KMB - Cameco: One Of Few True Safe-Haven Stocks In Event Of Recession

2023-05-18 05:52:51 ET

Summary

- With more and more talk of a possible US and perhaps global recession on the horizon, the inevitable question that arises is where it might be safe to invest.

- Due to the nature of current recessionary pressures, ranging from geopolitical to financial uncertainty, classic defensive stocks, such as consumer staples are unlikely to work as a safe haven.

- Uranium miners could be that rare alternative, given the non-cyclical nature of uranium demand. Cameco is by far my favorite uranium mining stock, given its solid, well-established position within the industry.

Investment thesis

There is growing talk of an impending recession. It might be perhaps just certain countries that may experience it, or perhaps it could become a global one, which means that it is time to talk about safe haven investments. Generally, the sectors we automatically think about tend to be along the line of the consumer staples sector, as well as a few other potentially non-cyclical industries. Whenever the next recession will occur, most of the commonly held notions will fail, because this recession will differ from most recessions since WW2 in terms of causes, as well as consequences. Few industries will be unaffected, but uranium mining may be an exception. It is a non-cyclical commodity and Cameco ( CCJ ) is arguably the most solid, and least exposed company within the sector to a growing list of increasingly diverse risks. It is therefore my number one pick as a stock that I expect to hold up well within the context of an impending potential recession.

Cameco stock is expensive and its financial performance has not been overly impressive, but it can be expected to remain steady regardless of US, regional, or global economic trends

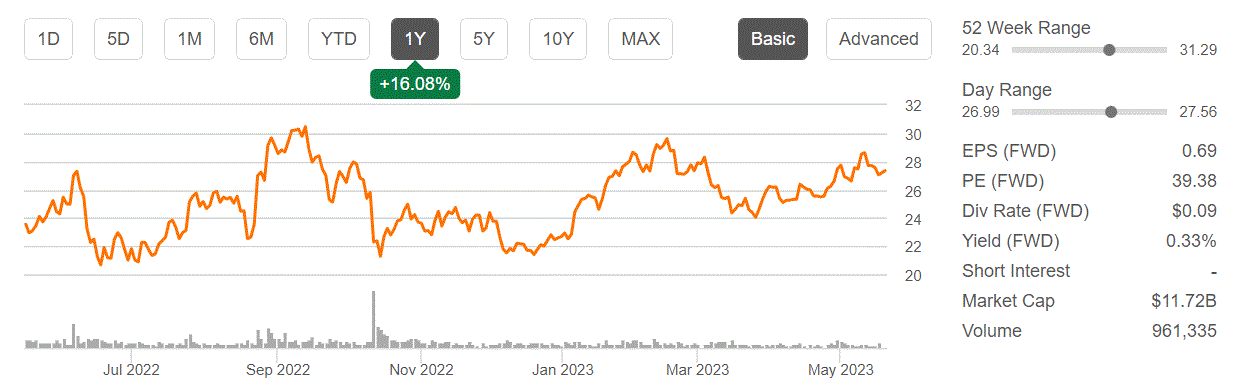

For the first quarter of this year, Cameco saw a decent increase in net income, which almost tripled from $40 million in the first three months of 2022, to $119 million now. Revenues increased by 73% for the same period to $687 million. The most important factor that impacted revenue growth was an increase in the sale of uranium from 5.9 million pounds in the first quarter of 2022, to 9.7 million pounds in the latest quarter.

Cameco's current forward P/E ratio is less than enticing, going at around 39.

{kind=link}

Its market cap of over $11.7 billion towers over its revenue levels which came in at just under $1.9 billion in 2022 . A market cap that is about six times higher than yearly revenues is generally not seen within the mining sector, or most other sectors for that matter, except for some companies that are expected to experience sustained exponential growth. Cameco does have the potential for revenue growth, on the back of a hypothetical rise in uranium prices going forward, and we may have seen some potential for stronger growth ahead based on Q1 results. It also has the reserves and facilities needed to further increase production.

