CPE - Callon Petroleum: Acquiring Its Way Into Mediocrity

2023-09-10 11:18:29 ET

Summary

- Callon Petroleum's management made a costly mistake that resulted in an impairment charge of about $400 million.

- Management may make the same mistake by purchasing Permian acreage while selling usually cheaper Eagle Ford acreage that in the past performed just as well.

- Investors should consider alternatives like Hess Corporation, which has a clear line of sight to future earnings and reduced execution risk through its partnership with Exxon Mobil in Guyana.

- Another alternative is Baytex Energy with the very low cost Clearwater Play.

- Investors pay management find a bargain. Both Hess and Baytex did that.

Callon Petroleum ( CPE ) has long been a market darling. But the management that got the company to market darling status has been long gone. The current management sold the Eagle Ford acreage while acquiring Permian acreage. But that trend is so established that the Permian acreage is often very expensive to purchase. In fact, management probably should have expanded the Eagle Ford acreage while selling the Permian acreage.

The Permian acreage has long been "the place to be". It is well established that this acreage produces excellent profitability results. But the key is what you pay for the geology you have acquired. This is where management's track record falls apart. The latest quarterly earnings contains an impairment charge of more than $400 million.

An impairment charge during a time of strengthening oil and gas prices is exceedingly rare. This would indicate a management valuation error (that led to an overpayment or a development overinvestment) in the past that has now cost shareholders.

Managements that discuss fully something like that impairment charge rarely repeat it. As the press release shows, there is really little to no discussion of the charge. That could imply a higher chance of another impairment charge in the future. What shareholders need is a discussion of the history that led to the charge and how management will avoid it in the future or with the current transactions.

Not only that, but since the Permian is "the place to be", the midstream capacity has often been overwhelmed by production increases. This has led to selling price discounting and very high transportation costs to get the product to market. That is especially true for newcomers that "buy now and worry later" as that impairment charge appears to indicate.

Management touts the margins and the productivity that is supposed to be above average. But impairment charges in the current pricing environment just do not happen if that is the case. Investors need to see gains on sales of acreage should management be correct about the progress made for the price paid.

Put this down as a huge investment red flag.

Furthermore, the Eagle Ford has not had the takeaway issues of the Permian. Oftentimes, production from the Eagle Ford usually sells at a premium. The acreage prices are not nearly as competitive as the Permian acreage and the sales prices often reflect this. The result is often that the Eagle Ford acreage often "unexpectedly" outperforms the Permian acreage in the business cycle due issues like takeaway capacity of midstream.

More to the point, investors really should not be paying management for "safe purchases that are often full value (or as the impairment charge implies, full value plus). Investors should be paying management to find bargains in places that other companies have not yet found. Then the entry fee can be very cheap. Management should also have paid more attention to the Eagle Ford as acreage there is not nearly as competitive. But the results are often as good or better than pricier places because of actual execution issues.

Let's look at some alternatives to this situation.

Hess Corporation

There are a lot of investors that believe that Hess (HES) is expensive because it sells at a relatively high price-earnings ratio. But Hess has a clear line of sight to a lot more earnings in the future than is the case for many upstream companies. Furthermore, that "line of sight" is nailed down far better than is typically the case.

