses: a) the sales ramp of Tarpeyo accelerating in 2024 with the label expansion and improvement in market access, and b) label expansion around disease modifying claim and full approval (positive catalyst for the stock considering that Tarpeyo would be the first agent).

In this article, we focus on key updates disclosed by the company around Tarpeyo's market launch and important market launch metrics. Although the Q3 2023 sales print may look a little soft, we continue to believe 2024 to be an inflection point, as such, we maintain a buy rating on CALT. Please read our initiation article for a deep dive into the company's technology and the lead product Tarpeyo.

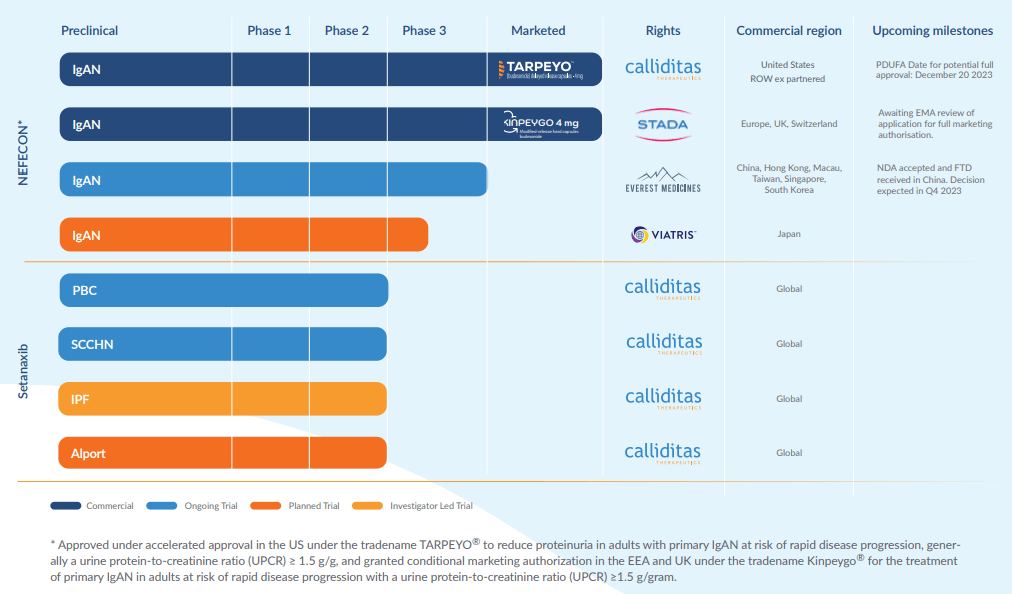

CALT Pipeline Overview (Company IR deck)