{kind=link}

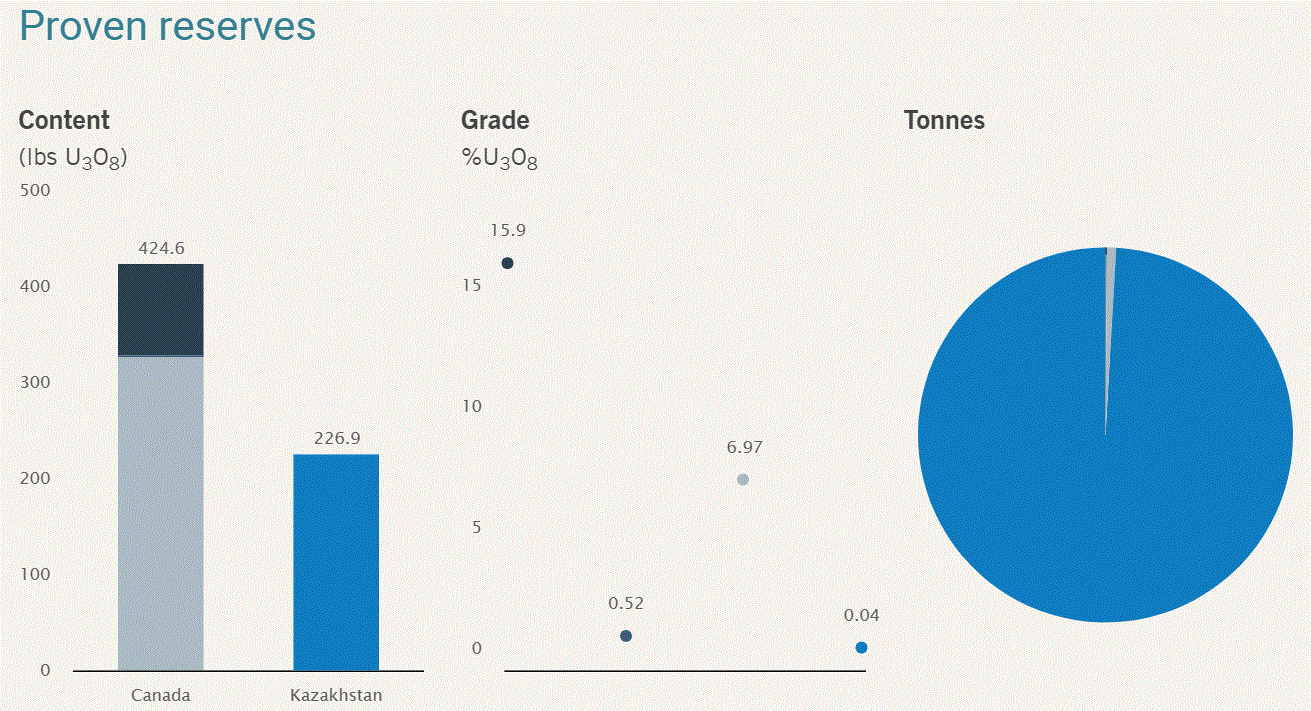

Based on its production rate of 4.5 million pounds in the first quarter, for an annualized rate of 18 million pounds, reserves should last Cameco for 36 years. Increasing production without further increasing reserves would shorten its reserve life significantly but whether through expanding its reserves from its existing base, or through future acquisitions, tapping new potential resources in the future through exploration, it can potentially increase production significantly without relying too heavily on drawing down its reserve life.

Its dividend is not exactly generous either, with about a third of a percentage point. What makes Cameco's stock highly prized more than anything is the theory that mined uranium demand is set to be in high demand by global utilities for the foreseeable future, regardless of whether the global economy will be booming or grinding to a halt. Nuclear power generation tends to be non-cyclical. In other words, utilities are more likely to shut in hydrocarbon-powered electricity generating capacity, than nuclear power plants.

