CATC - Cambridge Bancorp: Probably Not The Right Time To Invest In It

2023-11-21 12:31:31 ET

Summary

- Cambridge Bancorp is 37% below its all-time high and has a dividend yield above the industry median.

- The bank's loan portfolio, particularly fixed-rate mortgages, has been negatively impacted by high interest rates and low demand.

- The securities portfolio has also suffered from investments made before the rate hike, resulting in unrealized losses and a reduction in equity.

Despite its recent rise, Cambridge Bancorp ( CATC ) is still 37% off its all-time high. Its dividend yield is 4.45%, above the industry median of 3.72%. At first glance this bank may seem like a buy, but there are a number of considerations to evaluate.

Loan portfolio

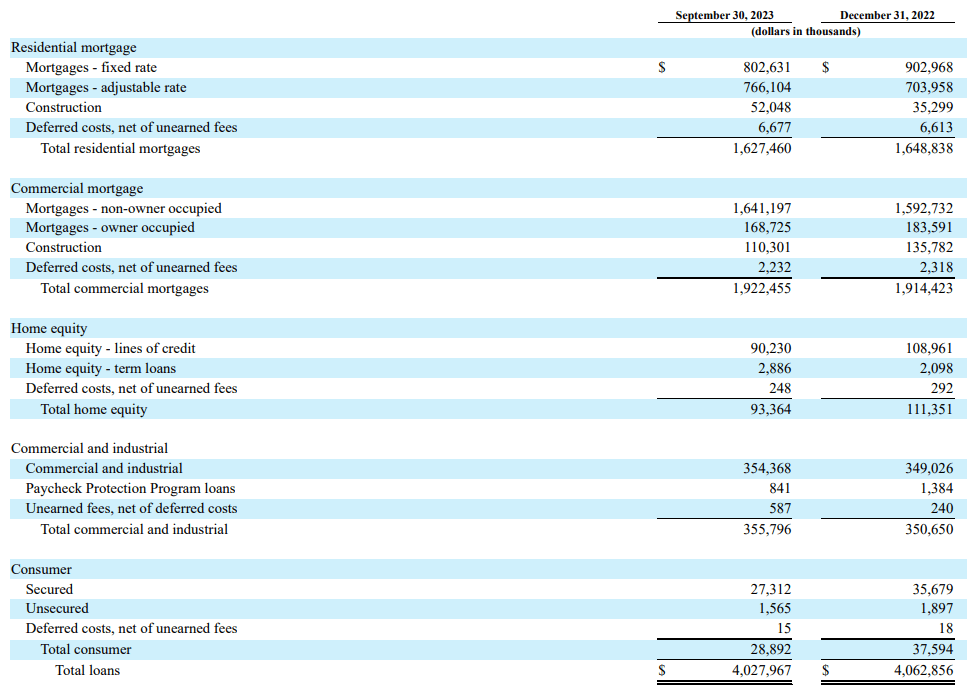

CATC's loan portfolio consists mainly of residential mortgage and commercial mortgage: together they make up 88% of the entire portfolio.

{kind=link}

Starting with the former, according to Q3 2023 , their total amounted to $1.67 billion, down 1.30% from the end of 2022. In particular, fixed rate mortgages are the ones that have taken the worst hit, in fact they have plummeted by 12.50% in nine months. This figure, while negative, is not surprising.

Interest rates are at 20-year highs and American households are waiting for better times to buy a new home to live in. Their choice is understandable, but this is a problem from the bank's perspective. Being able to provide fixed-rate mortgages at this time in history would be ideal for increasing profitability, especially when interest rates are reduced and the cost of bank funding is no longer the same. In any case, there is a lack of demand, and even if there were, the borrower's financial position should be assessed: we are no longer in the early 2000s where anyone can get a mortgage.

On the commercial mortgages side, growth here also appears to be rather stunted. As of today that segment amounts to $1.92 billion, only 0.40% more than at the end of 2022. In this case, it is owner-occupied mortgages that have fared the worst, declining 8% in nine months. Again, demand is not the same as it was when getting into debt was much cheaper.