{kind=link}

Q3 2023 Earnings and Tarpeyo's Launch

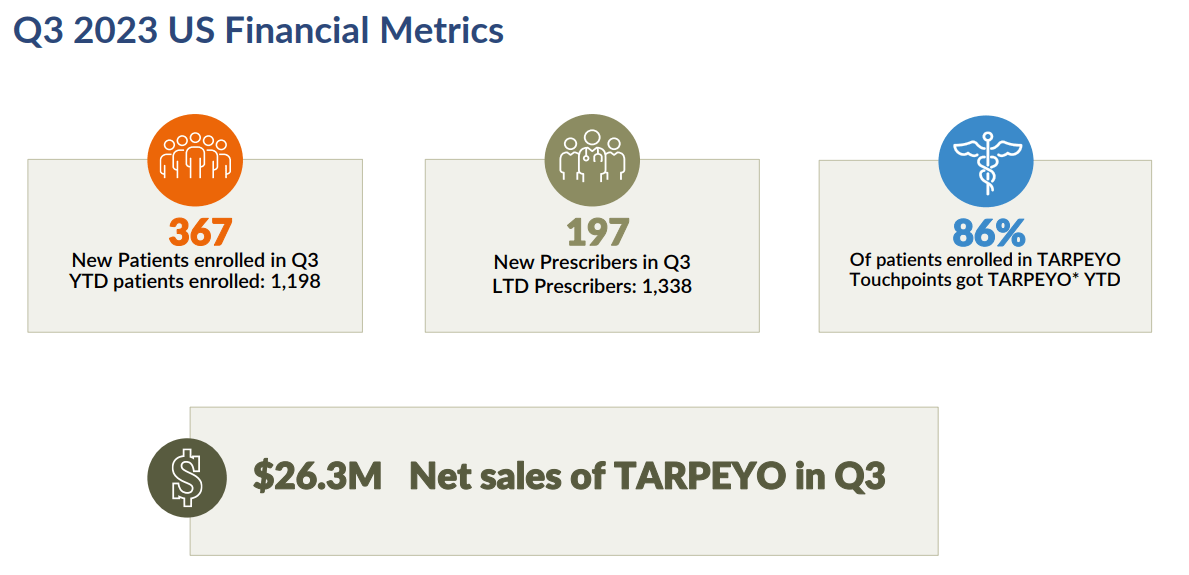

In the third quarter of 2023 , Calliditas Therapeutics AB (publ) ((CALT)) reported earnings: while falling short of street expectations, revealed crucial insights into the company's trajectory and potential. The period was marked by the launch metrics of their flagship drug, Tarpeyo, aimed at treating IgA Nephropathy (IgAN). We believe the earnings miss was largely attributed to a combination of summer seasonality and turnover within the sales team, which temporarily slowed patient service forms (PSFs) and affected overall sales performance. Despite these challenges, the quarter ended on a promising note - a continued growth in the number of prescribers and improvements in market access, which are critical for long-term success. Importantly, CALT reiterated its revenue guidance for 2023, projecting sales between $100 and $120 million. In the face of a challenging quarter, we believe this reiteration underscores the management's confidence in Tarpeyo's market potential and the drug's foundational role in CALT's portfolio. The quarter also saw a significant growth in patient enrollments and unique prescribers for Tarpeyo, indicating a strong underlying demand for the drug.

BTVI summary of launch metrics

{kind=link}

-

Quarterly Sales Figures : The Q3 sales for Tarpeyo were reported at $26.3 million, which was below the expectations set by analysts (the consensus was around $29 million). This figure, however, represented an incremental growth from the previous quarters, with $24.7 million in Q2 and $17.8 million in Q1.

-

Patient Enrollments : During the third quarter, there were 367 new patient enrollments for Tarpeyo. This was a decrease compared to 422 enrollments in Q2 and 408 in Q1. The total patient enrollments to date reached approximately 2237, compared to 1870 in Q2 and 1447 in Q1.

-

Unique Prescribers : The number of unique prescribers for Tarpeyo was 197 in Q3, which showed a slight decline from 232 in Q2. The cumulative number of unique prescribers exceeded 1,338 by the end of Q3.

-

Prescription Service Forms (PSFs) Conversion Rate : The conversion rate for PSFs remained stable at 86%, consistent with the rate in Q2. This indicates a high level of effectiveness in turning prescriptions into actual patient treatments.

-

Market Coverage : The drug maintained a strong market coverage with over 90% of lives covered (approximately 70% through commercial/cash payers and the majority of the rest through Medicare/Medicaid). We see Tarpeyo predominantly covered by private payors positively as private payors tend to place less intensive step-edits or prior authorizations and are more generous with gross-to-net discounts, unlike public payors.

-

Price Stability : Management indicated no plans to increase the price of Tarpeyo following the anticipated 'full' approval. As such, we don't expect any negative surprises due to the company cutting the drug price moving forward.

Many positive catalysts in 2024

Looking ahead to 2024, there are several reasons to believe that it could be an inflection point for CALT. The expected 'full' approval of Tarpeyo, with eGFR data inclusion on the label, is a pivotal event scheduled for December 20, 2023. This full approval is anticipated to bolster the drug's market position, given that Tarpeyo would be the first drug granted full approval based on the eGFR endpoint following accelerated approval based on the UPCR endpoint. Moreover, the positive Phase III two-year data and a planned expansion of the sales force are likely to enhance CALT's market reach and impact in 2024.

Competitors thinning

With the recent failure of Narsoplimab from Omeros Corporation ( OMER ) and Travere's Sparsentan's phase 3 trial blowing up, we expect the potential threats in the IgAN landscape have narrowed down considerably. We believe, especially with Tarpeyo's label expansion on disease modification and eGFR stabilization/slowing down should add a tremendous tailwind to the current market ramp.

Competitive dynamics within IgAN Space - Evaluate Pharma data

Drug Company Description Status Reduction in proteinuria Tarpeyo Calliditas Oral formulation of budesonide Approved (accelerated); eGFR data reported Mar 2023 34% (31% pbo-adjusted) in ph3 Nefigard Filspari (sparsentan) Travere Oral endothelin type A & angiotensin II type 1 inhibitor Approved (accelerated); eGFR data due Q4 2023 50% (35 points adjusted for irbesartan control) in ph3 Protect Narsoplimab (OMS721) Omeros Anti-MASP2 antibody Ph3 Artemis-IgAN trial failed Phase 3 failed Atrasentan Chinook Oral endothelin A receptor inhibitor Ph3 Align ; proteinuria data due H2 2023 55% (no control arm) in ph2 Affinity Iptacopan (LNP023) Novartis Oral complement factor B inhibitor Ph3 Applause-IgAN ; proteinuria data due H2 2023 23% pbo-adjusted in ph2 * Sibeprenlimab (VIS649) Otsuka Anti-April antibody Ph3 Visionary ends Dec 2026 43% pbo-adjusted in ph2 **