Uranium demand looks set to remain strong for the foreseeable future, while mined supplies do not seem to be forthcoming at current uranium market prices

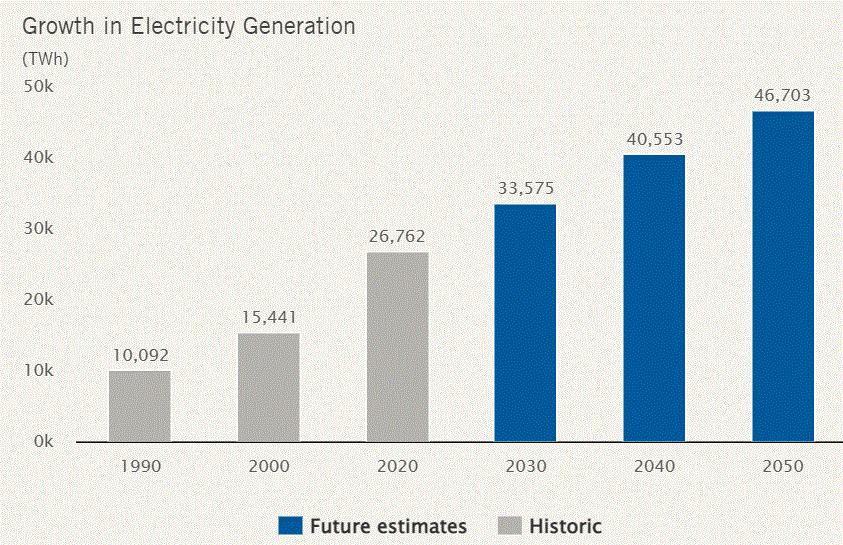

By Cameco's own expectations that are in turn based on IEA forecasts, between now and 2050, we can expect an increase in electricity demand of about 75% from current levels.

{kind=link}

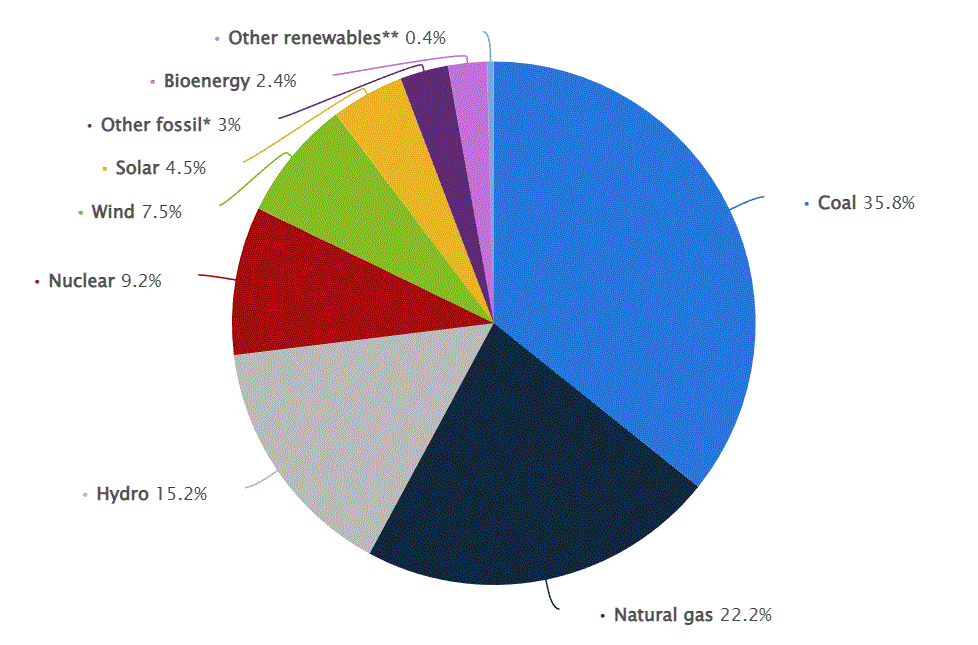

The massive increase in electricity demand is supposedly set to be covered even as the world greatly reduces its coal and natural gas demand, which are currently the number one and number two top sources of electricity generation, collectively providing about 58% of total power generation on the planet.

{kind=link}

Nuclear power will probably have to not only grow together with the global electricity-producing industry but significantly increase its market share if we are to have any chance to at the very least keep coal & natural gas generation from growing from current volumes. Going through the list of other potential candidates for generation growth, wind & solar are the only ones, but they come with shortcomings, such as their intermittent nature that makes it very hard to manage power grid flows.

