CCO:CC - Cameco: A Turnaround Is En Route

Summary

- Cameco is set for a turnaround, which is overlooked by many market participants.

- McArthur and Key Lake are back online after a prolonged standstill.

- Plans are being made to reroute Inkai's production to avoid Russian infrastructure and port reliance.

- The firm's joint acquisition of equipment supplier, Westinghouse, might add valuable cost synergies and improve Cameco's economies of scope.

- Uranium prices remain supportive, and an operational pivot could realign Cameco stock's valuation.

In September last year, we initiated a bearish call on Cameco Corporation ( CCJ ) on the premise that excess idiosyncratic risks would hinder the stock's prospects. The position yielded moderate gains of approximately 8% and 11% on an index-relative basis. However, our outlook on the company and its stock has changed, given a structural shift in the company's operational outlook.

We believe Cameco provides an excellent turnaround opportunity with commodity price advantages; here's why.

Operational Update

Prices Remain Supportive

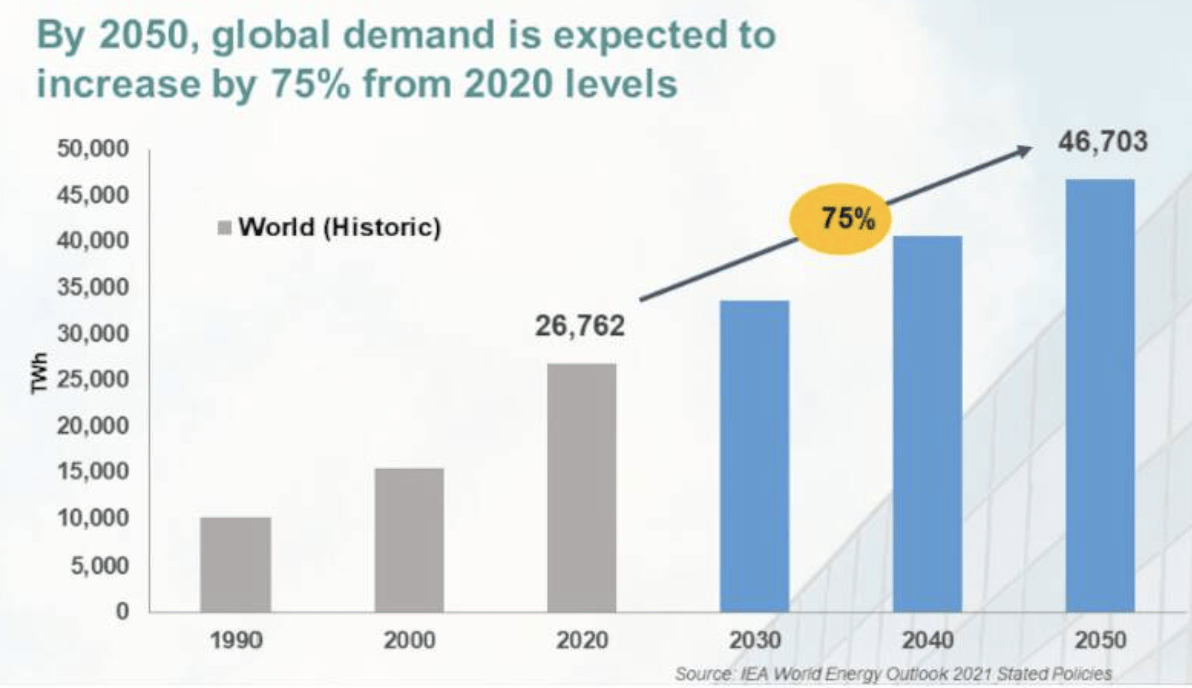

Despite a recent capitulation in various commodity prices, uranium remains resilient amid rising demand for nuclear energy (uranium is used as fuel to power nuclear energy) in Asia and Europe. Yes, uranium has retraced from its highs as the European energy crisis has eased, but the commodity's long-term growth trajectory remains intact.

According to the International Energy Agency, global energy demand is anticipated to skyrocket by 75% before 2050 as a growing population, and continued industrialization commences. Despite an existing fossil fuel infrastructure, the consensus is that politicians and big corporates alike are pivoting toward a zero-emissions landscape. Some include nuclear energy as a renewable source, and others do not since they consider it a 'risky' method of generating electricity. Thus, nuclear generation will likely be regional.

One nation that's fully committed to nuclear power is China. It is forecasted that nuclear will make up approximately 10% of China's energy mix by 2035, meaning six to eight power plants will need approval by 2025.

Furthermore, Europe and the United States generate more or less 25% and 20% of their energy from nuclear sources. However, the prior hosts anti-nuclear activists, which leaves the energy source's regional exposure on a knife's edge.