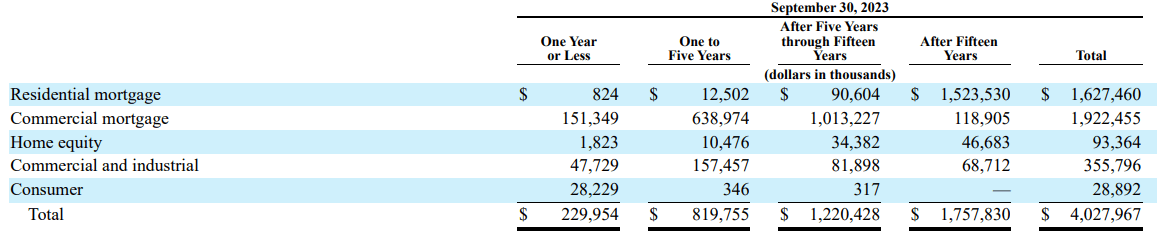

Regarding the loan portfolio, two important aspects to note are maturity and interest rate composition.

{kind=link}

Starting with the former, we can see that CATC has an asset structure very much focused toward the long term: loans with a minimum maturity of five years account for 74% of total loans, while those with a minimum maturity of 15 years are 44%. Notably, 94% of residential mortgages have a maturity of more than 15 years.

Given that loan growth has been stagnant since the Fed began raising rates, this means that the origination of almost all of CATC's long-term loans dates back to before monetary policy tightened. So, these loans were made at a rather low rate compared to what it could get now.

{kind=link}

56% of total loans are not fixed-rate, and this partially improved the situation during the Fed's rate hike, however, the problem remains. As of today, the Loan-to-Deposit ratio is not that high, 88%, so the bank still has room to improve the situation, but the demand to do so is lacking.

In conclusion, although loan yield is something that perhaps needed to be better managed, at least for now it seems that credit risk has been well balanced.

{kind=link}

Non-performing loans are up slightly from nine months ago but represent only 0.19% of gross loans, a minimal percentage.

Securities portfolio

The securities portfolio has the same problem as the loan portfolio: there were too many investments before the rate hike.

{kind=link}

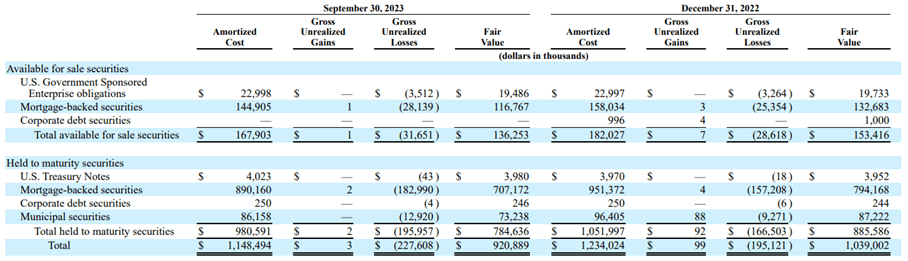

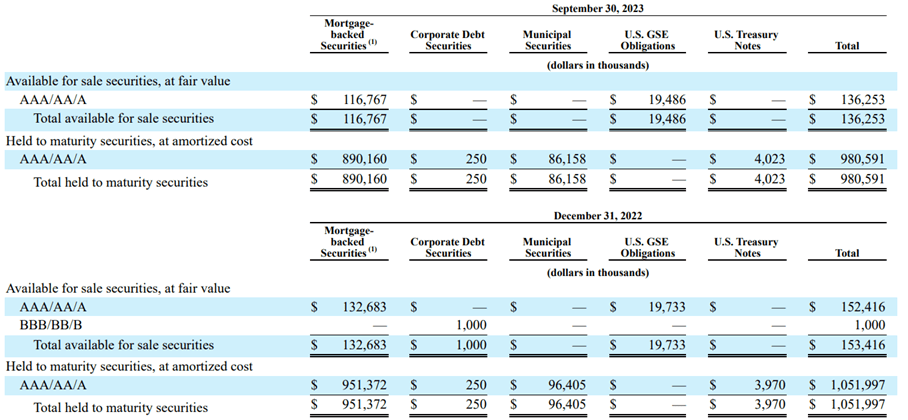

Available-for-sale securities amount to $167.90 million and have unrealized losses of $31.65 million. These have to be recorded at fair value on the balance sheet, and this is resulting in a reduction in equity.