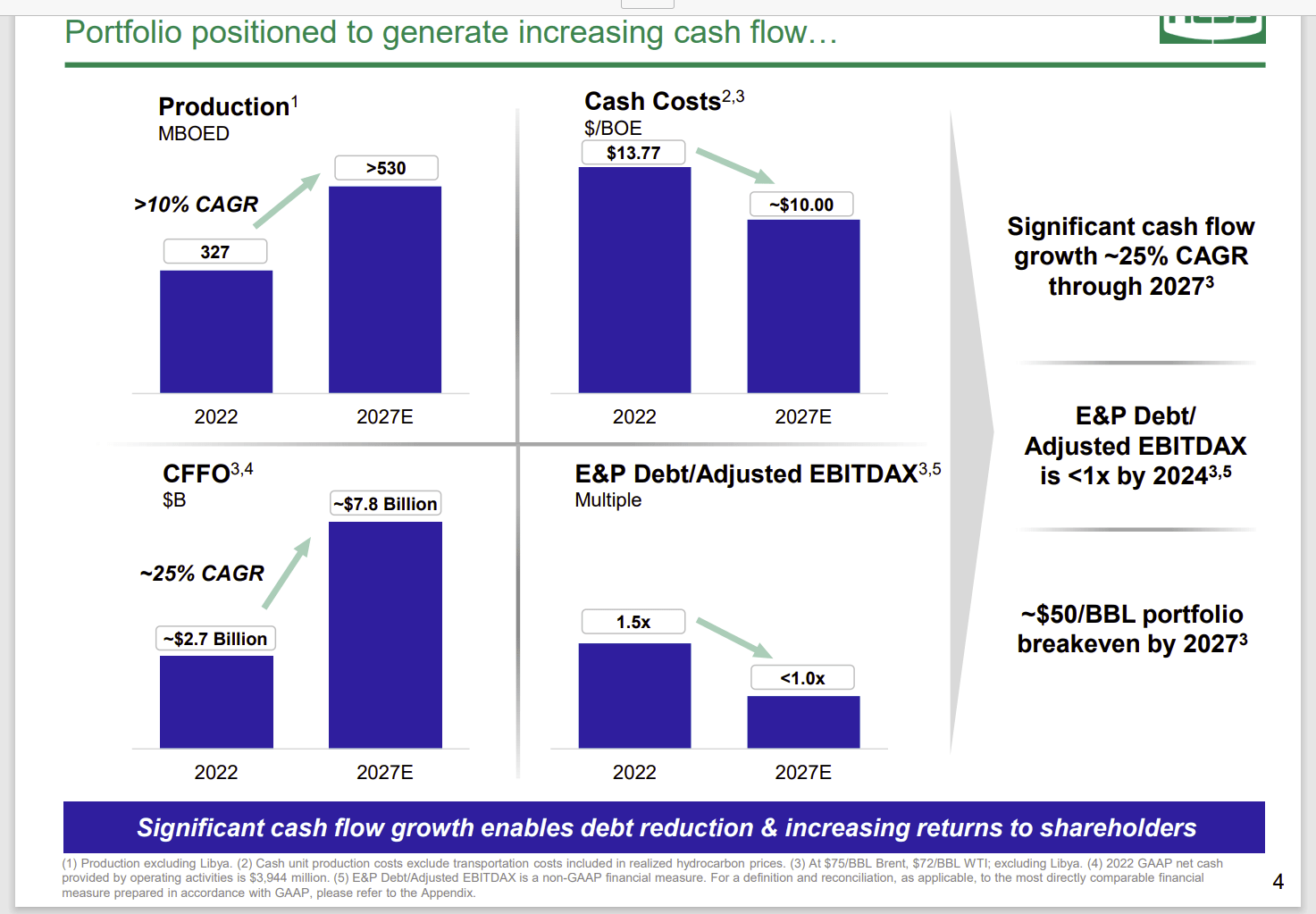

Hess Corporation Management Growth Guidance Summary (Hess Corporation Presentation At Barclay's CEO Energy Power Conference September 2023)

{kind=link}

Hess is part of a partnership operated by Exxon Mobil ( XOM ) that has found some of the lowest cost breakeven point production in Guyana. Even if there was never another discovery, Hess will still grow profits at a 25% compounded rate of return as shown above. That will triple cash flow from operating activities assuming that the oil price is at Brent $75 ($72 WTI). This is a price that is low compared to current prices.

Notice that cash flow is growing far faster than production. This is due to the very low breakeven prices of Guyana production as well as the fact that offshore projects demand a lot of cash up front. There is a relatively large depreciation component throughout the life of the project to protect cash flow from taxes.

Not only that but the partnership can now justify 10 FPSO's which should assure fairly rapid profit growth through at least the end of the decade.