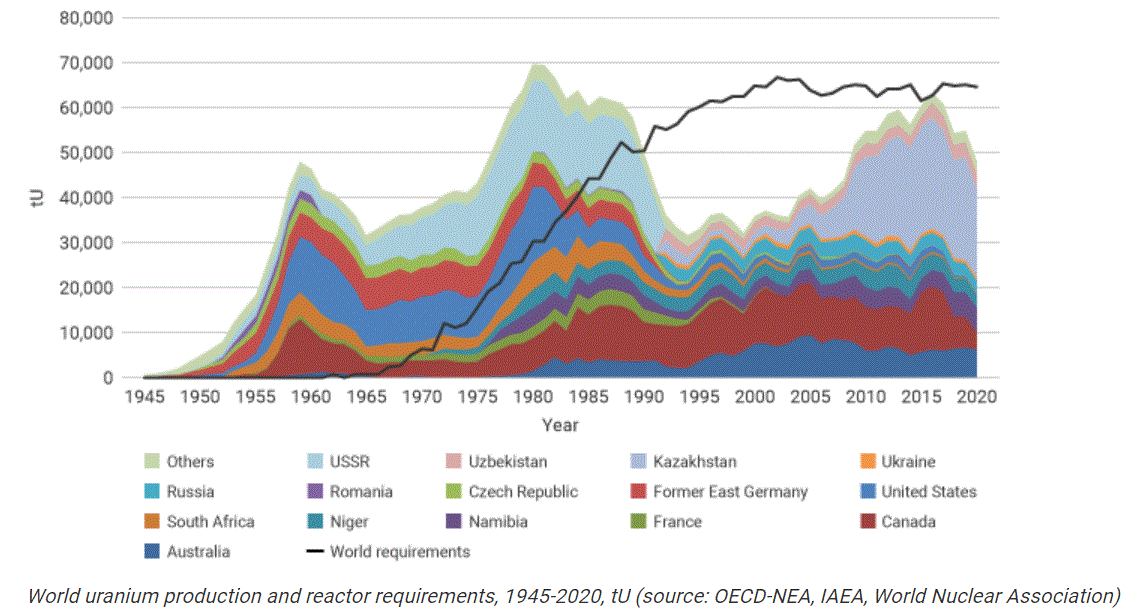

As far as the more immediate global mined supply/demand balance, when only looking at mined supplies, versus demand, there is a widening gap since 2015, mostly due to a drop in mined supplies.