As for securities held to maturity, they total $980.59 billion and have unrealized losses of $195.95 million. The latter, are not to be accounted for at fair value, so as long as there is no sale they will not adversely affect equity. In any case, it remains bad timing to invest large sums of money in these fixed-rate securities when real interest rates were close to 0%.

All unrealized losses amount to about $224 million, just over 40% of equity. CATC's good fortune was that most of the securities are held to maturity, otherwise the book value would have collapsed much more than it did, and consequently so would the price per share.

Today, money market rates are above 5%, while CATC's long-term locked rates are in many cases below 1.80%.

{kind=link}

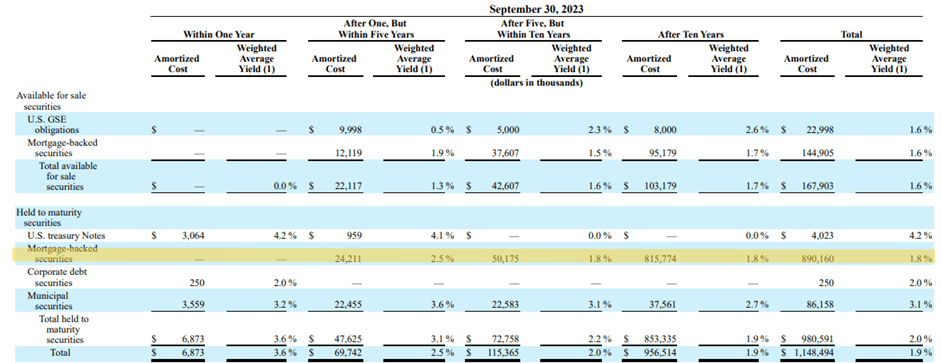

Weighing most heavily on unrealized losses are MBS with maturities over 10 years. The latter amount to $815.77 million and have a weighted average yield of only 1.80%.

Finally, just as with the loans, credit risk is minimal here as well. All securities have a minimum rating of A.

{kind=link}

Deposits and net interest margin

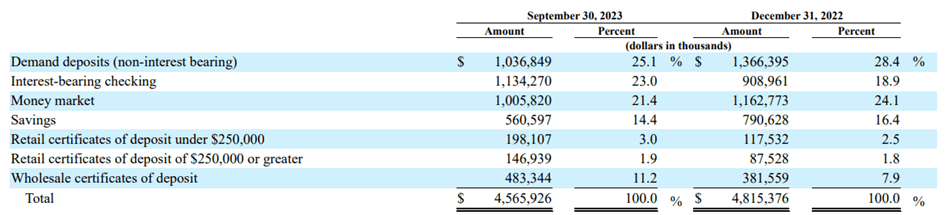

The composition of deposits has gradually deteriorated in recent quarters, in fact the cheaper ones have been replaced by retail CDs and wholesale CDs.

{kind=link}

Overall, CDs amounted to 12.20% of the total at the end of 2022, today they account for 16.10%. In contrast, demand deposits plus savings had a weight of 44.80% at the end of 2022, today they are down to 39.50%.