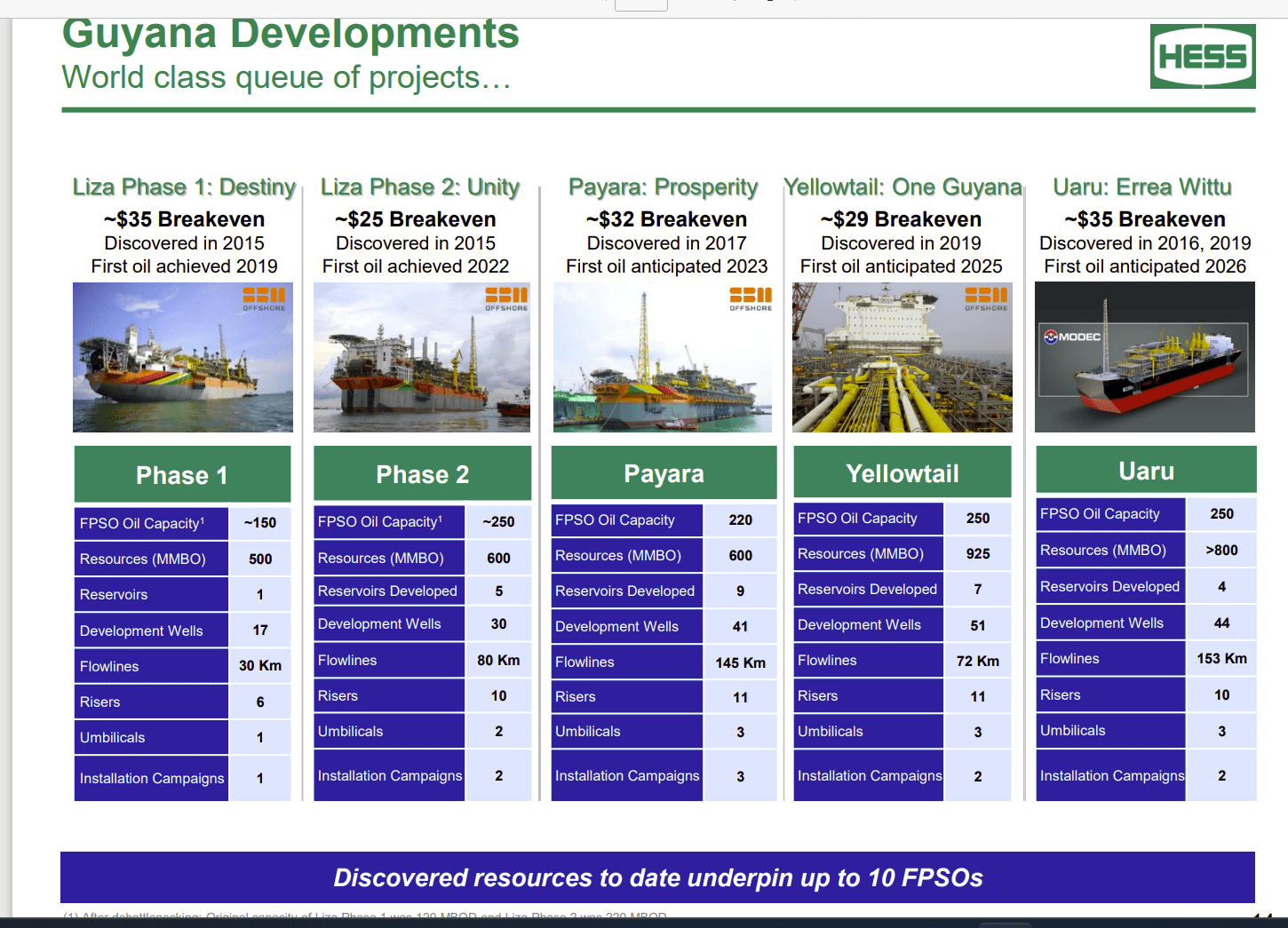

Hess Corporation Summary Of Approved FPSO Projects (Hess Presentation At Barclay's CEO Energy Power Conference September 2023)

{kind=link}

Having Exxon Mobil as the partnership operator sharply reduces a lot of execution risk. As shown above there are already 5 projects that have been approved. The third FPSO (Floating Production Storage And Offloading) will soon begin production.