{kind=link}

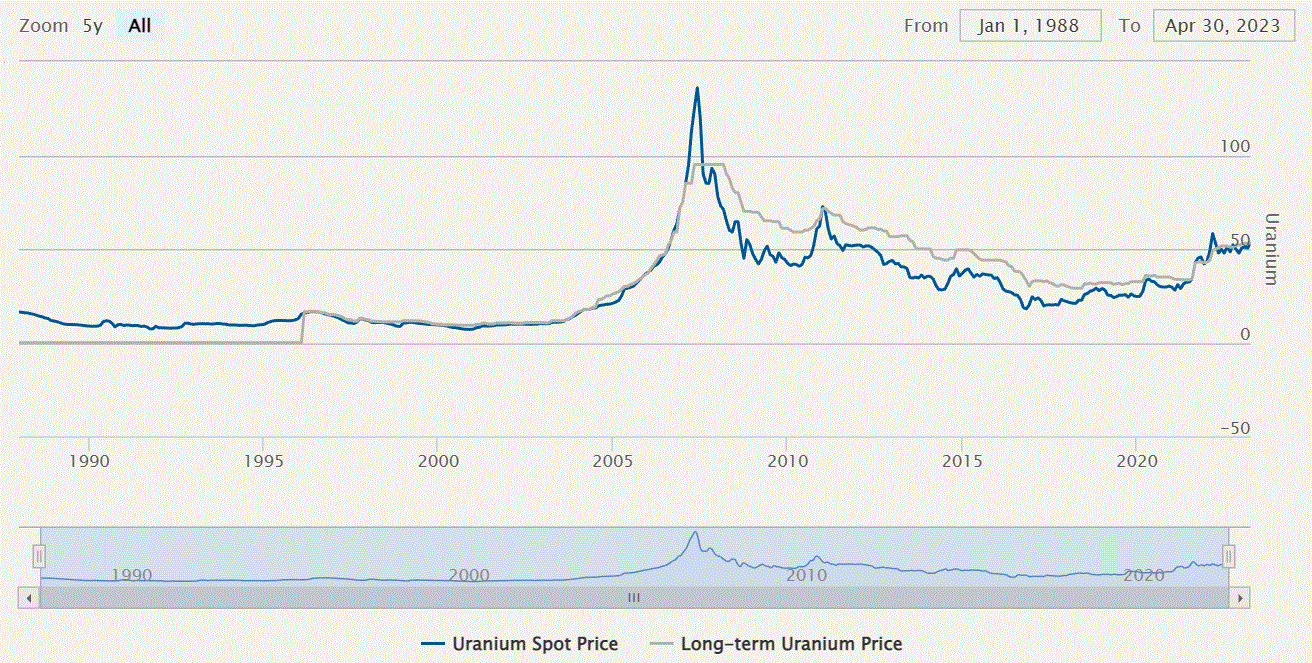

Clearly, we are not headed back to the uranium prices we saw in the middle of the last decade when uranium miners started reducing production in response to uranium prices that were perceived to be too low to justify capital spending. In other words, there seems to be a solid uranium market price floor emerging, which looks increasingly steady near current spot price levels.

{kind=link}

As we can see from its latest financial results, Cameco can thrive on current uranium prices. If prices will increase, it can respond by ramping up its operations, thus, between higher uranium prices and higher potential production, Cameco's revenues and profits could rise significantly from current levels.

Investment implications

With all the talk of an impending recession possibly caused by a number of potential factors, ranging from geopolitical risks to a much-feared banking crisis, Cameco's stock price is likely to ease further down in coming months, although nowhere near as much as the overall stock markets. The uranium market is non-cyclical, therefore a potential recession, regardless of its causes and its nature is unlikely to have much of an effect on uranium prices or on demand volumes. As long as uranium prices stay at current levels, there is very little sustained downside for Cameco's stock price, despite its relatively high P/E ratio, which is currently far above the overall market average.

On the other hand, there is a significant potential upside for its stock price, despite the already high valuation if uranium prices improve, which fundamentals suggest may be the case in the long term. There is potential for higher production that can be marketed at higher prices going forward. Eventually, there may be a crowding effect pushing its stock beyond what is fundamentally justified, as fewer and fewer safe haven investments are available to investors, in conjunction with good performance based on fundamentals. This could amplify Cameco's future stock price gains.

The potential for a crowding effect in Cameco stock may become increasingly apparent once we come to terms with the nature of the current global economic slowdown. It is mostly the result of geopolitical instability, which, unlike other previous recessions, it can disrupt the business of any company that in the past was seen as a traditional safe haven, such as consumer staples. I covered Kimberly-Clark ( KMB ) last fall, where I highlighted how the nature of risk today differs from what we saw in past economic downturns, where its supply chains can be severely disrupted, even if demand for its goods remains strong.

There are of course certain geopolitical scenarios where Cameco can also see its production facilities disrupted by events. The Inkai mine in Kazakhstan for instance, where Cameco has a 40% stake could be nationalized at some point on Kazakhstan's terms. Its production could be halted by internal unrest, similar to what we saw last year. There could be sanctions, disruptions to export logistics, or other factors that could potentially disrupt Cameco's mining and sale activities from the mine.

At the same time, Cameco's geopolitical risk exposure is arguably limited, given that it has a solid domestic mining base in Canada. The greatest domestic threat it may face is perhaps environmental policy overreach, where at some point, misguided government initiatives may harm Canada's mining sector. At the moment, however, any such risk factors do not seem to have an imminent or even high probability of occurrence.

Adding all factors together, Cameco is in my view the safest stock I own in my portfolio in the event of a recession, even though it may arguably seem overpriced. The market is probably putting a premium on this stock primarily because of the overall bullish uranium price and demand outlook. However, there is arguably also the non-cyclical nature of it that probably makes it attractive for segments of the investment community, within the context of an increasingly unstable investment environment. It may not pay as high of a dividend as typical safe havens, mostly within the consumer staples segment of the economy. But within the current context, Cameco seems safer, more shielded from the factors that make this decade a particularly treacherous one for investors to navigate through.

For further details see:

Cameco: One Of Few True Safe-Haven Stocks In Event Of Recession