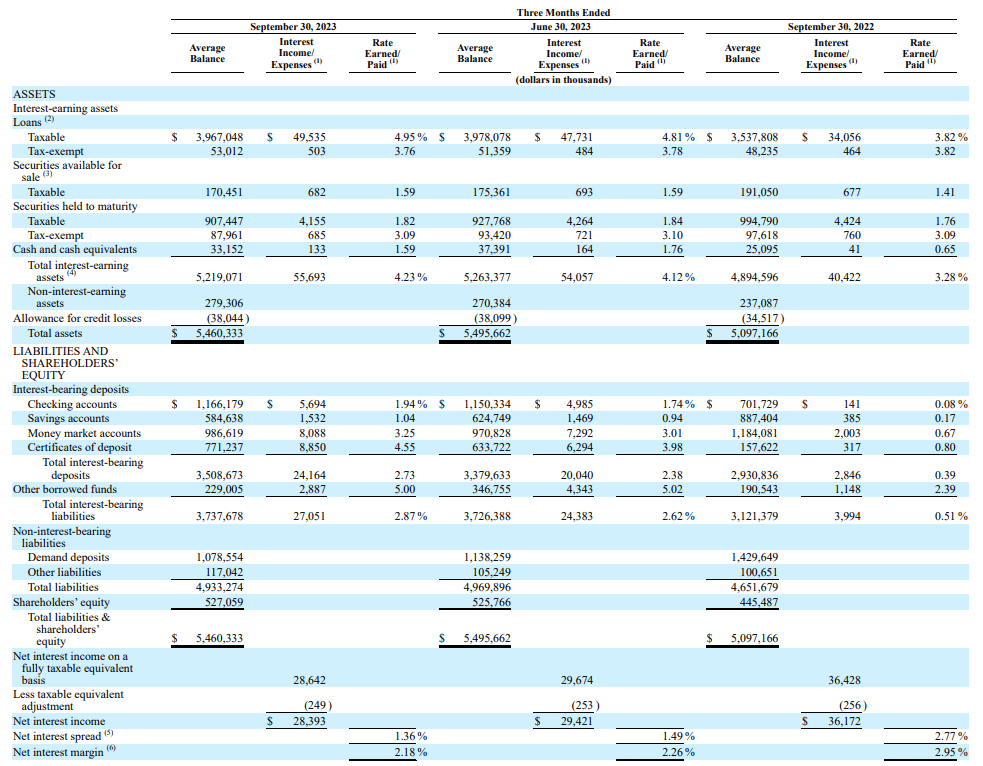

The different composition of deposits has obviously had effects on the net interest margin, now at 2.36% and down 8 basis points from the previous quarter and 77 basis points from last year.

{kind=link}

As we saw earlier, the yield on total interest-earning assets has improved too little relative to the increase in the Fed Funds Rate, while the cost of total deposits has increased much more. Compared with September 30, 2022, the yield on total interest-earning assets has increased by 95 basis points, while the cost of total deposits has increased by 234 basis points. As a result, the deterioration in profitability was inevitable.

{kind=link}

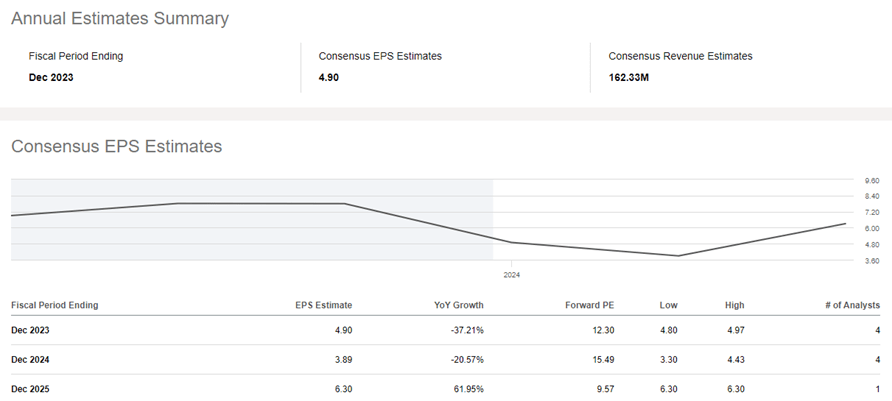

Finally, based on Street Estimates, we can expect the difficulties to continue until the end of 2024. From then on, the net interest margin should return to growth, thus leading EPS to grow again.