As far as upstream goes, the growth here is about as certain as is possible. To keep that growth coming, Exxon Mobil handles the "paperwork, execution, and submissions" for the partnership generally for 3 projects at any one time. Once the partnership has an operating FPSO, those type of requirements drop to routine functions.

That means with Payara beginning operations soon, the next two shown above and one new one are going through the process of getting to the production stage at any given time. Exxon Mobil is one of the best in the business. So what would be an issue for many operators, Exxon Mobil has reduced from a typical 10-year process to a 3-year process (per John Hess, CEO, Hess Corporation).

This has enabled the construction of the first four ships to be bid on and of course built at a time when the industry hit a cyclical rock bottom. John Hess, CEO, Hess Corporation mentioned how this saved the partners billions while making the partnership a lot of money sooner rather than later. The usual 10-year cycle would not have allowed for anything close to that bargain situation.

More importantly, the partnership obtained the leases at a time when no one knew where any oil was. From here on in, the value of those leases will only climb from the small amount paid to engage in risky exploration before the first discovery.

The upside here is that management has discussed the TotalEnergies ( TTE ) discovery several times on a neighboring lease block in Suriname. Once that discovery is evaluated for commercial use, Hess (and that partnership) may have another block to develop. Hess also holds additional neighboring blocks in Guyana with various partners. This discovery is a game changer for Hess. The considerable upside potential provides an enormous potential future return.

Hess is a relatively small player in the large project offshore game. Management rolled the dice and came up a winner with a solid line of sight growth for the foreseeable future.

Baytex Energy

Baytex Energy ( BTE ) is a Canadian company that reports in Canadian dollars. Recently the company acquired Ranger Oil ( ROCC ) to increase the company exposure to the Eagle Ford (which now brings in the majority of cash flow). Management has many times reported that the Eagle Ford breakeven in the low $30's.

Before the acquisition, the owned Eagle Ford acreage was operated by Marathon Oil ( MRO ). Marathon has an excellent operator reputation. The operator has led the basin in low cost production for some time.

The disadvantage of this was that Baytex did not control the development of the acreage as it was a passive investor. Therefore the property probably had a discounted value in the eyes of the market

That made the acquisition of Ranger Corporation so important. Now management has acreage it fully controls as an upstream player and Ranger management has access to the Marathon operated acreage information because Baytex is a partner in that non-operated acreage. Expect this acquired acreage to have a performance increase.