{kind=link}

It has been demonstrated that nuclear energy has growing regional demand. Therefore, we conclude that medium term prices will likely remain supportive, which could benefit Cameco for the foreseeable future.

Key Assets Back Online

Two of Cameco's key assets are back online after a four-year absence. Initially, McArthur River and Key Lake were offline due to weak demand in the uranium market. In addition, the Covid-19 pandemic restricted the firm's ability to regenerate the projects once price support surfaced.

Despite all their obstacles, the two assets are ready to rumble once again. McArthur and Key Lake already produced roughly 1.4 million pounds of Uranium concentrate in 2022. Moreover, the Company plans to produce 15 million pounds of uranium concentrate annually starting in 2024.

Despite McArthur and Key Lake's comeback, Cameco has warned that short-term costs will likely outweigh the benefits due to high restart rates that will be expensed upfront as they can't be amortized over time.

Westinghouse Acquisition & Inkai Update

Much optimism surrounds Cameco's recently constructed joint venture with Brookfield Renewable Partners (NYSE: BEP ). The pair have entered an agreement to acquire nuclear power equipment manufacturer Westinghouse for $7.9 billion. We think the deal adds an ancillary factor to Cameco's business model, which could 1) see the firm cut input costs, 2) onboard further expertise, and 3) develop economies of scope via a more diverse revenue stream.

According to our knowledge, U.S. GAAP allows Cameco to consolidate the acquisition's assets, liabilities, revenue, and expenses on its balance sheet under a JV agreement. Financial statement consolidation and operational synergies could provide investors with significant value; nevertheless, we concede that the concurrent $650 million share offering and $1 billion short-term bridge loan could dilute ordinary shareholders' residual value.

In some unwanted news, the Company's flagship Inkai mine in Kazakhstan still isn't yielding results due to the ongoing war between Russia and Ukraine. Although Inkai has produced and shipped, its inventory is stuck in transit as Cameco is trying to find a trading route solution to prevent it from using Russian ports and infrastructure.

It remains unclear when Inkai will yield results again. However, its shutdown is an abnormal event, and we believe that 'relief' adjustments can be made to the Cameco's long-term valuation.

Valuation & Dividends

At face value, Cameco's valuation seems underwhelming as its stock is trading at 2.88 times its book value and 105.74x the firm's earnings. However, investors need to consider that a variety of the company's assets have been at a standstill the past year. With McArthur and Key Lake back online, we see an improved valuation occurring around midyear. Furthermore, the addition of Westinghouse and potential solutions to Inkai could add substance to the Company's bottom-line performance.

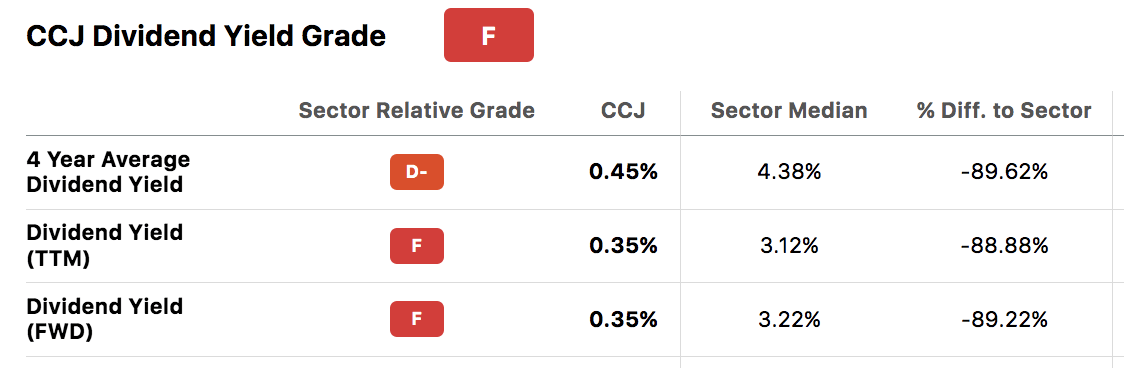

Cameco's dividend yield is underwhelming and has been that way during the past four years. Thus, investors are essentially betting on price returns. Whether Cameco's dividend increases in the next few years is beyond our scope; however, it will be no surprise if the company scraps its dividend to focus on short term restructurings.

{kind=link}

Concluding Thoughts

Cameco's stock is back in investable territory. The company has reactivated its McArthur and Key Lake assets, which could adjust its valuation outlook. In addition, plans are being made to establish new trade routes for Inkai, and a JV acquisition of Westinghouse could provide key synergies.

The stock remains grossly overvalued with an underwhelming dividend profile. However, we believe a turnaround is in motion.

For further details see:

Cameco: A Turnaround Is En Route