Dividends and valuation

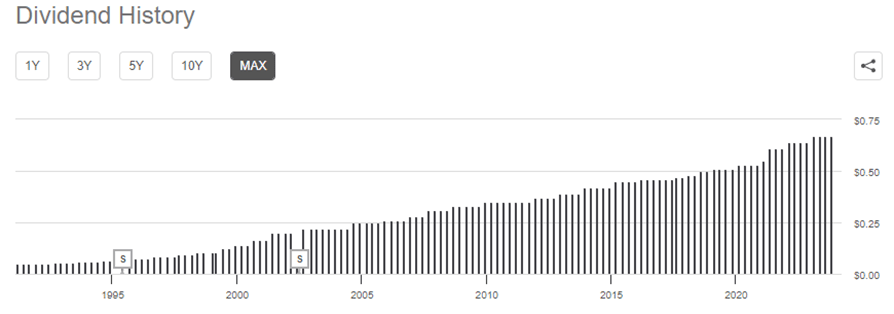

An interesting aspect of this bank is the dividends, in fact they have been increasing for 21 years in a row.

{kind=link}

This is an uncommon statistic among regional banks, in fact many of them cut or suspended their dividend for years during the 2008 crisis. CATC, on the other hand, has always kept their growth steady, so that is a point in its favor. However, dividend growth has been slightly subdued in recent years:

- Dividend Growth Rate 5Y ((CAGR)) was 6.46% versus 6.79% for the industry median.

- Dividend Growth Rate 10Y ((CAGR)) was 5.56% versus 7.89% for the industry median.

Yet despite this lower growth , the payout ratio is still higher than peers: 56.30% versus 35.95%. In its favor, however, it has a loan and securities portfolio with a high credit rating, thus less profitable but also less risky.

As for valuation, on paper CATC is undervalued. The 10-year average Price/Tangible Book Value per Share is 1.65x; multiplying this figure by the current Tangible Book Value per Share of $57.96, the fair value amounts to $95.63 per share. However, applying the same principle with 10-year average PE and EPS expected in 2024, the fair value amounts to $53.13.

Thus, CATC is undervalued on the basis of TBV but overvalued on the basis of EPS. Personally, at least for the time being, I prefer not to buy this bank.

Conclusion

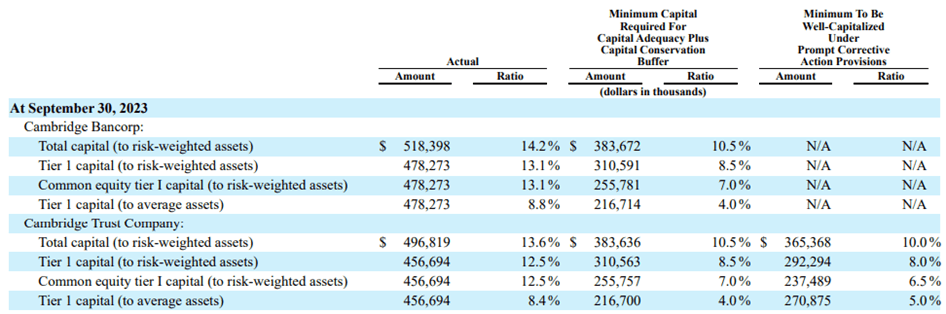

CATC is a bank that suffered greatly from the negative effect of the rate hike and its deteriorated net interest margin is evidence of this. In hindsight, it would have been better off investing less in fixed-rate securities when the Fed Funds Rate was very low. In any case, the bank remains well capitalized as evidenced by capital ratios.

{kind=link}

Although the dividend has been growing for 21 years, there are also downsides: growth appears rather slow even though the payout ratio is higher than peers.

Based on TBV this bank seems undervalued, but the EPS outlook prevents me from investing in it.

For further details see:

Cambridge Bancorp: Probably Not The Right Time To Invest In It