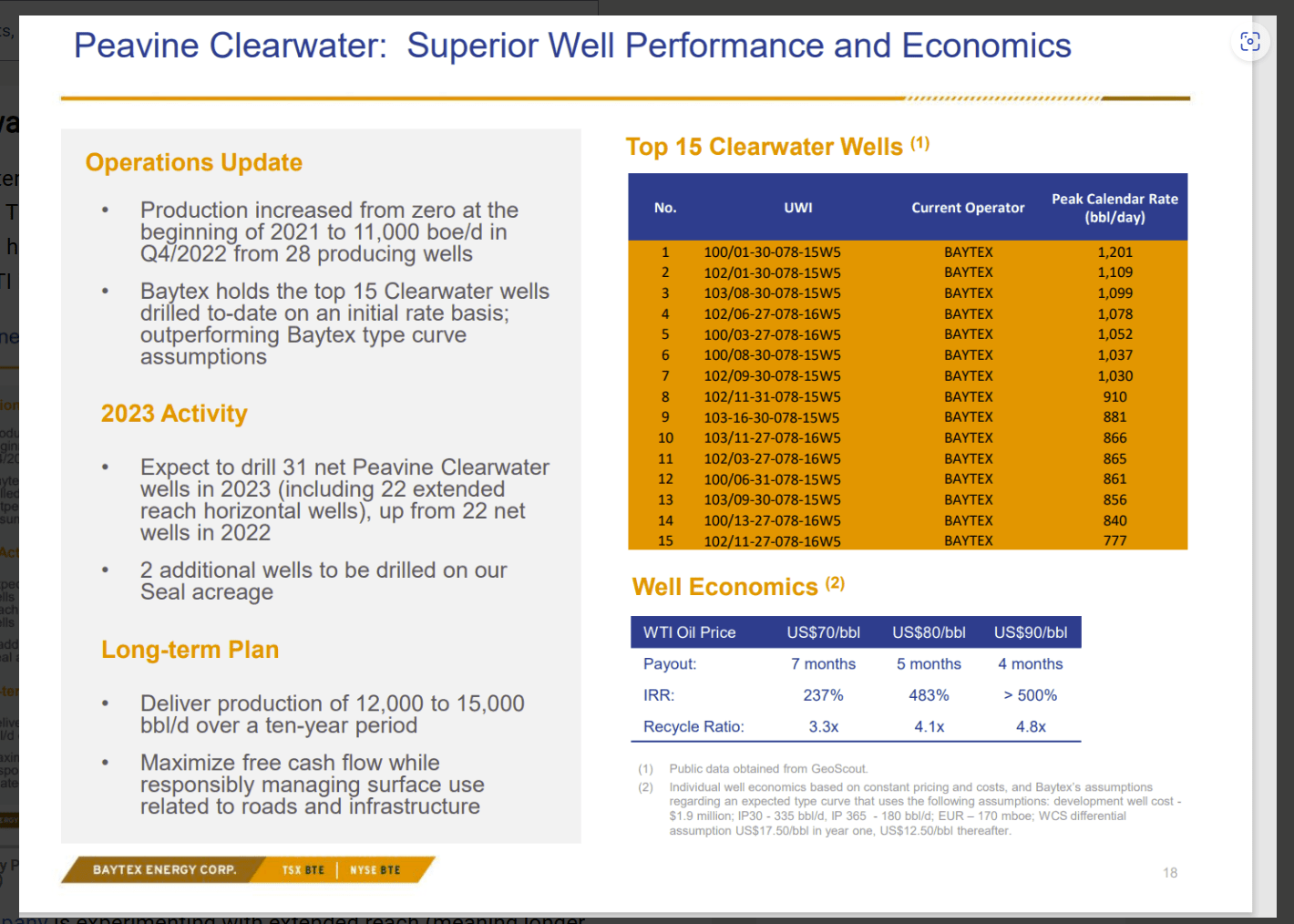

Baytex Energy Presentation Of Clearwater Profitability Characteristics (Baytex Energy Corporate Presentation March 2023)

{kind=link}

More importantly, the additional light oil cash flow gives the company the opportunity to safety develop the Clearwater discovery. This heavy oil discovery breaks even at a good $10 below any other heavy oil discoveries. It may be the lowest cost play in North America at the current time. Development of this discovery is just beginning and Baytex has a lot of acreage to develop.

Light oil cash flow holds up much better than heavy oil at the bottom of the market. On the other hand, during times like these, heavy oil plays are often more profitable. Therefore, the light oil production serves as a cash flow source during times of weak pricing when the heavy oil discount may well expand.

Management has mentioned that the Clearwater play acreage breaks even in the WTI $20's which is highly unusual in upstream. But that assumes a discount that may not hold during cyclical downturns. There is a chance that Clearwater will not have to be shut-in at business cycle bottoms due to the low breakeven. But that has yet to be fully determined.

This stock has considerable upside potential from the Clearwater discovery as well as the Eagle Ford acquisition.

Key Ideas

The Callon Petroleum impairment charge is a huge red flag for investors. There is no reason for an impairment charge that is acceptable when oil prices are where they are at the current time. Acquiring more acreage in the Permian often means paying full price. The only thing that can happen now is for another basin to become the favorite and the value of this acreage to decline. Investors could break-even if the acreage remains in favor for the entire time of the investment.

Furthermore, investors should look for management that goes the extra mile to find those "out of the way places" that frequently perform as good or better than the known "hot spots". Both Baytex Energy and Hess Corporation fit that bill. Shareholders have benefitted as a result and there is probably a lot more benefits in the future for shareholders of both companies.

For further details see:

Callon Petroleum: Acquiring Its Way Into Mediocrity