Sufficient Funding for Operations

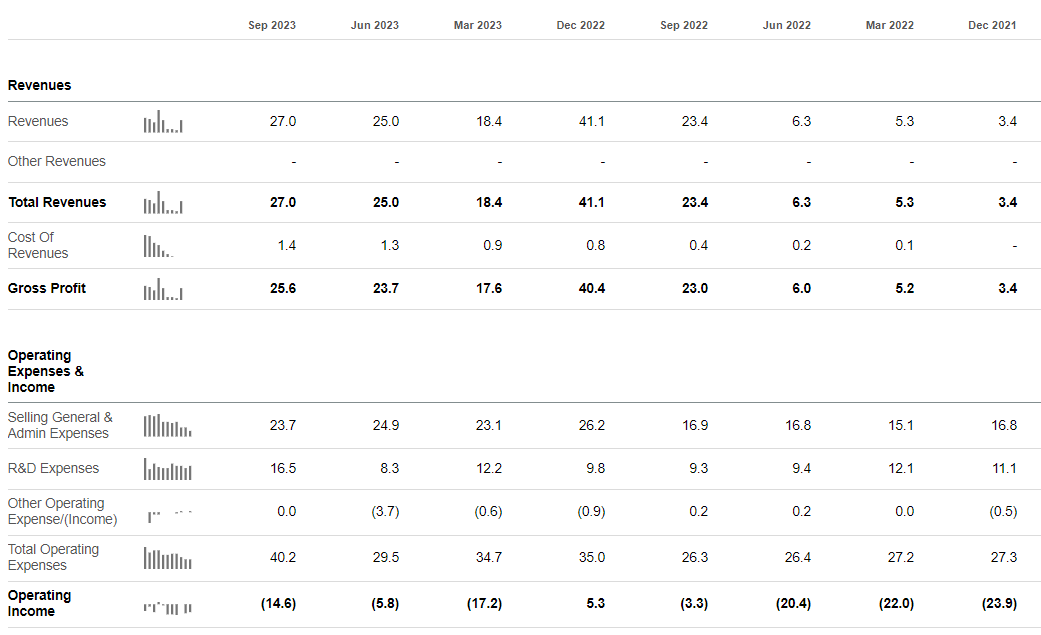

At the end of 3Q23, the company reported ~US$72m in cash and cash equivalents, and considering that the company burnt SEK40-50M during the last few years, we believe the company to have at least 1-2 years of cash runway. This is a robust cash runway for a SMID cap biotech, which gives us comfort in maintaining a buy rating on Calliditas. To achieve cash flow breakeven, we believe CALT needs Tarpeyo net sales to reach approximately $40 million in quarterly revenue. This milestone could be attained as early as Q4 2023 if Tarpeyo sales align with the higher end of the $100-$120 million guidance range.

CALT Income Statement (SeekingAlpha)

{kind=link}

Risk factors

-

Dependency on Tarpeyo's Success : CALT's current and future financial performance is heavily reliant on the success of Tarpeyo, their leading drug for treating IgA Nephropathy (IgAN). This includes risks related to the drug's market adoption, pricing strategy, competitive landscape, and continued regulatory approval. Any setbacks in these areas could significantly impact CALT's revenue and growth prospects.

-

Clinical Trial Outcomes for Pipeline Products : While Tarpeyo is the flagship product, CALT is also developing other drugs. The company's future growth depends on the successful outcome of clinical trials for these pipeline products. Unfavorable results or delays in these trials could hinder the company's ability to diversify its product portfolio and reduce dependency on a single product.

-

Market Penetration and Reimbursement in Different Regions : CALT faces the challenge of penetrating diverse markets with varying regulatory and reimbursement landscapes, including the U.S., EU, and China. Successfully navigating these different healthcare systems and achieving favorable reimbursement terms is critical for Tarpeyo's global success. Any difficulties in these areas could limit market access and revenue potential.

-

Regulatory Risks in Expanding Indications : CALT's strategy includes expanding the indications for which Tarpeyo is approved, such as seeking a label expansion based on eGFR data. This process involves regulatory risks, including the possibility of not receiving approval for expanded indications or facing delays. The outcome of these regulatory processes can significantly impact the drug's market potential and the company's growth trajectory.

Conclusion

Net-net, we maintain a buy rating moving into 2024. While the Q3 2023 earnings did not meet street expectations, the underlying launch metrics of Tarpeyo's launch and the strategic moves by CALT suggest a potential inflection point in 2024. Furthermore, the recent failure of OMER's Narsoplimab and Travere's Sparsentan should only solidify Tarpeyo's market positioning as the only approved therapy for IgAN that can slow down the progression of the disease. Lastly, we appreciate CALT's robust cash runway and potential cashflow positive status moving into 2024.

For further details see:

Calliditas Therapeutics: Undervalued Rare Disease Commercial Stage Biotech (Maintaining Buy)